Written by: Meng Yan, Solv Co-founder

From June 20 to 24, I was invited by the Monetary Authority of Singapore (MAS) to attend the first "Inclusive Fintech Forum" held in Kigali, the capital of Rwanda. I stayed in Singapore and Dubai for several days on the way there and back. It took a full two weeks, which just happened to be a semicircle along the northern edge of the Indo-Pacific region.

Before I went there, I had heard people analyze that the real economy application of blockchain, or the real opportunity of blockchain, is not in the United States, Europe or East Asia, but in Africa, the Middle East and Southeast Asia, which happens to be the Indian Ocean region, also known as the Indo-Pacific region. Although these analyses are also well-reasoned, for me, after all, they are hearsay, so I am still skeptical about this view.

As the saying goes, "Reading ten thousand books is not as good as traveling ten thousand miles." I personally took the trip and gained some intuitive feelings. I also thought more about the development prospects of blockchain in the Indo-Pacific region. Therefore, I would like to share my main views through this article. Of course, a short two-week trip, a glimpse of the past, is not enough to draw any profound conclusions. It is only for reference in the industry, and criticism and different opinions are also welcome.

1. Background

The reason why I was able to attend the "Inclusive Fintech Forum" this time was because Solv Protocol and our ecological partner incubated in Australia, Unizon Blockchain Technology (hereinafter referred to as UBT), were invited by MAS to sponsor and participate in the forum.

As a representative of Solv, I set out from Melbourne, Australia, passed through Singapore and Dubai, and arrived in Kigali, the capital of Rwanda, in the early morning of June 20.

During my stay in Kigali, I co-hosted a sub-forum on the application of ERC-3525 in the real-world asset (RWA) industry with UBT representatives Ms. Belle Lou and Mr. Chong Ren, delivered an exhibition speech, participated in two roundtable forums, and exchanged views with the Deputy Governor of the Central Bank of Rwanda, the Chief FinTech Officer of MAS, as well as central bank officials and entrepreneurs in the FinTech field from Ghana, Cambodia, Nigeria, Kenya and other countries. I visited the Rwanda Genocide Memorial and spent a day touring Rwanda’s Akagera National Park and walked around the country’s rural areas. It can be said that I gained a lot.

Opening Ceremony of the Inclusive Financial Technology Forum

The Inclusive FinTech Form is a government and industry summit initiated by Singapore's MAS. In my opinion, the main content is that financial officials, bankers and entrepreneurs from developing countries sit together to discuss how to provide financial services to small and medium-sized enterprises and ordinary people in these countries through financial technology innovation, helping them achieve rapid and sustainable economic development.

In addition to the host Rwanda and the organizer Singapore MAS, the participants mainly came from Southeast Asian and South Asian countries, such as India, the Philippines, Vietnam, Thailand, Indonesia, Malaysia, Cambodia, Bangladesh, and African countries, especially sub-Saharan African countries, such as Nigeria, Kenya, Tanzania, Zambia, Uganda, Ghana, South Africa, etc. Almost all of them were represented. The reason why this conference had such a pattern for the first time was mainly because of the brand appeal of Singapore and Rwanda.

As a late-developing country with a small land area and scarce resources, Singapore has grown into a high-income advanced economy in just a few decades. Its achievements in financial services, social governance, and technology industries have established a good image among developing countries in the Indo-Pacific region and become a role model for them to learn from. After the tragedy of the 1994 genocide, Rwanda rose from the ashes and became a model of social governance and economic development for sub-Saharan African countries in less than three decades. The governments of these two countries joining forces is indeed very attractive.

The conference attracted 2,500 participants from dozens of countries

2. Impressions of Rwanda

This conference is my first time to visit Africa, and the destination of my first trip to Africa is Rwanda, which I actually did not expect in advance. More than ten years ago, when I was at IBM, the company had proposed that I go on a business trip to Kenya to support the African expansion strategy, but it was not implemented in the end. At that time, I understood the basic situation of Africa and thought that if I went to Africa one day, I should go to a more "developed" region like Kenya or Nigeria. I never thought that my first visit to Africa would be to Rwanda.

Like most people, my only impression of Rwanda was the horrific genocide 29 years ago. The Rwandan genocide took place between April and July in 1994, but when the news about the genocide reached China, it was already July, so my memory of the genocide was linked to the World Cup in the United States that year. In my memory, the TV news program was still broadcasting the exciting scenes of the World Cup in the first minute, and the next minute was the tragic scene of the bodies of the victims in the genocide.

I remember that my biggest feeling about this news was not horror or sadness, but shock and disbelief. I felt that the 21st century was just around the corner, Maradona had taken doping, Baggio's penalty kicks were anti-aircraft guns, and the United States had built an information superhighway. How could there be a country in the world that was engaged in racist massacres? And more than a million people were killed in one go! It was simply unbelievable. What a barbaric and backward place this must be. Many years later, I watched the movie "Hotel Rwanda" and had a little understanding of the causes and consequences of the massacre, but I still didn't think I had any connection with Rwanda.

But before I went to Rwanda this time, I had heard many people tell me that Rwanda is the most successful country in Africa in the past two decades, known as the "Switzerland of Africa" or the "Singapore of Africa". But I checked Wikipedia, after all, it is a poor country with a per capita GDP of less than $1,000, how can it be compared with Switzerland and Singapore?

I spent four days in Rwanda, which was a huge shock to me. I initially understood why the outside world praised Rwanda. A comprehensive introduction to my impression of Rwanda would take thousands of words, so here I will just briefly introduce a few points in conjunction with the theme of this article.

Natural conditions: Rwanda covers an area of 27,000 square kilometers and is mountainous, known as the "Land of a Thousand Mountains". Our deepest impression of Rwanda's natural conditions is its excellent climate. Rwanda is close to the equator, but in summer, the temperature is only a dozen to twenty degrees, and the humidity is around 40. It is dry and cool, extremely comfortable, in sharp contrast to the humid Singapore and the hot Dubai. Moreover, Rwanda has only dry season and rainy season in a year. The dry season is generally dry and cool, while the rainy season is humid and warm. In terms of climate alone, it is indeed a very suitable area for human habitation. Of course, as far as we know, large areas of nearby Kenya, Uganda, and Tanzania have similar climate characteristics, which are completely inconsistent with our impression of the equatorial region. This may be due to the climate regulation effect of the huge nearby Lake Victoria.

Rwanda is located on the southwest side of Lake Victoria, the world's second largest freshwater lake, close to the equator.

Population: At the time of the Rwandan genocide, the country had a total population of 7 million. The three-month genocide killed more than 1 million people and another 1 million became refugees. The country lost more than 2 million people in just a few months. However, with the end of the war, national reconciliation, political stability, and economic development, Rwanda's population has increased rapidly in the past 29 years and has become a major destination for immigrants from neighboring countries. It now has a population of 13 million.

The genocide was a brutal act committed by the Hutu against the Tutsi. After the genocide, the Rwandan government no longer allowed the distinction between the Hutu and Tutsi. Everyone was a unified Rwandan nation. In terms of appearance, Rwandans do have some characteristics. There are many tall people, and it is not uncommon for men to be over 190cm tall. They have slender and handsome figures, three-dimensional facial features, and lighter skin than southern Africans. There are many beautiful women and handsome men.

Photos of some of the victims at the Kigali Genocide Memorial

Economy and infrastructure: Rwanda is a landlocked mountainous country with scarce resources. Its main specialties are coffee and tea. Its per capita GDP is more than 900 US dollars, which is roughly equivalent to the level of my country in 2000. However, in fact, the living standards and infrastructure conditions are equivalent to our situation in the early 1990s. The road quality is good, but too narrow. It is often a two-way two-lane road. A slow car can block the car behind for half a day. During my stay in Rwanda, I encountered a power outage. I don’t know if it is occasional or normal. The living conditions of urban residents are roughly equivalent to those of my country’s fourth- and fifth-tier cities and towns, and many mud houses can still be seen in rural areas. However, the government has launched a plan to build and provide free housing for all poor people, and the conditions are quite good. Basic medical insurance is universal for all people. There are many cars, and the brands are not bad, but the oil quality is poor. The air is full of choking exhaust smell, which makes me feel like I’m back in the early 1990s.

Kigali CBD, the capital of Rwanda

Free housing built by the Rwandan government for the poor (under construction)

Security and civilization: Compared with Rwanda's economic level, its security and civilization have reached a surprisingly high level. The security is very good, and a foreigner walking alone on the road at night does not have to worry about safety. People are generally warm, friendly and polite. When we stopped by the roadside and prepared to cross the road, all kinds of vehicles on the road would stop and wait, and children would wave enthusiastically when they saw foreigners. Of course, we also noticed that Rwanda has a large number of military and police patrolling the streets with live ammunition. Obviously, this kind of security is the result of the government's active governance. It is said that Rwanda's security has become its national business card, a unique advantage that neighboring countries do not have.

Political situation: Paul Kagame, the current president of Rwanda, is a hero who led the Rwandan Patriotic Front back from overseas in 1994, overthrew the interim government that committed genocide, and saved the people from suffering. He first served as vice president in the new government, and became president in 2000. He has been in power for 23 consecutive years. According to the Rwandan Constitution, he can stay in power until at least 2034. Under Kagame's rule, Rwanda has a stable political situation, rapid economic development, rapid population growth, and continuous strengthening of social security. Not only has the problem of food and clothing been solved, but also medical insurance has been popularized, and housing problems are being solved for all people. Therefore, President Kagame has extremely high support among the people.

A photo of President Paul Kagame hangs on the wall of a travel agency

Language: Rwandans are multilingual. In addition to the local language, many people can speak French, English and Swahili. English and French are compulsory courses in school. Because they were colonized by Belgium for a long time, French is the first choice of foreign language for Rwandans. Therefore, their English pronunciation is generally not standard, with a strong French accent. However, they are very fluent in expression and can use more advanced vocabulary and sentence patterns freely. Once we are familiar with their accent, we can communicate with them in English more smoothly.

Media, communications and financial infrastructure: Rwandan households do not yet have televisions, and desktop computers are even rarer, but almost every adult has a smartphone. The most popular mobile phone in the country is Techno, the African brand of Chinese mobile phone manufacturer Transsion, followed by Samsung.

Apple iPhones are used only by a few rich people. The currency is the Rwandan franc, which is exchanged at 1160 to 1 US dollar and depreciates by a few points almost every year.

In terms of payment, cash is still the main payment method, followed by mobile phone payment. If you can only pay by card, you may encounter payment difficulties in many places. ATM machines can be found, but their popularity needs to be improved.

The most popular mobile payment brand in the country is MoMo, but there are also some competitors, such as BK launched by the Bank of Kigali. M-Pesa, a well-known mobile payment system in Kenya, is also very popular in Rwanda. The country is basically covered by 4G network, and many public places provide free WIFI. According to our personal experience, the network speed is good.

Mobile payment app advertisement on the streets of Kigali

The above are some of my impressions of Rwanda. Although they may seem irrelevant to the topic, understanding its social background is actually very necessary to understand my main points below. Of course, because the time is too short, it is inevitable that there are biases and fallacies. I hope that friends who know more about the situation can point them out.

3. Jump into blockchain in one step

To be honest, before the conference, I thought that the blockchain-based ERC-3525 digital bill technology we brought might be a bit ahead of the times for these Indo-Pacific countries. I thought they should popularize electronic payments first. But what I didn’t expect was that our proposal received a warm response.

During this conference, I introduced to the audience the digital invoice pilot project we developed for the Australian central bank's CBDC. A Rwandan entrepreneur raised his hand and said, this is what we need in Africa. A technology VC from Nigeria directly asked to establish contact with us to discuss investment intentions.

Officials from the Central Bank of Ghana, a West African country, asked me if ERC-3525 technology could help African countries solve the problem of interoperability of central bank digital currencies. A representative from the Science and Technology Innovation Department of the Central Bank of Cambodia also invited us to discuss with them how to apply ERC-3525 technology in cross-border supply chains. All these surprised me and also aroused my strong interest: Why do Indo-Pacific countries favor this cutting-edge technology so much?

I discussed this with several newly interpreted African friends and Singaporean friends who are more familiar with the Indo-Pacific market, and came to a very important conclusion, that is, the latecomer countries in Southeast Asia and Africa are not satisfied with "making up for lost time" in the construction of digital economic infrastructure. They do not want to repeat the path taken by the United States and China, but hope to jump directly into the 3.0 era in one step, that is, the digital economy based on blockchain.

Why do they generally have such a mentality?

If we regard the electronic payment system pioneered by the United States, based on POS machines, credit cards, and interbank clearing and settlement networks as digital finance 1.0, and the mobile Internet payment system that has flourished in China as digital finance 2.0, then we can say that the general state of Indo-Pacific countries is that both 1.0 and 2.0 are at a very early stage. As I mentioned when introducing Rwanda's network and financial infrastructure, many of their stores do not have POS machines, bank cards are not popular, and payments are mainly made in cash. How should we move forward?

Obviously, they do not intend to spend precious funds on "making up lessons" for 1.0, because most of these countries do not have sufficient economic scale and banking system, and do not want to waste funds on laying POS and ATM machines. This is understandable to most people.

At the same time, although the centralized mobile payment system, also known as Digital Finance 2.0, is already very mature, there are still some problems that make these countries hesitant.

First, the centralized Internet payment system naturally has a tendency to monopolize data. The operating center of this system can snoop, use and control the private data of all users at will, thereby easily obtaining the main operating information of an economy. In this case, these Indo-Pacific countries obviously do not want a centralized payment system operated by foreign companies to monopolize their domestic market. Therefore, they generally hope to support their own centralized payment system.

Secondly, the fragmented Internet payment system with many mountains and hills brings huge integration friction and reduces the efficiency of regional cooperation. In Africa and Southeast Asian countries, regional economic cooperation is very active. In Rwanda, the Africans I met, whether from Rwanda, Nigeria, Kenya or Ghana, always mentioned Africa. Therefore, they have very high requirements for the interconnection and interoperability of payment and financial systems between each other. During the entire forum, all topics and sessions involving the interoperability of financial systems have the largest number of participants, the most crowded venues, the most active speeches, and the most heated discussions, which shows how much they value it. However, among these dozens of countries, except for a few countries with a population of over 100 million, the vast majority are low-income economies with a population of tens of millions. Each country has several mini Alipays of its own, adding up to hundreds of payment companies, which is not only redundant and wasteful, but also each one cannot grow up, cannot form a scale effect, and is not conducive to the deep development of digital finance.

In addition, hundreds of fragmented mini Alipay accounts will generate huge reconciliation friction, which will have a great impact on the efficiency and trust of collaboration. In addition, this flexible and efficient centralized payment system poses severe challenges to financial and data privacy supervision, which have not been solved in developed countries, let alone for Indo-Pacific countries to solve independently.

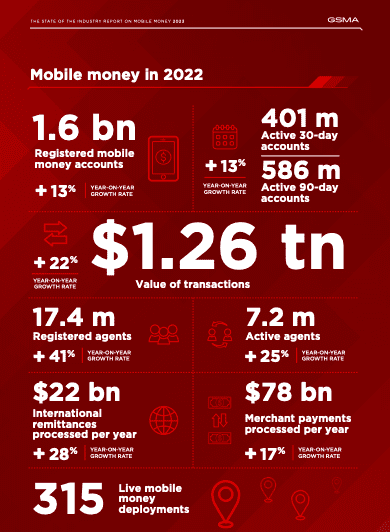

Africa's mobile payment market in 2022: 586 million active users, divided into pieces by nearly 200 payment companies

Of course, Internet payment is a convenient, fast and relatively mature technology, so these countries are still positive about it. However, when blockchain gradually reveals its technical advantages and application prospects, Indo-Pacific countries are indeed more enthusiastic about blockchain-based digital financial systems than other regions. Through communication with them, I have summarized four advantages of blockchain that they value:

First, blockchain balances the needs of these regions to collaborate in the digital economy while protecting privacy and data sovereignty. We know that in a centralized system, privacy and data sovereignty are inevitably controlled by the operators of the core platform because the centralized system indiscriminately hands over the operation rights of the infrastructure and the ownership of the data to the platform operators. If users want convenience and network effects, they have to cede their data sovereignty to the platform. For the platform, all regulatory measures can only make demands and shout slogans, and there are no substantive and effective technical regulatory measures. In the blockchain, the operation rights are separated from the data sovereignty. The operation rights of the infrastructure are dispersed in the hands of various nodes, while the data sovereignty is controlled by the users themselves through cryptographic mechanisms. There is no problem of the platform operator usurping the data sovereignty. At the same time, the data on the blockchain is tamper-proof and can be verified by a third party, so it is easy to gain trust. Trust is the basis of collaboration, so the blockchain can promote collaboration while protecting data sovereignty and privacy, achieving an ideal balance, which is particularly in line with the needs of regional economic cooperation among Indo-Pacific countries.

Secondly, the open and trusting environment of blockchain and the automatic execution mechanism of smart contracts can help solve the problem of interoperability of digital financial systems in different countries. Each country can issue its own digital currency, digital certificates and digital assets on the blockchain. Due to the inherent trust transmission mechanism of the blockchain and the degree of data standardization, the difficulty and complexity of integrating these systems is much lower than integrating traditional centralized systems, and a very high degree of automation can be achieved. During this forum, we suggested to the central bank of a certain country to use a mechanism similar to Curve to complete the automatic exchange between multiple currencies. We even envisioned interesting applications of flash loans in certain scenarios.

Third, blockchain makes currency programming a daily tool. Since the cryptographic security model of blockchain systems is simpler and more complete than that of centralized systems, it can be extremely open. Some operations that require layers of authorization and strict checks in centralized systems can be directly released to ordinary users on blockchains. Currency programming is an example. China's Internet payment has been around for so long, and the functions that really dare to be released to users, such as "grabbing red envelopes" and "group payment collection", have to be launched by the platform with great caution. Users themselves do not have the ability to program payments. Blockchain allows anyone to program currency and payments through smart contracts. This openness is unmatched by Internet payments and is also a very attractive capability for Indo-Pacific countries. When the audience saw the ERC-3525 automatic share calculation, automatic account division, payment status refresh UI, and setting payment limits and time that we demonstrated, they were very excited and hoped to be able to perform more customized programming and control of assets and currency flows on this basis.

Fourth, blockchain can support the establishment of new regulatory mechanisms. In a centralized financial technology system, since regulators cannot directly implement supervision at the system level, all regulatory rules are some kind of gentleman's agreement. The only means of supervision are fixed-point spot checks, which are not only costly and slow to respond, but also very ineffective. Many people complain that the financial supervision of developed countries now controls decent innovators to death, but when they really encounter a reckless giant, they are at a loss and do nothing, which is a complete pain for the enemy. In the blockchain, once a trusted digital identity, digital account, and digital certificate system is established, regulators can implement substantial control through smart contract codes. Whether it is legislative prevention beforehand, adjustment and response during the event, or evidence collection and execution after the event, the efficiency is at least two orders of magnitude higher than today's regulatory technology. Therefore, digital accounts and digital certificates have also become hot topics in this forum. I communicated with a Nigerian FinTech expert and asked him about his views on the issuance of Nigeria's central bank digital currency. He said that the main significance of the central bank's digital currency is not payment. Those who question the value of blockchain by citing payment efficiency every day have a narrow vision. The key point is that the popularization of the central bank's digital currency will prompt every enterprise and individual to establish a digital identity and digital account and use a digital wallet. This is the most important public infrastructure for the next generation of digital economy and financial supervision. I agree with this view.

It can be seen that there is a real logic behind these countries' interest in blockchain. In comparison, large countries and highly integrated economies like China and the United States are dragged down by user habits and existing systems. For a period of time, they may indeed have a heavy burden and insufficient motivation for the full adoption of blockchain. However, the late-developing countries in the Indo-Pacific region are lightly equipped and eager to leapfrog development, skipping 1.0 and 2.0, and directly constructing a future-oriented, cross-border digital economic infrastructure based on blockchain.

4. Conditional Analysis

The interest is real, but can it be done? We still need to analyze the conditions of this market.

First, the market has a strong demand for cross-border integration. A single large market will repeatedly struggle between centralized systems and blockchain systems. Regions with strong cross-border demand have a clearer demand for decentralized infrastructure such as blockchain. The Indo-Pacific region certainly meets this requirement, especially ASEAN, the Middle East Arab countries, and Africa, which are all politically fragmented and economically integrated regions, providing a natural breeding ground for the development of blockchain.

Secondly, there is a strong awareness of data sovereignty. If a country is willing to hand over its data sovereignty to another country's centralized platform, then there is no need to use blockchain. However, with the rise of awareness of data sovereignty and privacy protection in countries around the world in recent years, such countries should be fewer and fewer. Even in low-income countries in Africa, governments are no longer willing to accept their digital economy being controlled by foreign entities. This also enhances the attractiveness of blockchain to this region.

Third, the infrastructure is up to standard, especially the Internet and mobile Internet infrastructure. This is also basically met by the countries around the Indian Ocean. According to friends who are familiar with the situation in Africa, with the support of China, the telecommunications and Internet infrastructure in African countries has developed by leaps and bounds in the past few years. Now more than 80% of adults have mobile phones, and nearly 600 million people have opened mobile payment accounts, which meet the basic conditions for blockchain.

Fourth, economic development has put forward an urgent demand for digital financial infrastructure. This is also in line with the reality of the Indo-Pacific region. With the reconstruction of the global supply chain, the Indian Ocean Rim has increasingly become an active region for economic development covering the entire chain from raw materials to production and manufacturing. On the other hand, the more than three billion people in the region are mainly in low- and middle-income countries. In recent years, economic development has begun to accelerate and may enter a period of high-speed economic growth driven by trade and regional cooperation. This undoubtedly puts forward requirements for the development of digital finance, which is also conducive to the development of blockchain in this region.

From these four points of view, the Indo-Pacific region is very conducive to the development of the blockchain industry. Therefore, it should be said that this region is likely to develop into an important market for the blockchain industry in the next few years, and even lead the development of blockchain in some aspects.

Of course, they also have obvious disadvantages, mainly because the infrastructure is still weak, and many poor people cannot use smartphones or connect to the Internet. Another disadvantage is the extreme shortage of relevant talents, and they basically have no ability to develop relevant systems themselves, so they need to introduce them from outside.

5. Singapore’s strategy

Where there is demand, there will be supply. The above analysis was seen by one institution very early on, and that is of course the Monetary Authority of Singapore. Recently, the Monetary Authority of Singapore has released a series of projects and white papers, which are obviously aimed at cross-border blockchain infrastructure. There are three main plans:

The first is Project Guardian, a cross-border digital asset network composed of multiple blockchains and traditional centralized networks, which serves as the infrastructure of the entire system.

The second one is Project Orchid, which is Purpose Bound Money, a programmable digital currency. I have introduced this technology twice in the past few days. I think it is a very important technology. MAS promotes this PBM mainly to provide a new technical framework for the supervision of currency payments while maintaining several important properties of currency.

The third is digital certificate projects such as Project Savanah, which aims to reliably express and confirm the identity, account, qualifications, transaction records, etc. of the user subject.

The latter two projects are actually to solve the problem of supervision. In fact, the long-term failure of industrial blockchain is not due to too many restrictions, lack of hype, and lack of speculation as many people say. The fundamental reasons are two: accounts are not on the chain, and funds are not on the chain. Once these two problems are solved, all kinds of enterprises and individuals will flock to it. In order for the government to guide enterprises and individuals to go on the chain with confidence, and for traditional institutions to move assets, funds, and businesses to the chain with confidence, the problem of regulatory compliance must be solved first. Because in the modern mainstream economy, anti-money laundering, anti-terrorist financing, and the implementation of economic and financial sanctions are all unavoidable needs, which can also be said to be the biggest difference between crypto infrastructure and industrial blockchain. If these two plans of MAS can be promoted, on the one hand, the ability to manage accounts is established, and on the other hand, the ability to manage money is established, basically the shortcomings of industrial blockchain will be made up, and there will be hope to achieve account and fund on the chain.

This whole set of plans by MAS is obviously not designed for itself. Singapore has a population of 6 million, but the scale and scale of this plan is based on a billion people. I think Singapore has learned from the lessons of repeated failures in the past decade of industrial blockchain and has taken the lead in formulating a step-by-step, methodical and structured blockchain and digital economic infrastructure development strategy for the Indo-Pacific region.

I can't help but think that if China can implement a similar strategy in 2019 with the help of policies, and the government takes the lead in orderly building infrastructure, account systems, programmable currencies and regulatory technology frameworks, China's industrial blockchain applications may have taken shape and can be exported. For infrastructure at the level of the Internet and industrial blockchain, the government's strategy and support can still play a positive role in the construction of early systems. Looking back at the early development history of the Internet, we will understand that market mechanisms are more effective in finding innovative directions, but once the direction of innovation is established, appropriate government strategies and industrial policies can accelerate industrial development.

Of course, I am not saying that MAS will definitely succeed this time. After all, it will take a lot of time to meet all the conditions. Even if the infrastructure is built, it will take a lot of time for market liquidity to be gradually established. But I think MAS has found the right route and demand market, and it is indeed possible to quickly establish a value closed loop and feedback loop between technological innovation, infrastructure construction and application market, thereby leading this industry to achieve rapid development through rapid iteration and leading other regions in the world.

I have communicated with many Singaporean friends and learned that Singapore has positioned itself as the center of the future digital economy. Due to its small land area, Singapore's real economy has not had much room for development. However, in the digital economy, Singapore's physical space will no longer be a limitation, but it will have the opportunity to become a global digital economy power. This is Singapore's ambition.

With a solid demand and Singapore taking the lead, I now believe that the Indo-Pacific region will become a hot spot for the development of the blockchain industry. This market should bring rare opportunities to industry colleagues who are committed to creating real economic value with blockchain.