As the Azuki incident fermented, the NFT community and industry were facing challenges. Not only did the major blue-chip NFT series experience varying degrees of decline (see "The Azuki team took away 20,000 ETH, but the NFT market lost 200,000 ETH of liquidity"), many NFT lending platforms were also under pressure (see "Blue-chip NFT fell sharply, NFTFi accepted the challenge").

The market even further suspects that as NFT prices continue to fall, will it trigger a chain of loan liquidations, causing NFT prices to enter a new round of spiral stampede?

How prosperous is NFT Lending?

With the development of NFT, new projects in the entire NFTFi market are emerging in an endless stream, and various protocols are constantly emerging.

How many NFT lending platforms are there at present? As a relatively "hard-needed" product in the NFT field, there are countless lending agreements. Alchemy alone has included 42 NFT lending products, but since most of them are not popular, data is difficult to obtain. This article does not use this list as a research object.

According to DeFiLlama, 23 NFT lending protocols have been included in its statistics. As of the time of publication, the total TVL of the 23 protocols has reached 189 million US dollars.

Judging from the data alone, this number is quite impressive. If we use FT for a not-so-equal comparison, the total TVL of 264 FT (homogeneous token) lending agreements is as high as 14.7 billion US dollars, which is 77.7 times the TVL of NFT lending. The total market value of FT is about 1.2 trillion US dollars, which is 200 times the total market value of NFT of 6 billion US dollars.

Despite the large number of agreements, data shows that only a few are recognized by the market.

Among NFT lending products, the TVL of 5 protocols has reached more than 10 million US dollars, and the TVL of 4 protocols is between 1 million and 10 million. The leading protocols have obvious advantages. The total TVL of ParaSpace and BendDAO platforms is about 91 million US dollars, accounting for about 48% of the total TVL of all NFT lending protocols.

Flexible, “traditional” P2P lending injects liquidity into long-tail assets

In May this year, the famous NFT trading platform Blur introduced an NFT lending protocol called Blend, and thus entered a new track in the NFT market. Similar to Blur, NFTfi and Arcade are both NFT lending protocols that adopt the P2P model.

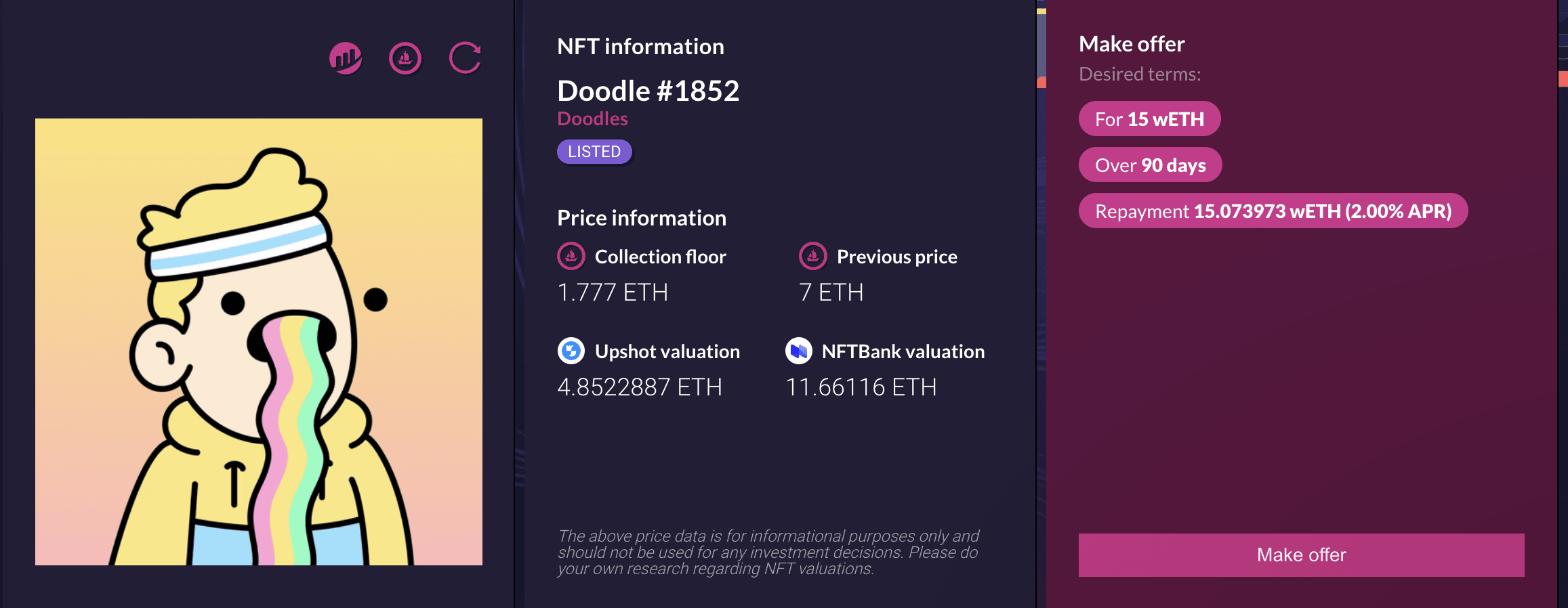

Taking NFTfi as an example, this protocol is a peer-to-peer (P2P) NFT lending protocol, which is also the current mainstream form of NFT lending.

NFTfi lending page

In this model, borrowers and lenders can be matched one-to-one on the platform, with a lender directly lending money to a borrower.

The P2P model is closer to mortgage loans in the traditional world, with the platform acting only as an intermediary.

In the P2P model, all quotations and transactions are completed on the platform, and the collateral is kept by the platform. If the borrower defaults, the platform will auction off the collateral. Since this model is closer to "one order, one price negotiation", the smooth transaction of such agreements depends on a large number of users and is closer to "semi-artificial". But the advantage is that its loan transactions are more diversified and more inclusive of long-tail assets.

But specifically speaking, although they are all P2P lending, each company has its own differences.

Specifically, NFTfi is closer to traditional loans. Lenders can set the loan amount, loan term, interest, etc. If the loan defaults, its NFT assets will be pledged to the lender, and the lender will have the opportunity to obtain the NFT at a price lower than its market value.

Arcade is also an old lending project. The predecessor of this project was Pawn.fi. Similar to NFTfi, the lender needs to initiate a loan request, set details such as the loan category, loan amount, repayment period, and loan interest rate, and sign a binding transaction based on this. In addition, Arcade also allows users to package multiple NFTs into an NFT package and pledge the package as a single asset. It also has greater flexibility in lending agreements. At the end of June this year, a user packaged the FTX debt token minted by Found into an NFT, and used this NFT as collateral to loan $7,500 worth of debt worth $31,307.81 on the protocol.

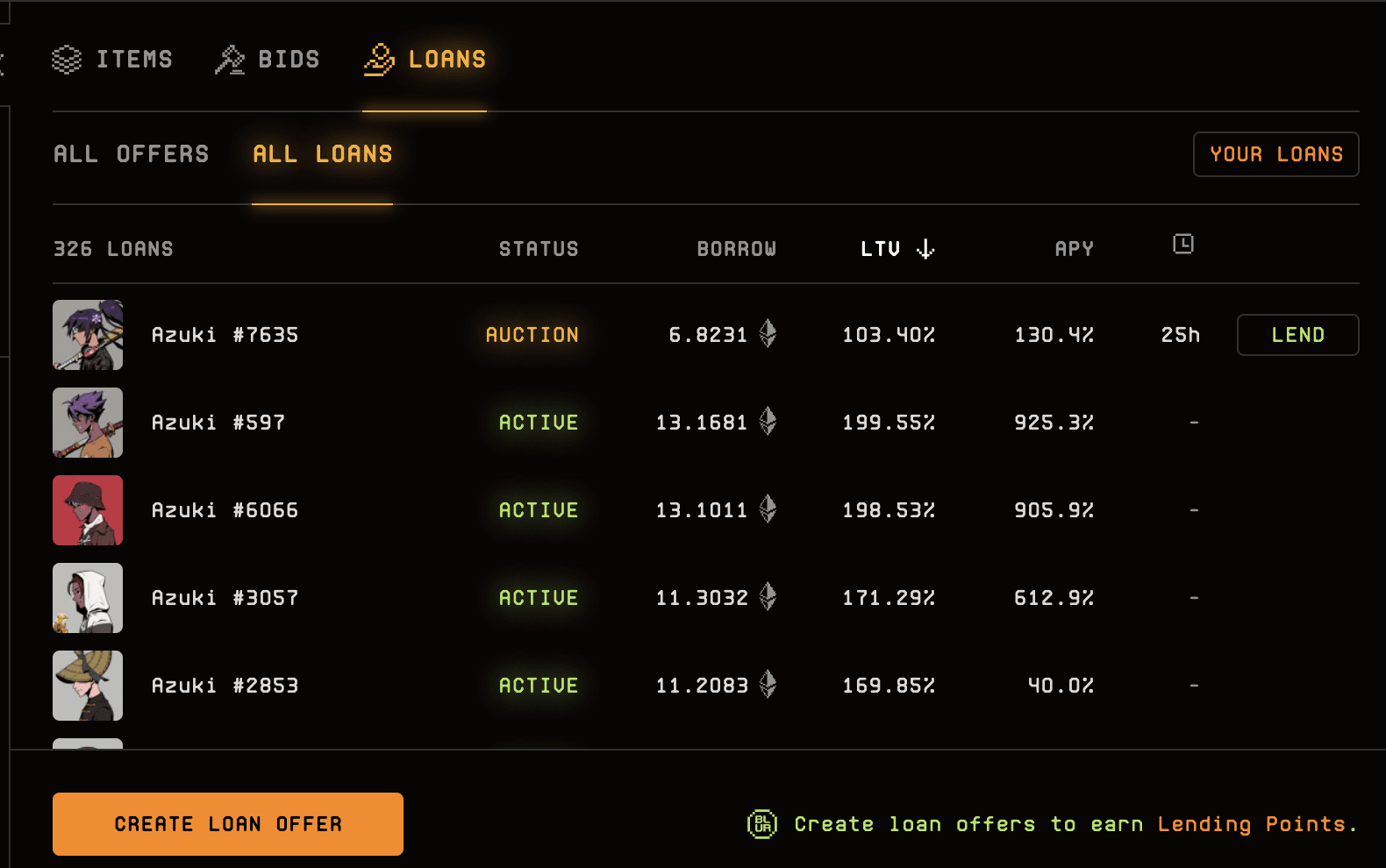

Blur Lending Loan List

Blend is a special P2P lending protocol. The protocol does not set an expiration date, achieving the effect of "perpetual loan". As long as there is a lender willing to use collateral for lending, Blend will automatically restart a loan position. Only when the interest rate changes or one party wants to exit the position, an on-chain transaction is required.

Blend also has different designs for defaults and liquidations. When the auction is triggered, the borrower can repay the loan within 24 hours. If the loan is not repaid, the interest rate of its loan agreement will be further increased, making its loan auction more attractive, and eventually its loan APY can even reach 1000%. If no one buys out the loan, the lender will receive the NFT as collateral 30 hours after the auction is triggered.

Overall, most P2P lending products do not require the intervention of external oracles. This is the flexibility of "peer-to-peer". The interest rate and loan value are negotiated and determined by the borrower and the lender, and each loan is matched individually.

How does the protocol lending of the liquidity overlord pose hidden dangers to the market?

Peer-to-peer transactions are a completely different lending model from P2P. ParaSpace and BendDAO, two leading platforms, both use this model. DeFiLlama data shows.

Its high TVL also illustrates the high efficiency of peer-to-peer lending to a certain extent. P2P NFT lending allows for more flexible and customized loans, while peer-to-peer lending allows NFT holders to obtain liquidity more quickly and conveniently.

In this model, users can directly obtain loans from the protocol after pledging NFTs, without having to wait for the right borrower to complete a "1 to 1" match. Similar to the FT lending protocol, the funds for the loan usually come from liquidity providers, and users can earn loan interest by providing funds to the protocol.

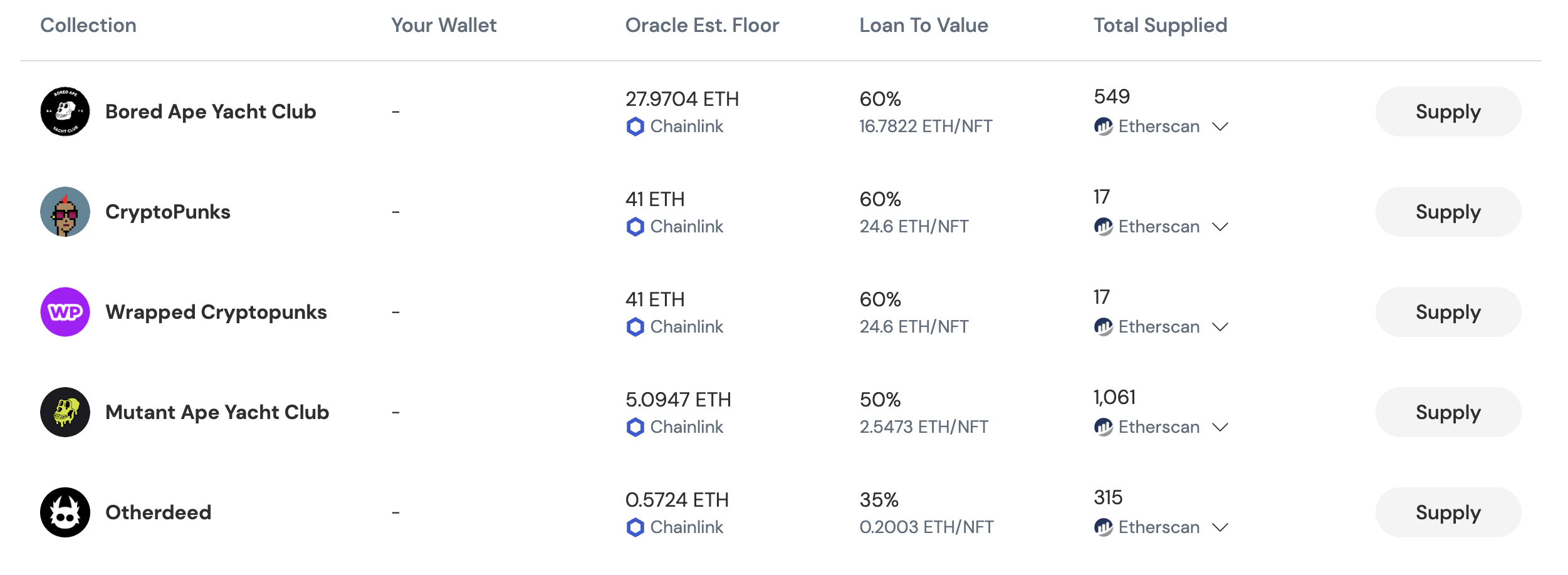

ParaSpace Lending Marketplace

Taking ParaSpace as an example, the protocol provides users with a more intuitive market and user experience that is close to traditional FT lending. Users can deposit NFTs and directly borrow a variety of FT tokens from the protocol.

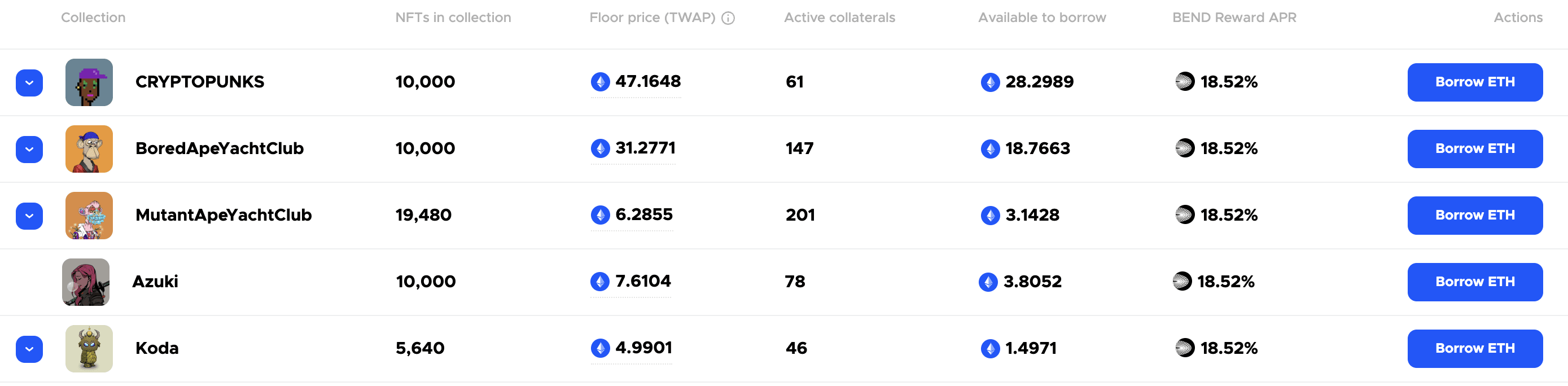

BendDAO Lending Market

Similar to ParaSpace, BendDAO also allows users to directly initiate loans to the protocol, and the protocol issues loans to borrowers through a unified reserve pool.

In this model, the biggest difference from peer-to-peer NFT loans lies in the importance of external oracles. Since such loans are not loan terms agreed upon by both parties, their debt default liquidation mechanism is different from that of the aforementioned P2P platforms.

In addition, the most important thing is that after the liquidation occurs, NFT will flow to the secondary market after being auctioned, rather than being transferred to the lending user. It is this difference that makes this model more "automated", but it also lays the hidden danger of NFT's "spiral decline".

Whether it is BendDAO or ParaSpace, the price feed uses Chainlink oracle and uses OpenSea's floor price as the price feed data.

JPEG'd is a unique project among mainstream NFT lending projects. The protocol does not adopt the conventional model of depositing NFTs and lending ETH. Instead, it follows the example of MakerDAO, allowing users to deposit NFTs as collateral and borrow synthetic stablecoins PUSd. Users can use PUSd to provide liquidity on the protocol and earn interest. This model is called NFDP (Non-fungible debt positions). Similar to other peer-to-peer lending platforms, JPEG'd uses Chainlink oracles to feed prices.

Liquidation triggers a spiral stampede?

When the health of the collateral is insufficient, liquidation will occur.

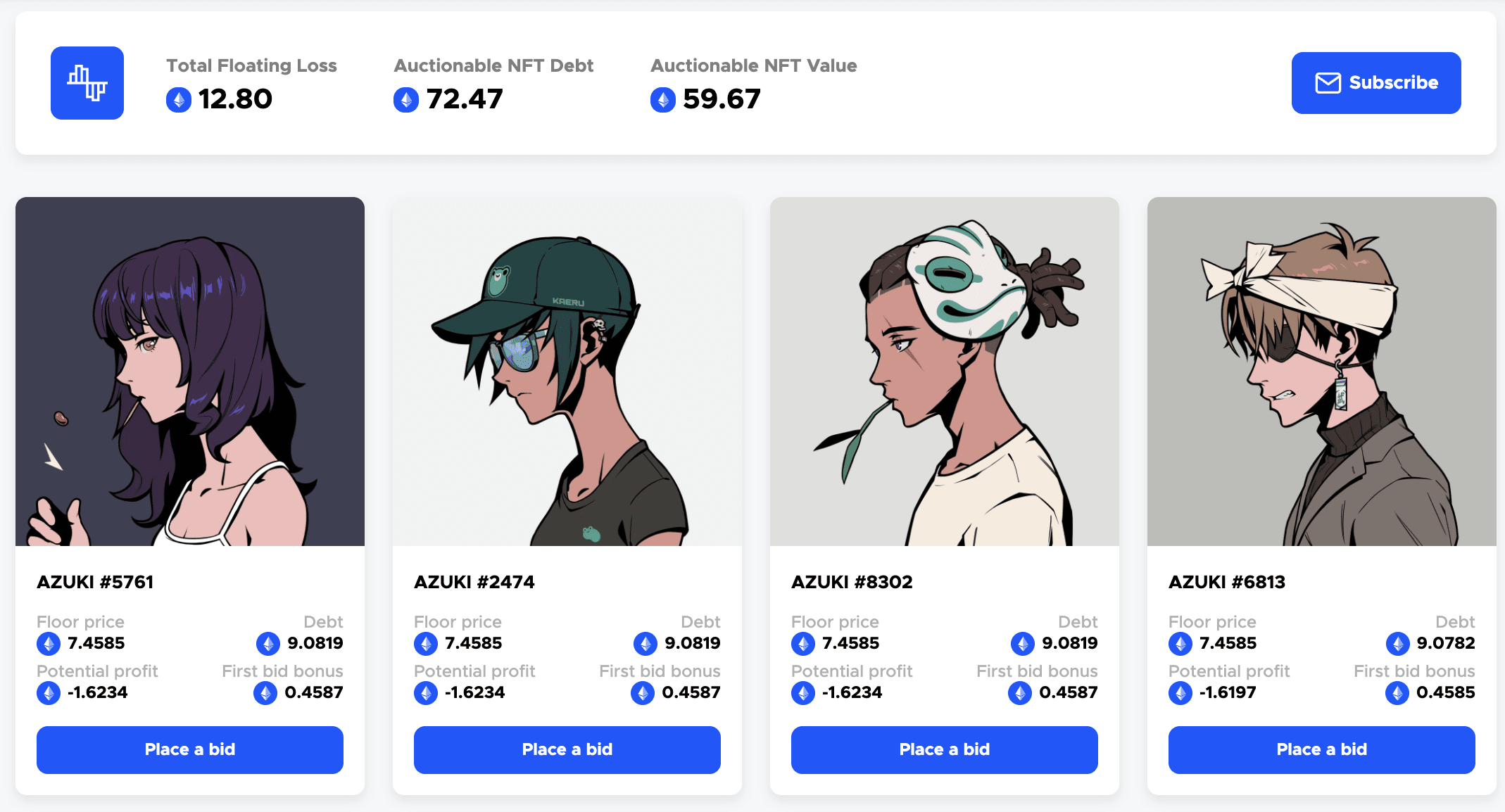

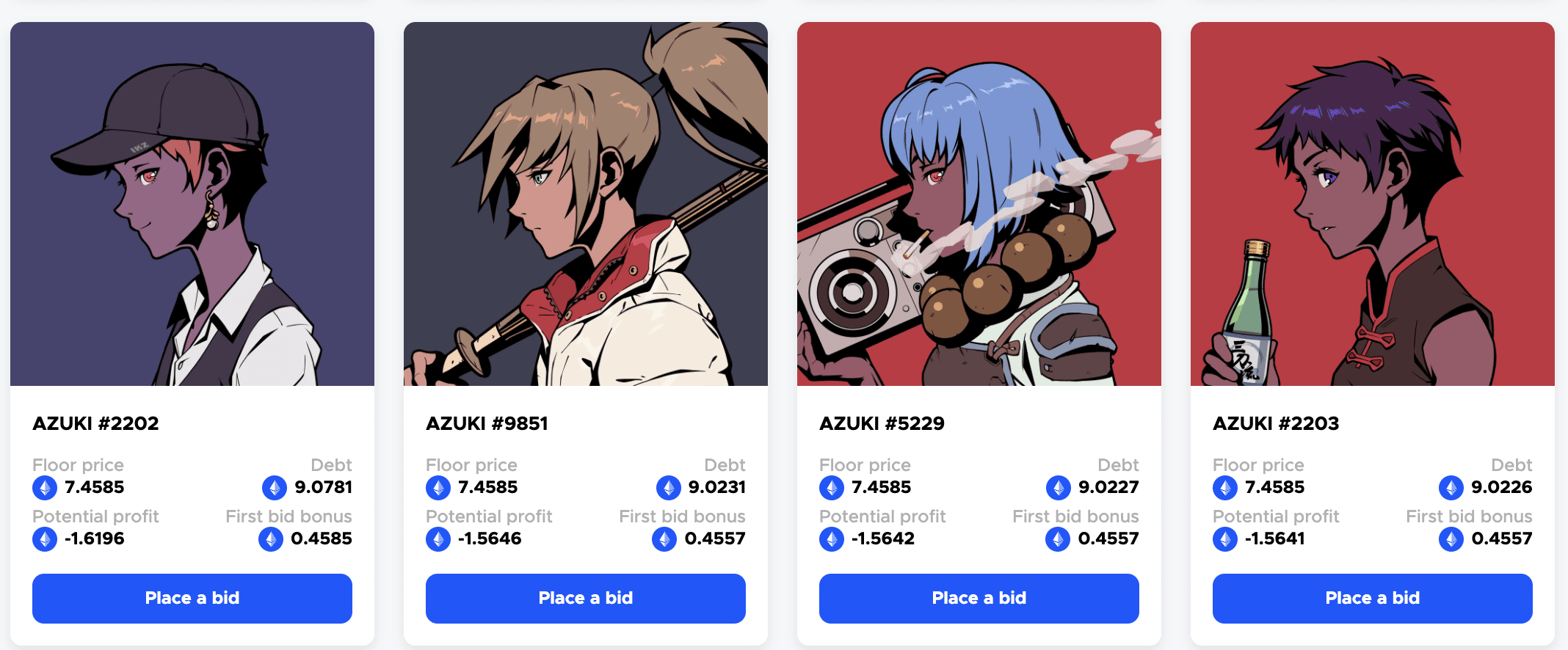

After the Azuki incident, the rapid drop in the price of Azuki caused the floor price of some NFTs to fall below the value of the debt. Taking BendDAO as an example, a total of 8 Azukis have become bad debts, and the mortgage assets worth 59.67 ETH owe 72.47 ETH of debt.

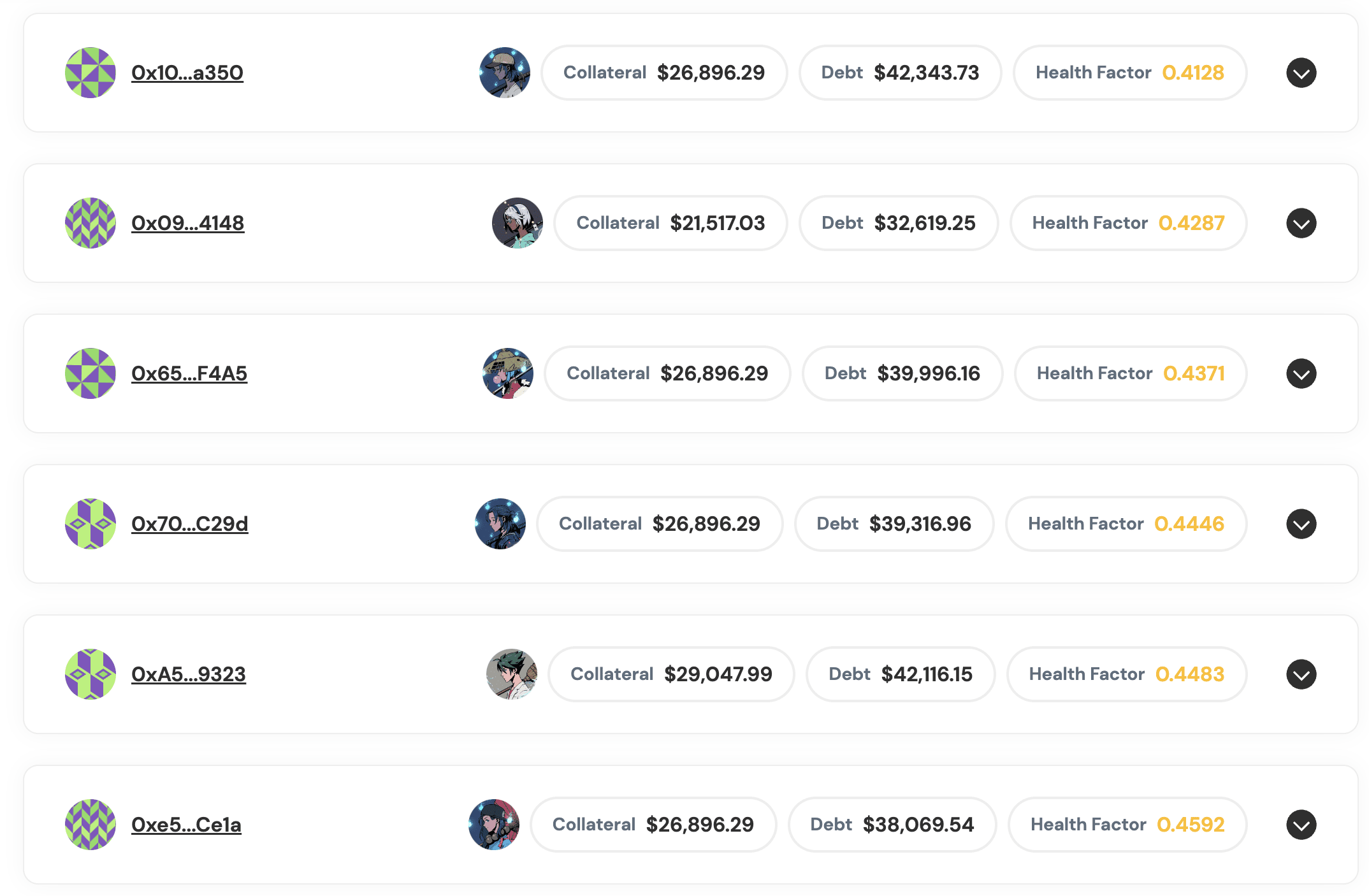

ParaSpace is in a similar situation, with multiple loans on the platform insolvent.

Currently, 13 (a total of 14) Azuki lending liquidations have been suspended by the platform, with a total collateral value of 359,900. ParaSpace said that the suspension of liquidation is intended to give users more time to replenish liquidity, repay loans and improve health, and liquidation will be resumed later. At present, this batch of bad debts is about 100,000 US dollars. ParaSpace said that there are enough reserve funds to deal with unexpected situations, and its reserve funds can fully cover it.

How terrible can a downward spiral caused by liquidation be?

In April this year, the cancellation of BAYC whale Franklin’s account and his exit from the community made people sigh. Franklin repeatedly used BendDAO and allocated a large amount of BAYC under leverage and market decline. He once owned 61 BAYCs, becoming the sixth largest BAYC holder. His loan amount also reached an astonishing nearly 20,000 ETH. But after a series of wrong operations, Franklin eventually suffered a large loss and retired from the community.

At present, the booming NFT lending market has brought more abundant liquidity, imagination and usage scenarios to the market. However, with the intensification of NFT financialization, various financial risks contained in the FT market will also be brewing in the NFT market. With the emergence of this round of large market fluctuations, how many risks will appear in the NFT market in the future?