By Colin Lee

Since the beginning of the year, the market has been discussing RWA (real world assets) more and more frequently, and some believe that RWA will trigger the next bull market. Some entrepreneurs have also adjusted their direction to tracks related to RWA, hoping to boost the rapid growth of their business under the blessing of the gradually warming narrative.

RWA maps assets in the traditional market to the chain in the form of tokens for web3.0 users to buy and sell. RWA tokens have the right to the income of assets. A few years ago, the scope of STO was mainly focused on corporate bond financing, but now the scope of RWA is broader: it is not limited to the primary market of traditional assets. Any assets circulating in the primary and secondary markets can be put on the chain through tokenization, allowing web3.0 users to participate in investment. Therefore, the narrative of RWA contains a rich variety of assets and a wide range of yields.

RWA has gradually attracted the attention of the market. There may be several reasons: First, the current crypto market lacks low-risk U-based assets, and under the wave of interest rate hikes in the traditional financial market, the risk-free interest rate of major economies has risen to 4% or even higher, which is attractive enough for investors in the crypto-native market. Corresponding to this phenomenon, during the bull market of 2020-2021, a lot of traditional funds also entered the crypto market to earn low-risk returns through arbitrage and other strategies. The introduction of low-risk and high-yield products in the traditional market through RWA may be welcomed by some investors; secondly, the crypto market is not in a bull market now, and even in the crypto-native market, there is a lack of enough narratives. RWA is one of the few tracks currently seen with solid income support, and may achieve explosive growth in business; finally, RWA is one of the bridges connecting the traditional market and the crypto market. Through RWA, there is also an opportunity to attract incremental users in the traditional market and inject new liquidity, which is undoubtedly a positive for the development of the blockchain industry.

However, judging from some RWA projects we have seen so far, their business indicators such as TVL have not grown rapidly, and the market may have too high short-term expectations for RWA. For an RWA project, the following dimensions need to be considered:

Underlying assets. This is the core issue of the RWA track. Choosing the right underlying assets will be of great help for subsequent management.

Standardization of underlying assets. Due to the different "heterogeneity" of different underlying assets, the difficulty of standardizing underlying assets is also different. The more heterogeneous the assets are, the higher the standardization requirements are and the more complicated the process is.

Off-chain cooperative institutions and forms of cooperation. High-quality off-chain cooperative institutions can not only smoothly fulfill their obligations, but also fully release the value of the underlying assets.

Risk management. The maintenance of underlying assets, asset chain, and income distribution all involve risk management. If it is a debt-type asset, it also involves risk management in asset liquidation and collection after the debtor defaults.

1. Underlying assets

The underlying assets are the most core elements.

At this stage of the RWA track, the underlying assets are mainly divided into the following categories:

Bond assets are mainly short-term US Treasury bonds or bond ETFs. Typical representatives include stablecoins such as USDT and USDC. Some lending projects, such as Aave and Maple Finance, have also joined this camp. Treasury bonds/treasury bond ETFs are currently the largest proportion of RWA;

Gold, a typical example is PAX Gold. It is still under the narrative of "stable currency", but its development is slow and the market demand is weak;

Real estate RWA, typical representatives are RealT, LABS Group, etc. It is similar to packaging real estate into REITs and then putting them on the blockchain. The real estate sources of this type of project are wide, and the project team often chooses their own city as the main source of assets;

Loan assets. Typical types include USDT, Polytrade, etc. The types of assets are relatively wide, including personal housing mortgage loans, corporate loans, structured financing tools, car mortgage loans, etc.

Equity assets, typical projects include Backed Finance, Sologenic, etc. The transactions of this type of assets seek real existence, but are greatly restricted by legal issues. An important development direction of crypto-native "synthetic assets" is listed and circulated stocks, which highly overlap with this field;

Others include farms, artworks and other assets that are larger in scale (larger amounts of individual assets) but less standardized.

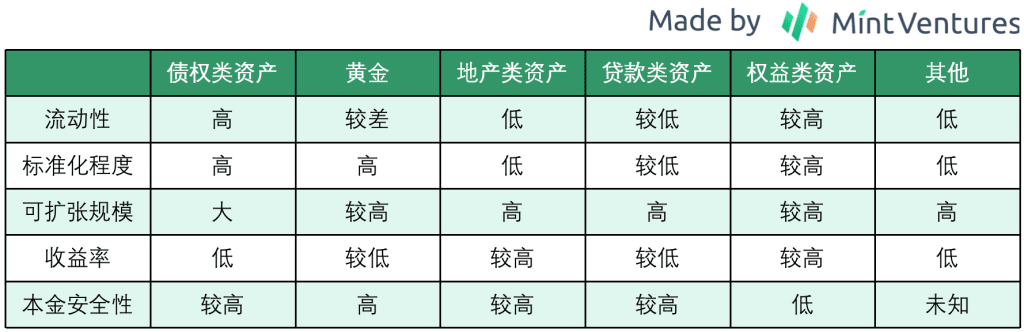

When choosing which asset to use as the underlying asset, we need to consider five dimensions: liquidity, standardization, principal security, scalability, and yield. From these five dimensions, we can roughly define the attributes of the above assets.

From the perspective of underlying assets, debt assets currently seem to be the most worthy category to explore. Based on their own positioning, they can seek differentiated routes: stablecoins anchored to legal currency, Yu'ebao in the crypto market, etc. Although the stablecoin track anchored to legal currency is already full of oligopolies, and major projects have formed ecological cooperation with a large number of projects, tracks such as "Yu'ebao in the crypto market" are still to be explored.

For real estate assets, although the REITs solution is mature, if the project team decides to select assets and manage regional and property diversification, it will undoubtedly increase costs: for example, in terms of project maintenance, if the regional distribution is too dispersed, the number of people involved in property management will increase, and the procurement costs and personnel transportation costs for property maintenance and other aspects will also need to increase. In the process of looking at projects, I have encountered situations where the project team hopes to control the value of a single property within US$100,000, distributed in more than 5 countries, and the property type is not limited to residential and commercial properties. Although it may be sufficiently decentralized, it is difficult to disclose information and manage properties. It will also be difficult to achieve rapid growth of underlying assets in the future.

At present, the author does not recommend paying too much attention to "other" types of underlying assets. The most important reasons are liquidity and standardization. For example, agricultural-related underlying assets are relatively non-standard, which adds a lot of difficulty to determining the quality of the underlying assets. Taking a single farmland as an example, the quality of the crops produced will also vary. Warehousing, transportation, and sales are also relatively specialized processes. If you want the income from agricultural assets to be finally delivered to investors, you need to work in the industry for many years. The fluctuations in the production capacity cycle and the impact of weather factors faced by cash crops are also difficult to predict. There is also great difficulty in the final realization.

If the project party searches for assets and packages assets by themselves, the growth potential of the project itself will be greatly affected, and it will be more difficult for this type of project to grow rapidly.

In terms of underlying assets, currently taking bond assets as the core direction and REIT-like assets as a way to increase returns may be a more practical and feasible direction.

2. Business Architecture

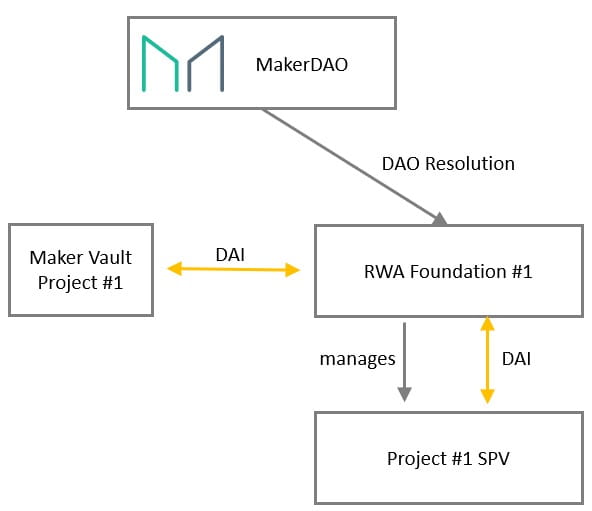

If there were still major problems in the past few years on how to put RWA on the chain, now a clearer path has been formed under the exploration of leading projects such as MakerDAO.

First, in order to facilitate the on-chain of RWA, an RWA Foundation architecture can be established. Under this architecture, MakerDAO can manage multiple RWAs through the RWA Foundation, and the new RWA can be loaded directly by the RWA Foundation to initiate the SPV (Special Purpose Vehicle).

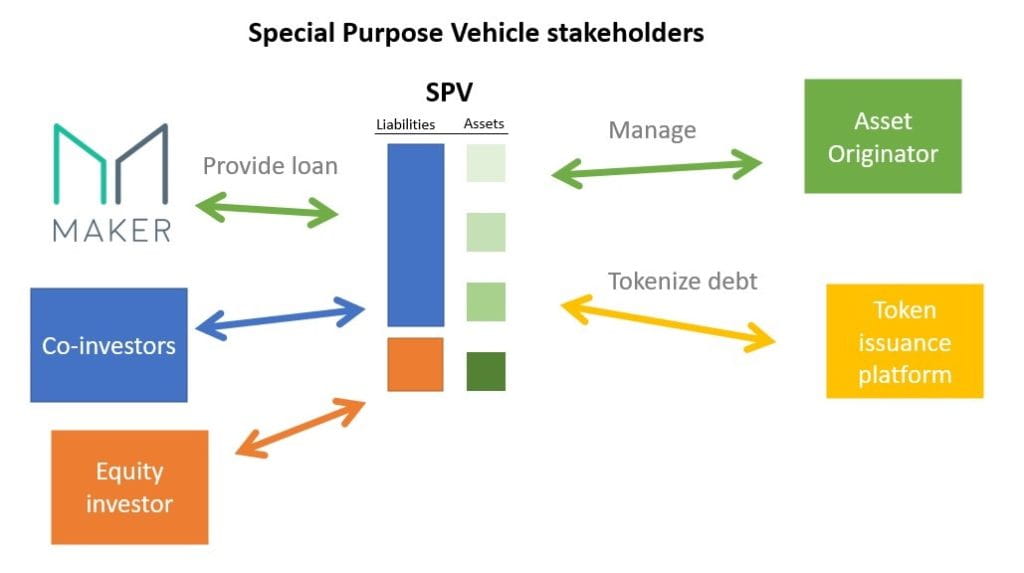

Secondly, for a single SPV, a management model similar to the securitization financing method supported by the assets of the ABS (Asset Backed Securitization) project can be adopted:

For the safety of funds, MakerDAO chooses to invest in priority assets, and the remaining investors can become investors in subordinated shares. For other project parties, they can determine the risk level of the assets held based on the risk preferences of the target user group.

Unlike traditional asset securitization steps, in MakerDAO's single SPV, there is no role of settlement and fund custody, but a tokenized issuance platform has been added. In the future, when the regulatory space becomes clearer, settlement and fund custody may still be necessary participants in RWA.

3. Risk Management

RWA's risk management is mainly divided into three dimensions:

1. Risk management of underlying assets. The lower the degree of standardization of assets, the higher the risk management capabilities required. Compared with forest farms and farms, government bonds have a high degree of standardization, better asset liquidity, and stronger price discovery capabilities. Therefore, it is easier to manage government bonds. However, even for the same type of assets, the difficulty of management varies in different regions and countries. For example, the level of electronicization in some developing countries is low, and debt assets may still exist in paper form. This requires that during the period of holding large bonds, the project party needs to find a place to store the bonds where they cannot be damaged. Assets in paper form are also more likely to be "replaced by a cat for a prince", and this type of incident has occurred in many regions with large cases.

In short, the most basic thing for risk management of underlying assets is to ensure that the underlying assets are real and valid during the project life cycle, and secondly, to ensure that the value of the underlying assets will not be lost due to human factors. Thirdly, it should also ensure that the underlying assets can be realized at a fair market price, and finally, it should ensure that the income and principal can be safely and smoothly delivered to investors. This type of risk has a large overlap with the attributes of traditional assets, and there are risk management measures that can be referred to.

2. Risk management on the chain. Because it involves data on the chain, if the off-chain institutions are not adequately managed, there may be cases of false reporting of data. Similar negative cases often occur in the traditional financial field. For example, in the fields of commercial bills, supply finance, commodities, etc., there have been huge amounts of fraud. Even through real-time monitoring by sensors and fixed delivery locations, there is still no way to avoid risks 100%.

For the RWA industry, which is still in its infancy, I believe that similar situations will occur. Moreover, there is currently a lack of corresponding regulatory details, the cost of violating the law is too low, and the risk of data falsification on the chain cannot be underestimated.

3. Partner risk management. This type of risk is still traditional, but the problem is that there are no detailed rules for RWA supervision. For example, in the custody stage, what kind of custodian is compliant? In the audit stage, can the current accounting and financial standards accurately and completely reflect the characteristics of RWA? In the process of project operation, if a risk event occurs, what kind of risk handling method and process can better protect investors? There is still no very accurate answer to this type of question. Therefore, partners still have the opportunity to do evil.

IV. Current User Structure and User Needs

As mentioned in the previous article “Prospects for the “Native Bond Market” in the Crypto World”, due to the strong volatility and cyclicality of the crypto market, relatively low-risk and conservative risk-taking investors find it difficult to obtain sustained and stable returns in the market. In such a market, a large number of users also show a strong risk appetite:

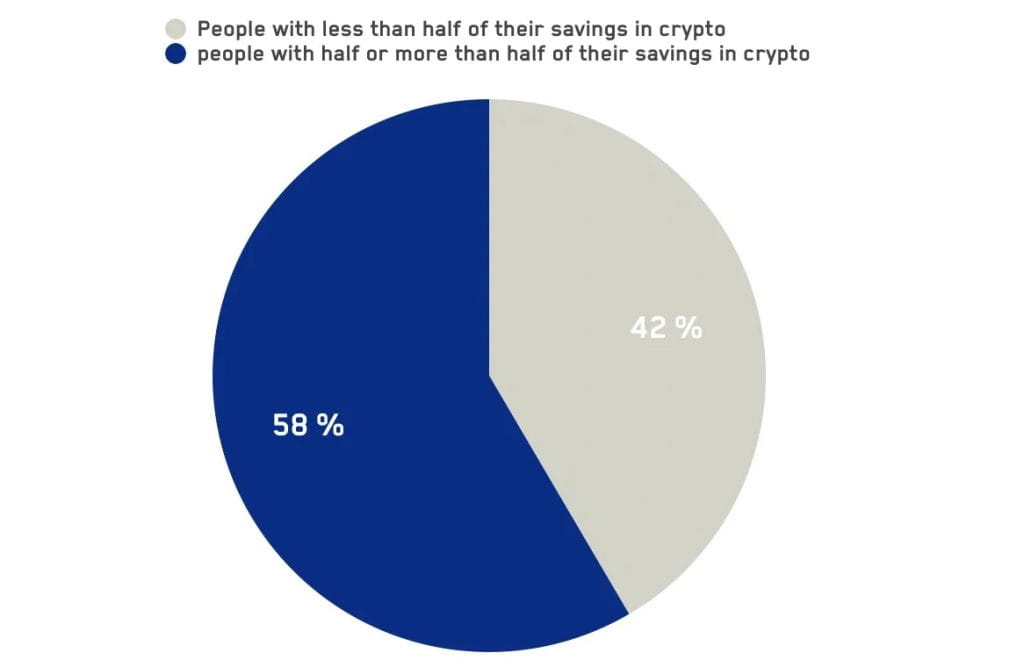

In a survey report released by dex.blue and other teams in 2020, half of the crypto market users surveyed invested 50% or more of their total savings in the crypto market; Pew Research and Binance also mentioned in their survey reports that young people currently account for a high proportion of users in the crypto market. Under such a market structure, the risk appetite of crypto market investors will be higher than that of traditional market investors.

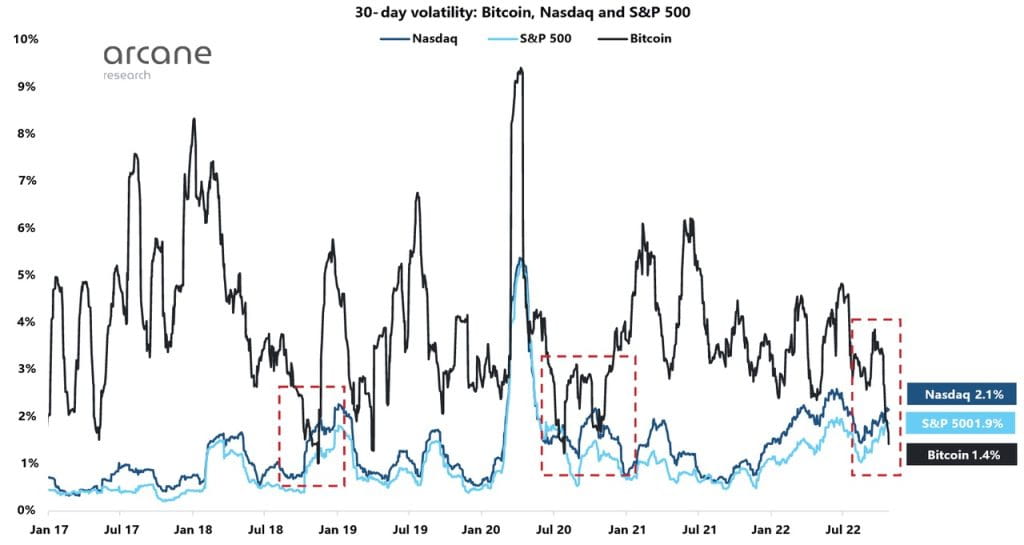

In the current market dominated by "arbitrageurs and extremely high-risk investors", its volatility also presents similar characteristics: K33 Reseach's research shows that from the beginning of 2017 to October 2022, Bitcoin's volatility was higher than that of Nasdaq and S&P 500 in most of the time period. Only when the market is extremely dull does the volatility of US stocks have a chance to exceed that of Bitcoin.

The two main investor groups in the crypto market may have different demands for yield: for arbitrageurs, "low-risk" investment opportunities are easier to obtain, and this type of trading opportunity, taking the Bitcoin perpetual contract funding rate as an example, the annualized yield from the product's appearance to date is between 15% and 20%, which is much higher than the long-term yield level of 5% in the global stock market, and higher than the long-term yield of various types of bonds. For high-risk investors, the expected return is much higher than that of arbitrage investors.

Therefore, even if stocks are tokenized, it may be difficult to meet the current market user structure and their expected return level. In the short term, the risk-return ratio of a large number of RWA products is awkward.

5. Regulation: Perhaps a potential opportunity

In early June this year, the U.S. SEC announced that it would define multiple tokens including BNB, BUSD, MATIC, etc. as securities, which triggered market concerns about regulation and the corresponding targets also experienced a significant decline.

If the SEC's regulatory measures are recognized by other G20 or more countries, more tokens will be listed as securities and included in the traditional regulatory framework, and the issuance of tokens on the chain may also be included in the regulatory scope in the future. From the current regulatory policies, we have seen similar signs: whether it is the United States, Japan, or EU countries, the regulatory measures for stablecoins have begun to move closer to traditional banks. Perhaps the future regulation of tokens will also refer to the regulatory measures of securities to a certain extent.

If such a situation occurs, some practitioners in the traditional financial field will feel more confident to put their assets on the chain: the advantage of this is that the assets are local, but can absorb global liquidity. This idea has been recognized by some RWA project entrepreneurs: although they are limited by geographical factors, with blockchain, they can obtain global investors. For these practitioners, putting assets on the chain under supervision will bring two benefits: 1. With the tentacles of obtaining global liquidity, the funding side will not be affected by geographical factors, which may raise cheaper money; 2. Because it is possible to find investors with lower yield requirements than local investors, the range of options for projects will increase.

At the same time, regulatory measures on the user side are also being promoted: KYC. Crypto-native projects only need a wallet to access, but some startup projects that raise funds in the primary market already need the assistance of KYC to determine whether users are qualified investors. Some projects that introduce RWA, such as Maple Finance, also regard KYC as an indispensable process in the customer acquisition process. If the KYC process is gradually implemented in more new projects, then the blockchain industry with clearer supervision and KYC coexisting may bring an additional benefit: more and more ordinary investors can enter the market with more confidence.

This type of user has a higher risk preference for familiar assets and is also interested in emerging crypto-native assets. At this time, RWA can serve as an important investment direction for this type of more ordinary investors.

6. Possible development paths for RWA

In the short term, RWA brings three benefits to crypto investors:

1. Low-risk investment targets based on fiat currency: At present, the risk-free interest rate level of major economies led by the United States has reached more than 3%, which is significantly higher than the lending yields of various types of U-based lending agreements in the crypto market. Without the need for circular leverage, it brings investors extremely low-risk investment opportunities. At present, projects such as Ondo Finance, Maple Finance and MakerDAO have launched investment projects based on the yield of US Treasury bonds, which is very attractive to investors who settle in fiat currency. In this track, there may be a "Yu'ebao" project in the crypto market.

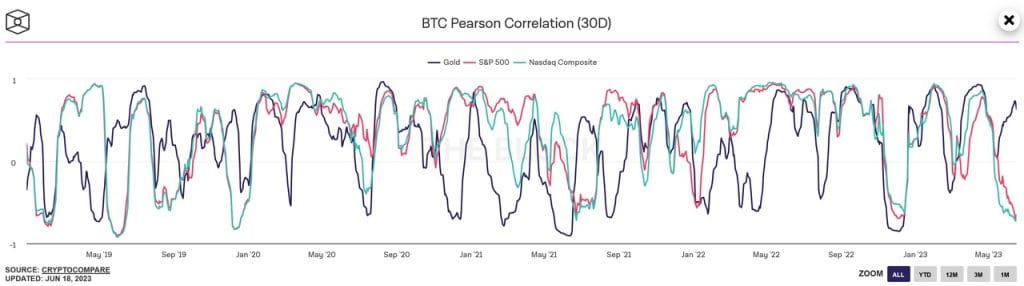

2. Risk diversification of assets: Taking Bitcoin as an example, its correlation with gold and US stocks fluctuates to varying degrees in different market stages.

Even in the big year driven by macro factors after 2020, assets in different asset classes still have a certain degree of diversification advantages.

For allocation investors, mixing crypto-native assets with various types of RWA can diversify asset risks to a greater extent.

3. A means for investors in developing countries to hedge against fluctuations in the value of their own currencies: Some developing countries, such as Argentina and Turkey, have long-term high inflation. RWA can help investors in these regions to hedge against fluctuations in their own currencies to a certain extent and achieve global asset allocation.

Judging from the above three dimensions, the RWA that will be widely accepted in the short and medium term is more likely to be the high-yield, low-risk RWA of government bonds of major economies due to the current interest rate hikes.

In the long run, as the regulatory framework becomes clearer, more investors gradually enter the crypto market, and the operation of the crypto industry becomes more convenient, RWA will have the opportunity to replicate the grand occasion of China's Internet finance explosion 10 years ago:

1. Blockchain-based RWA assets provide unprecedented "accessibility" for mass investors around the world: RWA, as the most familiar asset to mass investors, may become the main on-chain investment target for non-Web3 native investors. For them, the borderless nature and permissionless access and operation of on-chain assets open the door for them to invest in and use a wider range of global assets. In turn, for entrepreneurs in the field, this also provides them with unprecedented user breadth, scale and extremely low customer acquisition costs. The rapid development and widespread use of USDT and USDC as "on-chain dollars" have initially verified this trend.

2. RWA assets may derive new DeFi business models: LSD, as a new underlying asset, has stimulated the rapid development of LSD-Fi. Among them, in addition to the existing business paradigms such as asset management, spot trading, and stablecoins, which have been re-emphasized by everyone, there are also directions such as volatility in yields that have appeared in the past but have not been taken seriously. If RWA becomes an important underlying asset, the introduction of new and huge off-chain income may breed a new DeFi business model. In the future, RWA can also be combined with crypto-native assets and strategies to form hybrid assets, allowing more users who are willing to explore crypto-native assets to understand them in a more familiar way. From this perspective, the next RWA+DeFi project with ultra-high TVL may be "Yu'ebao on the chain".

3. The game between the industry and regulation will eventually have an answer, and practitioners can seek ways to acquire customers in compliance: Whether in Western countries or in Hong Kong in the East, the gradual implementation of regulation is the general trend. The crypto industry will grow to a size of 10 trillion US dollars in the future, and regulators will not sit idly by. As regulatory policies become clearer, we can see that some regions can implement businesses that were previously unattainable: stablecoins can already be issued through compliant channels in Hong Kong, and the Middle East is also exploring ways to combine the blockchain industry with traditional industries.

In the long run, one of the important factors for the booming crypto industry is sufficient liquidity. With the implementation of regulation, RWA, led by fiat-collateralized stablecoins, is bound to grow rapidly. Especially under the stimulation of the next round of global liquidity easing, if new players can have strong support in terms of ecology and channels, compliant fiat-collateralized stablecoins may also be able to replicate the ultra-high growth path of USDT.