Is a further rebound of Bitcoin to $35,000 "inevitable"?

Uncertain macroeconomic and inflation conditions, coupled with a seemingly hawkish Fed, could create short-term headwinds

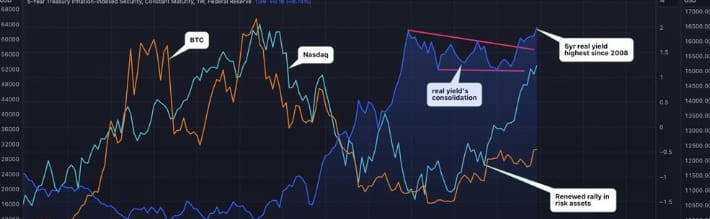

Inflation-adjusted U.S. government bond yields are rising, which has some observers worried about potential risk aversion in stocks and broader financial markets. Bitcoin and digital assets in general will remain resilient.

According to data tracked by TradingView, the real yield on 5-year Treasury bonds rose to nearly 2% last week, breaking the September 2022 high of 1.92%, the highest level since the end of 2008. The 10-year Treasury yield is 1.6%, which is very close to the data in 2009. At the same time, the real yield on two-year Treasury bonds has reached 3%, the highest level in at least a decade.

Rising U.S. Treasury yields could dampen economic growth and reduce the appeal of investing in riskier assets such as Bitcoin and gold. Bitcoin and Wall Street's tech-heavy Nasdaq index have historically moved inversely to U.S. Treasury yields.

Bitcoin has surpassed its April highs, while the altcoin market is 20% below April levels and 70% below its 2021 highs. Bitcoin doesn’t have to worry about regulatory issues, and its resilience and influence at the start of a new month and quarter set it apart.”

Considering the current market sentiment, Bitcoin may soon reach the $35,000 mark

July is usually a good month for digital assets. Bitcoin has been taking a beating since the FTX crash, but in early July we could see a strong rebound in Bitcoin.

Mainly affected by industry changes:

1. North American regulation is becoming more stringent, and Hong Kong is becoming more open to crypto. There is a clear decline in policies in the west and rise in the east. North American investors are beginning to accept and invest in Asia-Pacific startup teams.

2. There are few new narratives. Current projects revolve around ZK (web3 native), AI (web2 native), etc.

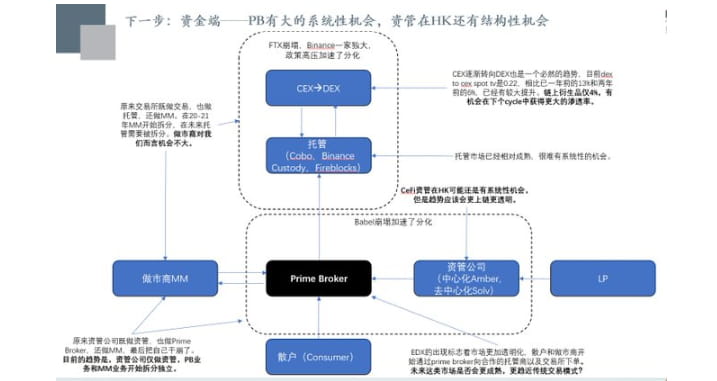

3. Wall Street capital represented by Citadel, Fidelity and Sequoia began to build their own compliant exchanges EDX, and the capital market began to modularize

4. Wall Street capital represented by Black Rock, Fidelity, etc. began to submit Bitcoin/cryptocurrency ETFs, which is an important reason for the recent market recovery

The direction of advancement in the second half of the year:

1. Crypto infra still needs attention, but the core should not focus on it

2. We need to pay special attention to the funding side. With the emergence of EDX, the overall trading model will become more traditional, thus bringing systematic opportunities to Prime Brokers and structural opportunities such as HK's CeFi asset management.

3. On the user side, we need to pay attention to whether the general conversion ideas based on games and the ideas of converting users in segmented tracks are correct. If there is a suitable team, we should focus on layout.

4. The logic on the development side is still correct. Although the direction is correct, the conversion speed is slower than expected. The current problem is that there are not enough users to support the new project. The overall development side projects will tend to be stable, and the risk is relatively small.

The emergence of EDX represents that crypto trading will gradually shift to the traditional exchange model. That is, institutions/MM/retail investors place orders through PB to the custodians who hold the exchange funds. In addition, the Singapore regulatory authority MAS also requires exchanges to hold funds on the trading platform today. Therefore, I am still optimistic about PB, HK CeFi, and on-chain derivatives exchanges in the long term.

The direction of users can be roughly divided into three categories. Traffic entry layer (axie, stepn, etc.), channel layer (various wallets) and tool layer (aa infra as a service). The traffic entry layer has strong explosiveness, that is, it starts to convert users from general games + various segments (preferably the third world). The channel layer is the most difficult to commercialize. Under the current situation of extremely high volume of the channel layer, the tool layer has a chance to run out

Secondly, I personally think that there are still structural opportunities in vertical L2, as well as ZK hardware acceleration that serves the entire Ethereum ecosystem (the key is that it can also serve Web2 giants), AA wallets (and their infra), DA, etc.