Author: Gryphsis Academy. Translated by: Cointime.com QDD

Brief summary

1. NFT lending is a financial product that occurs during the NFT holding phase. Its core mechanism allows holders to borrow short-term funds with their idle NFTs without having to sell them. By using their NFTs as collateral, holders can obtain liquidity in the form of cryptocurrency or fiat currency. This allows them to make a profit while enjoying the benefits of holding NFTs, thereby improving their capital utilization efficiency.

2. There are two main types of NFT lending agreements: secured lending and unsecured lending.

1) Mortgage loan:

Peer-to-peer (P2P): Suitable for bear markets with limited liquidity as the platform is unlikely to be affected by extreme market conditions.

Peer-to-Pool: Suitable for bull markets with abundant liquidity.

Hybrid mode: Based on the standard point-to-point mode, it provides greater operational convenience.

Collateralized Debt Position (CDP): A good option for those seeking the liquidity of blue-chip NFTs but avoiding paying high interest.

2) Unsecured loans:

Buy Now Pay Later (BNPL)

Flash Loans

Allow users who have purchasing intentions but temporarily lack full payment capabilities to enter the NFT market.

3. The revenue model of NFT lending mainly relies on the loan interest paid by users for mortgage lending. If there are additional functions such as flash loans, corresponding function fees can be generated.

4. The main risks associated with NFT lending are:

Volatility risk (default risk) in the valuation of NFT collateral.

High concentration of target users.

Due to the limited incremental supply of high-quality asset targets, the overall industry has limited quantitative growth potential.

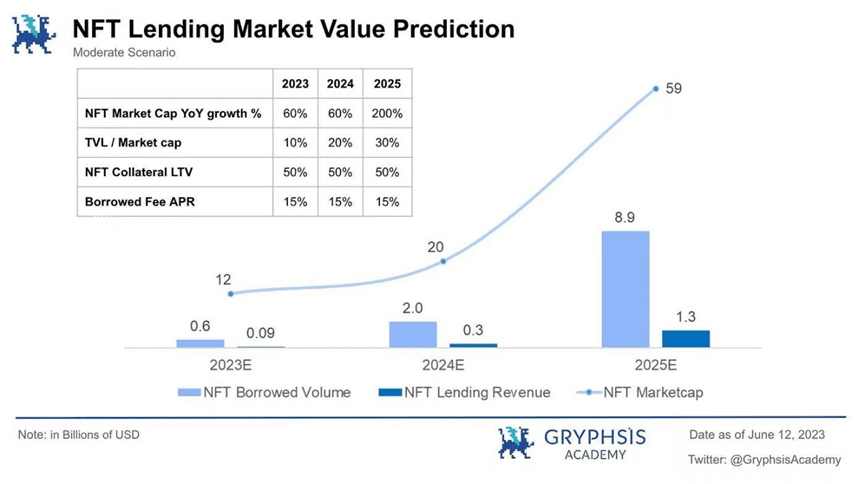

5. It is expected that within three years, assuming a moderate scenario, the overall market value of NFT may reach about US$60 billion, of which the total locked value (TVL) of NFT lending may reach about US$18 billion, meeting about US$9 billion in lending demand. The annual revenue of the NFT lending industry is expected to reach US$1.3 billion.

1. Industry Background

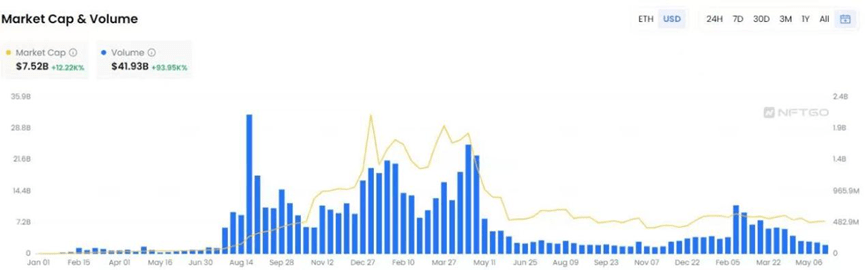

In the past few years, two areas in the cryptocurrency industry have experienced rapid development. One is decentralized finance (DeFi), which experienced the "DeFi summer" in 2020. The other is the NFT craze in 2021. The overall market size of NFTs on Ethereum has grown from about $61 million at the beginning of 2021 to a peak of about $32 billion in more than two years. Although the market has undergone major adjustments, the market size is still about $7.5 billion, an increase of more than 120 times.

Today, NFT-Fi, which combines NFT and DeFi, has rapidly developed from a niche field to an important part of the cryptocurrency world.

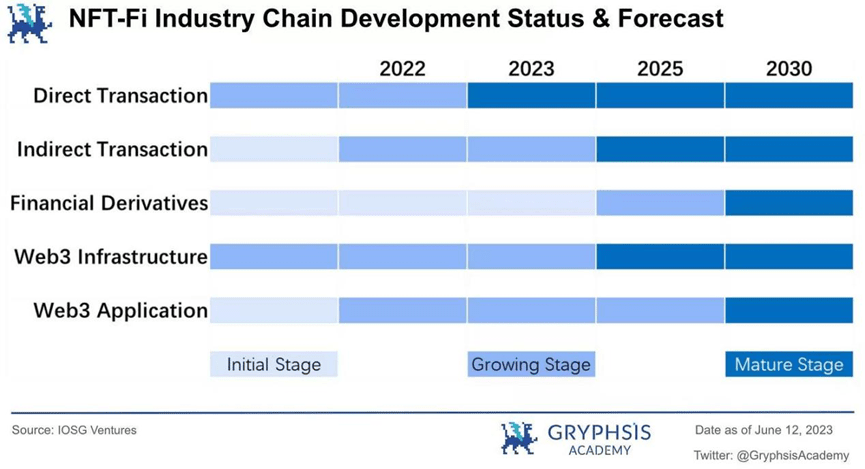

The financialization of NFTs has helped expand and enhance the consensus and demand for NFTs through financial means. The industry structure can be vertically divided into three layers:

1) Direct trading: This includes trading markets, aggregators, and automated market makers (AMMs) for cryptocurrency value exchange. Representative projects include Opensea and Blur.

2) Indirect transactions: This includes NFT mortgage lending, financing custody and other related services. Representative projects include BendDAO and ParaSpace.

3) Financial derivatives: These include options, futures, indices and other high-leverage trading products with associated risks. Representative projects include Openland.

Since direct trading is relatively mature, while financial derivatives are still in the early stages, the intermediate level involving deposits, loans, and borrowing has the basic characteristics of the financial system and is currently developing rapidly. Therefore, this article will focus on the current focus of indirect NFT trading direction - NFT lending.

2. Industry market value

First, let’s answer a question: Why is there a demand for the NFT lending market?

As we all know, NFT is the abbreviation of non-fungible token, which refers to a unique crypto asset that cannot be copied or replaced. NFT has the characteristics of being unique, indivisible and irreplaceable. The pricing of NFT is mainly based on personal subjective judgment or collective consensus.

However, due to these characteristics, despite the inherent aesthetic and collectible value of NFTs (as well as potential project utility), they generally face a limited audience compared to ordinary fungible cryptocurrencies. The lack of a standardized benchmark to assess the value of NFTs generally leads to their relatively poor liquidity in the overall cryptocurrency market.

Generally speaking, NFT investors hope to profit by selling NFTs when the price rises. However, this approach is greatly affected by the current market environment. In the bear market situation of the Web3 ecosystem, market confidence is low, trading activities are inactive, and liquidity is further shrunk. Therefore, in most cases, these NFT assets remain idle, resulting in extremely inefficient use of funds. Without lending services, users may be forced to sell their unique NFTs to obtain much-needed liquidity.

NFT lending is a financial product that occurs during the holding period of NFTs. Its core mechanism is to allow holders to borrow short-term funds without selling NFTs. By using their NFTs as collateral, they can obtain liquidity in the form of cryptocurrency or legal currency, while enjoying the benefits of holding NFTs and making profits, thereby improving the efficiency of capital utilization.

As a solution to the NFT liquidity problem, the demand for this innovative market is increasing. NFT liquidity solutions with good user experience and sustainable trading models will emerge quickly in the entire NFT-Fi field.

3. Industry barriers

The industry barriers to NFT lending business mainly revolve around the feasibility of realizing the core business model, mainly including:

1) Effective NFT lending demand user matching system

Due to the unique nature of NFT, users usually need to have specific assets and relevant financial knowledge to connect NFT assets to lending services. Designing an attractive business model that attracts lenders and borrowers is crucial to effectively matching user needs.

2) Reasonable pricing mechanism for NFT assets

Pricing is a key component of the NFT lending business. When estimating the value of NFT assets, calculating factors such as loan-to-value ratio (LTV) and liquidation system, a system that can provide fast and reasonable quotes is essential for the NFT lending business. As the number of users within the protocol increases and the demand for services continues to grow, the quote mechanism, data tracking and update efficiency directly affect the overall customer experience.

4. Competitive landscape

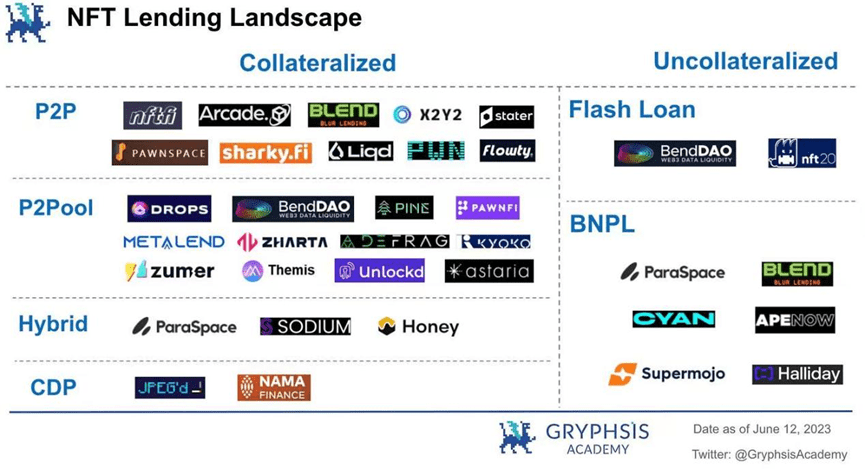

In the current NFT lending business, there are mainly two categories: mortgage lending and non-mortgage lending.

Mortgage lending can be categorized based on its agreement type:

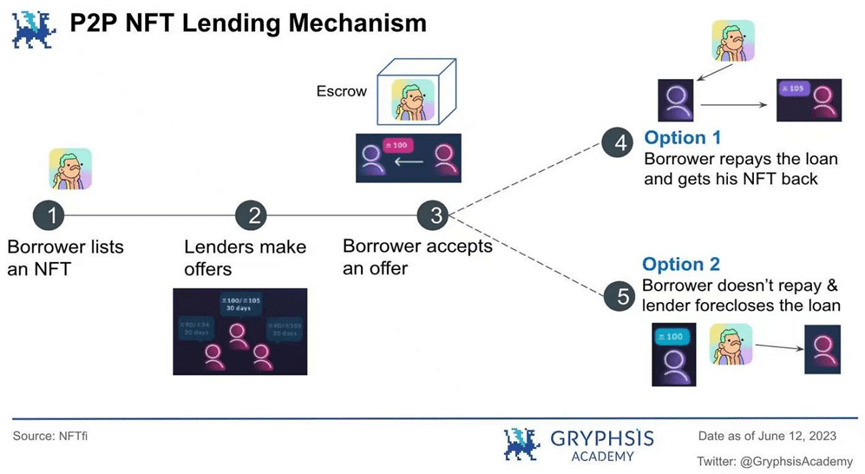

1) Peer-to-Peer (P2P)

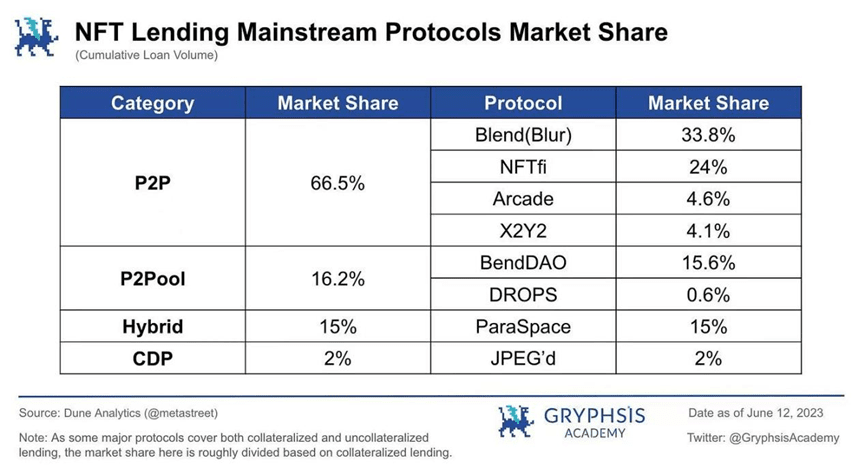

The model involves direct lending between users, where lenders and borrowers are matched in terms of interest rate, loan term, NFT collateral type, etc. Once the demand is matched, the lending transaction is executed. Representative projects: NFTfi, Arcade, Blur (Blend).

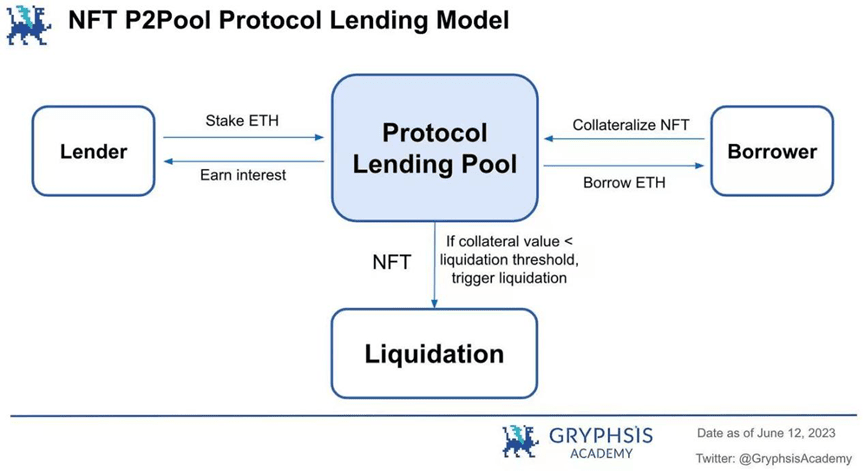

2) Peer-to-peer pool

This model involves lending between users and protocol pools. Lenders provide NFTs as collateral to the protocol pool to quickly obtain loans, while depositors provide funds to the protocol pool and earn interest. Representative projects: BendDAO, DROPS.

3) Mixed Type

This model combines elements of P2P and peer-to-pool protocols. In this model, lenders set parameters such as interest rates, loan terms, loan amounts, etc. When requesting a loan on the platform, it is equivalent to creating a separate protocol pool. Multiple borrowers can deposit funds into the protocol pool to earn interest income. Representative project: ParaSpace.

4) Collateralized Debt Position (CDP)

Introduced by MakerDAO, it is considered the ultimate model for NFT collateral lending. Representative project: JPEG’d.

Unsecured lending can be further divided into:

1) Buy Now Pay Later (BNPL) Representative projects: CYAN, ParaSpace, Blur (Blend).

2) Flash loan representative project: BendDAO.

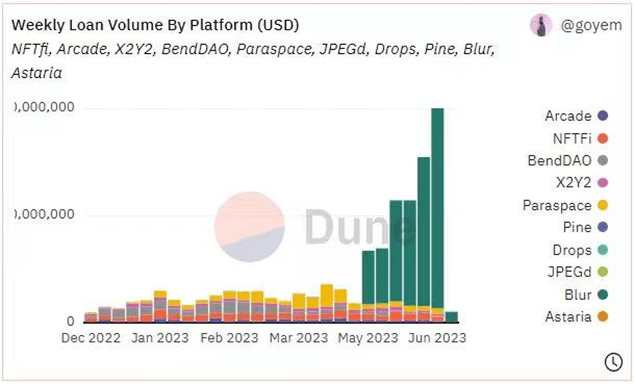

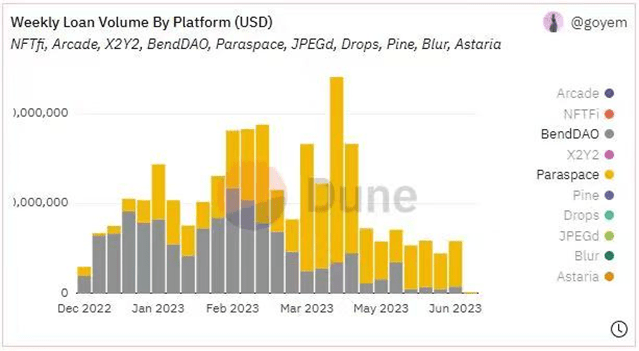

As can be seen from the above two charts, both peer-to-peer (P2P) protocols and peer-to-pool protocols dominate the NFT lending market in terms of lending volume.

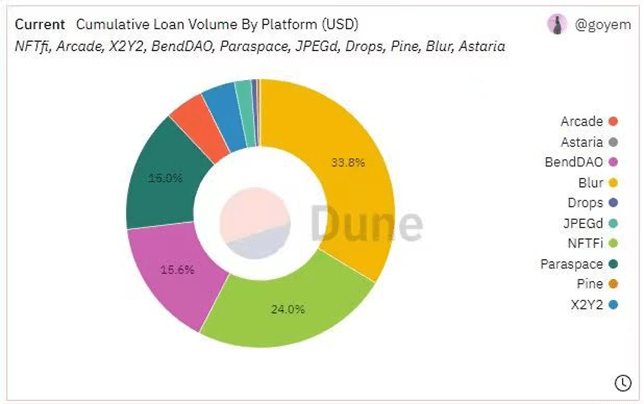

Notably, since Blur launched Blend in May, it has quickly taken the lead among mainstream lending protocols. Benefitting from Blur's status as the leading NFT trading market and its user base, Blend's trading volume has always been significantly higher than the other protocols combined. Currently, its cumulative loan volume ranks first in the industry.

5. Technical implementation path and advantages and disadvantages Based on the different protocol types of NFT lending business mentioned above, each type has its own unique characteristics.

5.1 Mortgage lending

5.1.1 Peer-to-Peer (P2P)

In P2P lending, the user valuation method is mainly used, that is, the pricing of NFT is based on the price estimate provided by the user. The user gives a specific quote based on the uniqueness of each unique NFT. It has the following characteristics:

Inefficiency: The matching process between lenders and borrowers can take a long time.

Valuation is relatively reasonable: NFTs in the same series may have different values based on their attributes. Lenders and borrowers can negotiate and determine valuations based on the attributes of individual NFTs instead of using a unified reserve price for the entire NFT series.

High security: If an individual defaults, it will only affect the lender and borrower involved in the specific loan, without spreading the risk to other users on the platform.

Support various types of NFT collateral: Since it involves direct quotes between users, theoretically any NFT series can be used as collateral for borrowing.

Summary: The P2P model is more suitable for bear markets with low liquidity because it is less susceptible to extreme market conditions that could affect the security of the platform.

5.1.2 Peer-to-peer pool

Time-weighted average prices (TWAPs) are widely used in peer-to-peer lending protocols. Oracle solutions like Chainlink can obtain and publish the time-weighted average price of sales and reserve prices, creating a hybrid price to evaluate the value of NFTs. By taking the average of multiple prices over a predetermined period of time, this model reduces the impact of abnormal prices on prices, making it more difficult for prices to be maliciously manipulated.

It has the following features:

High efficiency: Users can interact directly with the lending pool and borrow and lend at any time.

Less accurate valuation: The platform cannot perform detailed collateral valuation based on the properties of each NFT. The valuation is determined based on the reserve price of the NFT series, and the loan amount remains the same for any NFT with the same series, regardless of its specific properties.

Potential security risks: Every loan on the platform affects the interests of all depositors on the platform. In extreme cases, large-scale NFT liquidations may bring systemic risks.

Only a limited range of NFT collateral is supported: For security reasons, only blue-chip NFTs with high trading volume, good liquidity and relatively stable prices are supported as collateral.

Summary: The peer-to-pool model is more suitable for a bull market with sufficient liquidity.

5.1.3 Hybrid

The basic lending mechanism in the hybrid protocol also adopts a peer-to-pool model. Users can obtain liquidity as a borrower by pledging NFTs in real time, or they can provide liquidity as a lender and earn interest. The innovation lies in the introduction of a cross-margin credit system, rather than the independent margin pool design used by existing platforms, which allows users to use one credit line to provide loans against all collateral. Let's illustrate with an example: Suppose you own 61 Bored Ape Yacht Club (BAYC) NFTs, and you decide to borrow 5 NFTs as collateral and then buy another NFT. Using existing lending protocols and their independent margin models, you need to borrow ETH separately with each BAYC NFT and then buy a new BAYC NFT on the market. There are at least two disadvantages to this process:

1. User experience: Users need to perform 5 separate on-chain transactions and manage 5 separate lending positions.

2. If any of your loan positions are at risk of liquidation, you need to repay the loan immediately to avoid being liquidated. However, in a hybrid protocol, by pledging NFT assets, you generate a credit line and a health factor for your entire collateral portfolio. As long as the health factor of your entire collateral portfolio remains above 1, none of your NFTs will trigger a liquidation auction. To mitigate the risk, you can choose to deposit more collateral (NFTs or ERC-20 tokens) to maintain a high health factor. The credit system is similar to a valuation system that determines the value of all collateral based on the assessment and automatically approves the loan. As long as your collateral falls within the range of collateral types supported by the credit system, you can borrow based on its total value. This is called a cross-margin full-position leverage model. Simple and easy to understand, this model provides greater operational convenience over the standard peer-to-pool model. 5.1.4 Collateralized Debt Position (CDP)

After users pledge their NFTs in the repository, they can withdraw the corresponding protocol tokens. The CDP project protocol allows debt positions of protocol tokens up to a certain percentage of the collateral value and charges an annual interest rate on them. When a user's debt/collateral ratio exceeds the liquidation threshold, the DAO performs liquidation. The DAO repays the debt and retains or auctions the NFTs to build its repository.

Users can purchase insurance against liquidation when borrowing, paying a one-time, non-refundable fee proportional to the loan amount. With insurance, users have the option to repay the debt themselves within a specified time after liquidation (with an additional penalty).

CDP loans are a good option for those who need liquidity from their blue chip NFTs but want to avoid high interest rates. 5.2 Non-collateralized loans 5.2.1 Flash loans (down payment purchases)

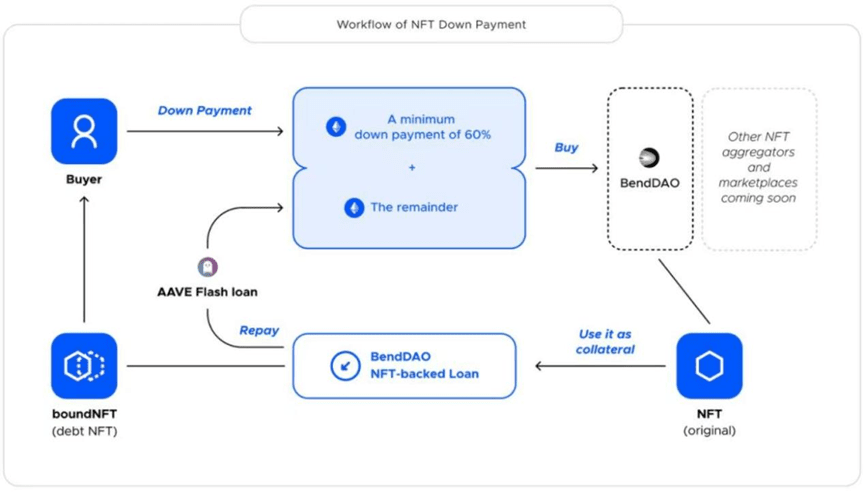

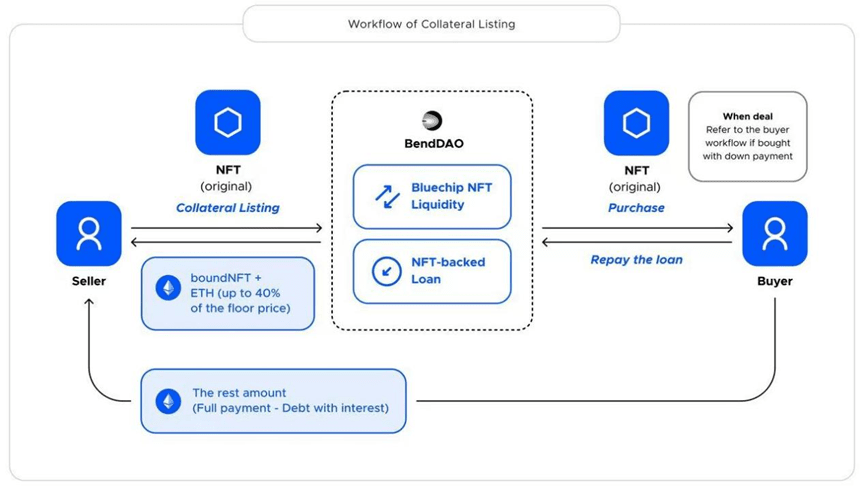

Flash loans (down payment purchases) are a variation of traditional loans. Users can pay a certain down payment on the protocol to purchase NFTs listed on the trading market. The rest of the funds come from third-party DeFi protocols (such as Aave) that provide flash loan services. After the buyer uses the down payment and the remaining funds obtained through the flash loan to purchase the NFT, they own the NFT and mortgage it on the NFT loan protocol. The protocol's funding pool returns the borrowed funds to the flash loan, and the remaining interest calculation, repayment mechanism, and liquidation mechanism are based on the provisions of the loan agreement. When the listing price exceeds the reserve price on the protocol, the down payment ratio increases. Fees usually include a down payment fee and a flash loan fee.

The workflow is shown in the following figure:

Source: BendDAO

Source: BendDAO

5.2.2 BNPL (buy now, pay later)

Here is a brief explanation of BNPL from a buyer’s perspective:

1. Bob wants to buy a Pudgy Penguin. He starts a BNPL program on the platform to buy any penguin currently listed on Opensea, LooksRare or X2Y2.

2. The platform offers Bob an installment plan, including a predetermined interest rate that he needs to pay back within three months. Regardless of how the NFT price fluctuates, the installment remains unchanged and fixed over the three-month period.

3. If Bob accepts the plan, he will receive ETH from the platform’s funding pool to purchase NFTs, which will be kept by the platform’s smart contract.

4. When Bob completes all installments, the NFT will be transferred to his wallet and he will have full ownership. (Note: If the NFT appreciates during this period, Bob has the right to repay the BNPL plan early and sell the NFT.)

5. Overdue payments will result in default, and the NFT will be retained in the Vault of the corresponding platform for liquidation. The BNPL function provides a "pawnshop" service, allowing users to temporarily exchange NFTs for loans as collateral. The loan is then repaid together with interest, which flows directly into the funding pool. In order to reduce planned defaults, the platform takes various risk management measures, such as regulating loans and preventing the holding of high-risk NFT products by setting higher interest rates.

We can see that the business model of unsecured loans, whether it is flash loans (down payment purchase) or BNPL, actually involves post-purchase collateral. Users can obtain NFTs with a smaller upfront investment by paying a partial down payment, and then repay the corresponding loan within a specified period of time. This model is suitable for NFT market users who have the intention to purchase but temporarily lack the ability to pay in full.

Therefore, the characteristics of this loan model include:

Reasonable use of capital, allowing users to make early purchases with smaller upfront investments, reducing financial pressure

A reliable credit assessment system is needed to assess the risk of each transaction through credit assessment

Risk control models need to be validated, especially in the early stages of a product. Effectively managing risk and maintaining business health is critical as user adoption increases.

6. Revenue Model

Generally speaking, the main sources of income for NFT loan protocols include: (1) interest paid by users for mortgages; (2) loan fees generated from functions such as flash loans; and (3) market transaction fees. The profit model of the NFT loan business mainly relies on loan interest and loan function fees, while market transaction fees are not related to the loan business.

The distribution of project revenue may vary depending on the protocol design. This may involve different proportions of distribution between project finances and token holders/users.

7. Industry Valuation

We can use a top-down valuation approach and make an analogy with the DeFi loan market. The growth logic is mainly based on the expectation that the NFT market size will continue to grow with the overall development of the Web3 industry. Since NFT loans are still in their early stages, the entire industry still has considerable room for growth.

7.1 Valuation Assumptions

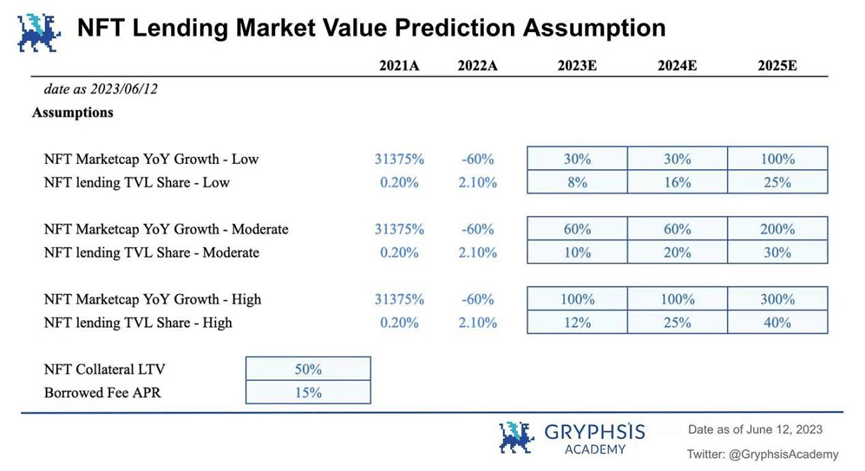

The cryptocurrency market is cyclical and is currently in a bear market, and the size of the entire NFT industry will fluctuate with the market cycle. However, the penetration rate of NFT loans (total locked value, TVL) is expected to increase relatively quickly.

(a) Annual growth rate of market value

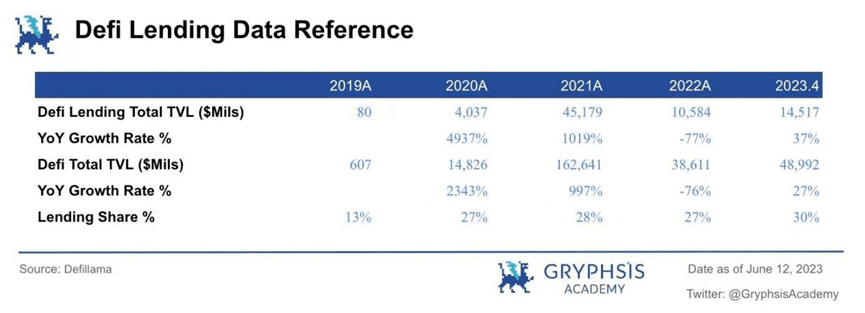

Looking back at the evolution of the DeFi lending market from 2019 to the present, we can see that the industry expanded rapidly in the first two years, and the market environment was relatively stable. Due to the small initial market size, the total market size was able to experience substantial growth, doubling several times. However, due to the sluggish market, in 2022, the total market value entered a clear period of contraction. The NFT market has also experienced a similar trajectory over the past two years. Entering this year, the total market value of the DeFi market shows signs of rebounding from the lows of 2022. If this recovery maintains a steady pace, we expect this year to make up for last year's decline. Therefore, we predict an overall industry growth rate of 60% for the NFT market this year. Taking into account the cyclical nature of bull and bear markets, we expect 2024 to be a period of fairly stable growth with a growth rate similar to that of 2023, while 2025 is expected to be a period of rapid growth in the bull market, with a growth rate three times that of the stable period. We regard these assumptions as medium cases. The pessimistic case assumes a medium-case growth rate of 50%, while the optimistic case proposes more ambitious expectations based on the medium case.

(b) NFT lending TVL share

Considering the historical penetration rate of lending business within the entire DeFi market, which has been around 25% to 30% in the past three years, we can estimate that by 2025, NFT lending TVL will reach a similar lock-up ratio, assuming a medium case of 30%, a pessimistic case of 25%, and an optimistic case of 40%.

(c) NFT mortgage value ratio

Based on the mortgage value ratio data of multiple mainstream NFT lending protocols, the valuation is assumed to be 50%.

(d) Annual interest rate for loans

Referring to the interest rates of DeFi lending and current NFT lending, it is assumed that the annual interest rate of NFT lending is 15%. 7.2 Market Value Prediction

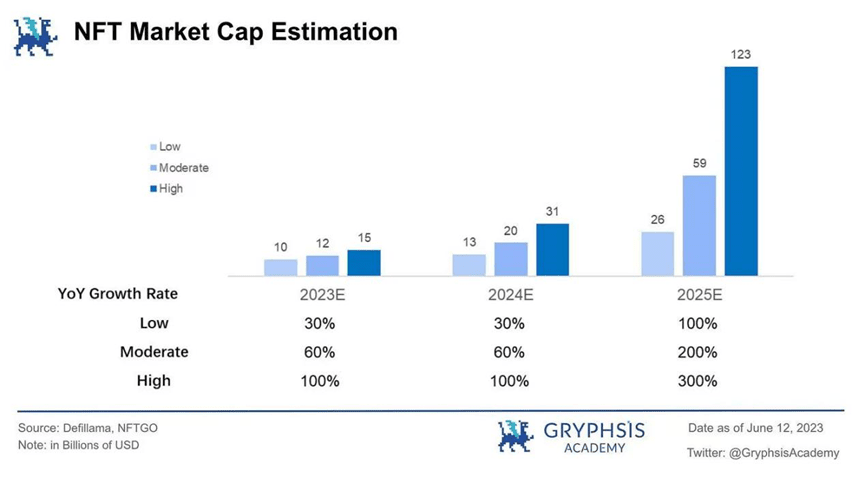

Based on the medium assumptions in our valuation forecast model, we assume steady growth in overall NFT industry market capitalization in 2023/2024 (60% annual growth), and significant growth in 2025 (200% annual growth) due to a potential bull cycle ). NFT lending TVL is assumed to be 30% of the total industry market capitalization. The mortgage loan-to-value (LTV) ratio is set at 50%, and the loan's annual interest rate is assumed to be 15%.

Based on the above assumptions, it is expected that in the next three years, the overall market value of the NFT industry will be about US$60 billion, and the TVL of NFT lending will reach about US$18 billion. This can meet the loan demand of about US$9 billion (assuming an average mortgage-to-value ratio of 50%). The total revenue in the NFT lending field is expected to reach US$1.3 billion, or nearly RMB 10 billion (based on an average annual interest rate of 15%).

Note: The income mentioned here only considers loan interest as the main income. Based on the historical lending data of major NFT lending platforms (interest rates are mainly concentrated in the range of 15% to 30%), and considering the evolution trend of DeFi lending rates, it is assumed that the average annualized interest rate of NFT lending is 15%.

8. Main companies/protocol products

8.1 Peer-to-Peer

8.1.1 NFTfi

NFTfi.com is a mature P2P NFT lending platform that operates in an auction-style format. Lenders and NFT collateral providers jointly determine the bid price, interest rate calculation, and term. It is one of the leading platforms in the P2P lending business.

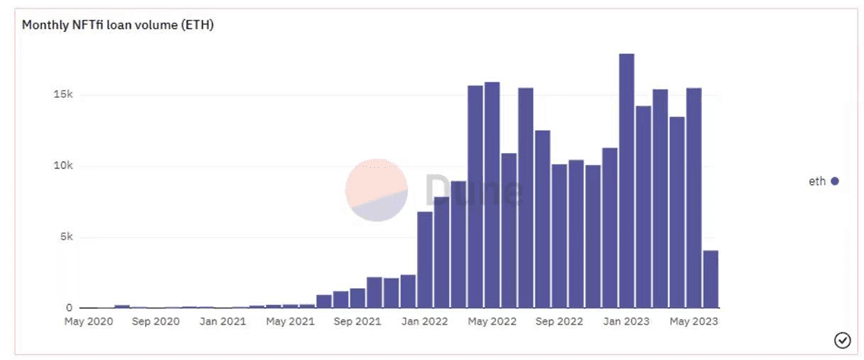

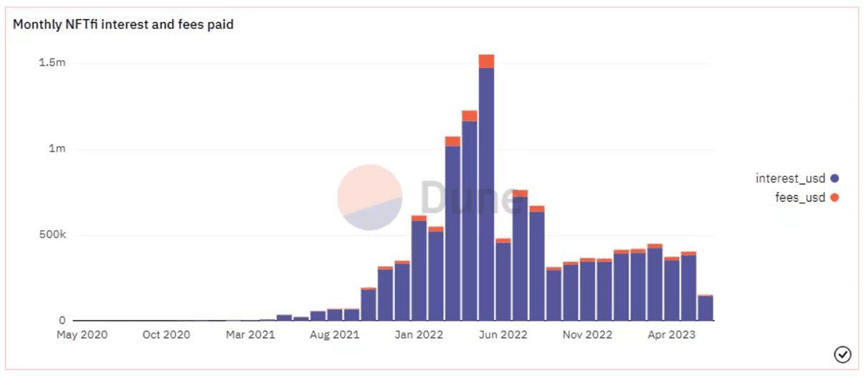

Since its launch in 2020, it has facilitated over 45,000 loans with a total loan amount of approximately $450 million (as of the end of May 2023). Monthly Ethereum loan volume has consistently remained above 10,000 ETH since April 2022, peaking at nearly 18,000 ETH in January 2023. From March to May 2022, monthly revenue exceeded $1 million, peaking in May at over $1.5 million.

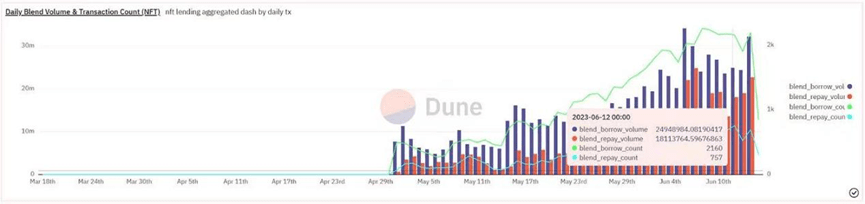

Source: Dune Analytics (@rchen8) June 12, 2023

Source: Dune Analytics (@rchen8) June 12, 2023

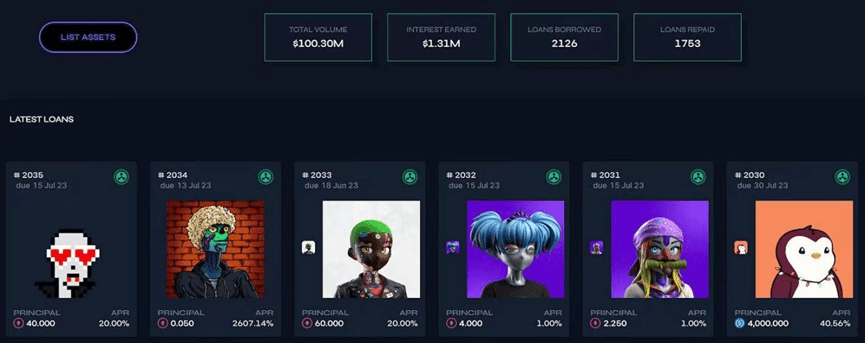

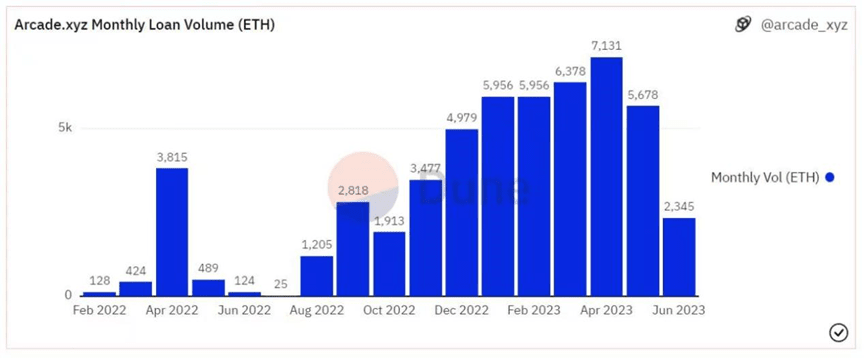

8.1.2 Arcade

Arcade is another P2P platform that provides NFT liquidity loans and is the successor to Pawn.fi. The project is built on the Pawn protocol, an infrastructure layer for NFT liquidity that consists of a set of smart contracts deployed on the Ethereum blockchain to financialize non-fungible assets. NFT holders can use their assets as collateral to apply for loans through the Arcade application, which enforces the specified loan conditions.

Source: Arcade (June 12, 2023)

Source: Arcade (June 12, 2023)

The platform creates a wrapped NFT (wNFT) through a smart contract, which represents the borrower’s collateral for the loan application. The wNFT is locked in an escrow smart contract, which records the time when funds are remitted to the borrower and repaid to the lender.

As of June 12, Arcade has facilitated more than 2,000 loans with a loan value of approximately $100 million. Monthly loan volume has been above 5,000 ETH for the past six months. Cumulative income from loan interest has exceeded $1.3 million.

8.1.3 Blur (Blend)

Leading NFT trading platform Blur partnered with Paradigm to launch Blend in May. Blend is a P2P NFT lending protocol that includes the ability to use loans to purchase NFTs. Blend’s core features include:

Perpetual P2P lending with no expiration date or need for an oracle.

Lenders define loan amounts and post offers with specific annual percentage yields (APYs), and borrowers select an offer.

If the lender withdraws, the borrower must repay the loan or borrow again within 30 hours, otherwise liquidation will occur.

The borrower can repay the loan at any time.

It supports the “buy now, pay later” (BNPL) model, where the borrower pays a deposit first and then borrows money to purchase NFT.

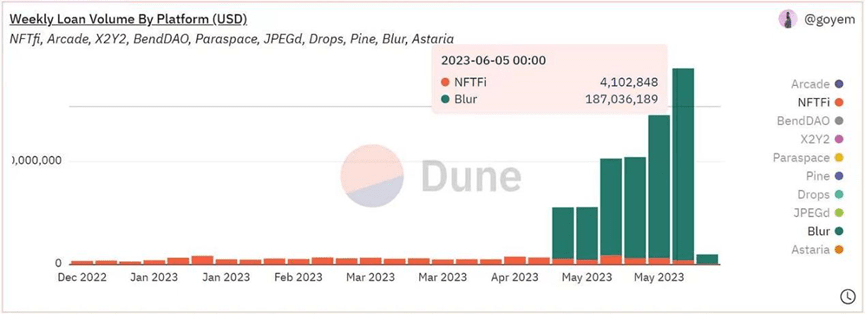

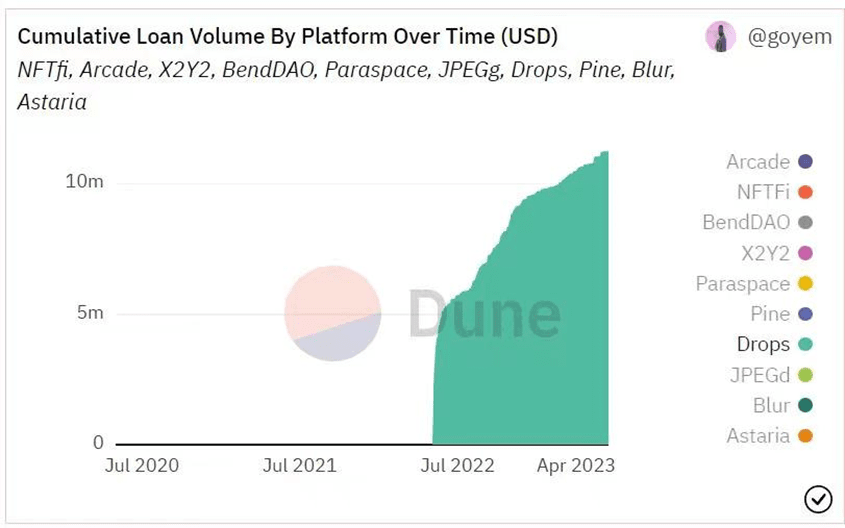

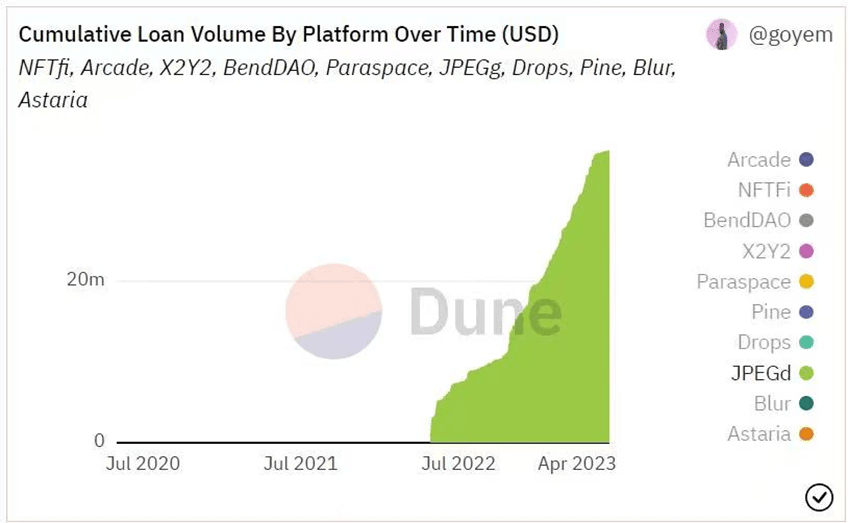

Blend's core advantage is to unify non-essential elements, reduce system complexity, and allow flexible migration of lending relationships within the system. Pricing risks and benefits are determined through market dynamics to maximize user satisfaction. Compared with the traditional P2P model, Blend improves the liquidity problem of lenders by unifying the loan period into a flexible permanent model. Blend unifies lender exit and liquidation, and the oracle determines the time of liquidation. Lenders can choose to exit to achieve flexible processing. Blend has achieved significant improvements by unifying non-essential elements in the traditional P2P lending model and widely integrating them into the Blur trading module. Shortly after its launch, Blend has gained market recognition, and its loan volume has grown rapidly, surpassing NFTfi as early as early May.

Since its launch in early May, Blend has achieved nearly 50,000 transactions in just over a month. The total loan amount has exceeded US$700 million, and the cumulative number of users is nearly 20,000. In June, compared with May, the business continued to grow, with an average of about 2,000 lending transactions per day, and the daily loan amount has been exceeding US$20 million. The peak was reached on June 6, with a single-day loan amount of US$34 million. (Data as of June 12)

Source: Dune Analytics (@goyem) June 12, 2023

Source: Dune Analytics (@goyem) June 12, 2023

8.2 Peer-to-peer pool

8.2.1 HeadDAO

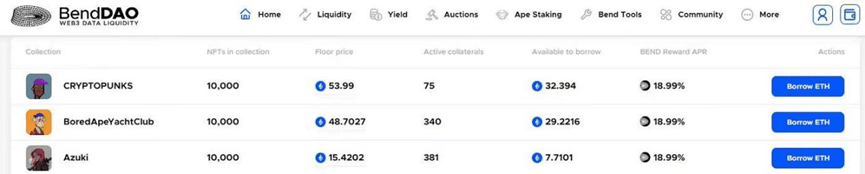

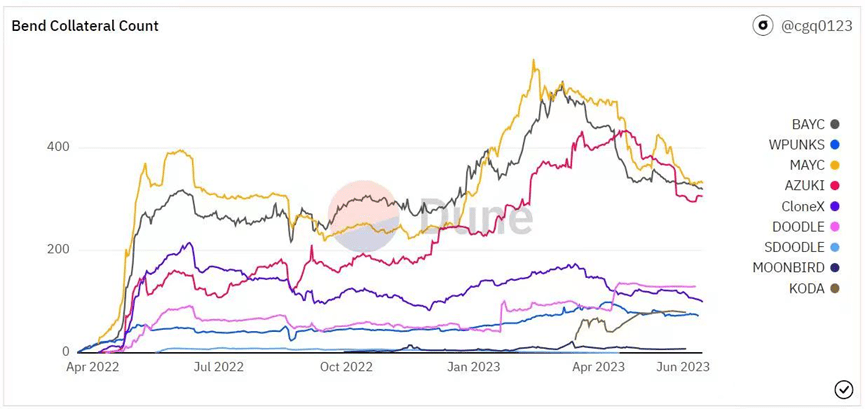

BendDAO is a leading protocol that pioneered the "peer-to-pool" NFT lending model in the field. It mainly serves blue-chip NFT holders. Lenders (peer-to-peer) can quickly borrow from the fund pool (pool) by pledging blue-chip NFTs, while depositors (peer-to-peer) provide Ethereum to the fund pool (pool) and obtain interest denominated in ether. Both lenders and borrowers will be rewarded with BEND tokens. When the price of the pledged NFT drops to a certain level, liquidation will be triggered. Currently, BendDAO supports the pledge of 10 mainstream blue-chip NFTs.

BendDAO UI:

The number of BendDAO blue chip NFT materials:

The lowest price data for NFTs is obtained through the Bend Oracle, which BendDAO developed in collaboration with Chainlink. The Oracle retrieves the lowest price raw data from Opensea, X2Y2, and LooksRare, filters the data based on transaction volume to calculate the low price, and uses TWAP (time-weighted average price) to ensure that the data is not manipulated.

Since its launch in March 2022, the protocol has continuously updated and iterated its features to meet market demand. In addition to its main lending business, BendDAO has also launched a built-in market that supports new features such as "flash loans" and "collateral listings", as well as "peer-to-peer" lending functions and "Bend Ape Staking", an asset pairing function designed specifically for Yuga Labs' staking.

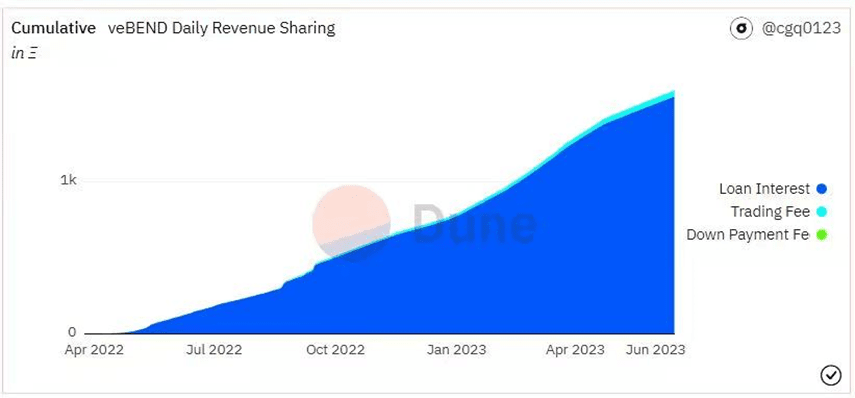

In terms of revenue sources, BendDAO’s revenue mainly comes from

(1) Interest on loans;

(2) Flash loan fees (buyers pay a 1% rate), which is related to the lending business.

Revenue also includes market transaction fees (sellers pay a 2% fee), but is not related to lending operations. Revenue allocated to the protocol treasury includes:

(1) 30% of the interest paid by the borrower;

(2) 50% of the flash loan fee.

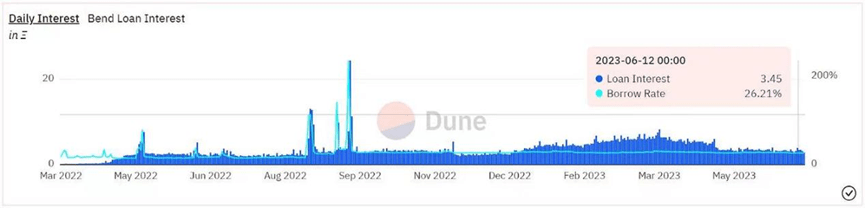

As of June 12, BendDAO has lent over 170,000 ETH, reaching a peak daily lending volume of 4,340 ETH in May. The project has a total revenue of 1,669 ETH, of which lending interest income is approximately 1,563 ETH, accounting for approximately 94% of the total revenue. The main collateral assets in this peer-to-pool model are BAYC/MAYC/Cryptopunks, accounting for more than 70% of the number of collateral assets. Since the beginning of this year, the lending APR has been in the range of 25-30%, and the daily interest income is between approximately 3-6 ETH.

8.2.2 DROPS

DROPS operates a money market similar to Compound, where users can pledge their NFT portfolio to obtain USDC and ETH loans. NFT prices are determined by Chainlink oracles, which adjust prices based on outliers and averages over a certain period of time.

Similar to Compound and Aave, DROPS uses a piecewise interest rate function that targets specific utilization rates. When withdrawals are insufficient, borrowers will pay significantly higher interest rates.

To limit the risk of liquidity providers, DROPS divides the protocol into isolated pools, each with its own NFT collection. This approach is similar to what Fuse does on Rari Capital, ensuring that borrowers can choose the collection they are happy with.

As of June 12, DROPS has accumulated more than $11 million in loan funds.

8.3 Mixing

8.3.1 ParaSpace

ParaSpace is an NFT lending protocol that uses a peer-to-pool model as the underlying layer, allowing users to pledge and borrow NFTs and fungible tokens. It enables users to wrap their ERC-721 or ERC-20 token assets, pledge them, and borrow funds, using underutilized capital to improve the efficiency of their on-chain assets and earn returns.

ParaSpace's innovative collateral lending model pioneered the first cross-margin credit system, a different approach from the segregated margin pool design adopted by existing platforms. This allows users to use a single line of credit to provide loans against their entire collateral portfolio.

By pledging your NFT assets to ParaSpace, you can generate a credit line and health factor for your entire collateral portfolio. As long as the health factor of your entire collateral portfolio remains above 1, none of your NFTs will trigger a liquidation auction.

The credit system is like a valuation system, based on which loans are automatically approved. As long as they are collateral types supported by ParaSpace, you can borrow based on their total value.

This is achieved through a cross-margin fully leveraged model.

In addition, ParaSpace has designed features such as a “hybrid Dutch auction” liquidation mechanism, delayed payments within a “buy now, sell now” credit system, higher limits on high-rarity NFT lending, and borrowing for short sales to meet the needs of current NFT market users.

Since its launch in December 2022, ParaSpace has experienced rapid growth, with a growth rate significantly higher than the overall NFT lending market and exceeding BendDAO's lending volume in the past six months. As of June 12, the protocol had a cumulative loan size of nearly $300 million and more than 13,000 users. It reached a peak lending size of more than $20 million per week in April, and the weekly lending size has remained at around $5 million in the past month.

8.4 Collateralized Debt Position (CDP)

8.4.1 JPEG’d

JPEG’d is an improved NFT P2Pool lending protocol that adopts MakerDAO’s CDP (collateralized debt position) model. Users of the protocol pledge NFTs and borrow stablecoins PUSd based on the pledged NFTs, with a maximum loan amount of 32% of the NFT’s reserve price. In JPEG’d, the first batch of NFTs that can be used as collateral are CryptoPunks, with an initial annual interest rate of 2% and a one-time borrowing fee of 0.5%. JPEG’d sets the loan-to-value (LTV) ratio to 32%, triggering liquidation when the LTV reaches 33%.

Due to the significant volatility of NFT reserve prices, JPEG’d uses Chainlink as its data source, with the core being the time-weighted average price (TWAP). Notably, JPEG’d has designed a novel insurance mechanism where users can choose to pay a 5% insurance premium for their loans. In the event of a liquidation, they can choose to repurchase their NFT within 72 hours after paying off their debt, interest, and a 25% liquidation penalty. Otherwise, the NFT will be owned by the JPEG’d DAO.

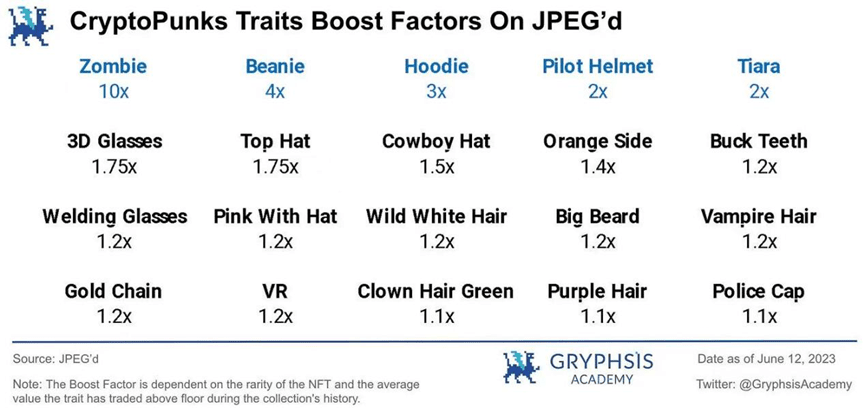

Another innovation of JPEG’d is that it provides platform-defined weighted valuations for specific blue-chip NFTs such as CryptoPunks, Bored Ape Yacht Club (BAYC), and Azuki. For each rare trait that receives a different weight, the valuation will receive a corresponding reward to increase the driving factor of the trait. Currently, relatively few platforms in the market provide valuations based on rare traits.

In addition, the pETH generated from JPEG’d can be staked on Convex to get a relatively good return. At the beginning of 2023, the yield of the ETH-pETH asset pair has reached about 30-45%.

As of June 12, 2023, the protocol has accumulated more than $36 million in loans. The highest weekly loan amount from January to February this year was about $770,000. CDP-based NFT lending protocols still hold a relatively small market share.

9. Risks and Outlook

At present, although the NFT lending industry is developing rapidly, there are some key risks that cannot be ignored: 1) NFT collateral valuation fluctuation risk (credit risk)

For a lending project, the worst case scenario is that the liquidity of the fund pool dries up and the borrower is unable to repay the loan due to bankruptcy. For NFT lending protocols, it is crucial to identify high-quality NFT collateral assets.

When the reserve price of the collateral NFT series drops sharply, many borrowers may choose to default on their loans and abandon their NFT assets. In this case, the NFT with collapsed prices may have no bidders in the auction.

(Review of historical events - BendDAO liquidity crisis: From August to September 2022, the reserve prices of blue-chip NFTs generally fell, resulting in the liquidation of several mortgaged assets but no bidders. This triggered market panic and caused the liquidity of the funding pool to dry up. Loan and deposit rates soared, bringing a potential collapse crisis to the BendDAO protocol. In order to resolve the crisis, the team proposed some suggestions for modifying parameters. As funds gradually flowed back to the protocol's pool in the next few days, market sentiment stabilized, and utilization and loan rates returned to normal levels.) 2) Concentration of target user groups

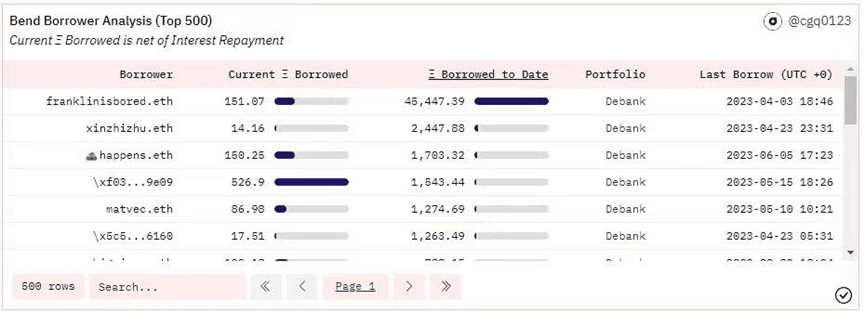

Although the industry is developing rapidly, the current NFT lending business does not have a broad user base. Data from some projects show that the scale of the business mainly depends on a small number of key users.

Example:

BendDAO Protocol: As of June 12, 2023, the total loan amount reached 178,820 ETH, and the user with the largest loan amount, Franklinisbored.eth, accounted for more than 25% of the total business volume, with a loan amount of 45,447 ETH.

3) The growth potential of the market size may be limited

To ensure healthy business development, NFT lending projects often consider high-quality blue-chip NFTs as eligible collateral assets because they have price consensus and strong risk resistance. However, there are a limited number of blue-chip NFT types that meet these criteria, and each project has a fixed supply of NFTs. In the current market environment, identifying additional high-quality NFT collateral assets requires time for market verification and is difficult to predict and evaluate in advance. This may pose a potential risk and may limit the overall market size and business growth potential of the NFT lending industry.

Regarding the overall development of the NFT market, specific categories, including blue-chip PFP (profile portrait) NFTs, high-quality GameFi assets, and NFT assets empowered by unique projects, are expected to be an important part of the future development of the industry. As the industry matures, more and more users will embrace and invest in the NFT space. The connection between NFTs and real life will become more and more diverse, and through various derivatives, the influence of NFTs will continue to expand. As the total size of the NFT market grows, opportunities in various specific areas within the NFT space will also increase. For NFT lending, the diversity of various protocols can meet the needs of different users. When lending protocols achieve high activity and widespread adoption, they will be able to provide better liquidity solutions, benefiting NFT and DeFi users.

10. Conclusion

In the current NFT market, most users are still concentrated in areas with the lowest entry barriers, such as markets and aggregators. However, these areas have not yet fully demonstrated the maximum efficiency of capital utilization. As more users join the NFT field, how to effectively improve market efficiency and attract user attention through NFT financialization may be a continuous breakthrough point for Web3 business growth.

As an important part of NFT financialization, NFT lending has gradually demonstrated its efficiency advantage over the P2Pool model in the competition with the P2P model, due to the improvement of oracle and liquidation mechanisms. The continuous updating and iteration of different products are shaping the maturity of the market's product landscape. How to independently rate and accurately price different NFT assets, as well as key issues such as establishing liquidity are crucial to improving customer experience.

We believe that NFT liquidity solutions with reasonable pricing mechanisms, seamless user experience, sustainable trading models and profit models, and comprehensive risk control mechanisms will become the cornerstone of the advancement of the NFT-Fi industry.

references:

Official website for each NFT lending protocol

The Ultimate Guide to NFT-Fi

NFT and DeFi: Lending Market

Explained: NFT loans and how they work

ParaSpace Pt.1 Introduction - Universal Liquidity, Instant Unlock

The road to NFT financialization

2022 Semi-annual Report

The State of Cryptocurrency Report 2022

2022 Digital Asset Outlook

Dune Analytics (@cqg0123)

Dune Analytics (@metastreet @goyem)

Dune Analytics (@rchen8)

Dune Analytics (@arcade_xyz)

Dune Analytics (@impossiblefinance)

Dune Analytics (@beetle)

statement:

This report is the original work of @enginezyq, an intern at @GryphsisAcademy, under the guidance of @CryptoScott_ETH and @Zou_Block. The author is responsible for all content, which does not necessarily reflect the views of Gryphsis Academy or the views of the organization that commissioned the report. Editorial content and decisions are not influenced by readers. It is worth noting that the author may own cryptocurrencies mentioned in this report.

This article is for informational purposes only and should not be used as the basis for an investment decision. It is strongly recommended that you conduct your own research and consult with a neutral financial, tax or legal advisor before making an investment decision. The past performance of any asset does not guarantee future returns.