Author: c-node Translator: Cointime Lu Tian

In recent months, the DeFi ecosystem for alt-L1s has dried up. The community believes that the reason for this is the lack of tokens that people want to trade, and people have been calling on developers to launch more tokens, such as protocol governance tokens or meme coins.

My view is that L1 tokens are the only tokens that can be invested in, and DeFi protocols should not launch their tokens. Protocols with governance features are the worst protocols, and protocols that minimize governance features are generally better. You may disagree with this view, for example, worrying about contract immutability, changing risk parameters, or managing oracles. You may also think that protocol developers need the asymmetric advantages of token launches as an incentive to build, or that they need to raise money from venture capital through token sales. In any case, I hope this article will dispel all your concerns.

Without a flood of new tokens, how can DeFi be saved?

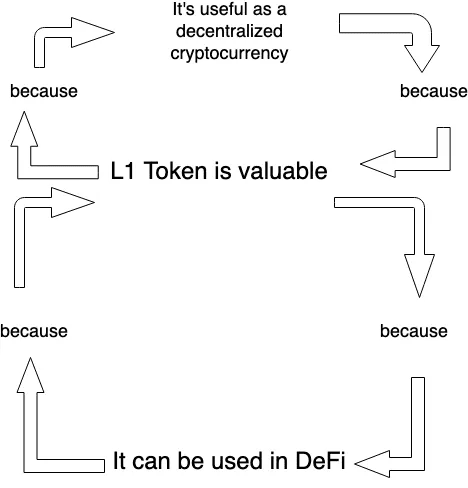

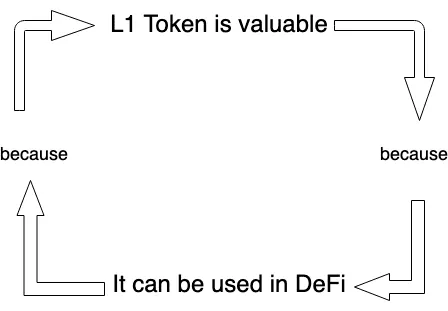

The best thing for the on-chain DeFi ecosystem is a strong L1 token. Some people argue that deflationary economics is bad because it "encourages saving and discourages use". This is incorrect because in blockchain and DeFi, IS is used to be saved. Long holders of L1 tokens are some of the top users of the Ethereum DeFi ecosystem.

Users lock their long positions on-chain, often using DeFi to gain liquidity by collateralizing decentralized stablecoins, synthetic assets, and derivatives positions. DeFi allows them to do this without the centralization risk of holding their long positions on exchanges or lending platforms like Celsius, or bridging to other specialized chains elsewhere. This solves a major problem because they can self-custody their long positions while doing a lot of useful and interesting things with it… a great option for long-term L1 holders.

One could argue that DeFi is useful even without a strong native token. It’s true that you can use DeFi with wrapped and bridged assets, but without self-custody it’s not as useful as DeFi with native assets. You might be thinking “you can still self-custody bridges and wrapped assets”, but there are no trustless cross-chain bridges - remember when SBF stole Bitcoin from Ren and Sollet? Plus, even if you could, if your goal is to be the best place to raise money using non-native assets, you’d have to compete with CeFi and endless new L1s and L2s, possibly with risk subsidy incentives.

Your country’s government could screw up and pass a lax regulatory framework for financial innovation, thereby destroying your value prop. While that day may never come, the possibility should make us think more seriously about the enduring use cases for financial disintermediation.

Some argue that even without self-custody, there are huge benefits to decentralizing other parts of the financial supply chain, such as execution and settlement, and that we benefit from transparency and accountability properties even if we can’t actually force CeFi intermediaries to play by the rules. This is absolutely true, but public blockchains with decentralized validator sets and native crypto tokens are an over-engineered and unnecessarily complex way to achieve that outcome.

What makes a strong native token?

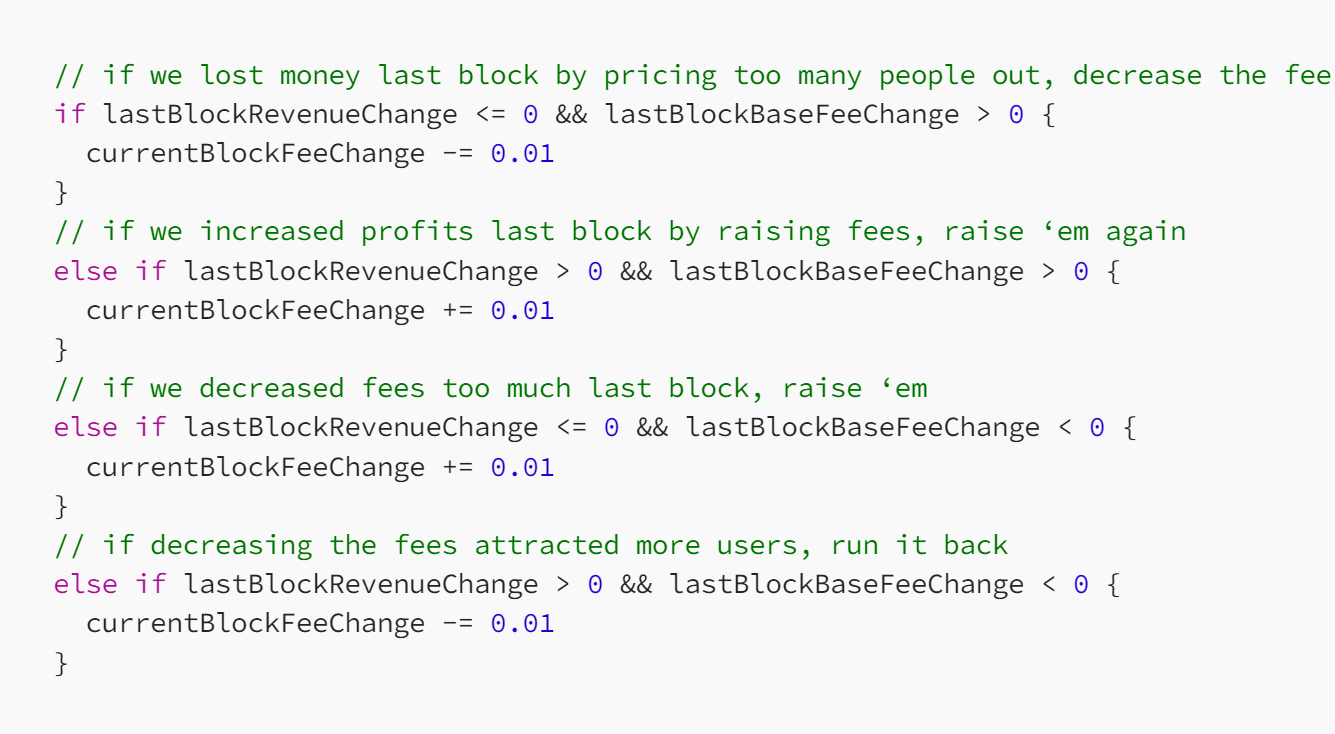

Contrary to the “ultrasound money” ETH memes that celebrate high fees, Aeyakovenko points out that unless fees are kept as low as possible, blockchains will be undercut by competitors. Low-fee blockchains generate revenue by selling priority access to state hotspots at a premium during periods of high competition, while near-zero fees attract developer and user activity, which creates state hotspots and brings more revenue to the chain.

But in reality, blockchains don’t make as much money from these transactions, and the base fee could be raised significantly before anyone flees to a subsidized blockchain in pursuit of cheaper fees. The base fee should be as high as users are willing to pay, but obviously not too high so that people are not priced out.

It’s wise to expect that many users will always flock to the cheapest option, but a blockchain without a strong native token is less useful. A decentralized stablecoin with 1 cent transfer fees is more useful as a cryptocurrency than a centralized stablecoin with zero-fee transfers, because the latter does not rescue users from centralized financial intermediaries and the purpose it serves is unproven and speculative.

The base fee can be priced dynamically so that the chain earns as much revenue as possible from the fees of each block. Control theory should be applied to design such a pricing algorithm. A naive example (designed without any knowledge of control theory) might look like this:

Second, if all value accrues to stakers, rather than unstaked tokens, then all of this valuable natively created value is difficult to use in DeFi. Staked tokens can be reused in DeFi through LST, but there are problems with LST at the moment. Some of the most popular LSTs are closed source and controlled by multi-signatures. Proposals have been made to decentralize LST, but this is a difficult problem to solve because tokens staked by different validators have different risk profiles and corresponding values.

An interesting fact is that if the chain is a sovereign rollup, it does not require validators or staking, and all of its revenue can accrue in unstaked tokens.

Does a protocol need a token to create value?

On-chain governance is inherently plutocracy. Cryptocurrencies should be autonomous and independent, without humans in the loop to rule them. Minimized governance protocols are best. MakerDAO voted to use centralized USDC to make DAI like a CeFi platform, while immutable, ungoverned LUSD perfectly blends the convenience of the dollar with the power of decentralized crypto.

Some protocols like Aave have a DAO that controls important risk parameters. There may be no way to avoid it, but automating these parameters may be possible in some way.

An often overlooked reason against protocols launching tokens is that it creates inconsistency with L1 and creates some perverse incentives for developers. It’s a tired cycle of creating a protocol, launching a token with incentives, having insiders dump, angering the abandoned users, creating resentment, moving on to the next protocol with different insiders, and it’s destroying the space. How many lending protocols are there now? It seems like a new lending and DEX protocol is launched every month. Imagine if every update to Microsoft Word was released as a brand new word processor. It’s getting ridiculous. The real motivation for launching new protocols is rarely to fix problems with previous protocols, but rather to create them because some developer who didn’t become an insider in the last dump wants to be an insider in the next dump-n-carpet.

It would be much better if all DeFi developers on L1 could unite around a standardized DEX, lending, synthetic stablecoins, etc. and make them fully consistent with L1, while unnecessary tokens that do not create any value will stimulate fragmentation, complexity and ugliness of the ecosystem.

What if something goes wrong? If it’s a locked smart contract, how can open source developers upgrade and improve the software?

Once protocols are truly fully aligned to L1, they can be written to the blockchain. While this may seem extreme, this solves some major issues and should be explored as a solution to some of DeFi’s biggest problems.

First, it allows governance and upgrades to the protocol without a governance token. Compared to ruthless and plutocratic token governance, EIP-style off-chain governance is more meritocratic, opt-in, and voluntary.

Second, it allows protocols to be resilient to code bugs in smart contracts because they gain security from client diversity. Protecting smart contracts from bugs is hard. Formal verification is a very slow and difficult process, and normal security audits are not a panacea. Hacks are devastating and remain a prominent unsolved problem in crypto, attracting negative scrutiny to our space. While this is an extreme solution, it may be time to explore the holy grail of DeFi as a solution to this ongoing scourge.

How can developers make money by developing protocols that fully comply with L1 protocols?

It’s simple: they make money by being long L1. They can receive L1 token grants from whales, who are incentivized to provide such grants to drive the value of their investment. They can also raise cash from institutional L1 whales, or these institutional whales can hire developers to develop the sacred protocol and profit by creating utility for their L1.

You are too idealistic. Developers want asymmetric benefits.

It doesn’t make sense to ask “why would I build a protocol if I can’t get rich by issuing tokens”. If I could get asymmetric benefits from visiting my grandmother, that would be great and I’d probably visit her more often, but that’s not how the world works. Just because you want protocol development to be profitable doesn’t mean it is or will ever be profitable. A few lucky protocol developers got rich by issuing tokens during past irrational bubbles, occasionally by doing dishonest things, and always by causing fragmentation and dislocation in the L1 ecosystem.

It is conceivable that governance rights over risk parameters are so valuable that the protocol’s governance token becomes very valuable for the right reasons. However, in general, most DeFi tokens are meme coins filled with incoherent response narratives.

Aside from governance rights, DeFi protocols have no scarce resources that need to be tokenized (DePIN may be an exception). This is in contrast to L1, where tokens have very direct utility and purpose. Pool L1 tokens, share love, and get rich together.

“You are describing a closed loop Ponzi scheme”

As I've described so far, yes.

But don’t forget that cryptocurrencies have been around and valuable for years even before DeFi came into being. They are convenient digital payment solutions that often have better privacy properties than centralized alternatives, are censorship-resistant, and borderless. We like them.