DerpDEX is a decentralized exchange (DEX) on zkSync, with the goal of becoming the leading decentralized exchange with centralized liquidity on L2 zkSync. The vision of DerpDEX is to create an automated market maker (AMM) with comparable performance to traditional market makers (MM). The reason for the existence of this project is that the team is a group of fintech developers, software engineers, product managers, traders, and DeFi native builders. Observing the evolution of the DeFi market, we have been able to absorb the essence of all the models so far and launch better products, better token economic models, and better execution.

The main features of DerpDEX include:

UniV3 Centralized Liquidity Market Making Algorithmic AMM on zkSync ERA

Superior decentralized exchange with Derp market making algorithm (CLMM with C parameters)

zkSync ecosystem, featuring “erc4337 account abstraction”

The latest $DERP token economics model, powered by GRAIL and xGRAIL on Camelot DEX

Initial Derp Offering (IDO) launch pad, using a spillover model

Experienced DeFi team, degen and proven #buidlers

Leading DeFi infrastructure and tools; API, trading bots, staking, farming, etc.

The team envisions DerpDEX becoming the native liquidity layer on the zkSync ERA network, enabling value creation by partnering with new and legacy protocols that need to solve cold start liquidity and initial launch bottlenecks, as well as long-term solutions to reduce the cost of incentivized liquidity.

The gap in the existing market is that one of the most important advances in decentralized finance (DeFi) is the evolution of decentralized exchanges (DEX) and automated market makers (AMMs). These decentralized protocols have transformed passive savers into liquidity providers for trading activities. However, current AMMs are still too simplistic compared to traditional market makers. The most popular form of AMM is the constant product market maker (CPMM), which derives a "fair" market price by keeping the product of the token inventory balance constant. This means that passive LPs can leave their assets in these liquidity pools and enjoy the rewards of market making activities that were previously only enjoyed by active market makers. However, this also means that traders can enjoy abundant liquidity because more capital is deployed in liquidity providing activities.

The limitation of current AMMs is that a big issue preventing AMMs from evolving towards traditional MMs is the gas bottleneck for performing complex calculations. The entire market making framework and intelligence needs to be done on-chain so that passive LPs can enjoy returns similar to traditional MMs. Another big issue is the constant fee model deployed by AMMs. AMMs are exposed to volatility risk and fees should be tied to the volatility level of the market. When markets fluctuate significantly, LPs’ profits are eroded by higher temporary losses. In volatile markets, complex LPs that dynamically balance their token inventory lose more money when doing these rebalancing. In contrast, AMMs accumulate profits in trading activity around stable prices. Constant fees fail to reflect these market dynamics. This means that LPs will be more inclined to withdraw liquidity from AMMs in volatile markets, exacerbating market movements. In stable times, traders will be reluctant to pay high fees on DEXs. This is the exact opposite of the desired dynamic! Volatility-sensitive pricing is needed to incentivize LPs to retain funds during volatile times, while traders continue to use DEXs during stable times. LPs should receive higher fees in turbulent times and lower fees in calm markets. This will lead to a fairer and more robust trading ecosystem.

Function

Function

AMM: stands for Automated Market Maker. It is a key component of most decentralized exchanges. Traditional exchanges rely on an order book model where buyers are matched with sellers who are asking the same price. AMMs use algorithms to ensure that both buyers and sellers benefit from the protocol, and liquidity providers also receive some fees. These algorithms ensure that there is always enough liquidity for the trade and that the ratio of assets in the pool is maintained.

DerpDEX adopts an AMM model based on the constant product formula. The constant product formula means that the product of the quantities of two assets (X and Y) should always be equal to a constant value (K) in the liquidity pool. This relationship allows the price of an asset to automatically adjust based on supply and demand within the pool.

X * Y = K, where X and Y are the asset values and K is a constant value that will remain constant.

If the liquidity of X increases, the value of X will decrease, while the value of Y will increase.

Likewise, if the liquidity of X decreases, the value of X will increase and the value of Y will decrease.

When a trade occurs, the constant product formula ensures that the product of the new quantities after the trade is equal to the initial constant value. This adjustment in quantity helps maintain balance in the pool and determines new price ratios between assets, ensuring that trades are executed fairly based on available reserves.

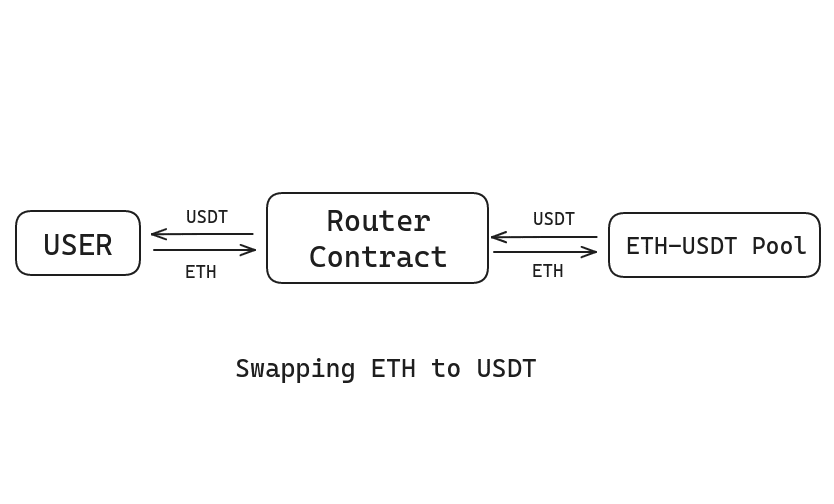

Swap: In DerpDEX, it refers to the process of exchanging one ERC20 token for another ERC20 token. Tokens are exchanged based on the current liquidity (value of the token) in a specific token pool. If the token pool exists in a decentralized exchange (DEX), tokens will be swapped directly from the token pool. Below is an example of a user exchanging ETH for USDT.

If there is no available token pool, the decentralized exchange (DEX) will automatically choose the best route to exchange the token the user wants. Below is an example of how a user can exchange their ETH for USDT if the ETH-USDT pool is not available.

If there is no available ETH-USDT pool, the DEX will try to complete the transaction through other available pools. For example, the DEX can try the following steps to help users exchange their ETH for USDT:

1. Try to convert ETH to BTC through the ETH-BTC pool.

2. Then, exchange BTC to USDT through the BTC-USDT pool.

In this example, the DEX will trade through multiple pools to achieve the user's desired ETH to USDT conversion. In this way, even if the ETH-USDT pool is unavailable, users can still trade and get the USDT they want.

There is a fee required to exchange tokens, and these fees are distributed proportionally to liquidity providers. By participating in liquidity provision, users can get incentives without locking their tokens in liquidity. Liquidity providers can remove liquidity from the pool at any time.

Liquidity: Anyone can become a liquidity provider on DerpDEX by depositing an equal value of two tokens into the liquidity pool. By doing so, they can earn a portion of the trading fees generated by the liquidity pool. Liquidity providers play a key role in maintaining the efficiency and liquidity of the platform.

DerpDEX provides a variety of features to help liquidity providers gain asset returns without taking too much risk. In addition, users can exchange tokens at low fees and reduce the volatility of funds.

Pooled liquidity allows liquidity providers to focus funds within a specific price range. This approach improves capital efficiency and reduces the need to over-allocate capital across the entire price range.

Irreversible losses occur when the value of assets in a liquidity pool deviates from their original proportions. DerpDEX uses innovative technology to minimize irreversible losses, thereby increasing returns for liquidity providers. Providing concentrated liquidity allows liquidity providers to earn the same reward by using only a portion of their assets. Therefore, if the liquidity of any token approaches 0, causing the value of other tokens to also drop to 0, the risk of losing all funds is reduced, as this will comply with the AMM formula.

Non-fungible liquidity gives liquidity providers fine-grained control over their positions. They can select specific price ranges and customize their risk exposure. Liquidity providers’ positions will be represented by non-fungible tokens (NFTs). However, shared positions can be converted to homogeneous (ERC20) through peripheral contracts or other cooperative agreements.

Fees for DerpDEX

DerpDEX charges a small fee for each trade, which is distributed proportionally to liquidity providers. This fee is usually a small fraction of the transaction value as an incentive for users to provide liquidity. By participating in liquidity provision, users can earn passive income and support the development of the ecosystem.

Token

DERP is the native token of DerpDEX.com on zkSync ERA. DERP is used as a utility to pay gas fees in the DerpDEX platform and to stake xDERP for DAO governance and enjoy additional benefits in the DERP ecosystem. xDERP is the custody token of DerpDEX. xDERP is a non-transferable custody governance token that corresponds to staked DERP. The main uses of xDERP are the ability to allocate protocol revenue, whitelisting for launchpad allocations and access to premium features on the DerpDEX platform.

Conclusion

Overall, DerpDEX is a project with potential that combines the best practices of web3, including "DeFi + memes + NFTs", to drive meme movements on the L2 zkSync network. By reviving derps as the old glory of designing to entertain global degen, they are making derps great again. By leveraging the power of L2 zkSync, DerpDEX ensures lightning-fast transaction speeds, low fees, and increased scalability, making it possible for DerpDEX to become the preferred platform for fast execution and high-performance transactions.

However, despite the attractiveness of DerpDEX's goals and vision, its success still depends on many factors. First, the success of DerpDEX will depend on whether it can attract enough users and liquidity providers. Although DerpDEX's memes-centric approach may attract a certain number of users, attracting and retaining users remains a challenge in the competitive DeFi market. Secondly, the success of DerpDEX will also depend on the stability and security of its technology. In the past, we have seen many DeFi projects fail due to technical problems or security vulnerabilities. Therefore, DerpDEX must ensure the stability and security of its platform to gain the trust of users. Finally, the success of DerpDEX will also depend on whether it can successfully launch new products and services on its platform. In the ever-changing DeFi market, projects that can innovate quickly and adapt to market changes tend to be successful.

Overall, while DerpDEX faces some challenges, its unique vision, strong technical foundation, and memes-centric approach make it a project worth watching. However, investors and users should carefully study DerpDEX and closely follow its development to make informed decisions.