Under the strict supervision of cryptocurrencies by US regulators, the crypto community may have been too FUD in the past two weeks.

The latest FUD is USDT, and the New York Attorney General recently provided Tether financial documents to CoinDesk, including customer and bank statement details. As the news spread, the USDT market price decoupled slightly from the US dollar.

Is USDT decoupled again?

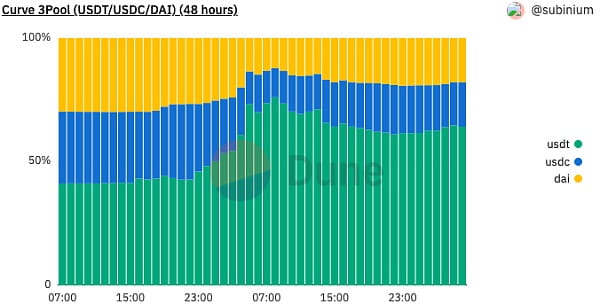

On June 15, Curve 3pool data showed that the proportion of stablecoins in the 3pool pool was unbalanced. The proportion of USDT soared to 76% at 08:00 on June 15, and USDT decoupled slightly to 0.997. In addition to Curve 3pool, a similar situation has also occurred in the Uniswap v3 USDC/USDT liquidity pool.

Curve 3pool is a liquidity pool composed of three stable coins: DAI, USDC and UDST. Ideally, all three stablecoins would account for 33.3%. When a certain stablecoin accounts for more than 33.3%, it means that investors are using this stablecoin to swap the other two stablecoins.

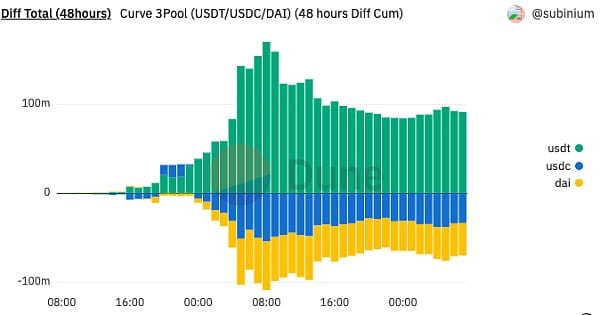

In the USDT case on June 15, investors were selling USDT in exchange for USDC or DAI. The inflow and outflow of USDT in Curve 3pool also illustrates this. Within 24 hours, Curve 3pool had an inflow of approximately US$200 million in USDT.

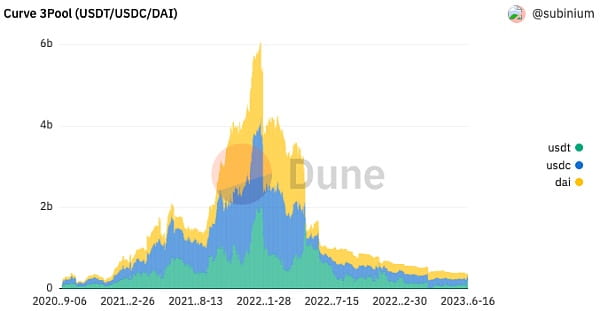

The reason why the crypto community is concerned about the deviation of stablecoins in Curve 3pool may be because Curve 3pool is the largest stablecoin fund pool, with a total locked-up value of US$410 million, and the price it reflects is of indicator significance in DeFi.

But on the other hand, the price decoupling of USDT in Curve 3pool may not be as important as imagined. There are three reasons: 1. Although the total lock-up value of Curve 3pool is US$410 million, compared with the peak of US$6 billion, the decline has exceeded 93%. 2. Compared with the total issuance of USDT of USD 86 billion, the sales volume of USD 200 million may not be enough to affect the overall market price of USDT. 3. As long as Tether maintains 1:1 redemption of USD and USDT is "decoupled" from Curve 3pool, there will naturally be market arbitrageurs to balance its price.

What exactly are people talking about when they say USDT is decoupled?

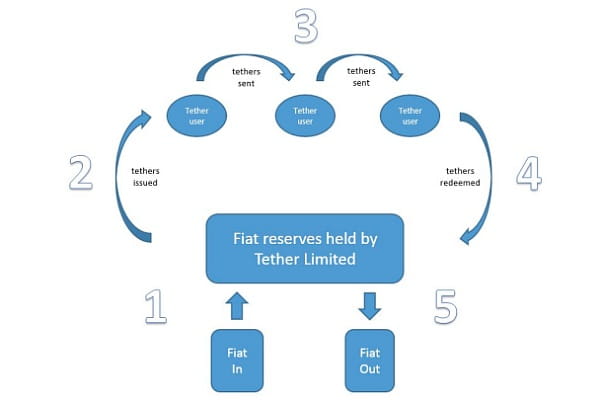

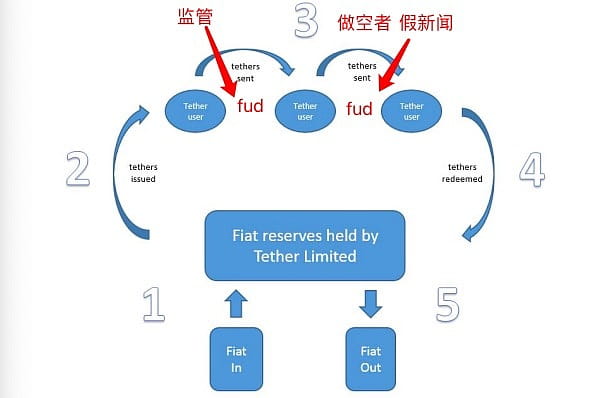

According to the Tether white paper, the operating mechanism of USDT is very brief. Tether will mint 1 USDT when it receives 1 US dollar of fiat currency from the customer. Tether will return 1 US dollar worth of fiat currency to the customer upon receiving the customer's redemption request for 1 USDT.

Tether said that its stablecoin USDT is supported by the U.S. dollar at a ratio of 1:1. It means that at the two key nodes of minting USDT and redeeming the U.S. dollar, Tether guarantees 1:1 minting and redemption. Tether does not guarantee that USDT will always be equal to 1 US dollar during the circulation process.

Therefore, USDT has two prices, the market price and the minting/redemption price. Tether has never guaranteed that the market price of USDT is pegged to 1 US dollar. It only guarantees that USDT will be minted or redeemed for US dollars at a 1:1 ratio, plus a 0.1% deposit/withdrawal fee (two-way charges).

In other words, the USDT market price has nothing to do with Tether. Tether or its related stakeholders even hope that the market price of USDT is lower than 1 US dollar, so that they can recycle USDT at a low price. Of course, for the sake of long-term interests and stable operations, Tether may not do this.

Because Tether's business is really a very good business. Tether takes the U.S. dollar fiat currency deposited by users and invests these dollars in almost risk-free, highly liquid income products such as U.S. Treasury bonds, overnight repurchases, regular repurchases, money market funds, etc. Tether's reserve is completely a " "The chicken that lays the golden eggs" is the real "earning money".

This is also true. According to the latest data from Tether, the issuer of USDT, Tether’s profit reached US$1.48 billion in the first quarter of 2023 alone, and its excess reserves reached US$2.44 billion.

In the market, various factors such as short sellers, fake news or regulation will cause market FUD, which will trigger investors to sell USDT, causing the USDT market price to diverge from 1 US dollar.

But as long as Tether fulfills its promise of minting USDT and redeeming USD at its two entrances and exits on a 1:1 basis, it can be said that USDT will always remain pegged to the U.S. dollar at a 1:1 ratio. Needless to say about minting, if you send reserves to Tether, he will definitely be willing to accept it and give you 1:1 USDT.

Can Tether guarantee USDT 1:1 redemption?

According to Tether’s reserve certificate report for the first quarter of 2023, if Tether’s report is credible, Tether’s direct holdings of government bonds exceed US$53 billion, accounting for more than 64% of total reserves. These Treasuries, along with other reserves in the cash and cash equivalents category (such as overnight repos, term repos, money market funds, cash and bank deposits), account for nearly 85% of Tether’s total reserves. These high-quality, liquid assets Collateral provided to Tether for quick sale to process redemptions.

After the USDC reserve was implicated in the bankruptcy of Silicon Valley Bank, Tether reduced its holdings in cash and bank deposits by 90%, which currently totals $480 million.

The remaining 5% is some high-risk precious metals, Bitcoin, other investments, corporate bonds and mortgages. What if something goes wrong with this $818 million? Tether said it has $2.44 billion in excess reserves.

Going a step further, Tether has already made sufficient preparations in terms of service. Tether has reserved the right to "physical return" in the USDT stablecoin terms of service. When liquidity is insufficient, Tether can return bonds, stocks or "reserves" to users. other assets held” without having to return the dollars. “If any reserves held by Tether to support Tether Tokens experience insufficient liquidity, unavailability or loss, it will cause a delay in the redemption or withdrawal of Tether Tokens, and Tether reserves the right to delay the redemption or withdrawal of Tether Tokens, And Tether also reserves the right to redeem Tether Tokens through physical objects, including securities and other assets held in reserves. As for whether Tether Tokens previously traded through the website can be traded at any time in the future (if any), Tether makes no representations or warranties."

So, can Tether reserve certificates be faked? First, countless regulatory agencies are staring at Tether, and the cost of fraud is too high; 2. As mentioned in the previous section, Tether reserves are a "chicken that lays golden eggs" and a real "profit-making" product. The benefit/risk ratio is too small.

Unless U.S. Treasury bonds, overnight repurchases, term repurchases, money market funds, cash and bank deposits all collapse, then such large-scale problems are simply beyond Tether's control.

Perhaps because of this, Tether CTO Paolo Ardoino directly stated on Twitter: "Tether is as ready as ever and we are ready to redeem any amount of funds."