Institution: Mint Ventures

Author: Colin Li

1. Research highlights

1.1 Core investment logic

In addition to ETH liquidity staking, the BNB and ATOM staking markets have begun to attract investors' attention. Among these projects, the development of pSTAKE Finance after embracing BNBchain deserves attention. If pSTAKE Finance's other public chain strategies, such as ATOM's liquidity staking service, can also achieve dual-line expansion of business and ecological expansion like its BNB liquidity staking service, then pSTAKE Finance deserves to be included in the scope of investors' prudent investigation.

1.2 Valuation

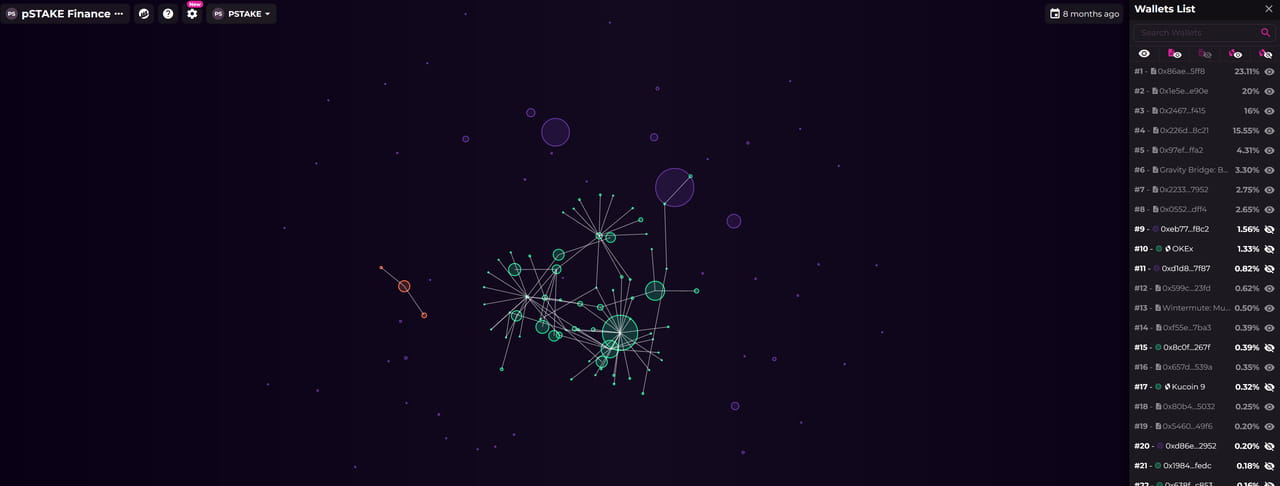

From the perspective of static valuation, pSTAKE Finance is relatively expensive, which may be related to the overly concentrated distribution of PSTAKE chips: currently more than 75% of PSTAKE chips are concentrated in a few addresses, and the circulating market value is relatively small.

1.3. Main risks

Risks of public chain development: pSTAKE Finance is now betting on the liquidity staking business of ATOM and BNB. The biggest beta in the future will come from the development of public chains. Currently, the staking ratios of BNBchain and COSMOS are relatively high, and the growth space from the improvement of staking ratios in the future is limited. In the future, it is necessary to expand other potential public chains with low staking ratios, which will test the strategic judgment of the founding team.

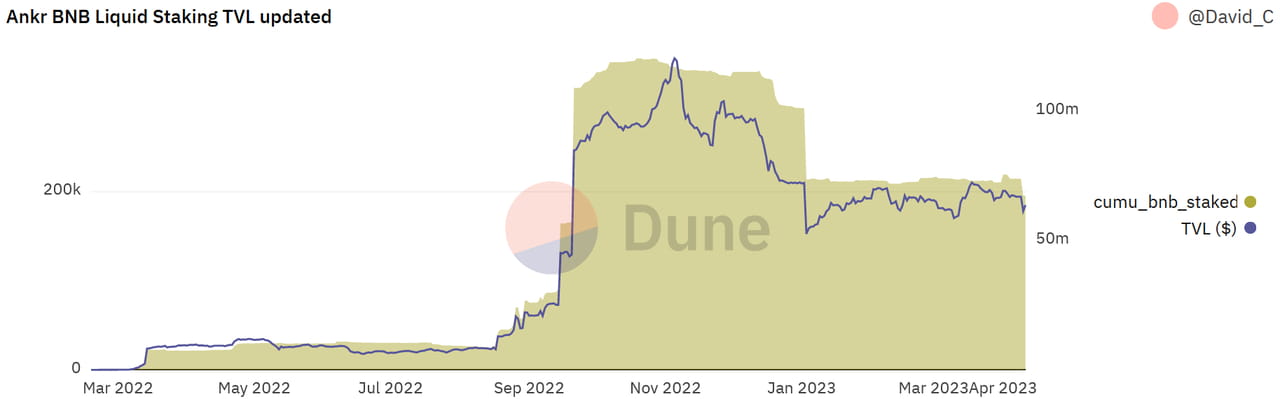

Contract risk: On December 2, 2022, Ankr had a contract risk issue that affected the BNB staking track, and it has not yet fully recovered to the level before the incident. If a similar incident happens again, and pSTAKE Finance provides liquidity staking services on such a public chain, then pSTAKE Finance is likely to be impacted.

Price war within the industry: As the staking rate of the PoS public chain continues to increase in the future, a price war may break out within the industry to compete for the limited market space: reducing staking and unstaking fees will undoubtedly reduce the value of the entire liquidity staking track.

2. Basic information of the project

2.1 Project Business Scope

pSTAKE Finance is a liquidity pledge protocol, currently focusing on liquidity pledge services for Ethereum, BNBchain, and Cosmos ecosystems. In the future, it is expected to expand liquidity pledge services for more public chains and expand the application scenarios of its own LSD in other DeFi.

2.2 Past Development and Roadmap

pSTAKE Finance was developed by the Persistence team. Since the project was launched in 2020, it has gone through the following two stages:

The first stage:

Fourth quarter of 2020: The project concept was finalized and the MVP was designed;

Q1 2021: pSTAKE Finance project was officially established, with the main business line being to provide staking services for Cosmos;

Q2 2021: Start airdrops and bug bounties, and conduct contract audits;

Q3 2021: pBridge (a cross-chain bridge developed by pSTAKE Finance) validators and pSTAKE validators go online;

Q4 2021: pSTAKE Finance mainnet will be launched and public offering will be carried out;

Q1 2022: Expansion to other COSMOS chains (Terra);

Q2 2022: Launch ETH staking service;

second stage:

Q3 2022: Launch V2 to promote the use of stkToken, reach a strategic partnership with Binance, provide liquidity staking services for BNB, and officially launch in August 2022;

Q4 2022: Promote PoS asset management, and plan to provide ATOM staking services in Persistence Core-1 Chain (a public chain based on COSMOS developed by the Persistence team), and provide stkATOM with more DeFi services.

2.3 Business Situation

2.3.1 Service Target

The main service objects of pSTAKE Finance are users who hold POS public chain tokens. In order to provide complete staking services and achieve the security of the verification process, pSTAKE Finance uses a validator scoring system to find validators who meet the requirements and hand over the user's public chain tokens to the validators for staking.

User side: Since the launch of pSTAKE Finance, it has provided staking services for four public chain tokens: ATOM, XPRT, ETH, and BNB. In the early plan, staking services for SOL, AVAX, and other Cosmos Layer 1 public chain tokens were also included in the future. With the advancement of the business, especially after reaching a strategic cooperation with Binance in 2022, the business focus of pSTAKE Finance has been concentrated on the staking services of the two tokens ATOM and BNB.

Validator side: pSTAKE Finance chooses to cooperate with some good validators to provide verification services for pBridge and liquidity staking business. At present, pSTAKE Finance's validator partners include Figment, Chorus One, CertiK, etc.

2.3.2 Business Classification

Currently, pSTAKE Finance supports staking services for three assets: ATOM, BNB, and ETH. Among them, stkATOM and stkXPRT are undergoing migration. In the future, the liquidity staking services of ATOM and XPRT will be carried out on the Persistence Core-1 Chain public chain developed by pSTAKE Finance.

2.3.3 Business details and multi-chain deployment

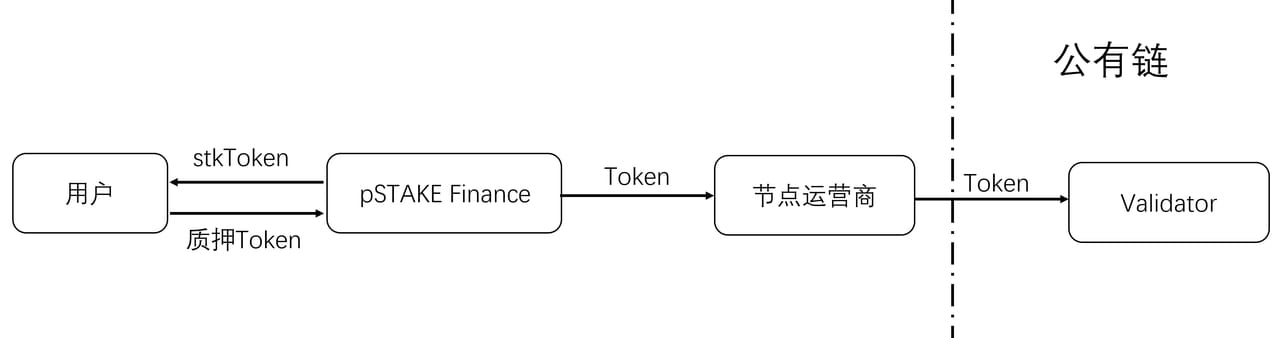

The liquidity pledge business model can be simplified as follows:

The mechanisms between POS chains are different, but the general business logic is as above. Among the staking of ATOM, ETH and BNB, BNB is more special. There are two chains related to BNB: BNB Beacon Chain, which is responsible for the governance and staking of BNB; BNB Smart Chain, which is EVM-compatible and supports the operation of various types of Dapps. In addition, 42 validators of BNB are designated.

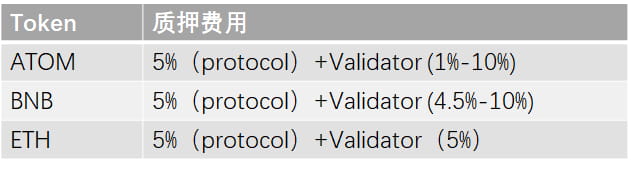

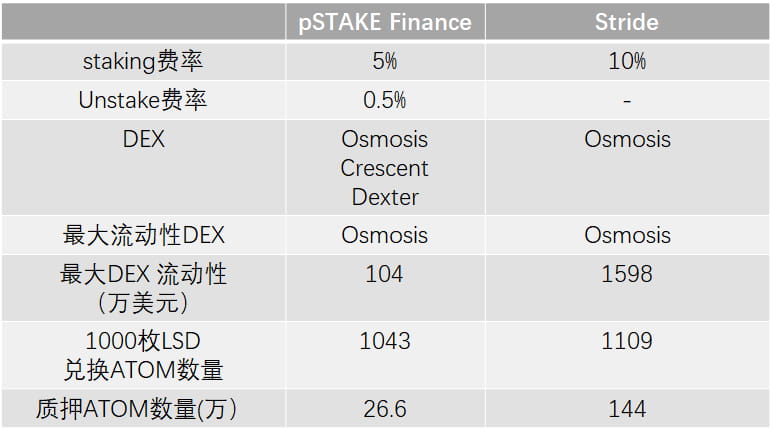

Like other LSD projects, pSTAKE Finance will charge certain fees when providing services: taking ATOM as an example, 5% of the staking rewards obtained by users during the staking period will be paid to pSTAKE Finance as fees; when users unstake, if they want to quickly obtain their staked tokens, there will also be a "Redeem Instantly" fee of 0.5% of the total amount.

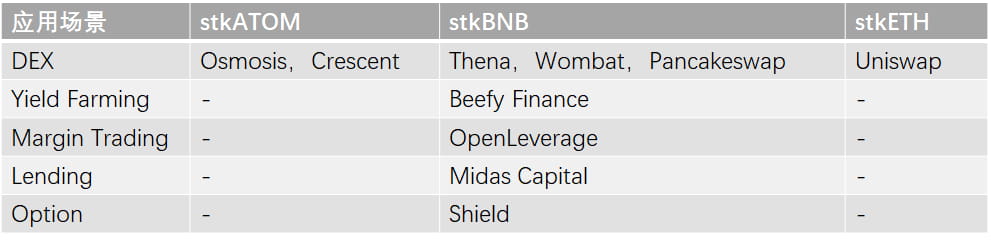

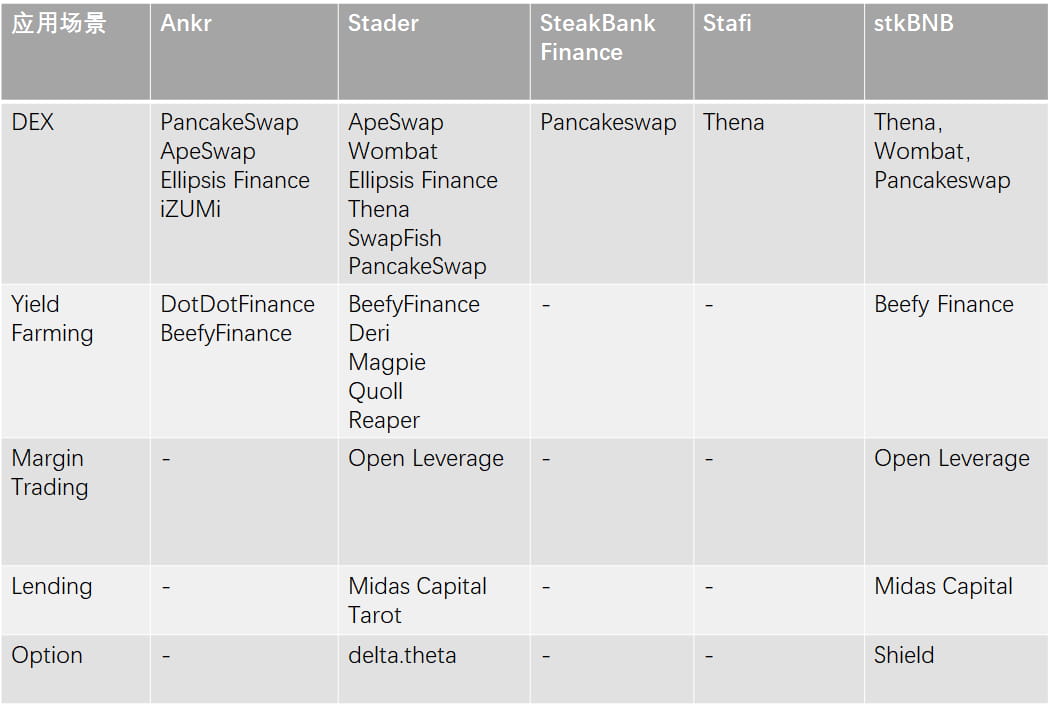

In addition to providing staking services, pSTAKE Finance also provides users with application scenarios for their own staking certificates: Taking pSTAKE Finance's BNB staking certificate stkBNB as an example, although the BNB staking business was launched later, due to the investment from Binance in the second half of 2022, the speed of access by ecological partners is very fast. Users' stkBNB can be applied to many mainstream DeFi in the BNBchain ecosystem. For example, stkBNB can be deposited in Beefy Finance to earn additional income, used as margin for trading in OpenLeverage, and deposited in Midas Captal to earn lending income, etc.

In contrast, the application scenario cooperation of stkATOM and stkETH has progressed relatively slowly.

2.4 Business Data

Overall TVL

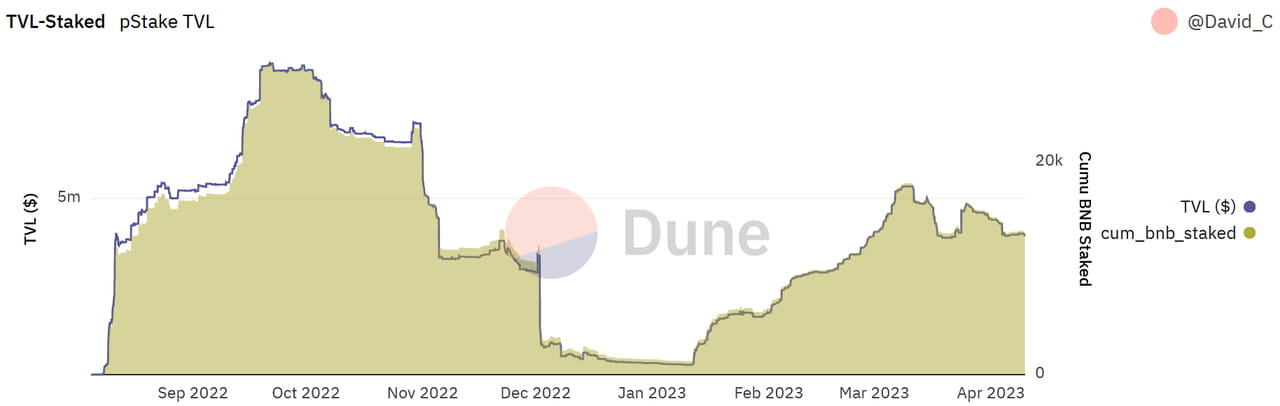

The current TVL of pSTAKE Finance totals approximately US$7.41 million, of which approximately 60% is BNB, 40% is ATOM, and ETH staking is almost negligible.

Price Anchoring and Liquidity

The following two pictures show the situation of stkATOM. Although the overall liquidity of the cooperating DEX is poor and the cooperation time is relatively short, stkATOM has not experienced a large deviation overall, and the ratio of stkATOM and ATOM in the trading pair is balanced.

In general, the liquidity of the two pools can basically meet users' needs for small-scale, slippage-free exchanges.

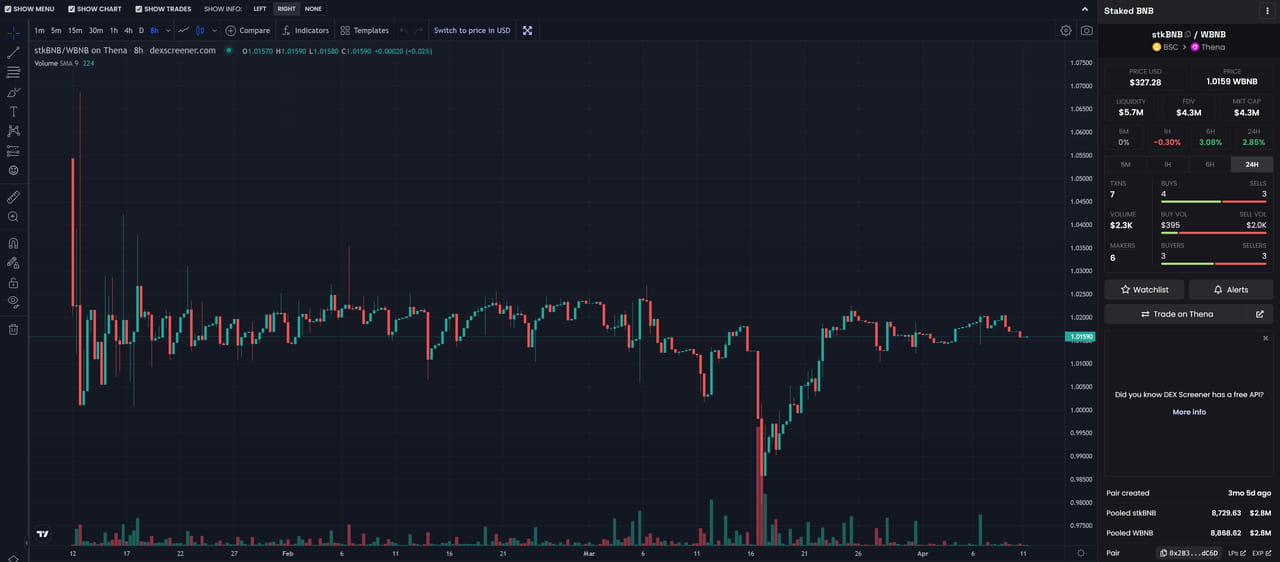

After the stkBNB-BNB trading pair was launched, the main unpegging time occurred on December 2, 2022, but this was not due to major problems with pSTAKE Finance itself, but was affected by the Ankr attack: on that day, Ankr was attacked, resulting in over-minting of aBNBc, which triggered market concerns about BNB LSD assets. However, stkBNB returned to the anchor one hour after the unpegging and was not affected lastingly.

The scale of the stkBNB-BNB pool in Thena and Wombat can also meet users' small-scale, slippage-free exchange needs.

As the ETH staking business has shrunk significantly, the TVL of the stkETH-ETH trading pair in the current Uniswap V3 project is only slightly over $50,000, and the price loss caused by trading one stkETH has reached 7.25%.

2.4 Team situation

2.4.1 Overall situation

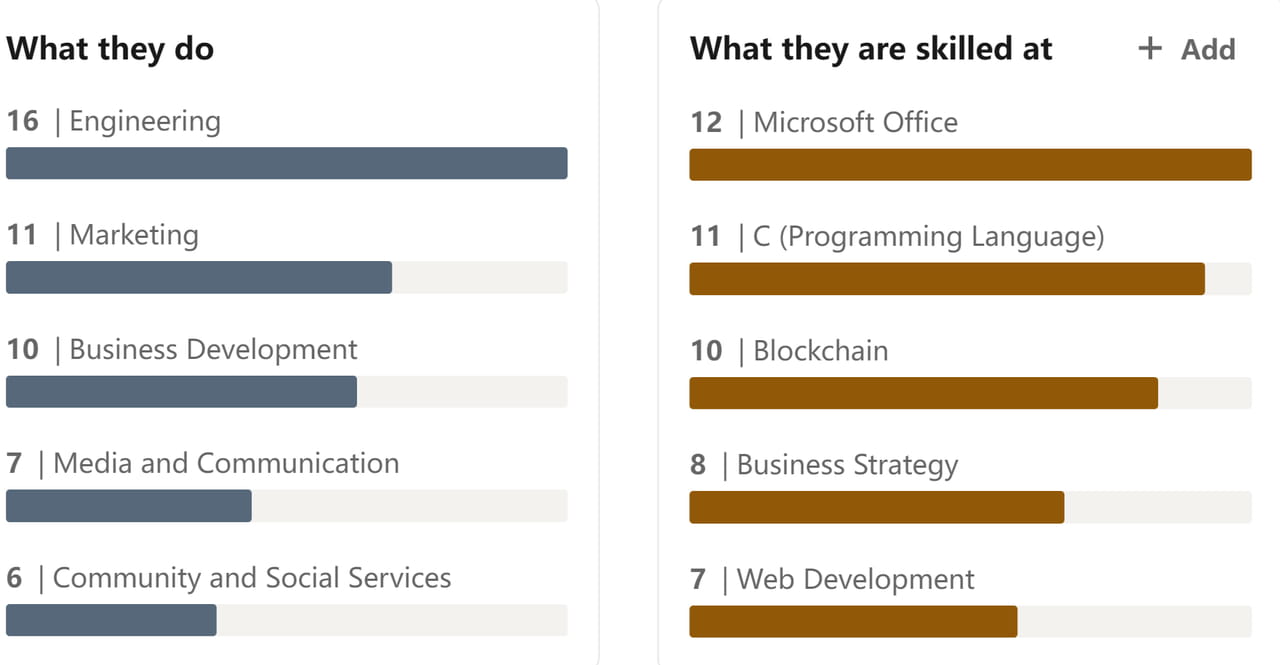

According to LinkedIn data, Persistence, the development and operation team behind pSTAKE Finance, has a total of 45 employees, mainly composed of engineers, marketing, BD, media and community operations personnel.

2.4.2 Founder

Tushar Aggarwal is the co-founder and CEO of Persistence and graduated from Nanyang Technological University, Singapore. Before founding Persistence, he worked in several crypto funds such as Decrypt Asia, Antler, and LuneX Ventures, and also served as a partner at Outlier Ventures. In 2019, Tushar founded Persistence, hoping to promote the development of the Cosmos ecosystem liquidity staking business. Subsequently, in 2020, he led the Persistence team to develop the pSTAKE Finance project.

Deepanshu Tripathi is the co-founder and CTO of Persistence and graduated from Vellore Institute of Technology. Before founding Persistence, he worked as an engineer at Mahindra Comviva and later became the chief software architect at Comdex. In 2019, Tushar founded Persistence and served as CTO. In 2022, he founded AssetMantle, a one-stop NFT service platform.

2.4.3 Core members

Members of the major business lines have rich and deep backgrounds in relevant fields.

Head of Ecosystem and Marketing: Abhitej Singh, who previously worked as the Head of Marketing and Media at BLOCK42.network and became the co-founder of Cosmos India in 2019.

Project leader: Mikhil Pandey, who has been working at Persistence as a market research assistant, strategy and business development lead, etc.

2.5 Financing

pSTAKE Finance has gone through two rounds of independent financing.

In November 2021, pSTAKE Finance completed a $10 million financing with a valuation of $50 million. The platform token PSTAKE was sold at a price of $0.1 per coin. Investors include Three Arrow Capital, Sequoia India, Galaxy Digital, Defiance Capital, Coinbase Ventures, Tendermint Ventures, Kraken Ventures, Alameda Research, Sino Global Capital and Spartan Group. Aave Institutional Business Development Head Ajit Tripathi, Terra Founder Do Kwon and Alpha Finance Co-founder Tascha Punyaneramitdee also participated in this round of financing.

In December 2021, pSTAKE Finance completed a $10 million financing on CoinList and sold 5% of its tokens. The platform token PSTAKE was sold at a price of $0.4 per coin, with a valuation of $200 million.

In May 2022, pSTAKE Finance received a strategic investment from Binance Labs, the amount of which is unknown.

3. Business Analysis

3.1 Industry space and potential

3.1.1 Classification and market size

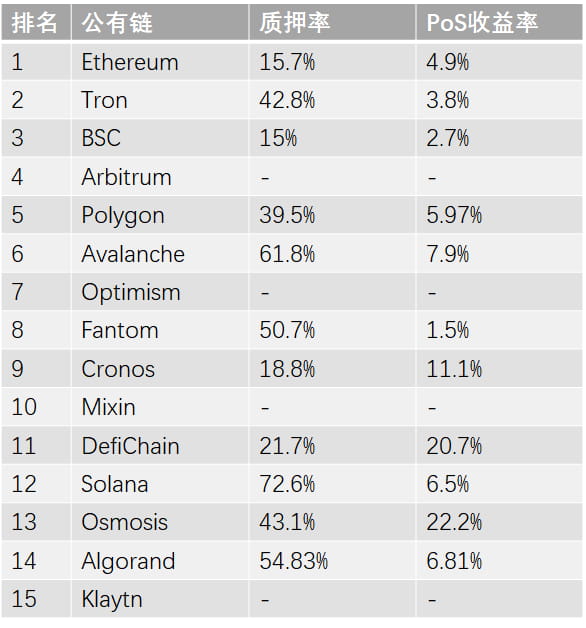

Among the public chains with TVL above 200 million USD, except for some public chains that have not launched staking services, the average staking rate is 46.9%. Among them, the staking rates of Ethereum, Tron, Polygon and other public chains are lower than this level. As Ethereum's Layer 2 network is gradually launched, more chains will provide their token staking services in the future. Some investors in the market are more optimistic about the staking ratio of public chains, and the staking rate of Layer 2 will also reach a corresponding proportion.

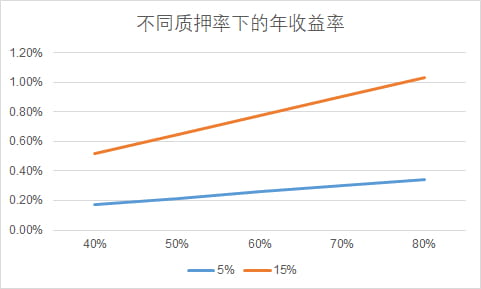

For the liquidity staking track, assuming that the market value remains unchanged, the staking scale of a single public chain is only related to the staking ratio, and the overall revenue scale of the track is also related to the PoS yield and the service fee ratio. The average staking yield of the public chain in the figure below is about 8.6%.

In the current market, liquidity staking projects generally extract 5%-15% of the income as service fees. According to the 8.6% PoS yield, the total yield of liquidity staking projects is between 0.43%-1.29%. From this, we can roughly estimate the rough relationship between liquidity staking profits and the market value of the public chain. Of course, we can also adjust the PoS yield for estimation.

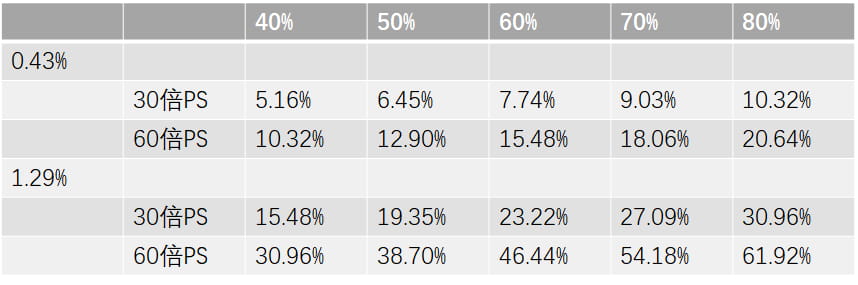

By assuming different valuation parameters - the price-to-sales ratio (PS ratio), we can also obtain the data shown in the following figure.

Therefore, if we only start from the basic dimension of liquidity pledge base, if we want to improve the overall valuation of the liquidity pledge track, we need to find a public chain whose pledge rate, PoS yield, and market value will increase significantly in the future.

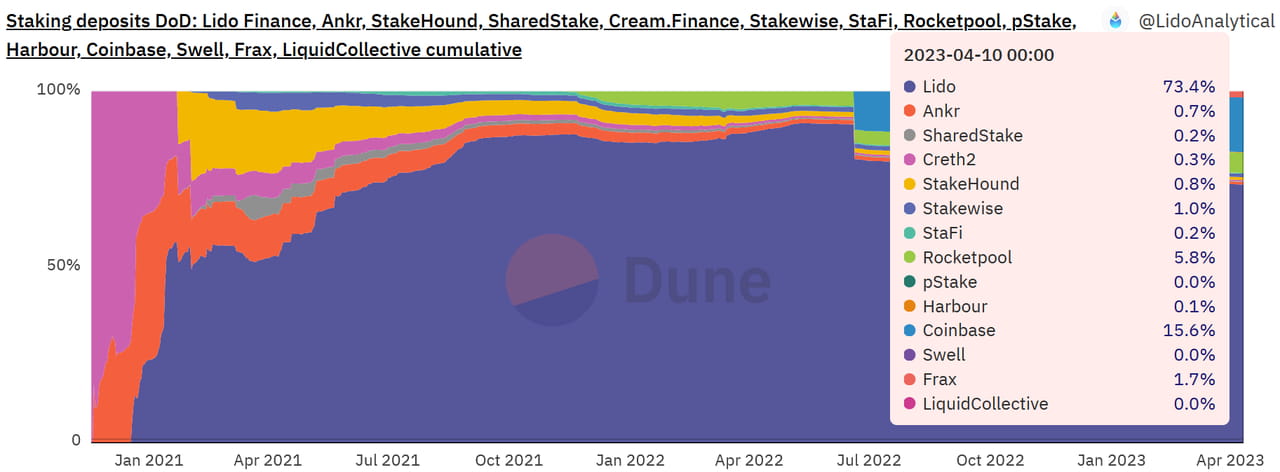

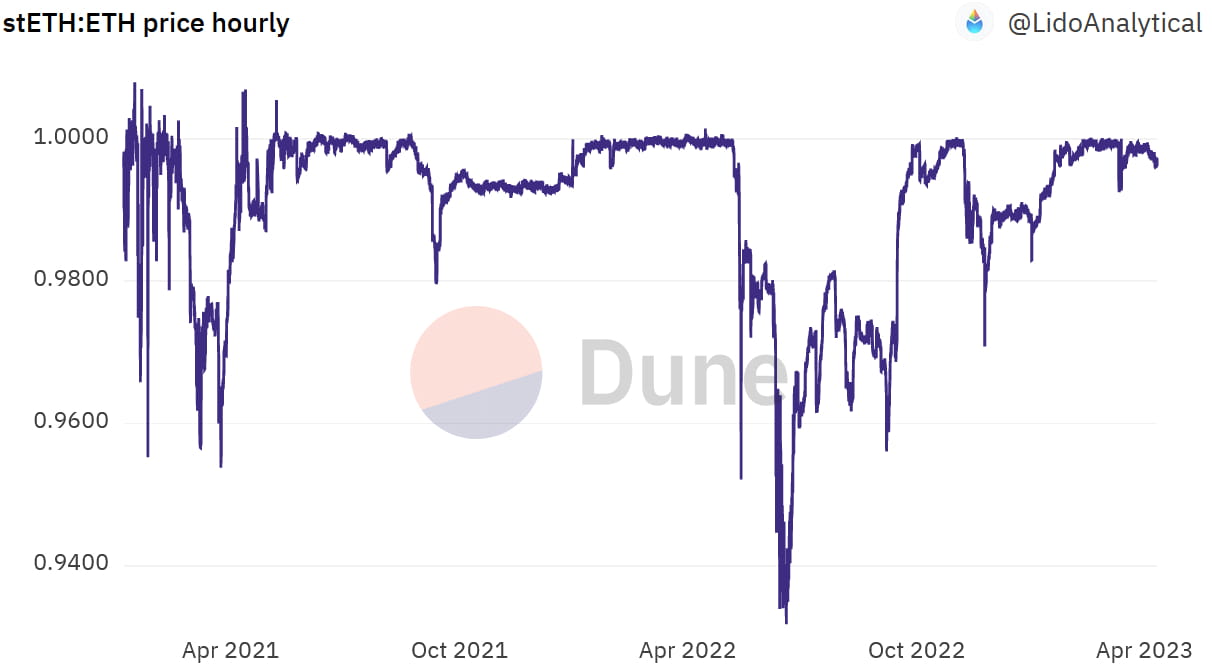

Since the liquidity pledge projects provide users with very similar services, under the condition that there is no obvious difference in the fee rate, users are more inclined to prioritize the market, have a long-term safe operation record, good LSD liquidity and no obvious discount projects. Taking the Ethereum liquidity pledge track as an example, the current market TOP 3 market share has reached 94.8%, of which Lido's market share has reached 73.4%. The Lido project was established earlier than some other liquidity pledge projects.

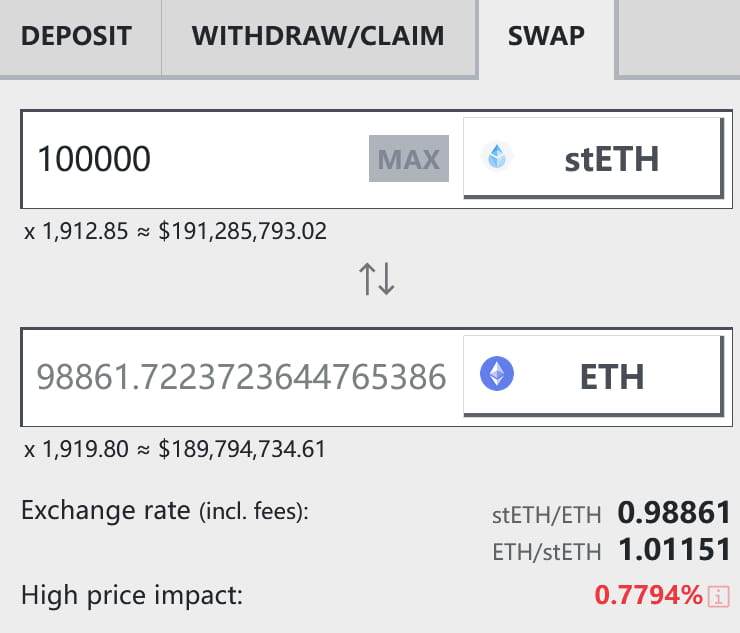

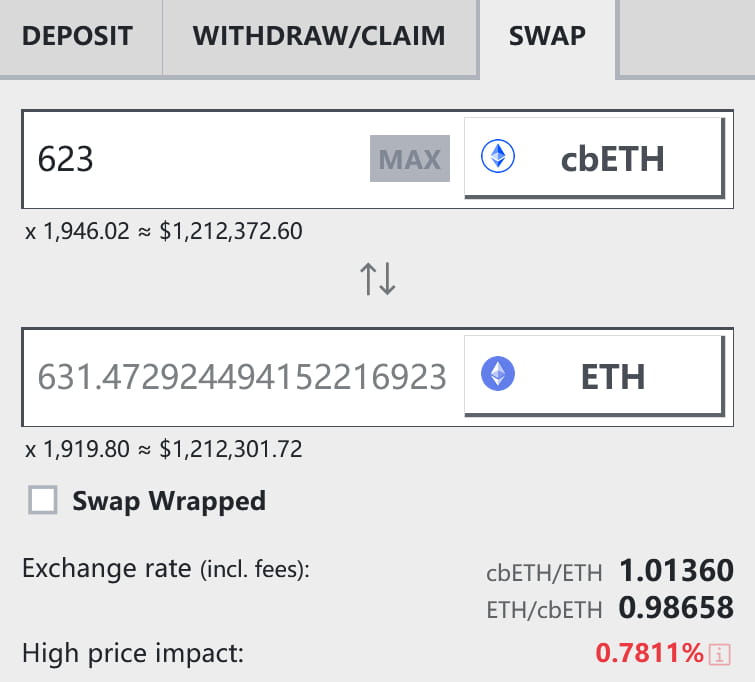

The ultra-high market share is also related to the performance of stETH. Except for the sharp market decline in the past two years, stETH has almost never experienced a significant de-anchoring. And its trading liquidity is also excellent. In the stETH-ETH pool on Curve, a single transaction of 100,000 stETH has an impact on the price of only 0.78%. However, for the second-ranked cbETH, a single transaction only requires a transaction volume of about 623 pieces to achieve a similar value loss. . It can be seen that for large investors who hold more ETH, choosing Lido is a better choice. Of course, the subsidy incentives provided by Lido are also one of the important factors leading to its ultra-high market share.

3.2 Token Model Analysis

3.2.1 Total Token Supply and Distribution

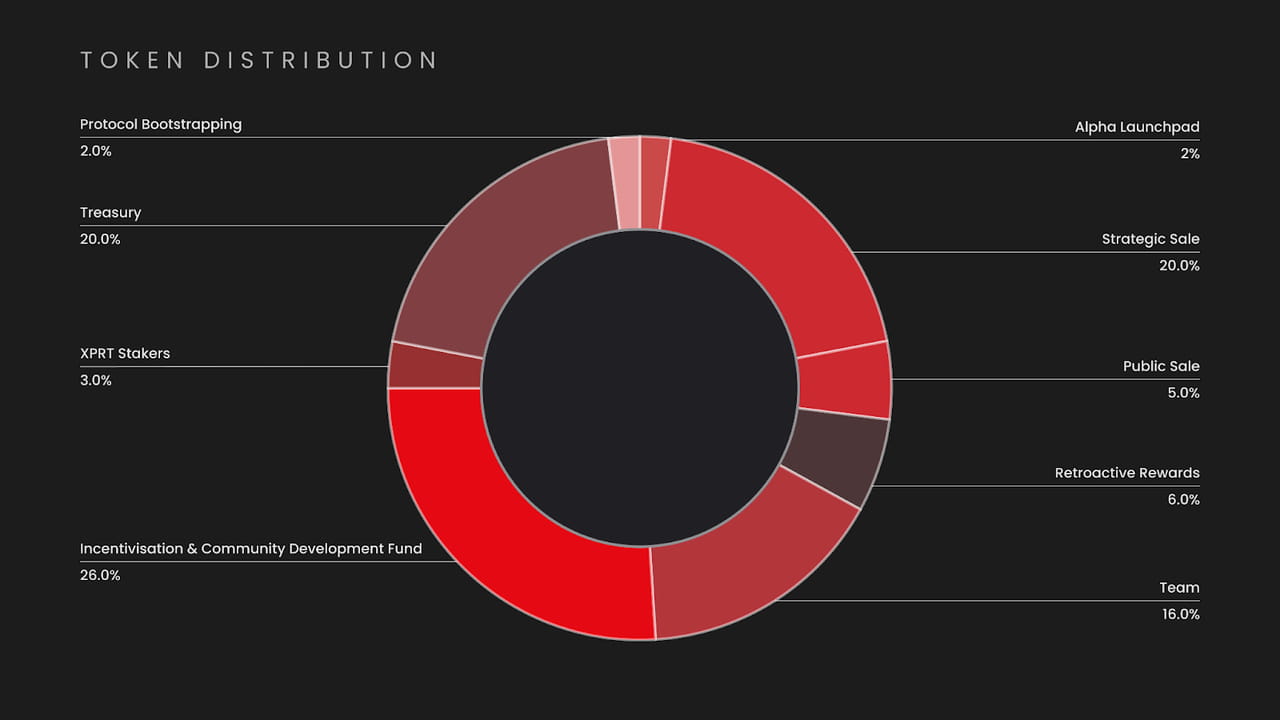

The total number of PSTAKE tokens is 500 million, which will be put into circulation in February 2022. Among them:

2% belongs to Alpha Launchpad, which is allocated to the pledge users of Alpha Finance and the Alpha Finance team (Note: it was a lending project at the beginning of its launch, and now it has become an Alpha Finance DAO, providing comprehensive services including project incubation and VC);

20% is a strategic sale, which will be unlocked starting 6 months after investment and will be unlocked linearly over the next 12 months;

5% is a public sale on CoinList, 25% of which is unlocked on the day of sale, and the rest is unlocked linearly over 6 months;

6% is a retroactive reward, which is provided to the liquidity providers of stkATOM-ETH and stkXPRT-ETH pools. It will be unlocked linearly within 6 months;

16% belongs to the team, which will be unlocked 18 months after the tokens are put into circulation in the secondary market, and will be unlocked linearly within the next 18 months;

26% belongs to the incentive and community development fund: unlocked linearly every quarter and fully unlocked within 2 years;

3% belongs to XPRT stakers, which will be unlocked linearly quarterly within 1 year;

20% belongs to the national treasury, and will be unlocked linearly within 24 months after the tokens are put into circulation in the secondary market;

2% belongs to the bootstrapping of the project and can be circulated after the token is launched.

According to the above token release rules, about 55.2% of the token PSTAKE is already available for circulation, and all will be released by 2025. The average annual inflation rate in the next two years is about 35%, which is a relatively high inflation rate.

3.2.2 Token Value Capture

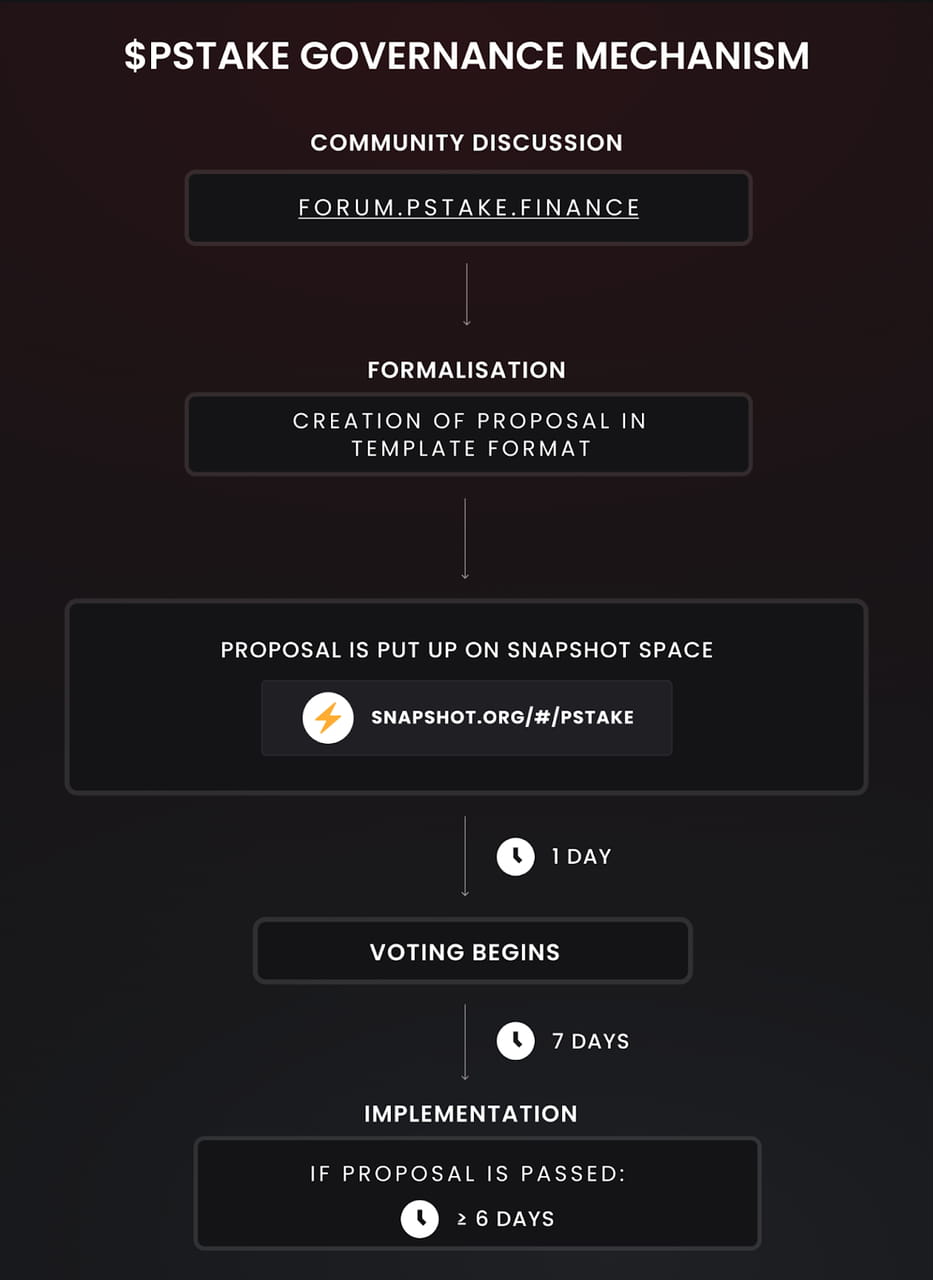

At this stage, PSTAKE tokens only have governance functions and cannot share the project's revenue. PSTAKE holders can participate in community governance voting, or pledge PSTAKE to maintain the security of the project.

3.2.3 Core Token Demanders

At this stage, the tokens with staking governance functions are recognized by investors due to two factors:

Directly participate in governance and influence the future development direction of the project. pSTAKE Finance stipulates that only investors/institutions holding at least 250,000 PSTAKE tokens can initiate proposals within the community. This may be more attractive to investors with large funds and the ability to bring ecological support and business resources to the project. By initiating proposals and voting, large investors can influence pSTAKE Finance fees, public chain deployment strategies, ecological incentive mechanisms, and other aspects. These strategies may increase the medium- and long-term value of PSTAKE.

Similar to UNI, the value capture function of the token may be achieved through subsequent proposals. However, UNI does not necessarily have to obtain the attributes of value capture or profit sharing in the near future. In the stock market, stocks issued by high-growth companies do not necessarily have to pay dividends within a certain period of time. For example, Amazon’s stock has not paid dividends for a long time, but it does not affect the long-term rise in Amazon’s stock price, because the company is still in a stage of long-term rapid growth and requires a lot of investment. Therefore, PSTAKE may not have the cash flow dividend attribute in the short term, but it needs to further expand its business, whether it is a multi-chain deployment strategy similar to Uniswap, or a multi-business line collaborative development model similar to Frax Finance. As long as the pSTAKE Finance project can achieve growth through expansion, the lack of value capture capabilities at this stage may not be the core concern of potential investors.

3.2.4 Summary of Token Model

From the perspective of the token economic model, PSTAKE has room for improvement. For example, in order to address the problem of excessive inflation in the short and medium term, the Ve model can be used to reduce inflationary pressure in the short and medium term, and it can also improve the efficiency of governance and retain long-term investors. It should be noted that the Ve model is a possible solution, and the final appeal of the token still depends on the quality of the project itself. If there is no obvious benefit of participating in governance, the Ve model cannot save the currency price.

Regarding the issue of value capture, in the middle and late stages of the project's rapid growth, pSTAKE Finance can use part of the fees for repurchases, etc. The income earned at this stage does not necessarily have to be kept in the treasury. Part of the money can be used for ecological promotion, or even to purchase tokens of other projects that can have synergistic effects.

3.3 Project Competition Landscape

3.3.1 Basic Market Structure & Competitors

From the perspective of pSTAKE Finance's business layout and external cooperation, the important direction that determines its future development is BNB and ATOM liquidity staking services. Regarding the liquidity staking of these two tokens, especially the competitive landscape of BNB liquidity staking, it is very critical. The dimensions of token liquidity and ecological cooperation are our focus.

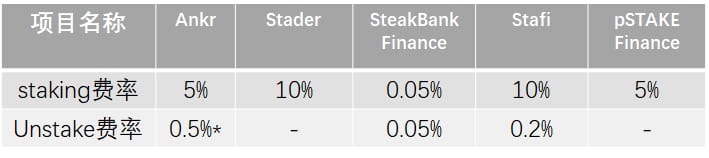

In the BNBchain ecosystem, there are currently five companies providing liquidity staking services, including Ankr, Stader, SteakBank Finance, Stafi, and pSTAKE Finance. From the perspective of fees, pSTAKE Finance charges in the middle.

In terms of ecological cooperation, pSTAKE Finance currently has the most diverse application scenarios and can basically meet most of the financial needs of PSTAKE holders on the BNBchain.

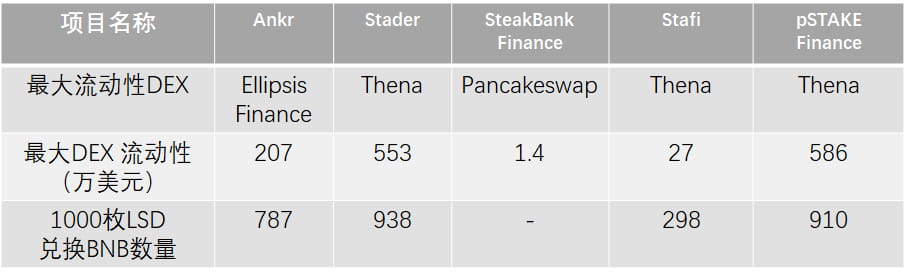

In terms of liquidity, pSTAKE Finance can meet the trading needs of large investors with smaller slippage.

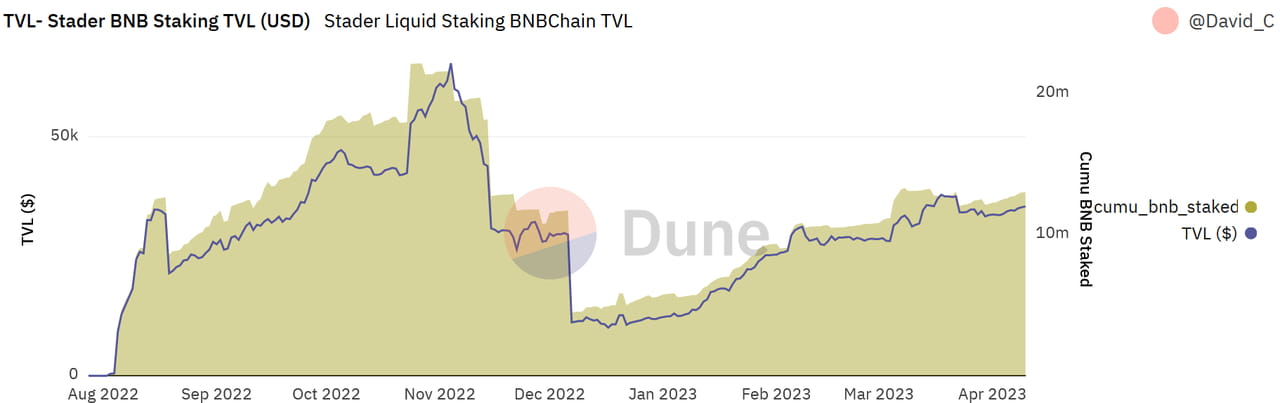

Currently, the amount of BNB pledged by pSTAKE Finance lags behind Ankr and Stader (ranked third in the liquidity staking track on BNB Chain).

The current liquidity pledge market of Cosmos mainly includes Stride and pSTAKE Finance. We still observe from the above dimensions. In comparison, the fee rate of pSTAKE Finance is relatively low, and the depth of its depositary receipts can currently meet the in and out needs of small and medium-sized liquidity. In the future, as the demand for ATOM liquidity pledge increases, at least in the competition with Stride, pSTAKE Finance has the opportunity to gradually increase its market share.

3.3.2 Project Competitive Advantages

From the above comparison, we can find that the core competitiveness of pSTAKE Finance is highlighted after Binance investment:

stkBNB has a wide range of application scenarios: After obtaining investment from Binance, pSTAKE Finance has the full support of the current BNBchain ecosystem. stkBNB can almost meet most of the users' on-chain financial scenario needs.

stkBNB has good liquidity, and the entry and exit channels are smooth for traders: the amount of BNB pledged on pSTAKE Finance has reached the third level in the current market, and the liquidity can also meet the entry and exit of ordinary investors.

These two key points are also the development direction of other liquidity staking businesses such as ATOM.

3.4 Project Risks

Combined with the problems of the liquidity pledge track itself, the pSTAKE Finance project mainly faces the following three types of risks:

Risks of public chain development: Because pSTAKE Finance is now betting on the liquidity staking business of ATOM and BNB, the biggest development beta in the future comes from the development of public chains. If COSMOS and BNBchain cannot achieve significant growth, the driving force from the public chain level will be reduced. Moreover, the staking rates of BSC and COSMOS are relatively high, and the growth space from the increase in staking rates in the future is limited. If pSTAKE Finance wants to further grow its business, in addition to stabilizing BNB staking and ATOM staking, it also needs to expand other potential public chains with low staking rates. Betting on public chains is undoubtedly the focus of many entrepreneurs and investors, but from the perspective of the development history of public chains, there are only a few people who can really grasp promising public chains, which undoubtedly tests the strategic vision of the founding team.

Contract risk: Contract attacks will cause a large number of bad debts in the agreement, and it should be noted that the risk of contract attacks is not limited to the project itself. If a project on the same track is attacked, it may also affect other projects on the same track. On December 2, 2022, Ankr encountered a contract risk problem, resulting in a huge increase in its liquidity staking certificate (LSD)-aBNBc. Subsequently, Ankr temporarily suspended the BNB staking business for processing, but the panic had a greater impact on other BNB staking projects: the business scale of pSTAKE Finance and Stader in the same period shrank by more than 70%, and it has only now basically recovered to the level before the incident.

Price war within the industry: With the growth of the PoS public chain and the continued increase in the staking rate in the future, a price war may break out within the industry to compete for the limited market space: reduce the fees in the staking and unstaking process. If the above deduction occurs, it will undoubtedly lead to a significant reduction in the overall profit margin of the liquidity staking track, thereby reducing the value of the track projects. This has happened more than once in the traditional financial market: the stock trading commission of China's A-shares has dropped to 0.05%, and the custody business of China's banking industry can even be given away for free along with other corporate businesses.

4. Preliminary Value Assessment

4.1 Core Issues

For pSTAKE Finance, the core issue that determines its value depends on the following three aspects:

The strategy of public chain selection: From the business inflection point of rapidly expanding the BNBchain business after receiving the strategic investment from Binance, pSTAKE Finance chose to embrace the public chain with development potential, and the strategy of linking the ecology through capital and other channels is worthy of recognition. Similar development models can be used as a template for expanding new public chains.

Is there a significant discount on the liquidity staking certificate LSD: At present, the staking of ATOM and BNB, the strategic focus of pSTAKE Finance, has not experienced a significant discount due to the project itself. This is relatively friendly to large investors. At this stage, liquidity will not become a problem that hinders the development of pSTAKE Finance.

Whether LSD links enough ecosystems and expands usage scenarios: What can be seen now is that the application scenarios of stkBNB are wide enough. The future of stkATOM is still uncertain, especially in the expansion of stkATOM application scenarios, which has not yet received support from Cosmo officials, other DeFi projects and related capital parties. The team's ability to independently expand the ecosystem remains to be examined.

4.2 Valuation Level

From the perspective of static valuation, pSTAKE Finance is obviously overvalued. The high valuation may be related to the over-concentration of PSTAKE chips: Currently, more than 75% of PSTAKE chips are concentrated in a few addresses, some of which are tokens that have not yet been released. The relatively small circulating market value provides investors in the market with a large room for speculation. Compared with the current situation of Lido where 85% of tokens have entered the circulation stage, the price of PSTAKE is more susceptible to the influence of market makers.

4.3 Summary

From the perspective of business development strategy and current layout, pSTAKE Finance currently has certain competitiveness in the BNB liquidity staking track. The next test is how to expand the application scenarios of stkATOM and how to acquire customers with a high ATOM staking rate. Whether it is the project party's own efforts to expand customers or by replicating the successful case of Binance investment, the development of stkATOM is a touchstone to test the team's real operational capabilities.

In terms of valuation, the current time window may not be the best to buy PSTAKE. Investors need to wait for the price to fall or the fundamentals to grow rapidly before making a decision. If the liquidity pledge business based on ATOM shows signs of improvement, PSTAKE may be within the investment range.

5. References

Financing and Token Economy:

https://blog.pstake.finance/2021/11/16/pstake-raises-10m-to-bootstrap-liquid-staking-protocol/

https://www.binance.com/en/blog/ecosystem/binance-labs-makes-a-strategic-investment-in-liquid-staking-protocol-pstake-421499824684903831

https://blog.pstake.finance/2021/12/10/pstake-sale-on-coinlist-step-by-step-guide/

https://blog.pstake.finance/2021/12/13/pstake-tokenomics/

Alpha launchpad:https://blog.pstake.finance/2021/09/13/pstake-to-launch-on-alpha-launchpad/

Retroactive Rewards:https://blog.pstake.finance/2021/10/25/introducing-retroactive-rewards-for-stktoken-liquidity-providers/>

Binance labs:https://blog.pstake.finance/2022/05/17/pstake-binance-labs-partner-to-develop-bnb-liquid-staking-solution/

Roadmap and member information:

https://coin98.net/what-is-pstake-finance

https://icodrops.com/pstake/

https://blog.pstake.finance/2022/12/30/pstake-2022-year-in-review/

https://blog.pstake.finance/2022/05/01/stketh-ethereum-2-0-pstakes-next-leap-forward/

business:

Token staking services provided: https://blog.pstake.finance/2021/12/10/pstake-zero-to-one/

Validator selection:

https://blog.pstake.finance/2021/11/22/introducing-pstakes-validator-ecosystem/

https://blog.pstake.finance/2022/10/28/stkbnb-ecosystem-overview/

https://blog.pstake.finance/2022/02/08/expanding-the-pstake-validator-ecosystem/

BNB chain situation:

https://blog.pstake.finance/2022/10/04/the-state-of-bnb-staking-september-2022-report/

https://blog.pstake.finance/2022/10/28/stkbnb-ecosystem-overview/

The difference between stkToken and pToken: https://blog.pstake.finance/2021/12/10/pstake-zero-to-one/

ATOM staking process: https://docs.pstake.finance/stkATOM_Technical_Architecture/

ATOM staking fee: https://docs.pstake.finance/stkATOM_Rewards/

BNB staking fees:

https://docs.pstake.finance/stkBNB_Rewards%26Fees/

https://snapshot.org/#/pstakefinance.eth/proposal/0xda92d83397663e12d582627207127081adb3bc0732e4dc198e41a31ec7198cf3

https://twitter.com/pSTAKE_stkBNB/status/1621171480229969920

ETH staking fee: https://docs.pstake.finance/stkETH_Fees/

BNBchain Staking Fees:

Ankr:https://www.ankr.com/docs/liquid-staking/bnb/faq/

Stader:https://docs-new.staderlabs.com/binance/fees

SteakBank:https://docs.steakbank.finance/tokenomics/sbf/deflationary-mechanics

Characters:

https://docs.stafi.io/rtoken-app/rbnb-solution

https://app.stafi.io/rtoken/stake/BNB?tokenStandard=Native

https://twitter.com/pStakeFinance/status/1620373647474167809

BNBchain cooperation ecosystem:

Ankr:https://www.ankr.com/staking/defi/?assets=ankrBNB&types=landing

Stader:https://www.staderlabs.com/bnb/liquid-staking/defi/

steakbank:https://app.steakbank.finance/

stafi:https://www.stafi.io/

BNBchain's largest liquidity pool:

Ankr:https://ellipsis.finance/pool/0x440ba409d402e25b95ac852e386445af12e802a0

Stader:https://thena.fi/liquidity/manage/0x6c83E45fE3Be4A9c12BB28cB5BA4cD210455fb55

steakBank:https://pancakeswap.finance/swap?outputCurrency=0x43c37e8240d0fccef747d12e201bf295e4226388

Stafi:https://pancakeswap.finance/swap?outputCurrency=BNB&inputCurrency=0xF027E525D491ef6ffCC478555FBb3CFabB3406a6

pSTAKE:https://thena.fi/swap?outputCurrency=0xc2e9d07f66a89c44062459a47a0d2dc038e4fb16

BNB staked amount:

Ankr:https://www.ankr.com/staking-crypto/binance-bnb/

Stader:https://www.staderlabs.com/bnb/

steakBank:https://app.steakbank.finance/

Stafi:https://app.stafi.io/rtoken

pstaKe:https://bnb.pstake.finance/