Dear friends, welcome to SignalPlus daily news. SignalPlus Information updates macro market information for you every day and shares our observations and opinions on macro trends. Welcome to follow and subscribe to follow the latest market trends with us.

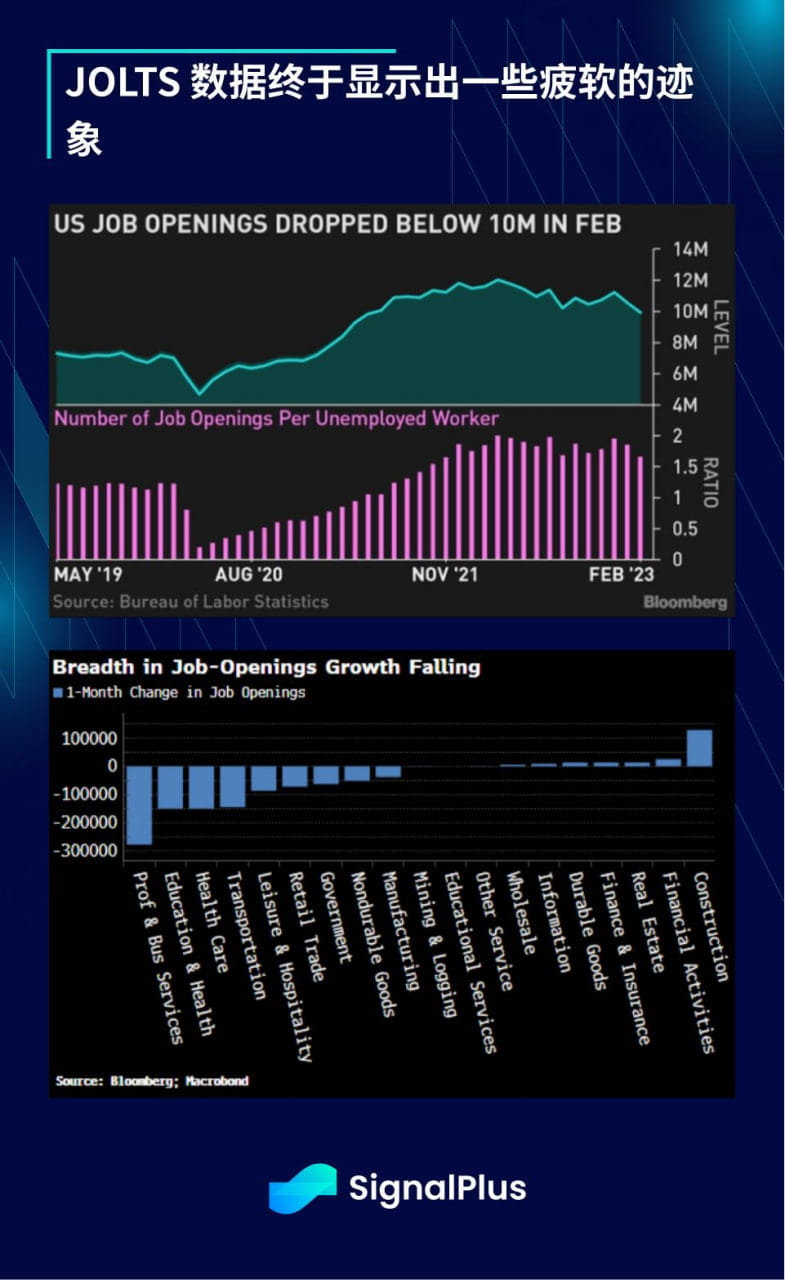

JOLTS data finally showed some signs of weakness. The number of job vacancies fell by 632,000 to 9.931 million in February, the lowest since May 2021. The ratio of job vacancies to the number of unemployed people was 1.7, and the job vacancy rate dropped from 6.4% in January. 6%, which is also lower than the high of 7.4% in March last year; the number of job openings fell to 6.163 million from the previous 6.327 million, and the hiring rate slipped to 4%, the lowest since December 2020; the weakness in job vacancies appeared in all Among industries, construction was the only one showing growth.

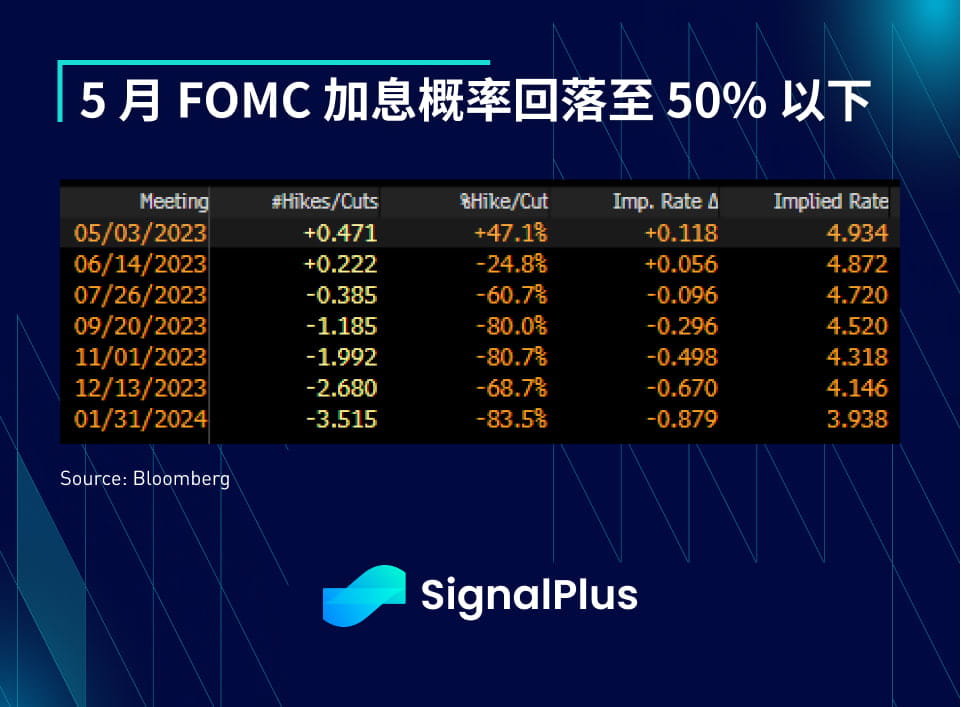

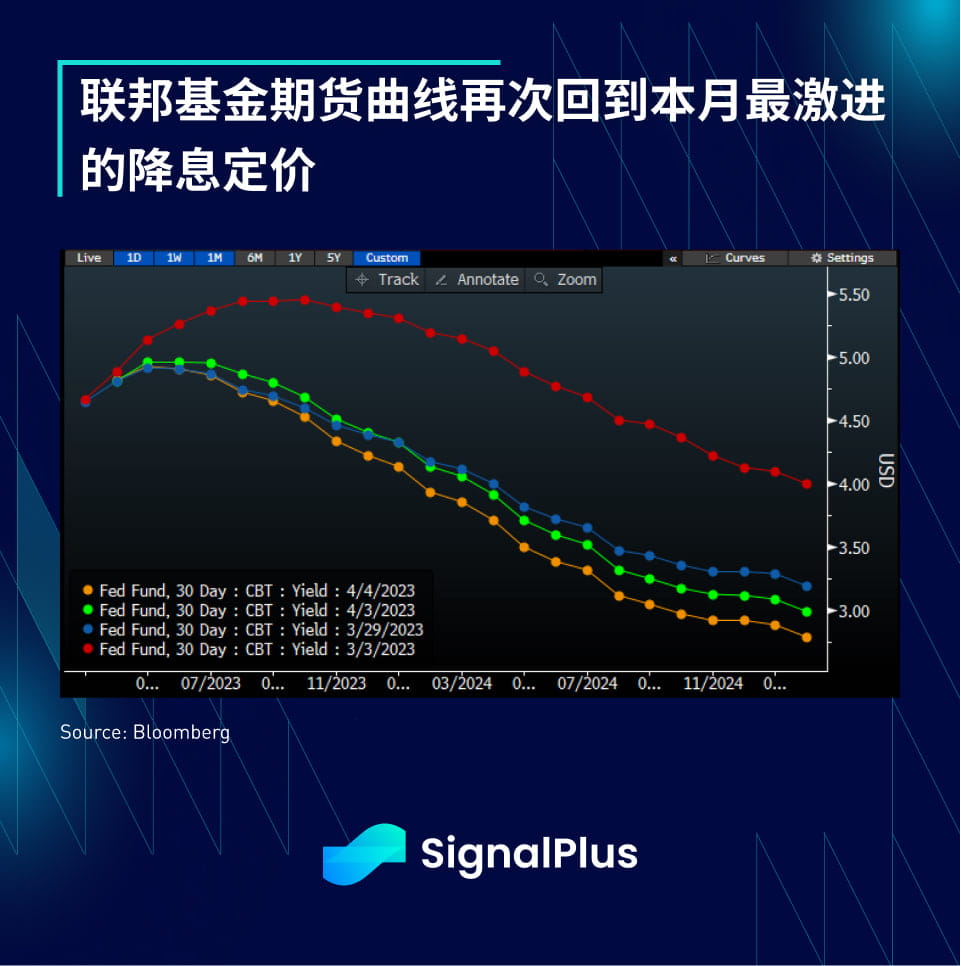

U.S. bond yields fell across the board. As the market predicted that the probability of an FOMC interest rate hike in May fell below 50%, the 2-year yield fell 12.5 basis points to 3.84%, and the 2/10-year yield curve steepened by 7 basis points. to -49 basis points. In addition, the federal funds futures curve has once again priced in cumulative interest rate cuts by the end of the year to be close to 80 basis points, with the entire forward curve falling to the lowest level this month.

Weak U.S. economic data (JOLTS fell short of expectations, Atlanta Fed GDP downgraded, U.S. factory orders dropped, etc.) caused the market's risk sentiment to cool down, interest rates fell, the yen rose, CDS spreads widened, gold prices exceeded the 2k mark, and the S&P 500 index suffered The decline in economically sensitive sectors contributed to a 0.6% decline. Equities are still performing well relative to other asset classes as corporate profits are expected to remain sustainable (at least for now) and investor positioning appears to have skewed bearish based on investor sentiment indicators. Additionally, historically April has been the S&P 500's best month since 2001, a fact that will undoubtedly be of concern to short-term investors and traders in the current environment.

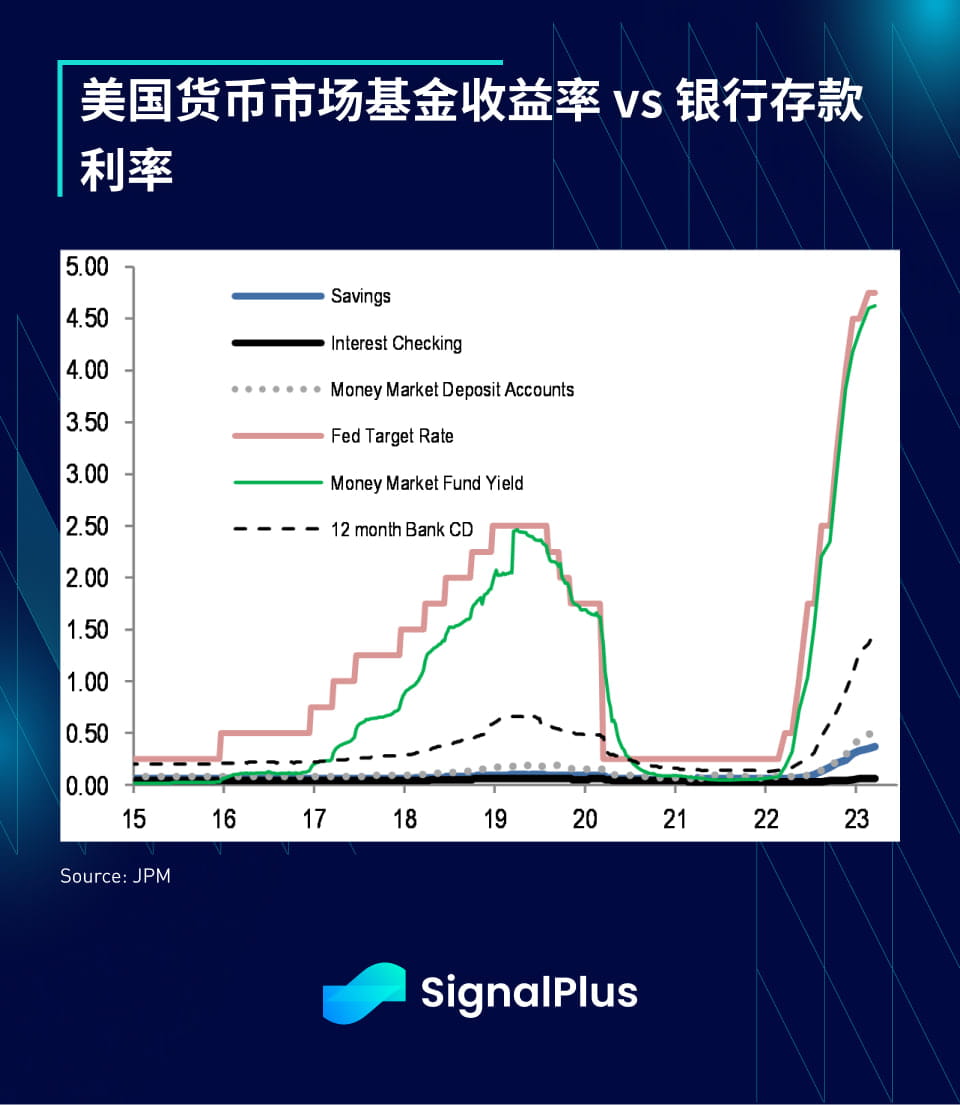

Since the banking industry failed to raise deposit rates as soon as possible, deposits continued to flow to money market funds. There was still a large gap between banks' deposit rates and money market rates. Rather than raising deposit rates across the board (that is, deposit borrowing costs), banks chose to go through the Federal Reserve BTFP plan (cost OIS+10bp) to raise funds for the deposit gap, apparently they think this will have a smaller impact on their NIM (net profit margin).

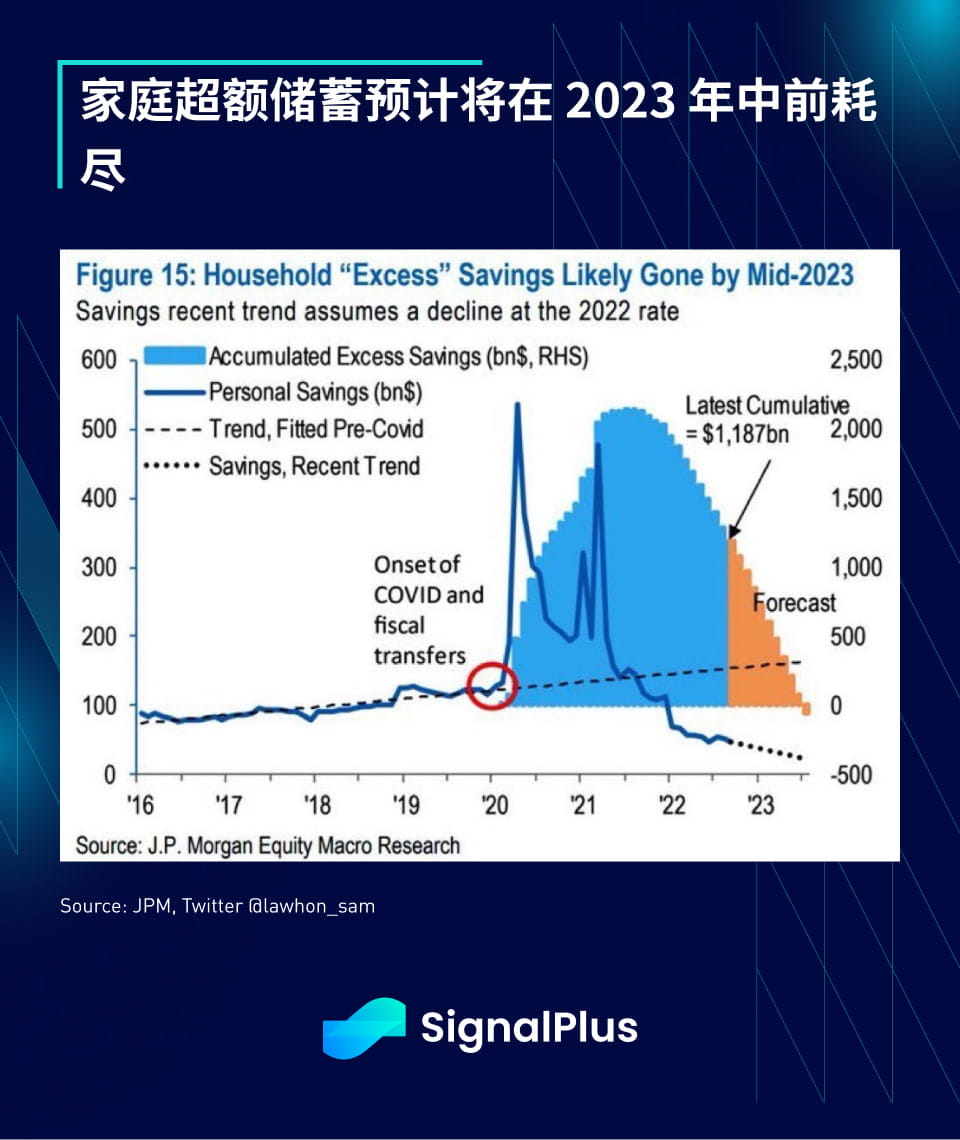

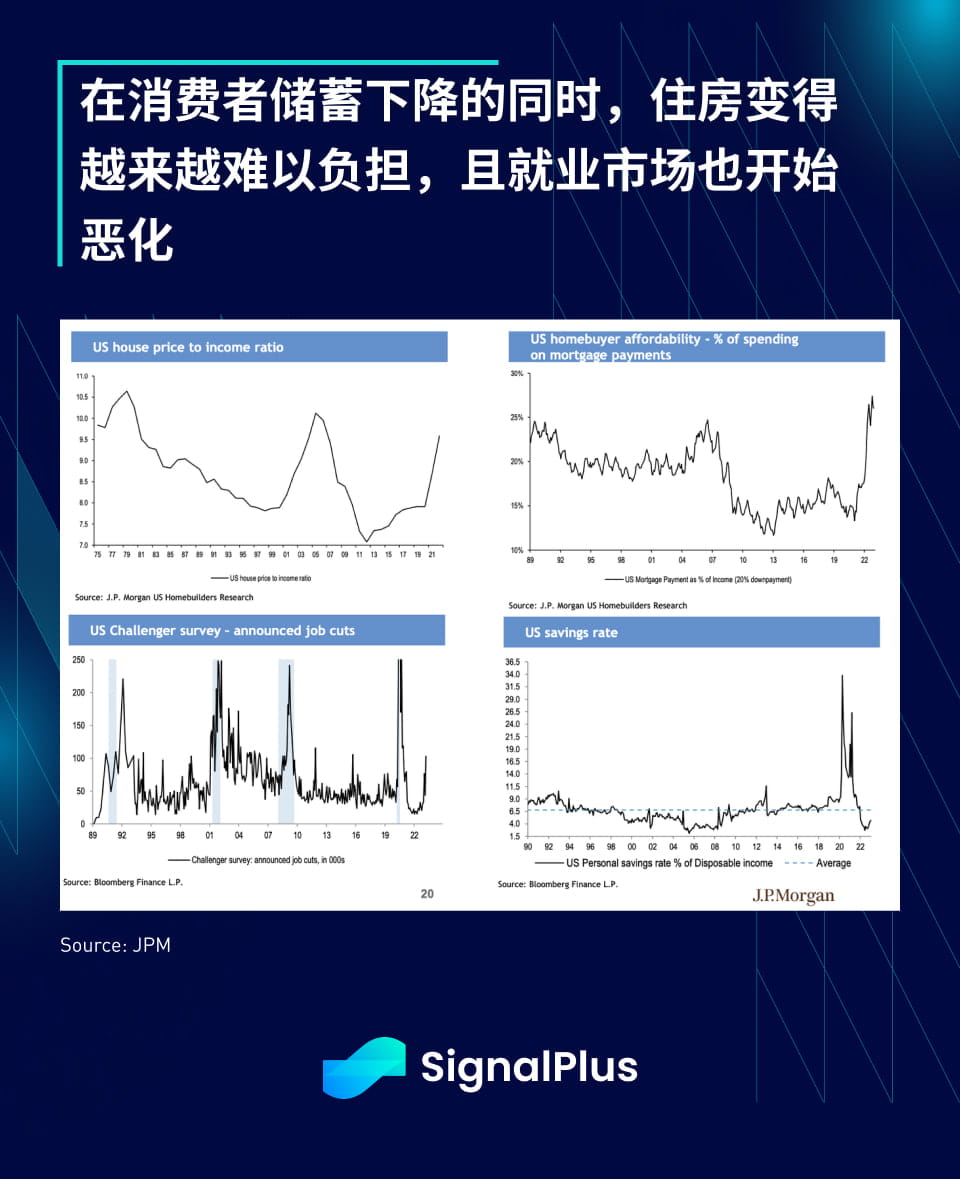

The U.S. consumer situation is finally showing signs of deterioration. The total credit card balance of U.S. consumers has exceeded a record high and has been rising sharply since the epidemic. JPMorgan Chase predicts that households’ excess savings will be exhausted before mid-2023. The total savings rate is currently at the lowest level since 2007, and This comes at a time when household affordability is also hovering near historic lows and layoffs are finally starting to increase.

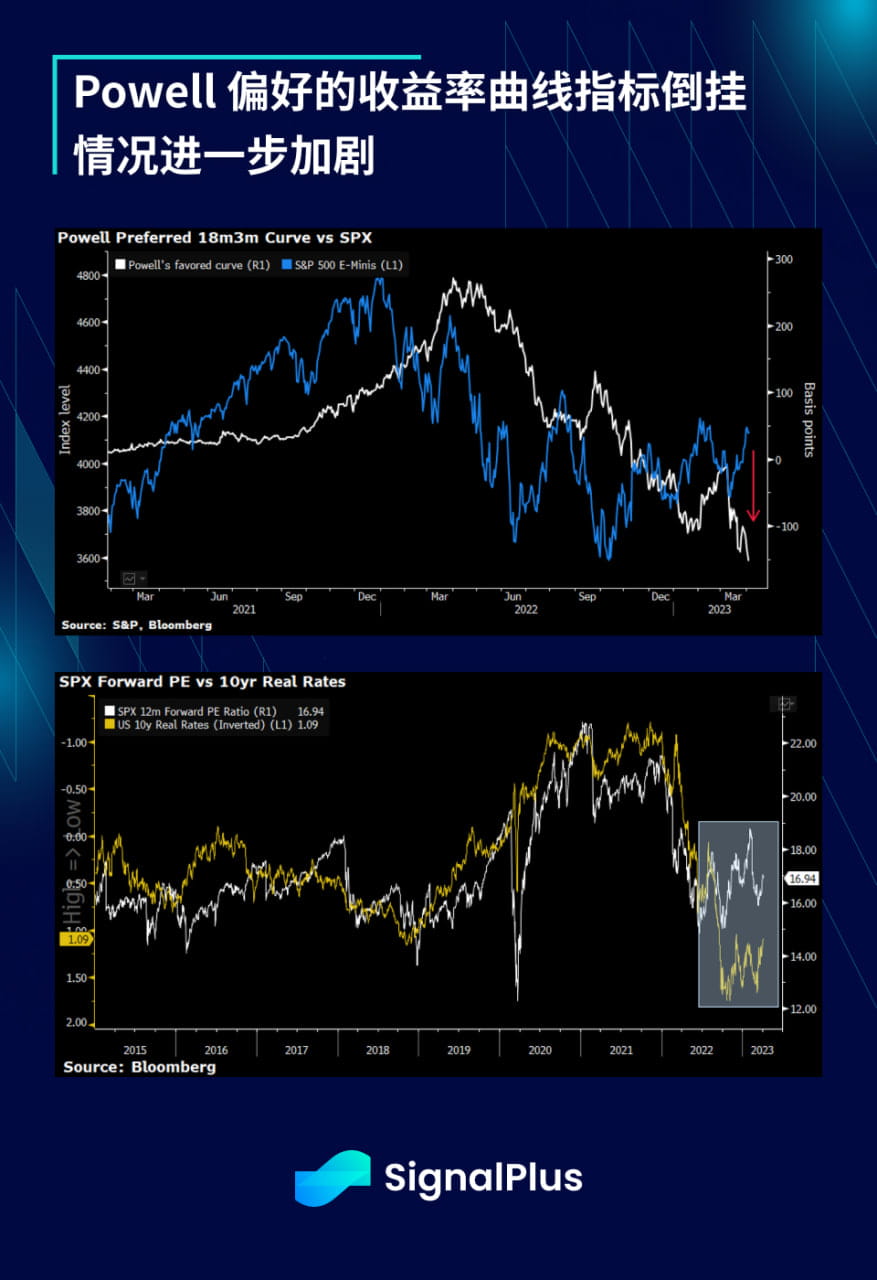

The inversion of the yield curve, Powell's preferred indicator, has intensified further, signaling concerns that the economic slowdown will become more severe. On the other hand, equity markets continue to diverge from the yield curve and overall interest rate levels and outperform, a possibility we have been reminded of since January that stocks could remain elevated until corporate earnings actually decline. Earnings season will begin in full force in about 3 weeks, and this will be the next critical period when stock prices will recalibrate based on actual Q1 earnings results.

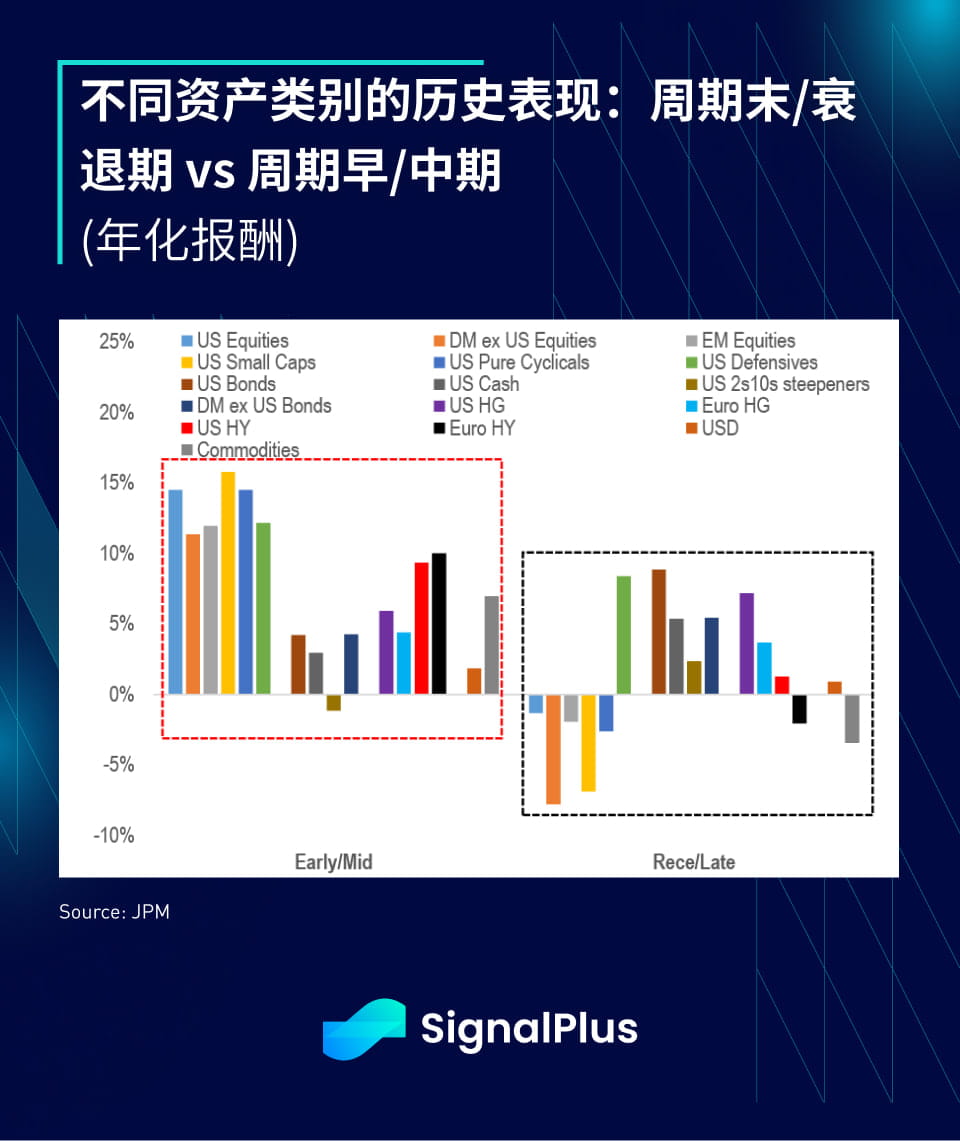

The historical performance of different asset classes shows that holding defensive stocks appears to be better than large-cap stocks at the end of cycles and during recessions. Historical performance shows that stocks other than defensive stocks may have lower than average returns while at the end of cycles. The yield curve also tends to steepen, which is what we've seen over the past month.

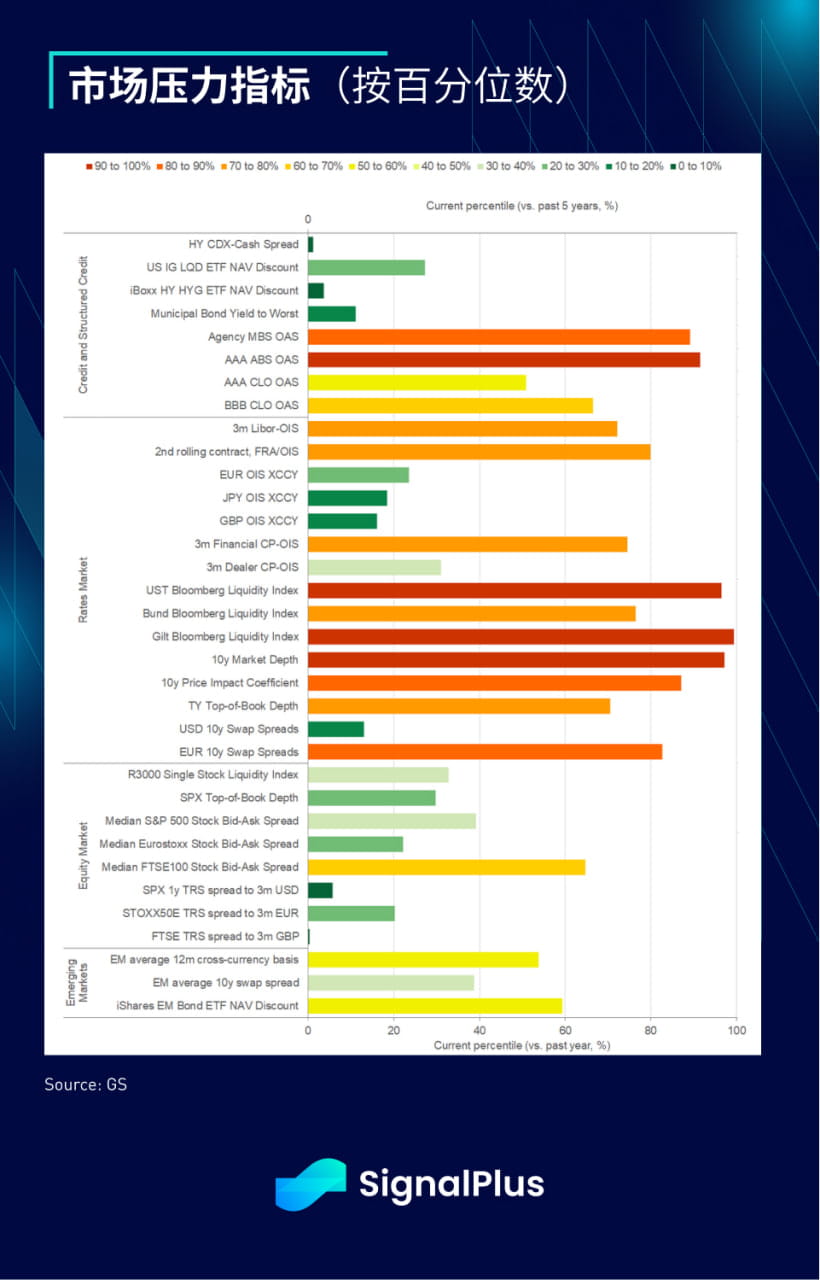

Market stress indicators show that the liquidity situation in the secondary market is still very severe. Although the performance of the stock market and high-rated credit bonds is relatively normal, MBS/ABS/CLO are still in trouble due to the surge in financing rates, and the overall liquidity situation is close to 90% levels of stress, leading to increased market volatility. The same is true for both TradFi and the cryptocurrency market. BTC’s market depth has deteriorated significantly compared to 2022. It seems that the retracement so far this year has caused a lot of pain to market participants and a lack of confidence among market makers.

The SignalPlus team will participate in the Web3 Festival organized by Wanxiang Blockchain Lab and HashKey Group at the Hong Kong Convention and Exhibition Center next week. We have prepared a series of exciting keynote speeches and roundtable forum sessions on the afternoon of April 12th. Welcome to Hong Kong. Friends come and participate in person, we are very much looking forward to meeting you!