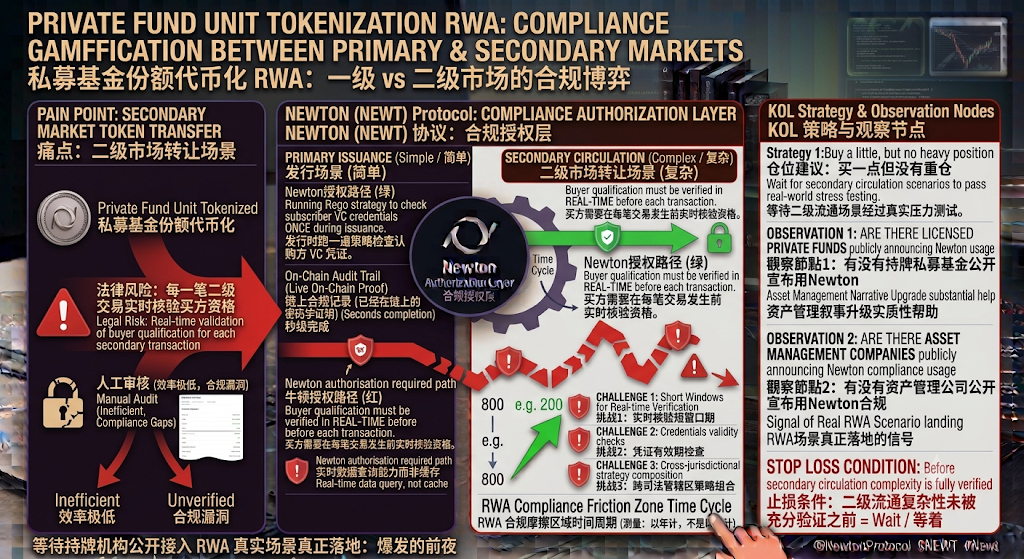

A-Yong works on LP relations at an asset management firm. They are exploring tokenizing private fund interests—so that LPs hold the fund interests in token form, which can trade in the secondary market. What’s stopping them isn’t the technology; it’s compliance: private fund interests may only be transferred to qualified investors, and every secondary-market transaction needs to verify the buyer’s eligibility. Right now, they rely on manual review, which is extremely inefficient and carries legal risk.

I said that behind the NEWT, Newton can meet this requirement at the technical level, but I need to separate the first-tier and second-tier scenarios first, because their difficulty levels are not on the same scale.

The verification process for qualified investors in primary issuance is relatively straightforward: run a strategy check at issuance, verify the investor’s VC credentials, and if it passes, allow the subscription. Newton’s architecture today can basically support this flow—with verifiable credentials + Rego policies + BLS authentication, the logic chain is complete.

The hard part is secondary circulation. For each transfer of tokenized private fund shares, the buyer must continuously verify eligibility in real time—not just verify eligibility once at issuance, but re-verify it every time shares change hands. This puts higher demands on Newton’s operator network: first, real-time performance—secondary market trading windows are much shorter than primary subscription windows; second, credential validity—buyers’ qualified investor credentials may have expired or their status may have changed, so strategies must be queried in real time rather than relying on cached results; third, cross-jurisdictional issues—secondary market buyers for private funds may come from different countries, and each country defines qualified investors differently, which makes the strategy composition significantly more complex.

All three of these challenges have corresponding technical solution paths in Newton—integrating real-time data providers, checking VC validity periods, and composing strategies across different jurisdictions. But I don’t have public data to reference whether these paths have actually been stress-tested on the mainnet.

I told A-Yong that this scenario is worth a serious assessment, but I recommend starting with a small-scale pilot beginning with compliance for primary issuance, and then expanding to secondary circulation after it works. The complexity of secondary circulation is higher than primary issuance, so validating the primary scenario first is safer.

From an investment perspective, tokenizing private fund shares is one of the fastest-growing sub-scenarios in the RWA space. If Newton can secure a few asset management firms with assets they can clearly name in this scenario, it would meaningfully help upgrade the project’s narrative.

Observational node: Are there any publicly announced regulated private fund managers or asset management firms that have used Newton’s authorization layer for compliant share transfers? Once this case comes out, I will reassess my position as a genuine signal that RWA scenarios are becoming reality.