1.

What is blockchain forensics?

A subset of digital forensics called blockchain forensics uses blockchain data analysis to investigate illegal transactions, fraud, and other types of crimes.

Blockchain is a distributed ledger, which makes it an ideal tool for financial transactions and other applications because it records transactions in a transparent and impenetrable manner. However, its decentralized and unchangeable nature also makes it an ideal venue for illegal activities.

In order to detect trends and investigate illegal activities, blockchain forensics requires the use of specialized tools and programs to extract and analyze data from the blockchain. This includes investigating blockchain data such as transactions, addresses, and other data, as well as locating and tracking people and groups engaged in illegal activities.

Many agencies, including law enforcement and regulators, are investing in creating tools and knowledge in the rapidly expanding field of blockchain forensics. As the use of blockchain technology continues to grow, effective blockchain forensics is likely to become even more important in the fight against financial crime.

2.

How does blockchain forensics work?

Depending on the specific application and the type of data being examined, the precise stages required for blockchain forensics may vary.

But by following a strict and organized process, investigators can learn important details about illegal activity on the blockchain and help fight financial crime. The general steps of blockchain forensics are as follows:

Data collection: This requires collecting all relevant blockchain data related to the query. This may include block data, transaction data, and other metadata.

Data analysis: Examining data using a variety of methods such as address clustering, transaction graph analysis, data scraping, network analysis, and machine learning. These methods can be used to discover patterns and connections between transactions and addresses, as well as to track down people and businesses engaged in illegal activities.

Visualization of results: Thanks to visualization, investigators and other stakeholders can easily understand the results of data analysis. Graphs, network diagrams, and other visual representations fall into this category.

Presentation of evidence: The presentation of analytical results in a manner admissible in a court or other legal proceeding. This may involve preparing reports, presenting evidence and providing expert testimony.

End of investigation: Once the investigation is complete, the findings are used to choose the best course of action. This may require going to court, recovering stolen property, and taking other steps to prevent financial crime.

3.

What are the various techniques for analyzing blockchain data?

Blockchain forensics involves the analysis of blockchain data to investigate criminal activities such as fraud, money laundering, and illegal transactions.

Nonetheless, the methods employed in blockchain forensics may vary depending on the specific application and the type of data being assessed, as it is a complex and rapidly evolving field. However, by combining various strategies and resources, investigators can gain a better understanding of criminal activity on the blockchain and contribute to the fight against financial crime.

The following are some of the key technologies used in blockchain forensics.

Network analysis

Blockchain transactions occur within a network of nodes. Using network analysis tools, it is possible to examine this network and discover any nodes that may be involved in illegal activity. Analyzing IP addresses, geolocation information, and other network data may fall into this category.

Machine Learning

Through machine learning, it is possible to examine large blockchain data sets and discover trends that might be difficult to spot using more traditional methods. Anomalies that could point to illegal activity can be discovered by grouping addresses, identifying strange transaction patterns, and other criminal activity.

Transaction graph analysis

Each transaction on a blockchain is linked to one or more previous transactions, forming a graph-like structure. Transaction graph analysis involves analyzing this structure to identify patterns and connections between transactions, which can help investigators identify illegal activity.

Address Clustering

Blockchain transactions are recorded using different encrypted addresses, which are called address clusters. Address clustering is a method of finding linked addresses and transactions by analyzing these addresses. This can help investigators locate people and groups engaged in criminal activities.

Data Scraping

As blockchain data becomes available to the public, specialized tools can be used to extract relevant information. Transaction data, addresses, and other metadata that can be used to discover trends and connections between transactions are examples of data scraping.

4.

What are the applications of blockchain forensics?

Blockchain forensics is a rapidly developing field with a wide range of applications in the modern digital economy. As blockchain technology is increasingly used for financial transactions, the demand for powerful and efficient forensic analysis tools is rising. Blockchain forensics can be used to improve the overall security of the blockchain ecosystem, monitor compliance, manage risk, and investigate fraud and financial crime.

Investigating fraud and financial crime is one of the main uses of blockchain forensics. Investigators can help uncover people and organizations involved in illegal activities such as money laundering and financing terrorism by studying blockchain data to discover patterns and connections between transactions and addresses. This information can be used to prosecute criminals and prevent similar crimes from happening in the future.

Monitoring compliance is an important use of blockchain forensics. Some regulatory requirements, including know your customer (KYC) and anti-money laundering (AML) laws, may apply to blockchain-based transactions. Blockchain forensics tools can help ensure that businesses and individuals comply with these standards by tracking the flow of funds and assets on the blockchain. They can also notify regulators of any suspicious activity.

Risk management of blockchain-based transactions can also be done through blockchain forensics. Blockchain forensics can help companies identify and reduce risks associated with money laundering, fraud, and other illegal activities by helping them find patterns and connections between transactions and addresses. This helps protect individuals and companies from monetary losses and reputational damage.

Ultimately, blockchain forensics can help improve the overall security of the blockchain ecosystem. Blockchain forensics tools can help stop potential criminals from using blockchain to conduct illegal operations by discovering and investigating criminal activity. This helps maintain trust in the blockchain ecosystem and ensures that it continues to be a safe and secure platform for financial transactions.

5.

How does asset tracking work on blockchain?

Asset tracking on blockchain is a process that involves recording and monitoring the movement of assets on the blockchain to increase transparency and accountability.

The following steps use Bitcoin ( BTC ) as an example to illustrate how asset tracking works on the blockchain.

Creation and registration of Bitcoin

When a new Bitcoin is created, it is assigned a unique identifier, called a transaction ID (TxID), which is recorded on the blockchain. This identity allows BTC to be tracked as it moves through the blockchain network.

Bitcoin transfer

The blockchain tracks all Bitcoin transfers that occur between users. As a result, a permanent record of BTC ownership and transaction history is created. For example, if user A sends 1 BTC to user B, the transfer is recorded on the blockchain and assigned a new TxID.

Verification and Validation

By viewing the blockchain record, the legitimacy and ownership of Bitcoin can be confirmed at every point in its path. Doing so can reduce fraud and prevent double spending and counterfeiting of BTC. For example, when user B receives Bitcoin, they can check the blockchain transaction to ensure that the BTC they received is authentic and has not been spent.

Reporting and analytics

In addition, blockchain records can be used to generate reports and analytics about BTC movements, such as the amount of Bitcoin transferred or the total number of BTC transactions. This can help companies identify patterns and improve their financial procedures.

In addition, blockchain records can be used to resolve disputes regarding the ownership or movement of Bitcoin. In this way, the ownership and mobility of Bitcoin can be clearly and independently verified due to the immutable blockchain records. For example, if there is a disagreement about who is the legal owner of a particular Bitcoin, the blockchain records can be used to determine which user has the legal rights.

6.

What are the advantages and limitations of blockchain asset tracking?

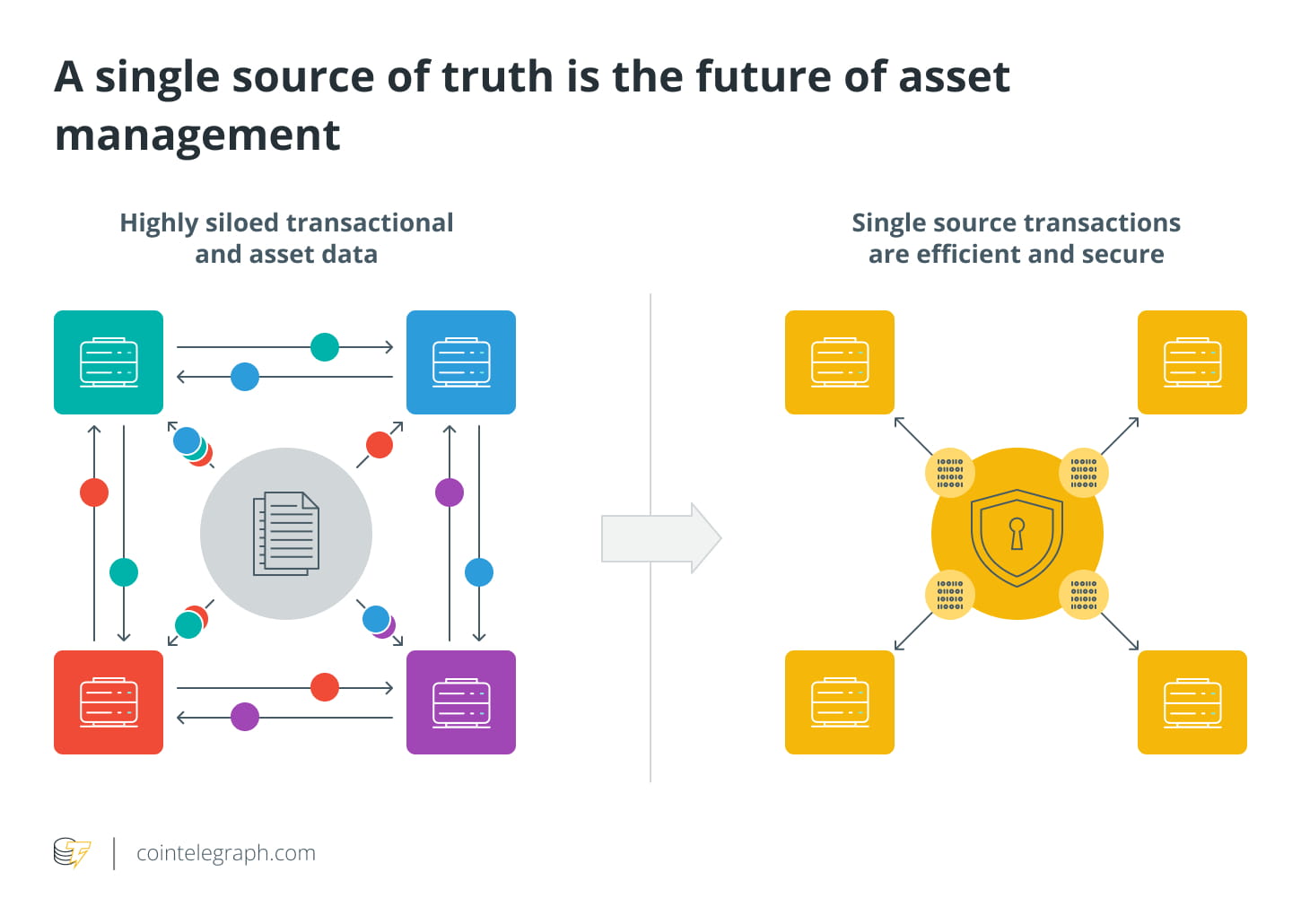

Asset tracking on blockchain has significant limitations in terms of scalability, interoperability, and lack of industry standards, but the benefits of greater efficiency, security, and transparency make it an ideal choice for many companies.

Blockchain technology offers various advantages for asset tracking, including increased efficiency, security, and openness. Blockchain provides a tamper-proof ledger of all transactions, making fraud much more difficult to occur, which is one of the main advantages. Every transaction on the blockchain is confirmed by multiple network nodes, which increases security and reduces the possibility of fraud.

Blockchain also enables real-time asset tracking, which can improve supply chain management and reduce the likelihood of product loss or theft. The ability to improve the effectiveness of financial procedures is another advantage of blockchain asset monitoring. Since blockchain-based asset monitoring does not require intermediaries such as banks or clearinghouses, transactions can be executed faster and cost less money. This can help businesses save time and money while improving cash flow.

Blockchain does have some limitations when it comes to monitoring assets, though. One of the key issues is scalability, as blockchain becomes slower and more expensive to use as the number of transactions increases. Interoperability is another issue, as there are several different blockchain platforms in use, making it challenging to track assets across multiple networks.

Furthermore, while blockchain offers a high level of security, it is not completely immune to hacking or other types of attacks. Additionally, the lack of industry standards can make it difficult for businesses to adopt blockchain-based asset tracking solutions.

7.

What are the possible future developments in blockchain forensics and asset tracking?

Blockchain forensics and asset tracking are rapidly evolving fields with great promise for future developments. These developments could help increase transparency, reduce fraud, and enhance security for a variety of stakeholders in supply chains, financial systems, and other industries.

The combination of blockchain forensics and asset monitoring with artificial intelligence (AI) and machine learning (ML) could be a game changer in the future. Large data sets can be analyzed using AI and ML algorithms to spot anomalies that could point to fraudulent activity. This could make it easier for regulatory and law enforcement agencies to investigate and prevent financial crime.

As Internet of Things (IoT) devices become more widely adopted, more assets may be tracked on blockchains. For example, IoT sensors can be used to track the location and condition of goods during transportation. As a result, supply chain participants may be able to track and confirm the legitimacy of assets in real time.

Additionally, smart contracts may be used in the future to simplify asset tracking and reduce the possibility of fraud. For example, a smart contract could be created to automatically transfer ownership of an asset when payment is received.

Additionally, zero-knowledge proofs can be used to provide more secure and private blockchain-based systems. Businesses and individuals concerned about data privacy may find this particularly important.