Gearbox V3 creates additional Alpha Pool revenue opportunities for main pool lenders, and can add more mid-tail and long-tail assets as well as a variety of DeFi and NFT protocols, and cross-chain deployment will also become possible. In addition, Gearbox V3 will adopt an innovative mechanism of whitelist asset risk exposure cap and quota customization to ensure sufficient available liquidity on the chain and alleviate lending risks to a certain extent.

Written by Karen, Foresight News

DeFi composable leverage protocol Gearbox Protocol announced the details of its V3 upgrade this week, and sees the new version as the DeFi leverage base layer that redefines leverage and lending. So what can Gearbox V3 achieve? What new features or characteristics are worth looking forward to?

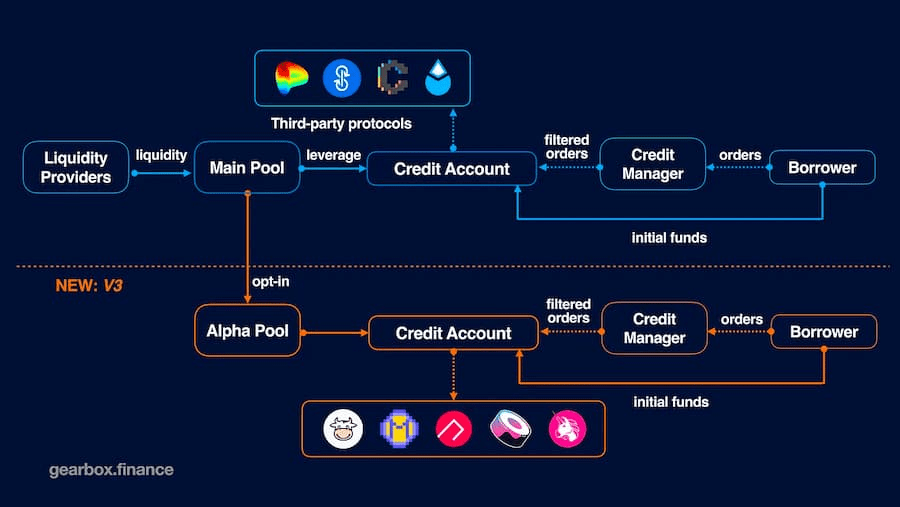

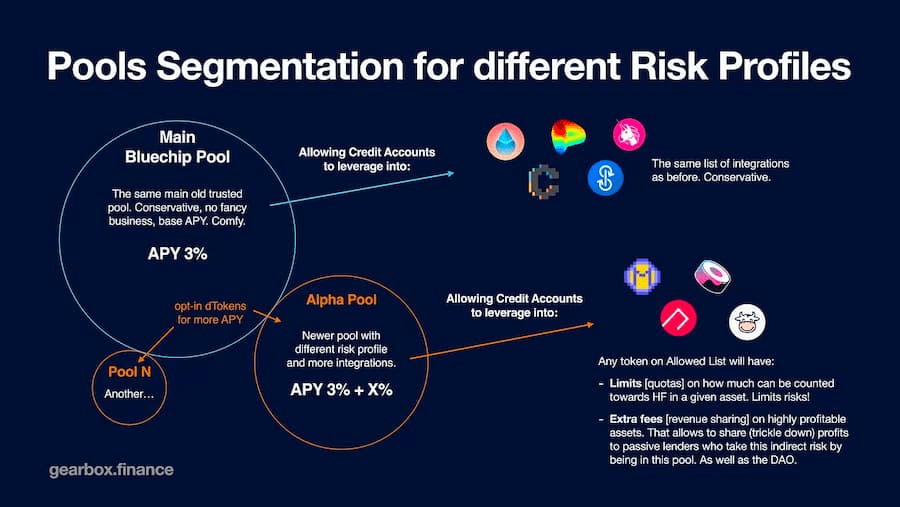

1. LP lenders: stay only in the mainstream blue chip pool or transfer dTokens to the Alpha pool

V3 builds on the performance and codebase of V2, allowing not only the addition of lower liquidity pools, tokens, and protocols, but also the ability to modularize these pools, providing users with more additional options without fragmenting liquidity.

That is to say, lenders continue to provide liquidity in the current very conservative mainstream blue-chip lending pools to obtain dTokens, or they can choose to deposit these main pool dTokens in the riskier Alpha pool to earn more APY, but they need to take more risks.

Additional Alpha pools will integrate more DeFi and NFT protocols, but the integration of such pools will still set relatively conservative LTV (loan-to-value ratio) and strict liquidation rules. The APY obtained by lenders includes the base APY of the mainstream blue chip pool plus the base APY of the Alpha pool and additional fees collected from quotas. In addition to Alpha, there may be other modular pools in the future.

2. Mitigate lending risks through customized settings of risk exposure limits and quotas

Gearbox V3 will allow the introduction of an overall risk exposure cap for whitelisted assets (recommended and governed by the Risk Committee). Each whitelisted asset will have a threshold (denominated in the underlying asset of the corresponding lending pool), that is, the total risk exposure value (quota) of this asset among all credit accounts borrowing from the pool must not exceed this cap.

The actual amount of assets used as collateral for a particular CA is determined by a quota, which is also denominated in the underlying asset. Each borrower can set any quota value they want for each mid-tail asset. The larger the quota you set, the higher the interest you will need to pay.

If the actual asset value of the user in the pool exceeds the quota, the excess will not be counted. If it is less than the quota, the actual value will be regarded as risk exposure. The sum of all quotas will not exceed the overall risk exposure limit.

Gearbox said that this mechanism can add long-tail, mid-tail assets and other low-liquidity assets, as well as other protocols or asset classes without increasing protocol risks, while ensuring liquidity availability and eliminating bad debt problems. It will also make cross-chain or Layer2 deployment possible without worrying about low Layer2 liquidity.

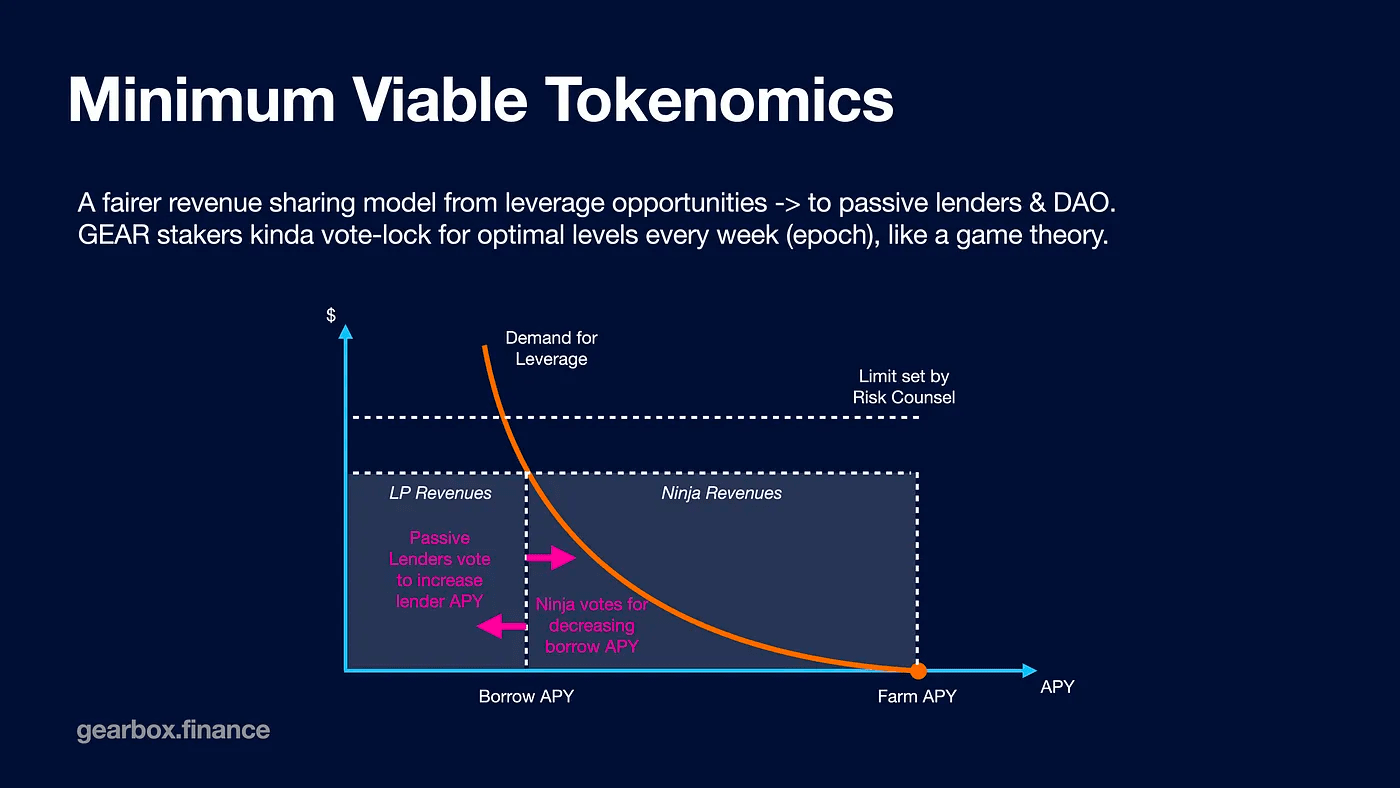

3. Introducing Quota Interest and Reshaping Token Economics

V3 will also introduce a new interest derived from quotas. The additional interest paid by borrowers is related to the quota of each asset, not the actual borrowing amount. The quota interest will be paid to the Alpha pool, that is, the interest received by the Alpha pool includes: the mainstream blue chip pool basic APY + Alpha APY + quota interest. Then the DAO will charge a certain interest fee from it.

The quota APR consists of two parts: one is the minimum risk premium paid to LP based on exposure risk, which is set by the Risk Committee and the APR must not be lower than this value; the other part above the minimum risk premium will be divided between leveraged borrowers (Ninjas) and LPs. The maximum APR is estimated by the Economics Committee, and both values are revised regularly.

The balance between Ninjas and LPs becomes a very important issue that deserves attention and caution. The specific distribution ratio will be determined by the on-chain voting of GEAR token holders. GEAR holders vote for LP bucket or Ninjas bucket. The proportion of GEAR in each bucket determines the actual APR value.

To avoid exploits and prevent flash-voting from quickly skewing funds towards a particular token or pool, GEAR token holders may have a 1-4 week unstaking period for tokens locked by voting. A vote is held at the beginning of each epoch, and votes that do not change the selection are automatically rolled over to the next epoch. Stakers may also share a portion of the additional revenue.

In addition, V3 will also add the automated contract Gearbot, which allows credit account owners to delegate certain management of their active accounts to third parties, thereby performing automated portfolio management, such as stop loss, stop profit, automatic maintenance of health index, automatic measurement management, etc. In addition, it will also become easier to create automated management on-chain funds, and depositors will not have to entrust their funds to third parties.

summary

Gearbox V3 is expected to be launched at the end of the second quarter. This version will not only create additional Alpha Pool income opportunities for main pool lenders, but will also add more mid-tail and long-tail assets as well as a variety of DeFi and NFT protocols. In addition, Gearbox sets an innovative mechanism for whitelist asset risk exposure caps and quota customization to ensure that there is sufficient available liquidity on the chain and alleviate lending risks to a certain extent. It is also expected to help Ethereum and other public chains/network ecosystems with lower liquidity provide safer, more liquid leverage and lending composable functions, thereby bringing more composability and possibilities.