Looking back at the crypto market over the past month, there seems to be signs of recovery. In the process of multiple narratives and sector rotation, the performance of the new public chain Aptos has left a deep impression: in just 20 days from mid-January, the price of Aptos jumped from US$4 to US$20, and its trading in the Asian market, especially in South Korea, was once very hot.

Under the axiom that "pulling the price is justice", people tend to focus on market sentiment, and there are endless discussions about when Aptos will get on or off the train; but in contrast to the lively market, the actual development of the Aptos chain is currently somewhat deserted.

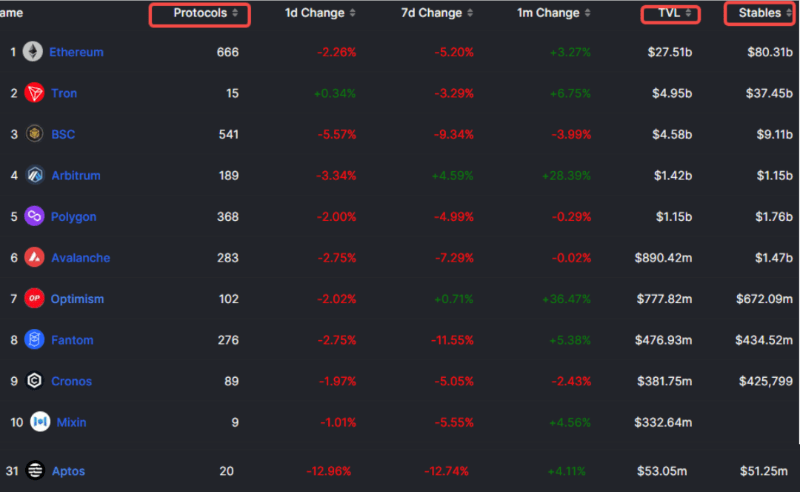

Statistics from DefiLlama show that the total TVL on the Aptos chain is only US$53 million, ranking 31st among all public chains; and data such as the total number of ecological projects and the total amount of stablecoins on the chain are quite different from those of popular new public chains.

A vertical comparison of the data intuitively shows the current weakness of Aptos' ecosystem, and the lack of native DeFi and stablecoins is even more obvious: Pancakeswap accounts for more than half of Aptos' total TVL, and the on-chain stablecoin USDC has a market share of nearly 80%.

On the other hand, well-known public chains and DeFi applications, such as BSC, Curve and AAVE, are all trying to develop their own stablecoins in order to gain a competitive advantage.

As the value anchor of the public chain ecosystem, native stablecoins can stimulate liquidity and create revenue, which is crucial for building successful DeFi applications and attracting users. Aptos’ lack of this link is bound to be unfavorable for long-term competition, but where there is a problem, there is an answer: the pioneer who fills the gap in native stablecoins has quietly emerged: Thala Protocol.

The project created the native stablecoin MOD on Aptos, "Move Dollar", based on the Move language, and built a relatively complete product portfolio with its own AMM and Launchpad;

When the Aptos market performs strongly, value is more likely to spill over to its ecosystem projects; and the numerous repeated narratives in this circle tell us that those projects that can fill the gap first often contain higher opportunities and are worthy of early attention and understanding.

On February 25, the project’s testnet was launched. After actual experience, the full picture of Thala Protocol gradually emerged, and we will also provide you with an in-depth interpretation.

Stablecoin MOD, the value anchor of Thala

In Thala, stablecoins are the cornerstone of the entire protocol. Faced with the problem of lack of native stablecoins on Aptos, the protocol first brings a new stablecoin "Move Dollar" (MOD for short). It is easy to understand from the name that MOD is developed based on the Move language and assumes the functions of on-chain value storage, medium of exchange and accounting unit; at the same time, MOD prioritizes serving the Aptos ecosystem and can be used to interact with various other DeFi protocols in the ecosystem.

Behind the name, the design mechanism of the MOD is more worthy of attention.

Unlike algorithmic stablecoins such as UST, MOD uses a collateralized debt position and over-collateralization model similar to DAI to design the supply and recovery of stablecoins. The first is the Collateralized Debt Positions (CDP), which is commonly known as the vaults we see in various DeFi protocols. It is essentially a lending management method based on smart contracts.

When a user needs to borrow (mint) MOD from the protocol, they need to deposit a certain amount of other assets into the vault as collateral; when the user returns (destroys) MOD to the protocol, they can get back the previously collateralized assets. When the total value of the collateralized assets is lower than a certain safety threshold, the collateralized assets will be liquidated. It should be noted that this collateral is excessive: users can only borrow MOD that is lower than the total value of the collateral, and each MOD is always pegged to $1. For example, to borrow 1 MOD, the total price of the assets that need to be collateralized in the vault may be $1.5.

So, what exactly will these over-collateralized assets be in the Thala protocol?

According to the official design documentation, MOD is supported by Aptos native and multi-chain assets, and continues to focus on yield-generating collateral types, including but not limited to: liquidity pledge derivatives, liquidity pool tokens (LP tokens), and certificate of deposit tokens.

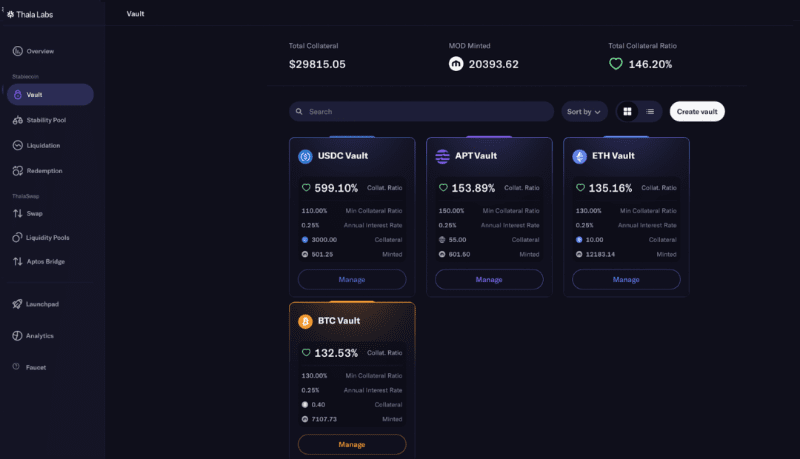

From the actual interface of the current product, we can see that on-chain assets such as USDC, APT, ETH and BTC can be used for over-collateralization. Users can freely select a Vault and click the "Manage" button to mortgage and redeem assets. In addition, the real-time mortgage rate displayed in the upper right corner of the interface is about 146%, which also means that the total value of the mortgaged assets is higher than the total value of the minted MOD.

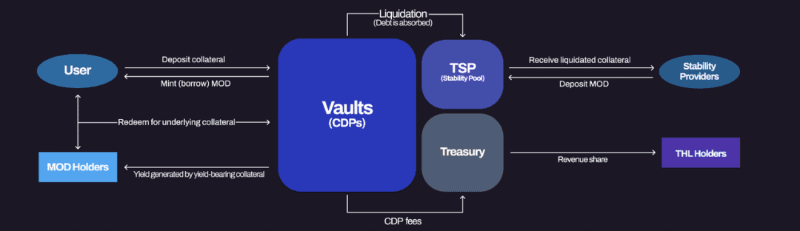

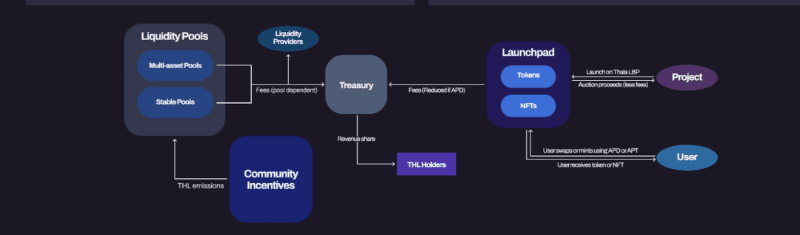

After understanding the design mechanism of MOD itself, we can more easily connect the entire business process related to MOD and further analyze the output, circulation, role and stakeholders of stablecoins:

Users pledge assets to the Vault, mint/borrow MOD stablecoins through over-collateralization, and can redeem pledged assets under normal circumstances;

Users holding MOD can obtain certain benefits through Staking or Rebase mechanism;

The fees incurred when users lend and redeem MOD, such as interest/redemption fees/liquidation penalty interest, etc., will flow into Thala's treasury and be rewarded to the holders of the project token (THL);

When the price of the collateral asset drops to a certain threshold, the liquidation process will be triggered. At this time, the collateral assets in the vault are unable to repay the borrowed MOD, resulting in a deficit.

To make up for the shortfall, the "stablecoin pool" that maintains the stability of the treasury comes into play: when liquidation occurs, it means that the price of the collateral assets drops. Others can deposit MOD stablecoins into the pool, which allows the MOD in the pool to buy these collateral assets at a "discount price".

At this point, the MOD used to purchase collateral assets fills the gap caused by the previous liquidation, and the providers of these MODs can be regarded as LPs of the "stablecoin pool" and also gain benefits. From the product's stable pool page, you can also see the various asset rewards that can be obtained by staking MOD. Users only need to click Claim to realize the benefits of the above liquidation logic.

When we look beyond the design details of MOD to consider its strategic value, we will find that its role as a value anchor becomes increasingly apparent: starting from the stablecoin itself, to create more product features, usage scenarios, and cooperation possibilities.

For the Thala protocol itself, the existence of MOD gives users more reasons to use the product. Whether it is a stable pool that can earn income or lending stablecoins to seek more income, users need to complete it in the Thala protocol; at the same time, due to the existence of MOD lending/returning mechanisms, the fees generated can be distributed to THL (Thala protocol token) holders, which has also become an important source of token value capture.

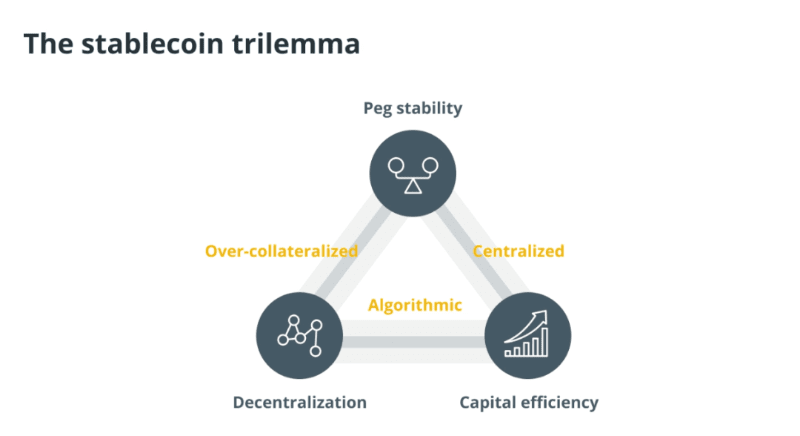

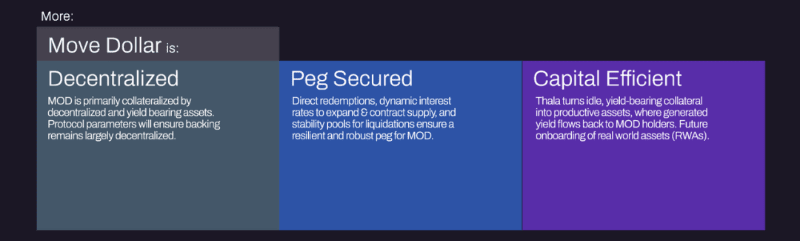

For the entire Aptos ecosystem outside of Thala, the minting and supply of MOD can provide a source of liquidity for other DeFi projects and derive more usage scenarios and utilities. But don’t forget that MOD is essentially still an “overcollateralized” stablecoin. While assuming the role of a value anchor, it may also be subject to the classic “stablecoin triangle dilemma” - for a certain stablecoin, it is impossible to achieve currency stability, decentralization, and capital efficiency at the same time.

MOD's over-collateralization and stability pool mechanisms ensure the anchoring to $1 as much as possible, and achieve decentralization through the design of smart contracts. However, over-collateralization also means reduced capital efficiency. After all, there is an opportunity cost for the "excess" part of the assets. Can the assets create more income and liquidity after being pledged?

Obviously, Thala is also aware of this problem and hopes to break through this triangular dilemma through Thala Swap related to the MOD stablecoin.

Thala Swap, providing liquidity for stablecoins

In order to provide MOD with higher capital efficiency, better liquidity and more usage scenarios, the Thala protocol designed another product: Thala Swap, a DEX based on the automated market maker mechanism.

In Thala Swap, MOD stablecoin is used as the underlying asset and derived into 3 different types of pools to obtain liquidity. While generating income, it interacts with different assets according to different pool formation rules.

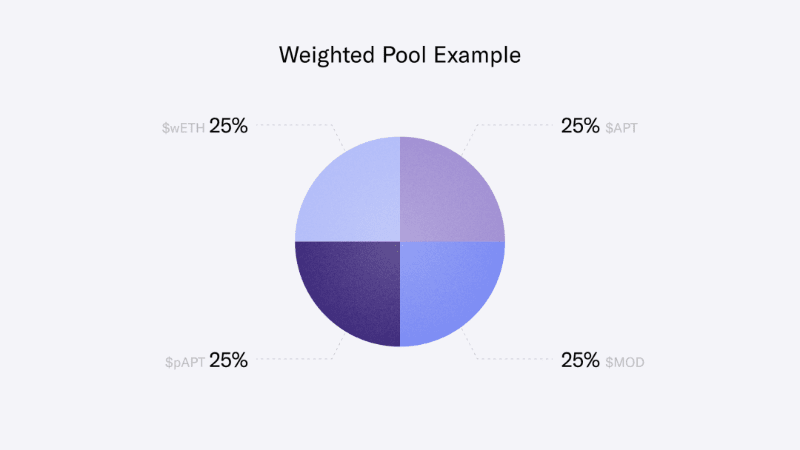

Weighted pool: permissionless creation, and the weight and number of assets in the pool can be freely designed

Generally, pools based on the automated market maker mechanism only contain two assets, each with a weight of 50%. Thala's weighted pool allows users to freely build pools with different numbers and weights of tokens without permission. For example, as shown in the figure below, users can choose to form a pool with four assets, THL, MOD, APT and wETH, with each accounting for 25%.

In this case, a significant advantage is that there will be more Swap options. 4 assets are in the same pool, and each asset can be traded with another, which also means that there are 6 different exchange possibilities for THL-MOD-APT-wETH. In theory, more redemption possibilities will increase users' willingness to redeem, thereby increasing the handling fees in the pool to reward LP providers.

At the same time, the MOD added to the pool has no strong correlation with the price of other assets, which is a security item that can be prioritized for pooling strategies. Since weighted pools are permissionless, MOD is more likely to be added to different pools, which not only increases its own liquidity, but also enriches the user's pooling strategy.

Stability pool: designed for equivalent asset exchange

Traditional AMM pools can perform well when exchanging multiple different assets, but they are unable to do so in some special cases. For example, for wETH and ETH, or stETH and ETH, the two assets are of equal value, and general AMM pools are often inefficient when exchanging such trading pairs.

Thala Swap's stable pool refers to Curve's design and is specifically used for the above scenarios, such as stablecoins, synthetic/wrapped assets, and derivatives generated by staking, allowing users to exchange at a lower fee.

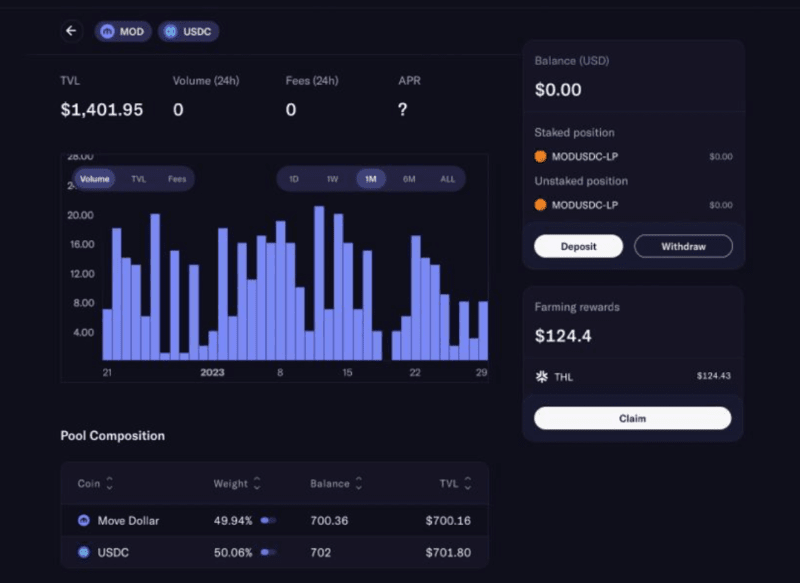

As shown in the figure below, users can find a stable pool consisting of MOD-USDC in the Swap function. Both stablecoin assets are anchored to the US dollar, and the value is usually 1:1. Users can choose to deposit assets to act as LP to earn income, or they can exchange one stablecoin for another in the pool.

For non-native stablecoins, if you want to participate in the pool composed of MOD after entering the Aptos ecosystem, you can choose to redeem MOD in the stable pool first. This actually facilitates the entry of liquidity on other chains into Aptos.

Liquidity bootstrap pool: created with permission and consistent with the weighted pool principle, suitable for new asset issuance

The principle that weighted pools can allocate multiple assets and design weights provides a good tool for the issuance of new assets. Similar to the design rules created by Balancer, liquidity bootstrap pools are special weighted pools that guide users' liquidity to participate in the exchange of assets in the pool by setting the initial weights and ending weights of two assets within a certain period of time.

Players who are very familiar with DeFi will quickly realize that this mechanism is actually a modified Dutch auction: due to the different initial weights of the two assets in the pool, assuming that the new asset to be distributed has a lower initial weight in the pool, its relative price will be higher; over time, after the pool is started, the price of the assets that need to be auctioned and distributed will undergo cyclical changes with buying and selling pressures. In market behavior, the price of distributed assets will gradually decline relatively, and eventually the weights of the two assets in the pool will be the same.

This liquidity bootstrap pool allows new tokens to be distributed more easily in a fairer way than the traditional IDO method, which means it is easier to gain favor from other projects in the Aptos ecosystem. When ecosystem projects want to start their own token distribution, the function of the liquidity bootstrap pool actually provides Thala Swap with a project launchpad:

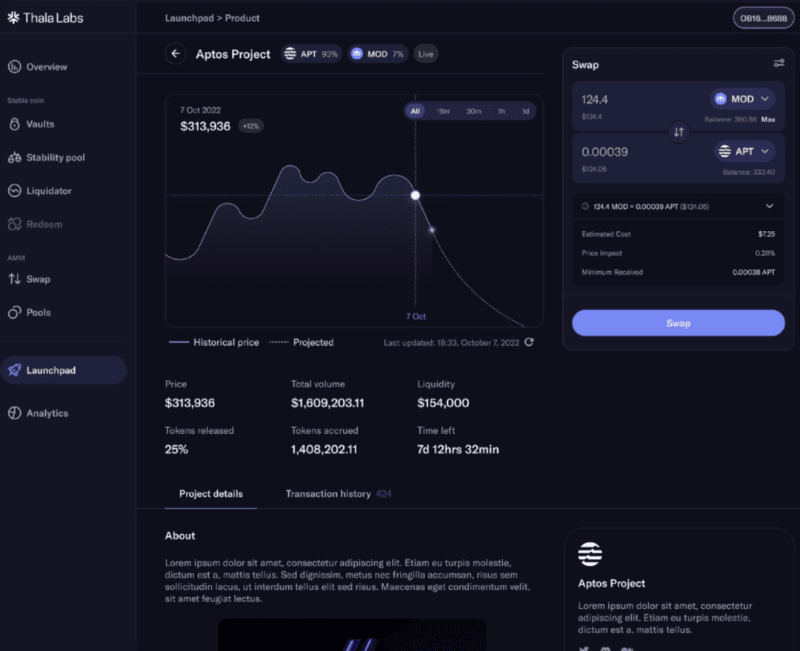

Ecological projects on Aptos can directly choose to open the above-mentioned liquidity bootstrap pool on Thala Swap, and quickly implement it by setting parameters such as weight and duration; on the user interface, the liquidity bootstrap pool means an auction of new tokens.

As shown in the figure above, users can directly view detailed information, related links, token distribution status, etc. of new projects through Thala's Launchpad page, and can use the assets specified in the bootstrap pool to redeem new tokens under the current market supply and demand environment.

In fact, Launchpad has served as an amplifier for the development of the Aptos ecosystem: considering the convenience of pooling and the support of the MOD stablecoin, projects in the Aptos ecosystem can give priority to logging into Thala Swap to complete the issuance of new assets, which objectively creates conditions for the flow of MOD in different ecological projects.

One possible scenario is that the Thala protocol may become an on-chain DeFi protocol that integrates stablecoin issuance, secondary markets, and primary markets. It will increase cooperation with other Aptos projects through stablecoins and launch pads, and attract user participation with diverse pooling strategies and benefits.

Future Outlook

Thala's testnet has just been launched for a few days, and more than 25,000 people have participated in the test. Although it is difficult for us to make a conclusion about the future development of the product, based on the current situation, we can see that Thala also has certain strength to polish the product.

Public information shows that most of its team members are real names, and the founders, core contributors and consultants have crypto-native and traditional technology backgrounds. Members come from companies such as MakerDAO, ParaFi Capital, NEAR, Twitter, Apple, Google, Amazon, etc.

Despite the sluggish environment in October last year, the project also completed a US$6 million seed round of financing, led by Shima Capital, White Star Capital and Parafi Capital, and followed by strategic investors including BECO Capital, LedgerPrime, Infinity Ventures Crypto, Qredo, Kenetic, Big Brain Holdings, Karatage, Saison Capital and Serafund.

Looking ahead, it is an indisputable fact that the competition among new public chains is not limited to performance narratives. Whether a chain is good or not ultimately needs to be measured from the perspective of ecology and application. The Thala protocol, which provides Aptos with stablecoins, asset liquidity, and ecosystem construction tools, is functionally solving the pain points of Aptos' lack of ecology and native original currency.

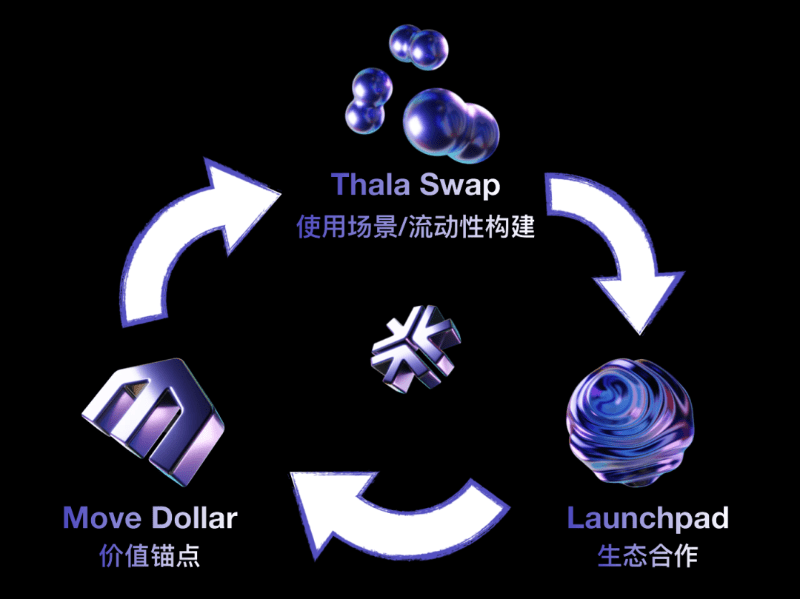

Judging from the functions and design concepts presented by the product, the overcollateralized MOD not only has decentralization and stability, but also connects to Thala Swap to maximize the efficiency of capital utilization and break through the "impossible triangle" of stablecoins as much as possible; and the combination of MOD + Swap + Launchpad allows us to see a flywheel that creates value from the inside out:

Internally, MOD is given functions and scenarios to generate income, and the establishment of various trading pairs is openly encouraged to promote the use of MOD within the protocol;

Externally, Aptos ecosystem projects are encouraged to interact their treasury assets with MOD, promoting the use of MOD in the Aptos ecosystem.

When more applications deeply collaborate and integrate with MOD, there will be more trading pairs listed on Thala, and liquidity will deepen. At the same time, more projects will sell tokens in the primary market on Launchpad, becoming the basic pillar of the Aptos DeFi ecosystem, which may be promising in the future.