When I received a reminder of 50,000 U at 3 a.m., I was still fantasizing about my car replacement plan. Three hours later, a bank text message suddenly popped up an "account freeze" notification. This 45-day card freeze made me run to the police station six times, submit 27 transaction certificates, and ultimately lose 32,000 U in handling fees + 18,000 U in deposits. As a "senior leek" who has paid millions of tuition fees, today I will disassemble this (safe withdrawal system) that I worked hard on into a reproducible operation manual to help you avoid 99% of the pitfalls.

Act I: Frozen Card Purgatory - The Minefields of Deposit in Those Years

Reconstruction of the bloody scene:

One night in 2024, I trusted a third-tier platform's "high exchange rate C2C" and used my personal WeChat account to receive three payments totaling 28,000 U.S. dollars in exchange for "buying a house." 72 hours later:

China Merchants Bank card frozen (the capital chain involved is linked to a gambling platform)

Alipay balance is under risk control (transfer received from the same account)

Received a call from the Economic Investigation Bureau asking for cooperation in the money laundering investigation

Even more bizarre was the second card freeze: I used a friend's bank card to collect 100,000 U.S. dollars. The other party's account was blacklisted by the central bank for "participating in virtual currency transactions," which directly led to the freezing of three of my savings cards. The bank employee pointed out Article 23 of the "Anti-Money Laundering Guidelines," which reads shockingly: "Knowingly accepting funds from virtual currency transactions may be treated as aiding and abetting money laundering."

Act II: Jedi Counterattack — Three Iron Rules to Reconstruct the Withdrawal System

Iron Rule 1: Compliance Screening — The Survival Rule of Only Recognizing Yellow Label Merchants

The life and death line of platform selection:

Risk Level Platform Type Card Freezing Probability Recommended Index Hell Level Non-compliant Small Platform 92% ❌ Caution Level Second-tier Exchange 37% ⚠️ Security Level Top Platform C2C 8% ⭐️⭐️⭐️⭐️

Practical example: Fixed use of Binance's "Aegis Merchant" system, with the following filter conditions:

Registration duration > 1825 days (more than 5 years)

Historical transactions > 10,000

Positive review rate 99.8%+

Support "T+3 Funds Isolation" (Merchant funds must be frozen for 3 days to confirm compliance)

Iron Rule 2: Dispersed Bomb Defusing — The Art of Risk Control at Ant Moving

Large withdrawal breakdown formula:

100,000 U = 5,000 U × 20 transactions (completed in 20 days)

Key tips:

Withdraw no more than 20,000 U per week (avoiding the bank's "abnormal transaction monitoring" threshold)

Use the exchange's "smart split" feature (such as Binance C2C's "auto split transfer")

With multi-currency channel: USDT → BTC → fiat currency (increases the difficulty of fund tracing)

Actual combat record:

Plan U: Withdrawal of 86,000 RMB in March 2025:

① 2500U each at 10:00/15:00 daily

② Use 3 dedicated bank cards alternately (daily transaction amount per card ≤ 5000U)

③ The interval between each withdrawal is ≥ 4 hours (simulating normal trading frequency)

Finally, zero risk control was implemented, and the total handling fee was 126U (accounting for 0.15%)

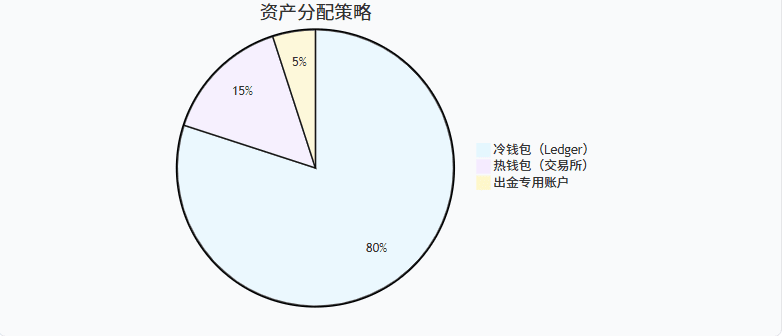

Iron Rule 3: Asset Fortress — Cold Wallet + Multi-Signature Defense System

The golden ratio of capital allocation:

Act III: Practical Manual - Double Insurance Withdrawal Line

Plan A: Small-amount Express (≤10,000 U/time)

Binance C2C → Filter "Taiwan Certified Merchants"

Exchange to Taiwan Dollars → Transfer to MAX Exchange (Taiwan compliant platform)

Withdraw NTD to E.Sun Bank personal account

Advantages: Taiwan dollar settlement avoids RMB regulatory red lines, and the arrival time is less than 2 hours

Plan B: Large Amount Worry-Free (50,000-500,000 U)

Binance → Kraken (US-compliant exchange)

Kraken → Huamei Velo Bank (US digital bank)

Huamei Velo → Domestic Bank (Foreign exchange settlement in separate transactions)

Key Nodes:

Complete "US Tax Residency" certification on Kraken (reduces fund scrutiny)

Huamei Velo single withdrawal ≤ $10,000 (compliant with US and Chinese anti-money laundering standards)

Ultimate Tips: 5 Life-Saving Rules for Beginners

Card-abandoning strategy: Get three "withdrawal-only cards"

E.Sun Bank (Taiwan): specializes in accepting Taiwan dollars

Huamei Velo (US): Accepts US dollars

Small local banks (such as city commercial banks): accept RMB (single transaction ≤ 5,000 yuan)

forbidden area for speech: Prohibited words in withdrawal chat

❌"Exchange" "Buy a house" "Overseas investment"

✅"Game Recharge"" Cross-border e-commerce payment""Service fee"Time Magic: Best Time to Withdraw

Weekdays 9:00-11:00 (Bank risk control system has just been launched, and the review process is relaxed)

Avoid the 15th of each month (bank settlement day, risk control upgrade)

Evidence chain management:

Each transaction saves:Exchange transaction screenshots

Merchant chat history (including fund usage description)

Bank deposit SMS (labeled "Service Fee/Payment")

Emergency Plan:

If frozen, take immediate action:Submit a (Virtual Currency Transaction Statement) to the bank (the template can be obtained by private message)

Contact the merchant to issue (proof of source of funds)

Call the central bank complaint hotline at 12363 (emphasizing "unaware of illegal funds").

Epilogue: The qualitative change from frozen card to silky smooth

Now, before making a withdrawal, I will open my own risk assessment form:

✅ Is the merchant 3-factor verified?

✅ Does the number of splits comply with the risk control model?

✅ Does the funding path bypass sensitive areas?

When my one millionth U arrived safely, I finally understood: the true profiteering in the cryptocurrency world isn't about 100x returns, but about using systematic thinking to reduce the "withdrawal risk" to 0.01%. Remember: money earned on an exchange is only truly yours once it's deposited into your bank account.