In the past period of time, amazing DeFi innovation has taken place on Arbitrum. One of the main reasons for this is the deployment of the decentralized derivatives exchange GMX on Arbitrum. Thanks to the Lego properties of DeFi, other DeFi protocols began to build products based on GMX. Among them, the most common design is the product framework based on GLP.

Next, let’s take a closer look at this type of product.

First, what are GLPs?

In the GMX ecosystem, there are two types of tokens, one is the governance and dividend token GMX, and the other is the liquidity token GLP.

GMX is not an order book model. In the GMX market, one party is the liquidity provider and the other party is the trader. Investors can provide liquidity for traders on GMX by purchasing GLP, and accordingly, investors can get 70% of the GMX transaction fee share. Liquidity providers and traders are counterparties, which also means that traders' profits represent losses for GLP holders, and traders' losses represent profits for GLP holders.

GLP is composed of a basket of mainstream assets - 50% stablecoins, 28% ETH, 20% WBTC and some other mainstream assets. Liquidity providers enter or exit the market by minting or destroying GLP.

In the design of most GLP derivatives, their main goal is to reduce investors' risks and increase the returns of GLP holders, thereby increasing the capital efficiency of assets.

Next, let's look at the strategies of these protocols:

1. Delta Neutral Strategy

Providing Delta neutral strategies to investors to acquire users is the mainstream practice of most GLP derivative protocols.

According to Wikipedia, in finance, if an investment portfolio consists of related financial products and its value is not affected by small price changes of the underlying assets, such a portfolio has the property of Delta neutrality. In traditional finance, portfolio strategies that aim to make money in sideways markets are called Delta neutral strategies.

That is, a Delta Neutral trade is intended to establish a position that does not react to small changes in the price of the underlying asset. Therefore, the goal of the GLP Delta Neutral strategy is to provide returns to GLP holders while reducing their price sensitivity.

Let’s take Rage Trade as an example.

Rage Trade provides users with a vault product called "Delta Neutral Vault", which is divided into Risk-On Vault (9% APY) and Risk-Off Vault (5% APY). Users can benefit by depositing USDC, and the vault has reached its limit.

How does the vault work?

The basic work of Vault is to provide liquidity for GMX in a Delta-neutral way to earn ETH income. However, in order to reduce the risk exposure of users, Rage Trade has launched two products to meet the needs of users with different risk preferences. Through the mutual matching of funds in Risk-On Vault and Risk-Off Vault, Rage Trade realizes the realization of income under different risks.

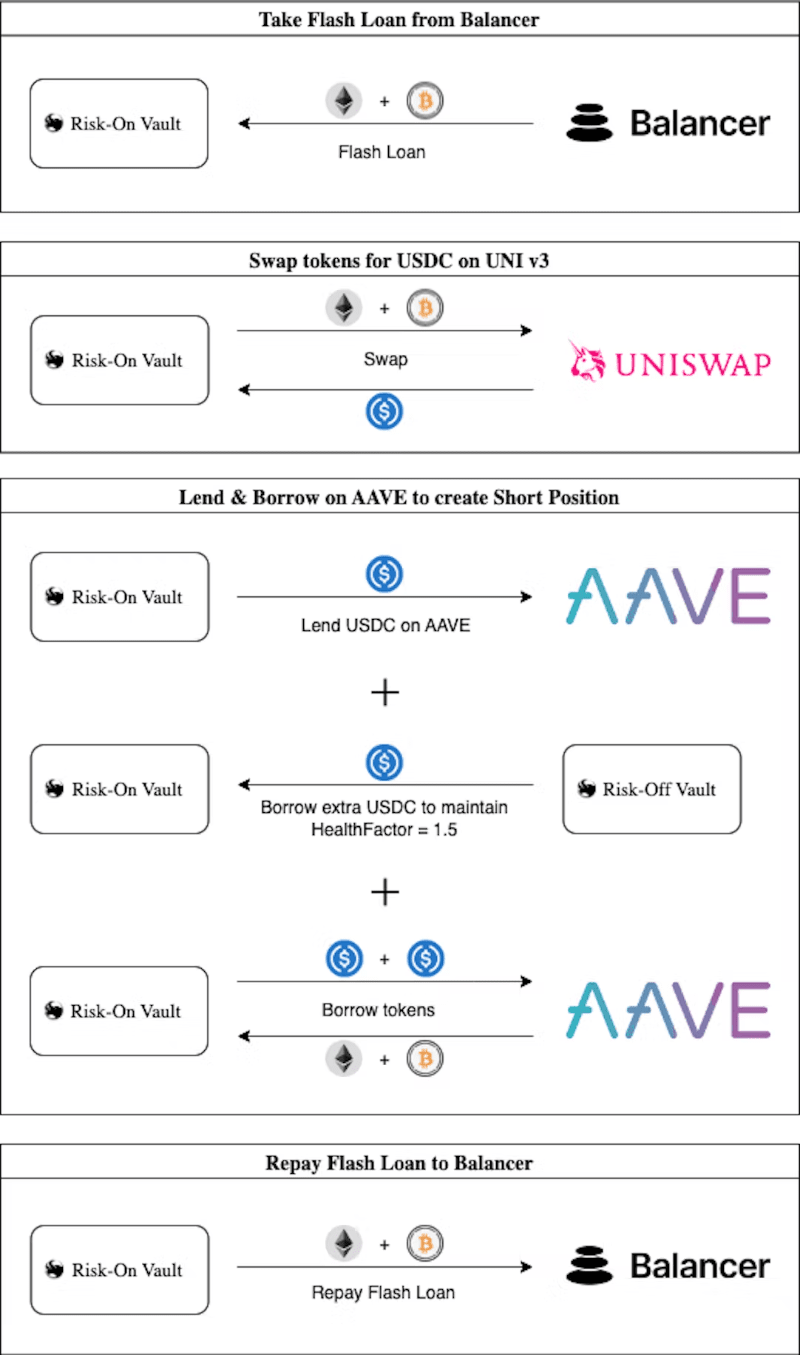

Phase 1: Rage Trade converts part of the user's USDC into GLP and deposits it in GMX to obtain a share of the transaction fee income.

Phase 2: Based on the ETH and BTC positions in GLP, ETH and BTC are flash loaned on Balancer, and ETH and BTC are sold on UniSwap to obtain USDC. Rage Trade then deposits USDC into AAVE and borrows ETH and BTC to repay the loan on Balancer. In order to improve capital efficiency, Rage Trade maintains a 1.5x health factor for its short position on Aave.

Among them, in addition to staking GLP to obtain GMX fee dividends, Risk-On Vault borrowed USDC from Risk-Off Vault to complete the opening of airdrop positions to hedge against price fluctuations of ETH and BTC.

The Risk-Off Vault earns interest by lending USDC on Aave, while also receiving a small portion of ETH rewards from GLP based on the amount of USDC lent to the Risk-On Vault.

Every 12 hours, Risk-On Vault will update its hedge position based on changes in weights and prices and automatically compound GMX’s ETH gains into GLP.

Phase 3: ETH rewards generated from GMX since the last rebalance are distributed between Risk-On and Risk-Off Vaults based on the utilization of the Risk-Off Vault.

The Risk-Off Vault’s ETH reward share will be automatically converted into USDC and pledged on Aave to earn more interest.

Rage Trade's product design pursues a Delta-neutral investment strategy, and provides different profit strategies for users with different risk preferences in the form of Risk-On and Risk-Off.

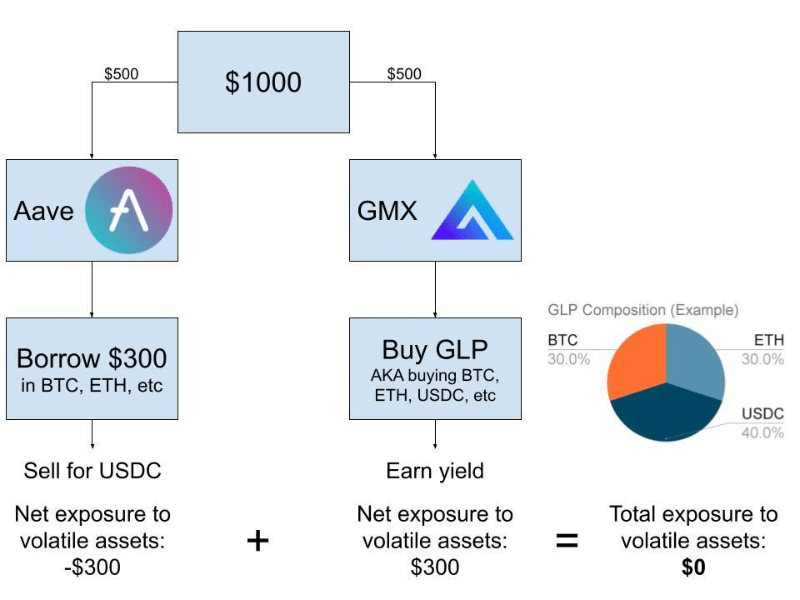

Compared with other Delta neutral vaults, Rage Trade's product design and volatility strategy are more complex. It refines the process of predecessors: for example, DeCommas only uses half of USDC to buy GLP and deposits half into AAVE to earn interest to reduce risk exposure. This design is also the main advantage of Rage Trade.

How the DeCommas Delta Vault Works

2. GLP mortgage lending and minting stablecoins

Since GLP consists of a basket of mainstream assets, 50% of which is USDC, it has low volatility and is very suitable for use as lending collateral.

Let’s take Vesta Finance as an example.

Users can deposit GLP into Vesta Finance, and Vesta will directly pledge GLP in GMX. Therefore, users will receive interest income from lending and GLP dividend income (Vesta takes 20%). Users who deposit GLP can mint stablecoin VST, which can be used for liquidation pledges and liquidity mining. This greatly improves the capital efficiency of GLP holders. At the same time, the protocol expects to accumulate esGMX to increase the income of pledged users.

Currently, Vesta Finance’s TVL (total locked value) is 22 million, and the number of VST minted is 8.75 million.

3. GLP liquidity certificate

Another way to improve capital efficiency is to mint liquidity certificates, just as Lido provides stETH certificates to ETH stakers.

GMD Protocol is a good example.

It adopts a pseudo-Delta neutral strategy and provides investors with a vault product called “Delta-Neutral Vaults”.

Investors can pledge USDC, ETH, and BTC into the single-coin vault of GMD Protocol. GMD Protocol will compound the user's investment. Users will receive gmdUSDC, gmdETH, and gmdBTC as asset certificates, and GMD Protocol will encourage users to obtain additional income through these tokens. When users choose to exit, they can redeem USDC, ETH, BTC, and additional income through their gmdToken.

Does GMX have any competitors?

The answer is yes.

Vela Finance is a perpetual leveraged exchange that has launched its liquidity supply product VLP. Compared with GMX, the only asset class in VLP is USDC. Users only need to pledge USDC to obtain VLP. Since there are no volatile assets, VLP holders will only lose money when traders make profits. The income of VLP holders comes from traders' losses and 60% transaction fees.

Due to its inherent Delta-neutral properties, VLP holders do not need other protocols to provide Delta-neutral strategies. Parts "2" and "3" in the previous article may be the parts for innovation based on VLP.

How does Vela Finance compete with GMX?

It provides higher liquidity injection rewards, using native tokens to reward VLP providers. The activity will start on March 14. Currently, $2.5 million worth of VLP vaults have been filled.

However, compared with GMX, which has already established its leading advantages and moat, Vela Finance, which has just started, still has a big gap. In the short term, especially when the GLP derivatives protocol has matured, VLP cannot pose a threat to GLP. Gains Network, which can really threaten GMX's market share, uses the DAI vault.

Due to the characteristics of DAI vault synthetic assets, Gains Network provides users with more trading pairs (cryptocurrencies, foreign exchange and stocks), higher leverage and complex risk control mechanisms with high capital efficiency. Thanks to this, Gains Network will be able to compete with GMX, which adopts full asset protection - it is now deployed on Arbitrum.

The DAI vault is based on the same principle as GLP, but does not have the high scalability of GLP. However, on December 8 last year, Gains Network announced a new vault strategy: users will receive gTokens after depositing assets into the vault. If we deposit DAI into the vault, we will receive gDAI certificates. The redemption price of gTokens is affected by accumulated fees and open interest PnL measurement data. The principle is similar to VLP, but more complicated than VLP. Later, Gains Network will also set up liquidity lock-up incentives.

Since the gToken model is more complex and delta-neutral, it increases the difficulty of building products based on it, and it is unlikely to form a trend among developers.

at last

GMX and the GLP derivatives protocol are a win-win cooperation. GMX provides investors with LP tokens with low volatility, and the GLP derivatives protocol provides GLP holders with a more capital-efficient and higher hedging yield strategy. The GLP launched by GMX not only feeds the GLP derivatives protocol, but the GLP derivatives protocol will also drive GLP to continue to expand its share and establish a strong liquidity moat for GMX. Challengers in the spot/futures leveraged trading track can only attract liquidity providers through higher incentives like Vela Finance. Perhaps only when innovators appear in this track can there be a chance to truly threaten GMX's leading position in the future.