As the Bitcoin narrative of a new round of bull market becomes the main line, the Ethereum ecosystem, which has been optimistic in the bear market, gradually weakens. Coupled with the strong outbreak of Solana, the crypto industry seems to have ushered in the beginning of 2024 with the "narrative of the rise of new public chains."

Although the price of Ethereum has doubled in the past year, it is still criticized by many people, and some even began to FUD Vitalik, saying that there are major problems in the decision-making level. The main reason for this phenomenon is that everyone has too high expectations for ETH (at least outperforming Bitcoin), and it is also related to the overly impressive performance of SOL. Today we will take stock of what new changes have taken place in the Ethereum ecosystem in the past year.

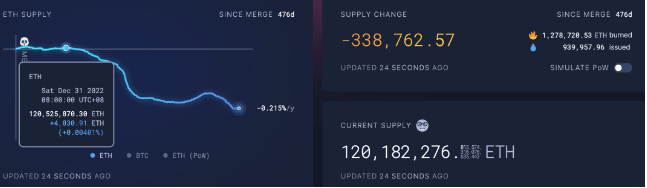

Ethereum has entered a period of complete deflation

Since the beginning of the year, the number of Ethereum has decreased from 120.5 million to the current 120.1 million, with a total of 340,000 destroyed in a year, worth $750 million. With the arrival of the bull market, the destruction volume will inevitably increase significantly.

LSD track burst

Since the merger of Ethereum was completed in September 2022, it has become a hot spot in the first quarter of 2023 after several months of development. As the end of the bear market, the stable annualized return of about 4% has attracted a large amount of funds to join. LSD projects such as Lido, RPL, and SSV have ushered in a wave of explosions. The Ethereum pledge rate has continued to rise. As of January 3, 2023, the pledged amount has reached 28.8 million.

As the amount of pledged funds continues to expand and the Shanghai upgrade approaches, a small number of project parties have begun to target this part of the funds and launched their own DeFi products. Through the layered nesting method, they have improved the utilization rate of pledged funds. After the wealth effect appears, more institutions and funds have begun to pour in and lay out related tracks, thus deriving LSDFi related tracks and gradually improving LSD-related infrastructure.

There are good things, but there are also unsatisfactory things. As the staking rate increases, Lido will occupy more than 1/3 of the Ethereum staking market share. The staking track is too centralized, and the market is beginning to worry whether Lido's growth will threaten the security of Ethereum mainnet consensus. There are various opinions on whether Lido's centralization is harmful.

On December 28, Vitalik mentioned the DVT (distributed validator technology) technology, which solves related problems from the perspective of centralized staking and decentralized verification. On November 28, 2023, Lido DAO has begun to adopt the DVT technology provided by Obol Network and ssv network.

With the arrival of the bull market and the increase in Ethereum’s value, it is almost certain that the Ethereum staking track will become a market with a scale of hundreds of billions. In addition, with the development of the industry, stable financial management will gradually become a rigid need for some people, and the development and innovation of related tracks are worth looking forward to.

In the DeFi track, RWA represented by Maker began to expand outward, but the response was mediocre. The old DeFi represented by Uniswap began to expand inward, making some micro-innovations in technology and launching full-chain expansion plans, hoping to further occupy more market share;

The blockchain game track is completely dead. Although some blockchain games have been launched on other chains and full-chain games have also been promoted to a certain extent, there is no blockbuster that has completely detonated the market;

In the NFT track, although Yuga Labs has made some efforts in games, the response has been mediocre, and its own NFT has not made much progress this year. Azuki raised 20,000 Ethereum at the end of June, but the final product directly copied Red Bean, draining the already limited liquidity of the NFT market, and the Red Bean series also ushered in a wave of declines. Regarding the NFT trading market, OpenSea has directly shrunk from its previous valuation of tens of billions to 1.4 billion, or even less, and institutions have lost more than 90%. Blur is also constantly eroding OpenSea's market share. Ethereum projects have already occupied the market share. It can be said that it is currently in a red ocean with fierce market competition. It is extremely difficult to make some achievements, but Bitcoin is just the opposite. It can directly copy Ethereum and is completely an undeveloped virgin land.

Some of Ethereum’s new innovations this year, including concepts such as account abstraction and AI, are also under construction, but no phenomenal products have emerged, so they are not listed one by one.

On the other hand, due to Ethereum's recent poor performance, many people began to FUD, believing that the reason was that Vitalik had major problems in the decision-making level of Ethereum's development. The decentralization of tax authority would lead to the separatism of Layer2 and the weakening of Ethereum's value capture. Regarding this statement, everyone has different opinions.

Finally, the next things worth looking forward to about Ethereum are: one is the Cancun upgrade, which is good for the second layer; the other is the approval of the Ethereum ETF application after the Bitcoin ETF is approved.