Original author: 0xLaughing

Original source: Rhythm BlockBeats

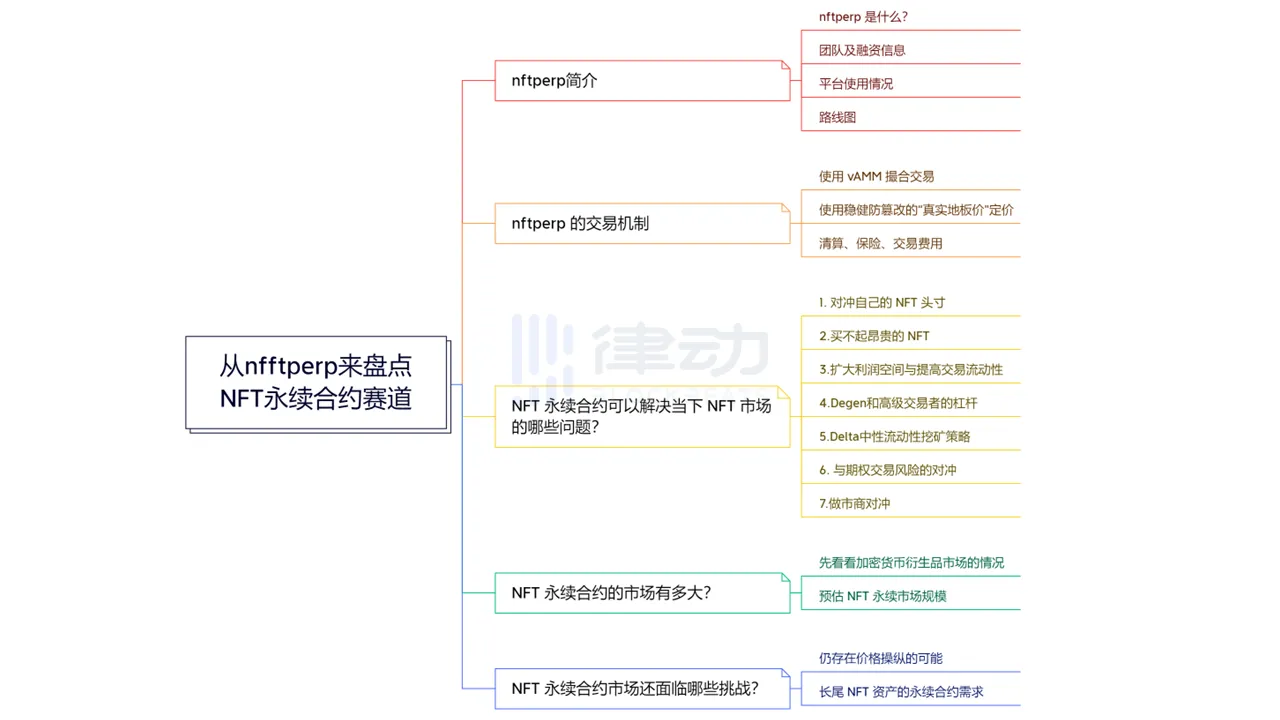

introduction

The NFT market has always been committed to solving the problem of "insufficient liquidity". From the aspects of NFT valuation, pricing, matching methods, etc., many excellent products and innovative mechanisms have continuously emerged to promote the continued development of NFT financialization. A healthy financial market needs to allow market participants to play the role of both long and short parties at any time to achieve the purposes of hedging transaction risks, increasing profit opportunities, and enriching trading strategies. However, NFT traders can currently only make profits by executing the strategy of buying low and selling high on NFT spot. The trading method is very simple. NFT traders have the need to go long/short NFT with leverage. The price of blue-chip NFT is high, and retail investors want to participate in the transaction but have no intention to do so. Powerless. In response to these questions, people are looking forward to the answers to NFT derivatives trading found in traditional financial markets and DeFi markets.

The traditional financial futures market once had an inherent limitation, that is, it had a settlement date and limited leverage trading capabilities, and could not adapt to this 724-hour trading encryption market. As a result, BitMEX launched the perpetual contract on May 13, 2016, using an innovative funding rate to control the spot and contract prices as consistent as possible, unlocking the opportunity to use up to 100 times leverage for long/short positions. Its emergence changed cryptocurrency and the entire financial field forever.

In fact, many NFTFi innovations are inspired by DeFi: for example, the first NFT AMM project sudoswap refers to the centralized liquidity solution of uniswap v3 AMM, and the leading peer-to-peer lending protocol refers to the lending protocol Aave.

With the DeFi market’s perpetual contracts as a reference, nftperp, a perpetual contract platform that can leverage long/short NFTs, is here.

Introduction to nftperp

What is nftperp?

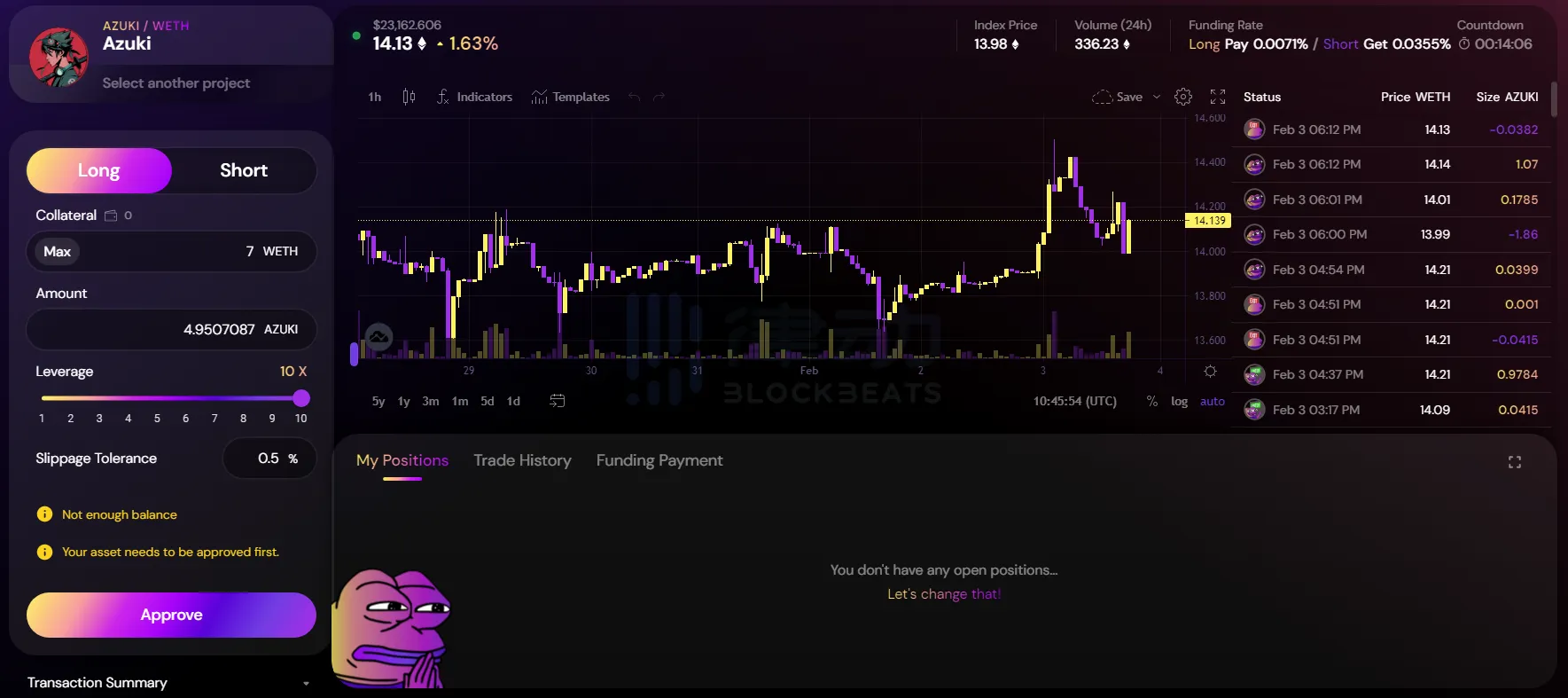

As the name implies, nftperp is a perpetual contract decentralized exchange for NFTs:

• Built on Arbitrum

• Users can use ETH as collateral to trade perpetual contracts on blue-chip NFT projects such as BAYC and CryptoPunk with a leverage of up to 10 times

• The protocol uses the NFT price assessment protocol based on the floor price of blue-chip NFTs. Upshot integrates Chainlink oracles to feed real-time NFT price data on the chain.

• No real liquidity providers are required, and no order books are used, but an improved vAMM (Virtual Automatic Market Maker) mechanism pioneered by Perpetual Protocol to match NFT perpetual contract transactions

Team and financing information

There is currently little information about the team announced, and only the founder of the team is known to be Joseph Liu. In addition, there are multiple investment analysts and researchers McKenna, Nick Chong, Ben Roy and Ben Lakoff as team consultants.

On November 25, the NFT perpetual contract trading platform nftperp announced the completion of a US$1.7 million seed round of financing at a valuation of US$17 million. This round of financing was funded by Dialectic, Maven 11, Flow Ventures, DCV Capital, Gagra Ventures, AscendEX Ventures, and Perridon Ventures. , Caballeros Capital, Cogitent Ventures, Nothing Research, Apollo Capital, Tykhe Block Ventures, OP Crypto and other institutions participated in the investment.

Platform usage

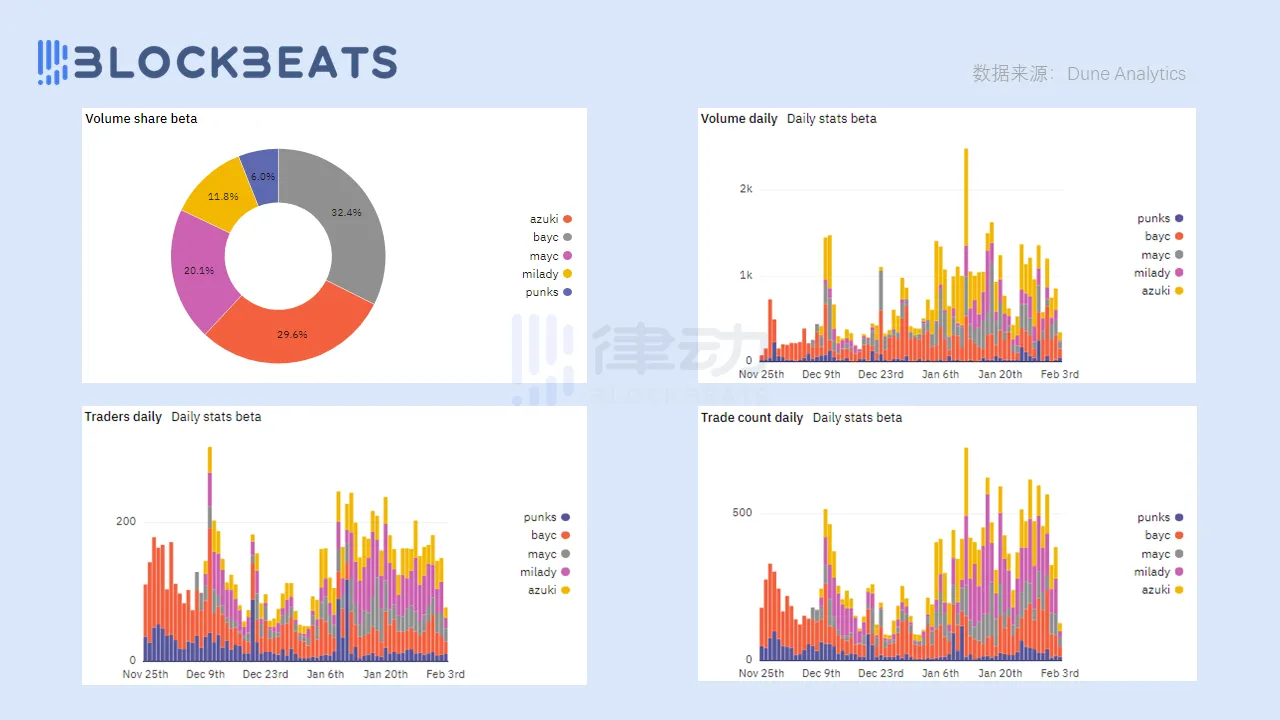

nftperp launched the beta mainnet on November 25, 2022. According to Dune Analytics data, as of the time of publishing the platform:

• Cumulative trading volume exceeds $70 million

• 1,381 users made a total of 21,150 transactions

• Currently, the platform only supports perpetual contract trading for five series: BAYC, Azuki, MAYC, CryptoPunks, and Milady.

• The most traded NFT series is Bored Ape Yacht Club with a 32.4% share, followed by Azuki with a 29.6% share

route map

According to the official roadmap, follow-up plans in 2023 include:

• V1 public mainnet launched

• Mafia Nuts collection sale

• L2 solution re-evaluation

• nftperp token distribution

• NFT index derivatives

• Permissionless marketplace

• Structured product launches and more

nftperp’s transaction mechanism

Using vAMM to match transactions

Original static vAMM

In 2018, the decentralized sustainable trading platform Perpetual Protocol launched the vAMM (Virtual Automated Market Makers) mechanism.

Like ordinary AMM, vAMM also uses x * y = k for automatic price discovery. The difference is that vAMM does not require a real liquidity provider. Users will cast virtual assets after depositing real assets as collateral into the smart contract vault. , and then trade and quote in the liquidity pool according to x * y = k, which also provides the functions of short selling and leverage trading, and avoids impermanent losses.

vAMM serves as an independent settlement market, and all profits and losses are settled directly in the guaranteed vault. That is, a trader's profit in vAMM is the loss of other traders.

How vAMM settles profits and losses independently

However, the original static vAMM will have problems in the unilateral market: if the spot price surges during the bull market, a large number of long positions need to be established to keep the contract price consistent with the spot price, so the funding rate is likely to need to be paid to the long holders. Yes, short sellers have no incentive to pay these funding rates, that is, the funding rate has caused an imbalance of long-short interests, and the price will deviate far from the joint curve. At this time, the protocol will face systemic risks.

To solve this problem, Perpetual Protocol v2 integrates the vAMM mechanism with the centralized liquidity of Uniswap v3, while providing PERP liquidity incentives and online limit order functions. Solana's perpetual contract protocol Drift developed Dynamic vAMM based on it through "re-pegging" and "adjustment of liquidity".

nftperp introduces dynamic vAMM

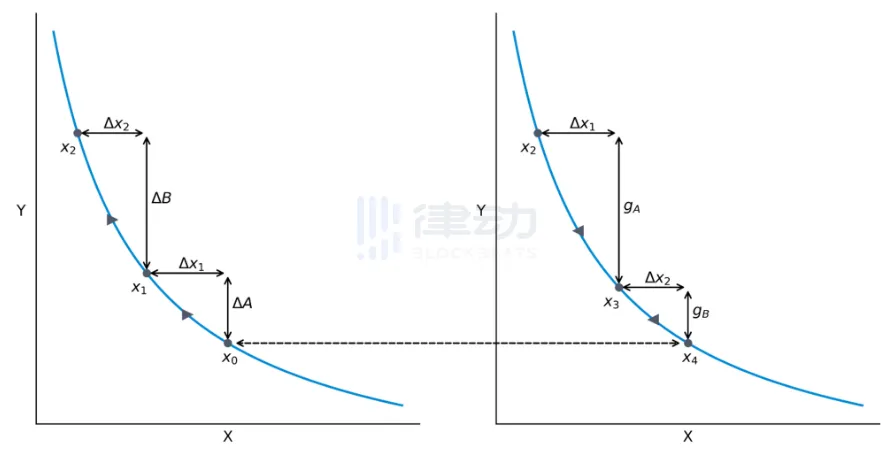

nftperp draws on Drift's dynamic vAMM and uses DVL (Dynamic Virtual Liquidity), so that the virtual assets x and y in the x * y = k equation can be dynamically adjusted according to the following two situations (reference nftperp documentation):

• Convergence event: When the price of the perpetual contract deviates from the oracle price by more than 5% for more than 8 hours, a convergence event is deemed to have occurred. The system will use the following formula to adjust the y value to match the oracle price. Once a convergence event is triggered, virtual liquidity resets to the center of the bonding curve.

In addition, nftperp currently offers convergence rewards indefinitely, using $vNFTP to incentivize users to narrow the price deviation when vAMM prices deviate from the index price by more than 2.5%. Convergence rewards are distributed based on the nominal value of convergence transactions (positions opened for more than 30 minutes).

• Dynamic expansion/contraction of liquidity factor k: Since the protocol cannot predict long/short positions on the platform, dynamic k is crucial. k represents the depth of virtual liquidity. The larger k is, the smaller the slippage is when the trade is executed. As long as the process of k expansion/contraction does not affect the ratio between x and y, the protocol can withstand any market conditions (high vs. low open interest).

Through the above model, nftperp ensures that the price always trades in the part of the curve with the deepest vAMM liquidity, and the available virtual liquidity corresponds to the trading demand, allowing traders to obtain the best slippage and available liquidity.

In addition, in order to ensure that nftperp vAMM maintains high availability in abnormal market conditions, the following two optimizations have been made:

• Dynamic funding rates: Standard funding rates take into account position size, contract mark price, and oracle price, while nftperp takes into account the overall ratio between longs and shorts to better balance open interest. In addition, the funding rate is updated hourly to ensure that the contract price does not deviate too far from the NFT trading market floor price.

• Volatility Limits: A ±2% change limit is set for the contract price per block to protect the protocol from manipulation by flash loan attacks and insurance fund drain during periods of high volatility. Drift v1 experienced this situation, where large fluctuations in LUNA prices resulted in an imbalance of unrealized losses and gains within the system, and excess gains could be withdrawn from the insurance fund without restrictions.

Use robust, tamper-proof "real floor price" pricing

According to the nftperp official documentation, due to the non-fungible nature of NFT, NFT pricing/valuation is very difficult. In current NFT-related protocols, most use floor prices as pricing/valuation indicators.

However, directly using the floor price of NFT as the price feed data for the oracle will cause some problems:

• Price manipulation

• A single NFT pending order (becomes the floor price) does not represent the broad consensus of the NFT series

• Minimum selling price only represents the seller and not the fair price (the price that both bid and ask agree on)

Among them, price manipulation is the most obvious problem, and even blue-chip NFTs such as BAYC with high unit prices are not immune to this problem. For example, in November last year, Franklin, the seventh largest holder of BAYC, "manipulated" the floor price to trigger BendDAO to trigger auction liquidation to realize his "smash arbitrage" strategy.

Upshot x Chainlink

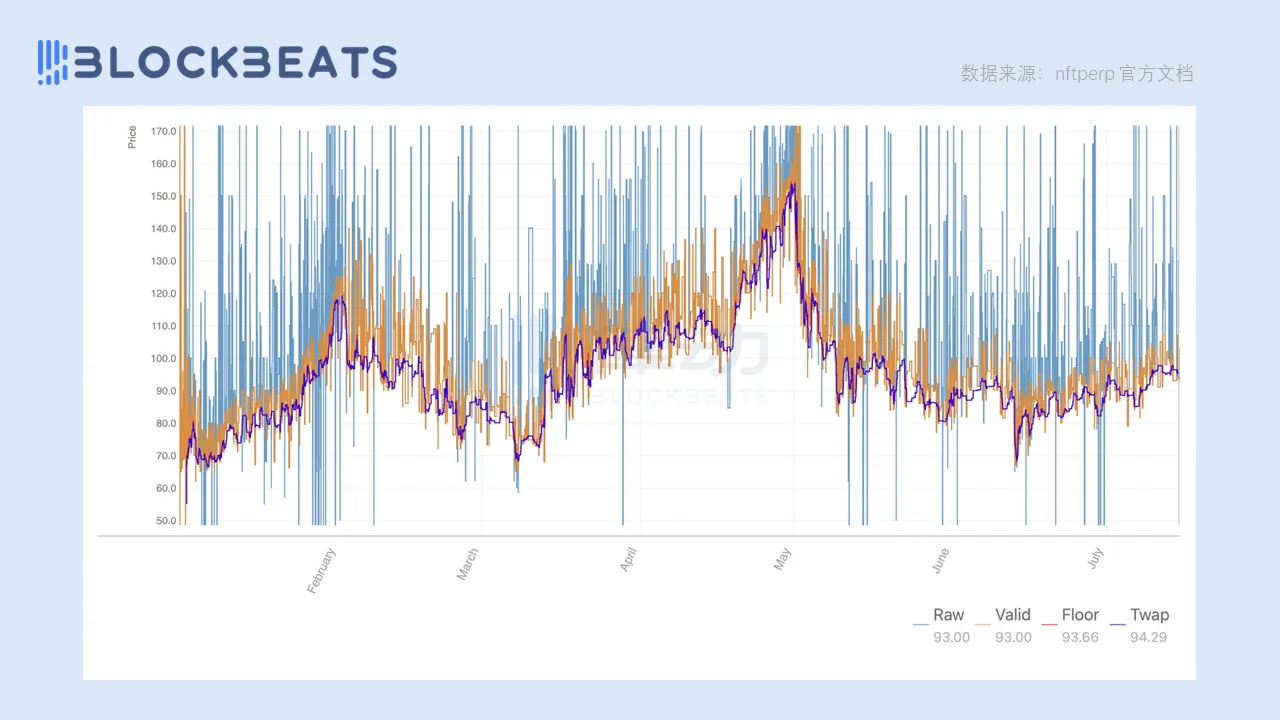

Referring to the DropsDAO NFT oracle model, nftperp uses the NFT price evaluation protocol Upshot to integrate Chainlink oracle data, and finally calculates a robust and tamper-proof "True Floor Price" and feeds it to the platform for use.

Calculation method

1. Collection and analysis: Collect and analyze on-chain/off-chain NFT transaction events in the top NFT market

2. Detect data qualification: Determine whether the data is qualified based on transaction event type, Token ID and clean transaction detection

3. Filter outliers: use statistical methods and volatility scores to filter extreme outliers and possible outliers

4. Calculation: Use the time-weighted average price algorithm to calculate the filtered data to obtain the "real floor price"

The data involved in the calculation of "real floor price" is transaction data extracted from the APIs of Opensea, LooksRare and X2Y2 through the oracle operated by nftperp. The calculated price is updated every time a qualifying public trade occurs, ensuring prices are up to date while protecting users from price manipulation. This process has been back-tested on a real blue-chip NFT transaction data set to demonstrate its effectiveness, as shown in the figure below.

Clearing, insurance, transaction fees

When traders open a leveraged position, they use collateral to borrow funds from the protocol, buy and sell assets. When the market moves against them and the value of the trader's position approaches a certain threshold relative to the value of the original collateral, the protocol will liquidate the position to maintain solvency.

When the trader's position value moves against them, their losses are transferred to their margin, the initial collateral. The protocol is now at risk, with sudden price movements potentially leaving traders with positions worth less than their initial collateral. When the value of a trader’s position gets too close to the value of the original collateral, the protocol will liquidate the position to maintain its solvency.

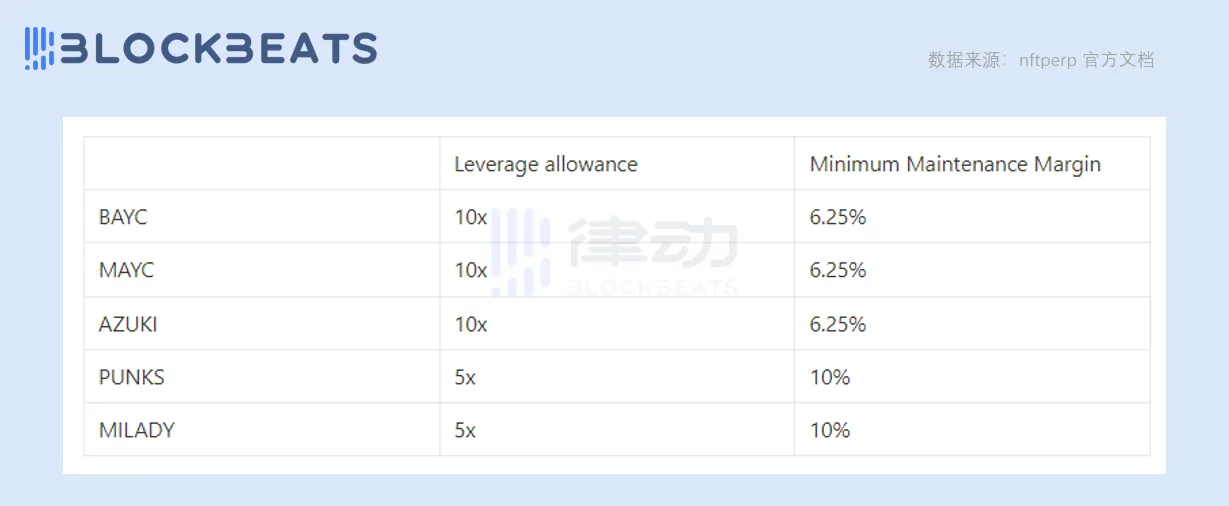

Each NFT collection has different maximum leverage and minimum margin requirements.

nftperp uses a traditional liquidation mechanism for Keeper bots, earning 1.25% of the notional position size on liquidation, with the remainder going into the protocol’s insurance fund.

The insurance fund is used to ensure the solvency of the protocol against bad debts, and the funds in the fund pool are composed of clearing and transaction fee income (the protocol’s 0.15% transaction fee). The size of the insurance fund will grow with the adoption of the protocol, allowing more open positions to be paid out in the future.

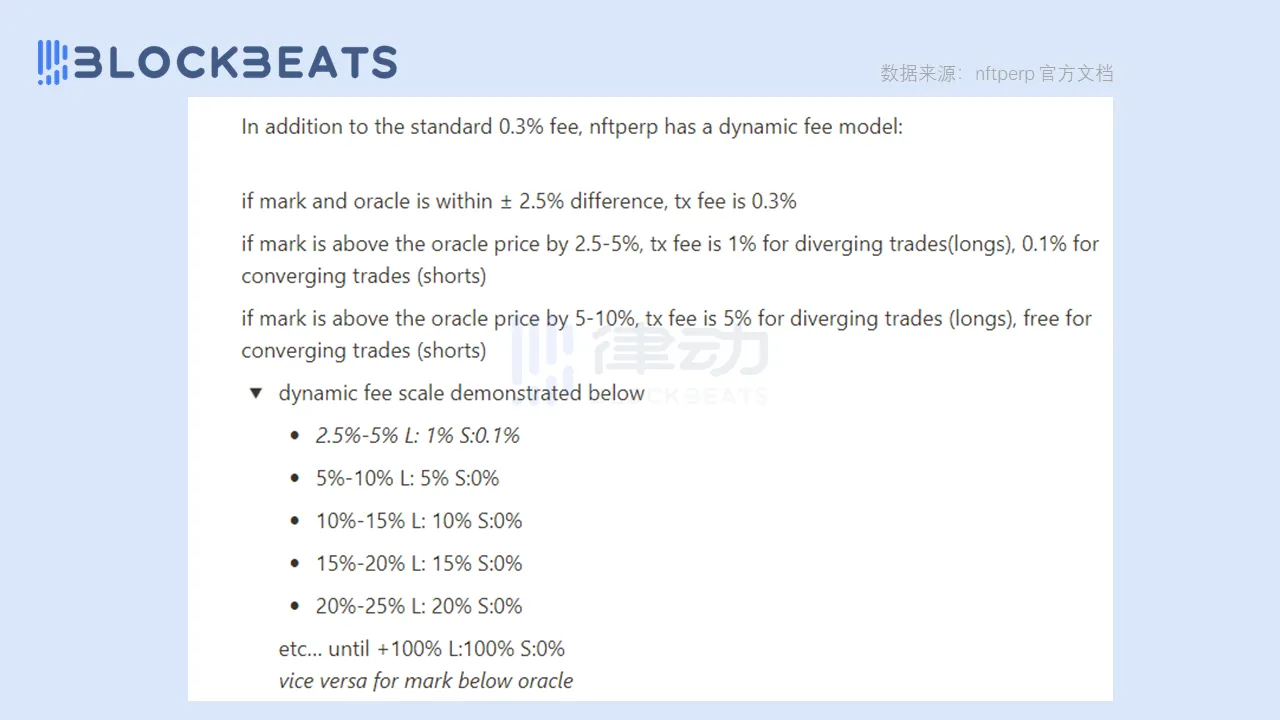

Dynamic adjustment of protocol transaction fees

The protocol’s base trading fee is set at 0.3%, but this number also dynamically adjusts as the mark price deviates to incentivize a balance between shorts and longs. The fee adjustment mechanism is shown in the figure above. The official document also mentions that token stakers will receive a portion of transaction fees, but no information has been released yet.

What problems can NFT perpetual contracts solve in the current NFT market?

Drawbacks of the current NFT market:

• Unable to hedge risks

• Expensive blue-chip NFTs are out of reach for most people

• There is no simple, capital-efficient way to trade with leverage

• Secondary market fees and royalties reduce traders’ profits

To address these problems, nftperp provides solutions for seven specific scenarios.

1. Hedge your NFT position

Holding an NFT means holding a spot, and after the price of an NFT rises many traders/collectors want to hedge against a potential fall while continuing to hold. In this case, one can choose to open a short position with an exposure equal to the price of the NFT being hedged. This hedging strategy helps protect returns while retaining ownership of the NFT, so holders still receive all associated benefits such as whitelisting opportunities, airdrop opportunities, and community access.

2. Can’t afford expensive NFTs

Blue-chip NFTs are notoriously expensive, and nftperp lowers the barrier to entry, making it possible to create positions on Punks, BAYC, MAYC, Squiggles, Azuki, and Moonbirds with as little as $1 in collateral.

Not only will this flexibility cater to existing NFT traders, but it will also make getting started with NFT trading more user-friendly, which is huge for the future of mass adoption of NFTs.

3. Expand profit margins and improve trading liquidity

For example, when a trader's BAYC purchase goes from 70 ETH to 75 ETH and there is a floating profit of 5 ETH, he decides to take profits. However, after deducting OpenSea’s 2.5% handling fee + BAYC’s 2.5% royalty + Gas Fee, the profit is less than 2 ETH. nftperp believes that the layers of overweighting by platforms and project parties have not only reduced traders’ profits, but also reduced the liquidity of the NFT market.

Nftperp offers a better option for optimizing trading profits, with the base fee for opening/closing positions set at 0.3%. The fee does adjust based on open interest in order to incentivize a balance between shorts and longs, but it would take extreme circumstances to reach a fee close to OpenSea levels. Additionally, the protocol is based on Arbitrum, which has a much lower gas fee than Ethereum.

In addition to lower fees, perpetual contracts are more liquid than NFT spot. Because there is no need to find a specific buyer for the NFT being sold, positions on nftperp can be closed at any time. Liquidity is king in financial markets, especially for institutional trading, but the benefits apply to all traders equally.

4. Leverage for Degen and Advanced Traders

Leverage is a powerful tool and nftperp offers up to 10x long and short leverage, but this amplifies all gains and losses. Therefore, typically the use of leverage requires expertise in NFT market dynamics and a catalyst for the specific set of NFTs being traded. For traders with a higher risk tolerance or a strong belief in a trade, leverage can provide greater capital efficiency.

5. Delta Neutral Liquidity Mining Strategy

NFT collateralized lending protocols like BendDAO and Jpeg’d allow users to deposit their NFTs into a vault to lend out funds. Users can bring these loaned funds into the broader DeFi ecosystem to earn income, and after making profits, repay the loan to get back the deposited NFT. The main risk for borrowers is that their NFTs will be liquidated if their value declines and reduces their collateralization ratio below a certain threshold. In this case, short hedging can be a useful tool. In the event that the deposited NFT loses value, shorts will profit, providing depositors with additional capital to repay sufficient loans and avoid liquidation.

6. Hedging against options trading risks

Options can serve as another form of NFT financial derivative. Another common downside protection strategy for holders is to purchase a put option, giving them the right to sell the NFT at a predetermined price within a set time period. The seller of a put option trade takes on this downside risk in exchange for a gain in the form of a premium paid by the buyer. To hedge this risk using nftperp, put option sellers would short on the same NFT collection to protect them if the option is exercised. vice versa.

You can refer to the recent cooperation between nftperp and NFT option protocol Hook Protocol regarding Delta neutrality.

7. Market Maker Hedging

NFT market makers and users of NFT AMMs can also benefit from hedging. With platforms like Sudoswap bringing liquidity pool-based trading to the NFT market, liquidity providers can now deposit their NFTs/FTs into these pools and specify their bid/ask prices for buying/selling NFTs. Traders can then buy and sell NFTs in the pool, with prices determined by the pool’s bonding curve.

When LPs can be hedged via nftperp, bid-ask spreads should tighten as bidders can reduce downside risk by shorting in the event of a price decline. This will improve liquidity within the pool and potentially increase traders’ capital utilization.

How big is the market for NFT perpetual contracts?

A first look at the cryptocurrency derivatives market

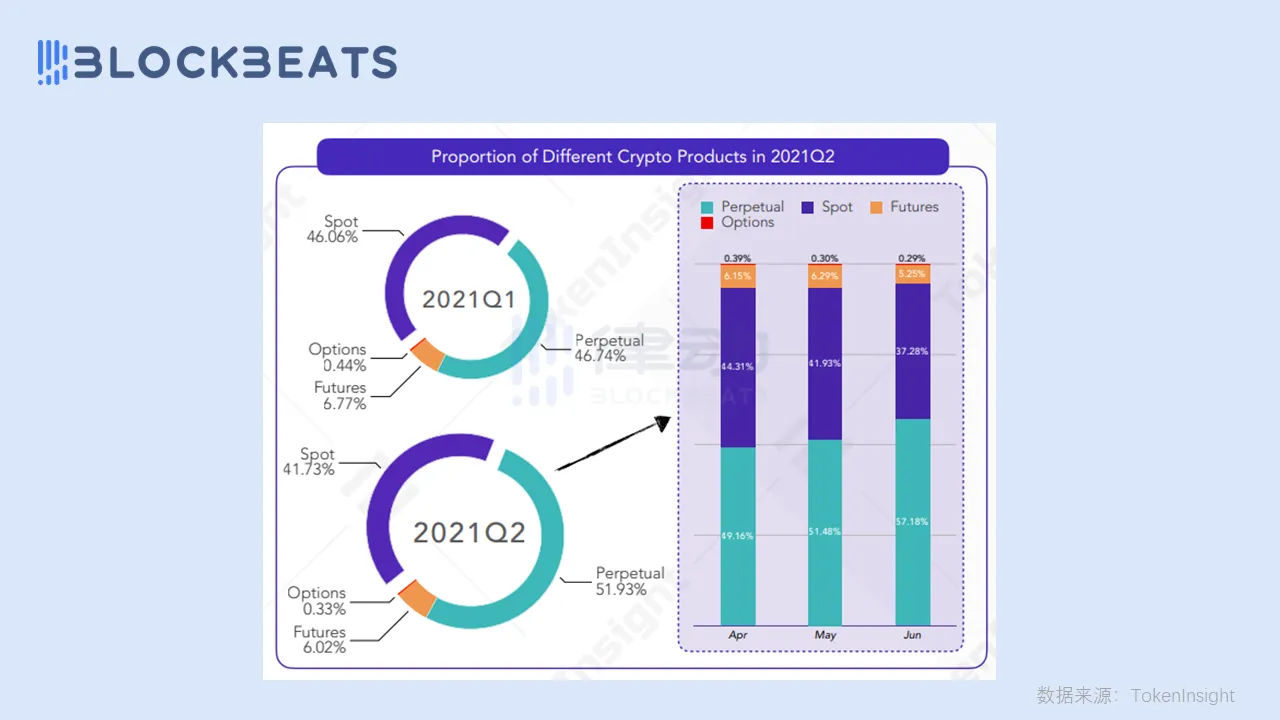

Consistent with traditional financial markets, the market size of derivatives trading in the crypto market is larger than that of spot trading. According to TokenInsight, the trading volume of perpetual contracts in Q2 of 21 was US$19 trillion, equivalent to a daily trading volume of more than US$200 billion, which has surpassed spot prices. If the total market capitalization of cryptocurrencies reaches $10 trillion within 5 years, the accompanying derivatives trading volume may reach $70-100 trillion.

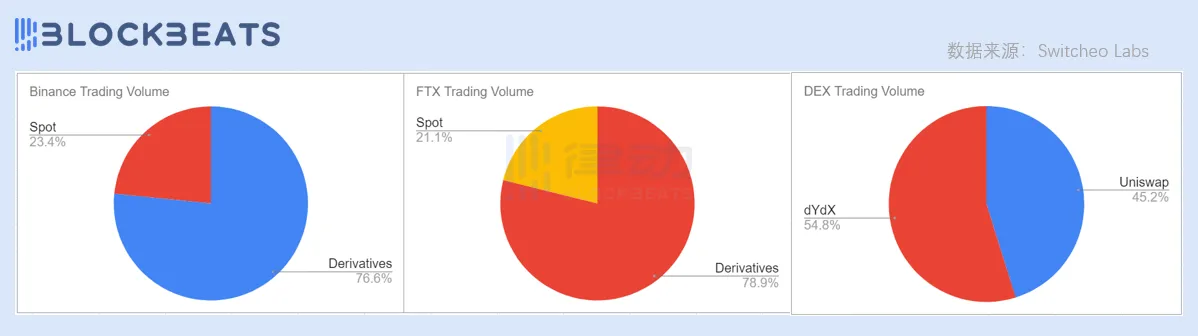

According to data from Switcheo Labs, cryptocurrency derivatives trading on centralized exchanges accounts for an average of 69% of total cryptocurrency trading volume. For example, 76.6% of Binance’s daily trading volume comes from derivatives ($49.52 billion out of $64.65 billion), while FTX generates 78.9% of daily derivatives trading volume ($6.22 billion out of $7.88 billion).

In terms of decentralized exchanges, let’s compare the trading volumes of Uniswap and dYdX, as they are the largest spot and derivatives markets in the space. Uniswap’s daily trading volume is $1.09 billion, while dYdX’s derivatives average daily trading volume is $1.33 billion. This amounts to 45.2% and 54.8% respectively.

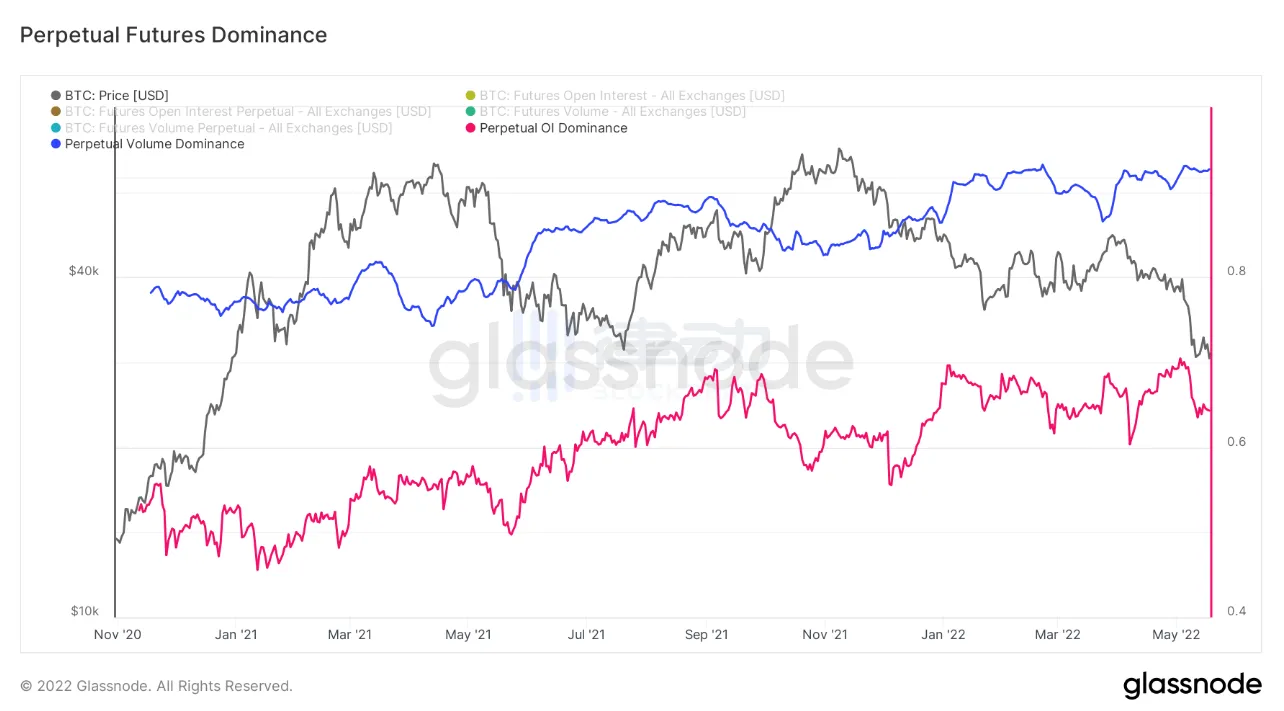

Bloomberg has previously reported that the trading volume of BTC perpetual contracts accounts for 93% of the total futures trading volume.

It can be seen that whether it is a traditional financial market, a centralized exchange in the crypto market or a decentralized exchange, the scale of the derivatives trading market is larger than that of spot trading. As the first and unique derivatives market in the crypto market, perpetual contracts have huge trading flexibility compared to other financial products and are favored by the market.

Estimated NFT sustainable market size

According to DappRadar data, the NFT platform with the largest trading volume in the past month was Blur, with a total trading volume of $442 million and an average daily trading volume of $14.73 million. By comparing the leading NFT spot trading platforms, we can estimate nftperp's market share when it is gradually adopted by more traders.

According to Dune Analytics data, nftperp’s cumulative total trading volume since November 25 is US$71 million, with an average daily trading volume of US$1.01 million. By analogy with the ratio of spot trading to derivatives trading on decentralized trading platforms, it is conservatively estimated that nftperp’s average daily trading volume can reach the same level as the largest NFT spot trading platform. nftperp charges a 0.3% trading fee on all positions on the platform, with a portion of the proceeds going to stakers of its platform token $NFTP.

NFT market trading volume over the past year

In addition, according to NFTGO data, the total trading volume of the NFT market in the past year was US$17.06 billion, with an average daily trading volume of US$46.74 million. Similarly, similar to the cryptocurrency market, the NFT derivatives market has huge potential.

What other challenges does the NFT perpetual contract market face?

There is still the possibility of price manipulation

There is the possibility of price manipulation in any financial market. Due to the small size of the NFT market, spot prices are relatively easy to be manipulated. When spot price manipulation occurs, violent price fluctuations may lead to a large number of liquidation events in the derivatives market. The agreement's insurance fund may not be enough to repay bad debts, and the agreement will face systemic risks.

It is foreseeable that the market share of NFT derivatives will gradually increase. When the profit opportunities from the derivatives market are greater than the cost of manipulating the spot market, price manipulation events will definitely occur. Therefore, how to avoid or minimize the probability of such an event needs to be considered in advance.

The robustness of vAMM and the “real floor price” mechanism, and whether it can cooperate with funding interest rates to maintain normal operation of the system, have yet to be tested by the market.

Perpetual contract demand for long-tail NFT assets still needs to be met

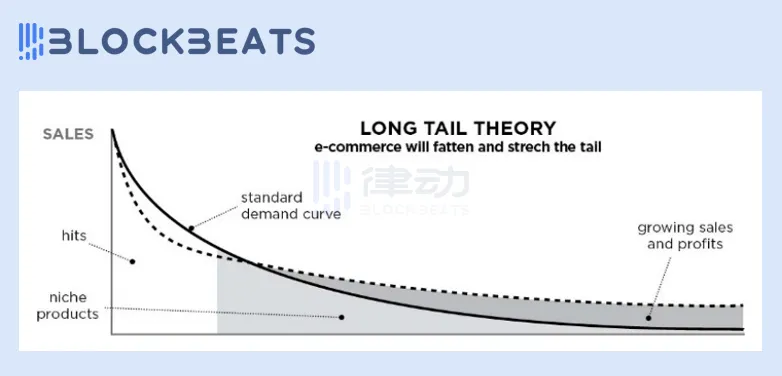

In 2004, Chris Anderson, editor-in-chief of Wired magazine in the United States, proposed the famous "The long tail" theory, believing that the Internet will empower niche markets with a long tail, and the benefits of the long tail will The base market size will even exceed the short-term economies of scale.

The NFT market also has its own "long tail" version, which refers to those NFT projects with small market value, low transaction volume, and low visibility. There are currently tens of thousands of NFT projects in the NFT market, but only a few can enter the top 50 , becoming the so-called "blue chip" and "quasi-blue chip", while other projects constitute the "long tail". The same goes for the cryptocurrency market.

Therefore, platforms/services targeting the long-tail niche market of NFTs and cryptocurrencies may have greater value in the future.

Referring to the decentralized trading platform, Uniswap, a DEX that trades spot goods, provides liquidity for many long-tail assets through permission-free listing. However, few decentralized perpetual contracts can achieve the permission-free listing function (CoinFLEX, Mycelium platforms have been implemented), the reason is that perpetual contract transactions are more complex than spot transactions, and have higher requirements for matching transaction mechanisms, on-chain response speed, on-chain liquidation, etc. At the same time, the threshold for creating a perpetual contract pool is high. For example, if you want to deploy a Token perpetual contract pool in the decentralized perpetual contract protocol TracerDAO (now Mycelium), you need to configure many parameters: leverage function, update interval, coinage/ Burn fees, etc.

For the NFT market, the demand for perpetual contracts for long-tail NFT assets is still there, but products that can realize functions such as lending and derivatives trading for non-blue-chip NFT projects have not yet appeared. This is due to multiple reasons.

Take nftperp as an example. Its "real floor price" has very high requirements for data quality and calculation methods. There is a large amount of unreliable data in the NFT market (such as wash transactions), which means that it is currently only applicable to blue-chip NFTs with high liquidity. series. Taking BendDAO as an example, even the top blue-chip BAYC will have its floor price manipulated by large investors for "liquidation arbitrage", let alone long-tail NFT assets with smaller market value?

In the final analysis, upstream problems such as poor liquidity of NFT and difficulty in valuation and pricing of NFT have not been well solved, which restricts the development of downstream NFTFi products and fails to unleash the potential of NFT long-tail assets.

Conclusion

Focusing on DeFi, NFT, and even the entire crypto space, constant financial innovation is pushing the market to higher levels. The improvement of composability between products in different segments will further stimulate market innovation. NFT-specific derivatives will provide the market with more trading strategies, and the nascent NFT market will gain more depth, just like options and futures. Contracts play an important role in mature financial markets.

As the NFT infrastructure becomes more and more complete, I believe that the upper-level NFT financialization process will continue to accelerate. NFT will be more than a small picture. It will become an important part of the encryption field and even the financial world together with NFTFi.

(The above content is excerpted and reprinted with the authorization of partner MarsBit, original text link | Source: Rhythm BlockBeats)

Statement: The article only represents the author's personal views and opinions, and does not represent the objective views and positions of the blockchain. All contents and opinions are for reference only and do not constitute investment advice. Investors should make their own decisions and transactions, and the author and Blockchain Client will not be held responsible for any direct or indirect losses caused by investors' transactions.

This article Can you increase leverage to short NFT? Taking stock of the NFT perpetual contract track from nftperp first appeared on Blockchain.