Original author: HOPYDOC

Original translation: MarsBit, MK

Evaluating app chains has been one of the trickier tasks facing investment analysts because app chains function like standalone applications at a basic level but inherit the characteristics of the protocol or what is now called the base layer, such as security and data availability.

Therefore, it is unfair to apply the transaction multiples of independent applications to application chains; but at the same time, it is difficult to argue that application chains should trade at multiples of the base layer due to the obvious difference in the value accumulation mechanism. Take Injective’s rally this year as an example, which is widely regarded as a re-rating transaction. When the team announced the ecosystem fund backed by Pantera Capital and Jump Crypto, etc. to support the construction of other applications on top of the application-specific layer, the market began to regard application chains as protocols.

Injective announces $150 million ecosystem fund

This sparked my interest in the first generation of the "Fat Protocol Thesis" because I thought that by understanding the evolution of how the market views the value of blockchain, it would give me some ideas on how to consider the value of current application chains; or specifically, application chains with ecosystems.

Fat Protocol Thesis

The “Fat Protocol Theory” was originally proposed by Joel Monegro while at Union Square Ventures in August 2016; the argument revolves around the fact that crypto protocols should theoretically capture more value than the applications built on them.

In short, the argument suggests that what we now call base layer protocols either provide two unique core value propositions or sources of value accrual and should therefore always be considered more valuable than applications; or simply put, justify some very astronomical valuations; they come from

A permissionless shared data layer; blockchain effectively lowers the barrier to entry for more new players, leading to more intense competitive dynamics in the system, and more importantly, makes composability between each other possible, thereby driving the growth of the protocol.

A positive feedback loop that drives the speculative value of the native network token; as rising token prices attract the attention of developers and investors, which then converts into human or capital invested in the ecosystem and starts the flywheel of its speculative value.

As an extension, protocols can capture the value created by the application layer through increased demand for native tokens, usually in the form of transaction fees; so in theory, the more transactions an application brings to the protocol layer, the more value the protocol can capture.

Why the “Fat Protocol” is no longer relevant

The “Fat Protocol Theory” subsequently went through much debate about its timeliness, as the claim was made in the maximalist era, when the concepts of modularity and application-specific chains did not even exist.

The market then believed that the “Fat Protocol Theory” was not fully applicable to the current market structure for the following reasons:

The overwhelming abundance of block space; judging by the number of newly minted Layer 1 candidates in the previous cycle, the protocol layer can no longer retain the value created by applications because the abundance of block space compresses the price users pay for the same amount of transactions.

The rise of modular blockchains; effectively breaking down the functionality of blockchain into execution, data availability, and settlement, resulting in cheaper data availability solutions that further compress the fees users pay for the shared data layer in the original paper.

Multi-chain convenience; applications can easily be launched on multiple chains and even interact across chains with the help of interoperability tools like LayerZero, so the dependence on a single protocol has been significantly reduced, weakening the original Positive feedback loops in essays.

App Chain Thesis

The demise of the “Fat Protocol Theory” came with the introduction of the “App Chain Thesis”. App Chains are blockchains built for specific use cases; their design enjoys several advantages, including the following:

Better value accumulation mechanism; native network tokens can be used for security purposes, resulting in a decrease in the supply of tokens; and value can also be captured from the blockchain’s business model.

Customizability; developers are free to customize any configuration in the technology stack to achieve specific goals, such as throughput and finality, and make trade-offs based on the needs of the application.

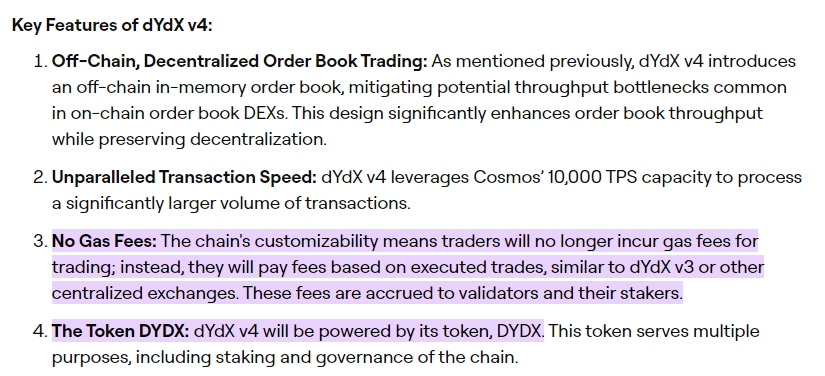

For example, the latest dYdX v4 is implemented on a chain powered by Cosmos-SDK; this ensures that traders no longer need to pay gas fees for transactions; instead, fees are charged based on the size of the transaction, which mimics the experience of trading on a centralized exchange.

That said, there are some inherent drawbacks to application chains, so the concept has not yet fully caught on for the following reasons:

Liquidity fragmentation and composability; native assets can only exist in specific application chains, and unless specific assets are very popular and supported by interoperability products, they cannot interact with assets in other chains.

Limited security; in theory, the security of the application chain is only guaranteed by a portion of the fully diluted valuation, depending on the consensus mechanism; however, the reduction in the value of the token will linearly affect the security level of the blockchain.

The protocol’s business model

If we think about the business model of the protocol or base layer; users are actually paying gas fees for the protocol to properly store transaction data and settle their transactions through the consensus mechanism.

While the original paper may not have been very timely, the beauty of the “fat protocol” era is that there is a clear division of labor between protocols and applications;

Protocols are actually looking for ways to get users to pay for security and data availability; and are committed to retaining users and applications in their respective ecosystems to maximize composability and direct value accumulation (in the form of gas fees)

Even with the rise of second layers, protocols are really just shifting from being customer-centric to being business-centric; the goal is to extract as much value as possible, with rollups paying for data availability and consensus

On the other hand, applications are competing for anything that can bring competitive advantage to their business; and this sometimes leads to a lack of value accumulation, such as how Uniswap maximizes the depth of liquidity without clear channels for capital flow.

This division of labor has given rise to many billion-dollar applications, such as Uniswap and OpenSea. For applications, they essentially outsource other important parts of the blockchain to the protocol level so that they can focus on the things that make the application function and succeed.

However, for the protocols themselves, the current business model is gradually and inevitably breaking down with the emergence of modular blockchains and the enrichment of blockspace; therefore, the protocols are becoming “thinner”.

Business model of application chain

The business models of application-specific chains are very different; although on the surface, both protocols and application chains operate as a base layer

Rather than requiring users to pay for storage of transaction data in the form of gas fees, appchains actually pay for the application itself; for example, Osmosis implements a protocol receiver fee that ultimately flows to token holders in the form of revenue.

However, the application chain also provides everything that a protocol should do; from providing a shared data layer to settling transactions and providing the security level of a proper blockchain; most importantly, the applications are competitive enough to each other.

The advantages of this business model design are a mixture of the following aspects, which should be considered more sustainable and defensible even as market structures evolve and expand in the future

Users are effectively paying for a service that the market agrees on a price for; for example, Injective takes a cut of the trading fees on its perpetual futures exchange, and the market generally believes that perpetual futures exchanges should charge fees; and there are also some exchanges that charge higher fees, such as GMX and Gains Network

Contrary to the market’s general belief that providing shared data and consensus should not be charged; and there is a concerted competition to provide cheaper solutions, effectively making it a zero-cost race

Value accumulation is not linearly related to the number of transactions, but rather to other variables that drive the success of the application; for example, Injective’s value accumulation is a function of perpetual futures trading volume, while Osmosis’s value accumulation is a function of spot trading volume

In short, the business model of Lisk fits well with the current market structure in hindsight; because the protocol is accumulating value from a more sustainable source. Expanding on this, it makes me wonder what would happen if Lisk took it a step further and amplified the benefits at the protocol level.

Fat Application Chain Discussion

The changing times and market dynamics have given rise to what I call the “Fat Application Chain” discourse; we have witnessed application chains such as Injective and Osmosis working hard to build their own ecosystems in order to achieve a win-win situation.

The application chain no longer competes with other base layers or protocols with lower gas fees; instead, it has found a more defensible and sustainable business model, which is recognized by the market; it effectively solves the value accumulation problem in the first-generation "Fat Protocol Theory".

On the other hand, when more applications decide to be built on the application chain, the application chain can also enjoy a positive feedback loop; thereby effectively solving the liquidity fragmentation and limited combinability problems arising from the application chain architecture.

At the same time, application chains provide a shared data layer that enables other applications to be deployed on the application chain itself; promoting the prosperity of the ecosystem, subsequently attracting the interest of developers and investors, and potentially driving the price performance of the network.

Most importantly, it solves the cold start problem that many other layer 1s or rollups may face; since many application chains initially started as applications seeking better composability.

So rather than becoming “thin,” application chains attempting to build an ecosystem show a clear path to becoming “Fat” and staying “Fat”; if justified, it could present an attractive investment case.

Post-mortem of Injective

As mentioned in the previous part of the article, Injective's outstanding performance this year proves the "Fat Application Chain Theory". Starting from an independent perpetual futures application chain, Injective runs a typical order book model and is the first to adopt zero gas fees to avoid malicious MEVs from running as before.

In terms of value accumulation, Injective essentially burns 60% of all transaction fees managed by community-led auctions, creating deflationary pressure on the entire token supply. The remaining 40% is taken by relayers to incentivize liquidity depth on exchanges. In other words, the value accumulation of the $INJ token is a function of transaction volume, not transaction counts like other alternative protocols.

$INJ tokens can also be used as collateral backing for derivatives, serving as an alternative to other stablecoins in the derivatives market. In addition, Injective integrated with Skip Protocol in February of this year to return MEV earnings to shareholders and strengthen the early value accumulation case.

At the beginning of 2023, Injective was trading at a value of $130mn, and the market subsequently adjusted the token valuation upwards following the Injective Ecosystem Fund announcement; well-known venture capitalists are supporting their efforts to build an entire ecosystem on top of the order book.

As of writing, Injective has over $1.3 billion in trading value, up more than 10x year-to-date, outperforming most other tokens on the market. That said, metrics haven’t improved drastically since expansion, with Injective’s daily trading volume remaining at $10 million, which puts the annualized value accumulation in the form of burned tokens at around $4 million.

Nothing much has changed, but the “Fat Protocol Theory” has basically converged with this shift to the “Application Chain Theory”. Injective enjoys the dual advantages of the base layer and the application chain, while avoiding the main disadvantages of both.

The positive feedback loop still applies; investors invest in building the ecosystem, attracting developers and projects, which kickstarts the speculative value of the native network token, which indirectly addresses the security level of the chain that was previously evaluated as an application chain.

The value accumulation part is not affected by fee competition; instead of charging gas fees from the beginning, Injective profits from transaction volume; and adds value by providing a security and shared data layer.

Liquidity fragmentation and composability issues are resolved; native assets on the chain now have more use cases in application chains.

Overall, Injective, which is trying to build an ecosystem, has found a clear path to becoming “Fat” and staying “Fat”; therefore, it may present an attractive investment case even over a longer period of time.

So what do you think of Sei?

It will be hard to replicate the miracle of Injective again. Sei, widely considered to be Injective’s closest comparable company in the industry, may not see a similar trajectory. Both operate as order books; $SEI’s native token does not accrue value like Injective does; but instead, it acts as the network’s native gas token.

This minor difference essentially inherits the legacy of the “Fat Protocol Thesis” and puts Sei on the same playing field as other alternative layers.

The positive feedback loop is still present and applicable; as Sei is backed by a number of notable investors in the industry, the infusion of capital has yet to attract developers to the platform to drive growth for the network.

Value accumulation is a legacy pain point that has not been solved and Sei inherits this part; blockchains provide a shared data layer and level of security without effectively capturing any meaningful fees from Gas.

Liquidity fragmentation and composability issues are not entirely related because Lisk positions itself as an independent ecosystem; rather than having to interact with other chains in the Cosmos ecosystem.

Osmosis could be the next step.

The “Fat App Chain Thesis” was first validated in the market with the success of Injective; now it is time to look for another opportunity that follows similar logic to replicate this play.

Osmosis may be the next in line; as the team slowly builds an ecosystem around AMM-based appchains, such as the Mars protocol providing a money market; and the Levana protocol providing a perpetual futures exchange, etc. The protocol has also opened up market maker fees from its spot trading volume; effectively bringing value accumulation to token holders for the first time.

As an application chain and liquidity center on Cosmos; Osmosis's average daily spot trading volume is 6 million, which is not impressive. Partly due to the weakening of DeFi activities on Cosmos; the price of the $OSMO token has been on a downward trend since the beginning of this year, from a high of $1.10 to the current $0.30.

Once again, the “Fat Protocol Thesis” is gradually converging with the “App Chain Thesis” in the case of Osmosis; but more validation is needed to kick-start the entire price rally, as described below

Positive feedback loops are still lacking; Osmosis community is strong and strategically aligned with the entire Cosmos ecosystem, attracting teams to deploy applications on the app chain; but investors don’t seem to be committing money to the ecosystem yet

Value accrual is again unaffected by fee competition; Osmosis implements a 10 bps protocol market maker fee and profits based on spot volume; while adding value by providing security and a shared data layer

The caveat here is that protocol market maker fees could erode the unit economics of traders and arbitrageurs; this could impact spot volumes in the long term unless Osmosis manages to build a sustainable moat around protocol liquidity.

Liquidity fragmentation and composability issues are being solved; native assets on the chain can be used in other DeFi primitives on the chain

in conclusion

When $INJ rallied earlier this year, I thought it was a one-time event because the market was actually revaluing the token, applying the perpetual futures exchange trading multiples to the protocol layer; and that the token price would stop advancing after the price adjustment was complete.

This turned out to be one of my biggest mistakes this year. When I reflected on the basic logic behind it; combining the "Fat Protocol" and the "App Chain" actually created the most annoying rally because it solved the legacy problems of both parties; and speculative value was injected into the system along with the capital of institutional investors to start the flywheel.

I believe more application chains will take this approach in the coming months; because most of them are seeking to diversify their product offerings and retain value within the system, rather than competing with each other at the application level. The "Fat App Chain Thesis" may create more miracles in the open market.