Original author: Nina Bambysheva, Steven Ehrlich

Original source: Forbes

Compiled by: daiily Planet Daily

Amid the cryptocurrency’s existential crisis, its largest liquidity provider, Tether, has withstood multiple multi-billion dollar redemptions. Will competition and regulatory pressure from rival stablecoins like USDC force Tether to be completely candid?

On Monday, November 7, 2022, Tether executives received an unusual phone call from a long-time business partner, FTX CEO Sam Bankman Fried.

Bankman Fried, the young, disheveled cryptocurrency executive who has made a $26.5 billion personal fortune riding the wave of cryptocurrencies, sounded desperate on the phone. A piece of news in the industry media five days ago revealed that underpinning the highly leveraged balance sheet of his trading firm, Alameda Research, was a token called FTT issued by Bankman Fried worth approximately $5 billion. FTX and Alameda are Tether’s big customers. To date, Bankman Fried has issued a whopping $36 billion worth of U.S. dollar-based stablecoin USDT, accounting for almost half of the total issuance.

“He contacted us and asked for financial help,” said Paolo Ardoino, Terther’s CTO. "He didn't reveal details or exactly how much it would take, but we flatly refused."

Paolo Ardoino said the request was a bit odd and he quickly decided to reject it. "He suddenly asked for something he had never asked for before, and the way he said it suggested he had a big problem. And he wasn't talking about $10 million, he was asking for billions."

In the weeks following that desperate call, FTT fell from $26 to less than $2, wiping out about $3 billion in market value. FTX and Alameda would soon file for bankruptcy protection, and on December 12, Bankman Fried was arrested and indicted on eight counts, including money laundering and fraud.

Bankman Fried's demise is bittersweet for Tether, the controversial company behind the $66 billion stablecoin USDT used for more than 50% of all Bitcoin transactions worldwide.

FTX is Tether’s largest customer, but unlike Bankman Fried, who cultivated the media and hobnobbed with politicians, Tether has resisted regulatory scrutiny, which has been a source of media scorn.

But in a turbulent year for cryptocurrencies in 2022, Tether has persevered. In May, Tether faced $16 billion in redemptions from panicked cryptocurrency investors when the cryptocurrency's then-third-largest stablecoin, TerraUSD, and its sister token LUNA (market cap of $45 billion) suddenly collapsed. While USDT fell to 95 cents during the panic sell-off, it met the market’s redemption demands and rebounded to full value within a week. During FTX’s collapse, around $3 billion in redemptions poured in over a few days, but Tether barely missed a beat, with all redemptions occurring 1:1 against USD.

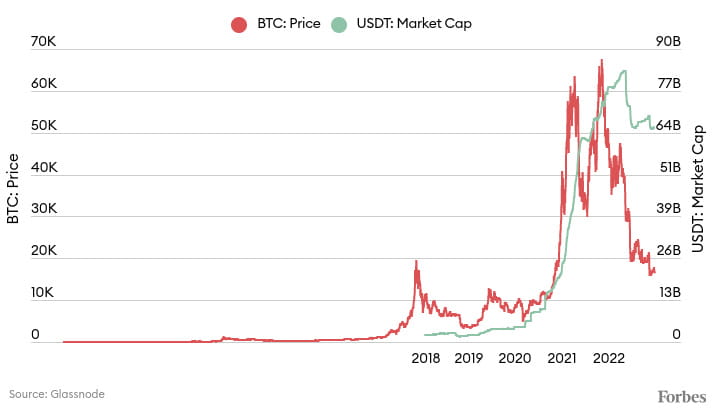

USDT market cap surges during recent Bitcoin bull run

“Everyone sees Tether as a ragtag group of people who don’t have the ability to do anything,” said Paolo Ardoino, Tether’s chief technology officer and the only C-suite member willing to speak to the media.

While Tether has proven its staying power in the market so far, the stablecoin provider has yet to gain enough trust outside of cryptocurrencies. Over the years, it has been accused of market manipulation, placing customer funds in the personal accounts of its executives, and propping up the price of Bitcoin. In 2021, the CFTC and the New York Attorney General forced Tether to pay fines of $41 million and $18.5 million, respectively, for misleading customers that USDT was backed one-to-one by U.S. dollars.

The company has never produced an audit report and has refused to disclose the exact mix of its collateral, which includes crypto tokens, loans and other illiquid investments. In contrast, its closest competitor USD Coin, operated by Boston-based Circle Financial, has revealed the specific Treasury notes, CUSIPs and maturities backing its $45 billion in digital dollars.

But if the cryptocurrency survives its current brutal winter, its dominant liquidity provider, Tether, must grow. That’s why Tether has recently been on a campaign to clean up its image. It has long been accused of padding its balance sheet with questionable commercial paper, and in June 2022 it pledged to eliminate $30 billion worth of commercial paper assets from its reserves and replace most of them with U.S. Treasury bills and other Cash Equivalents. Then in August it hired Big Five accounting firm BDO with the aim of conducting a full audit. Last Tuesday, the company announced that it would stop lending USDT by the end of 2023 – its loans represent 9% of its assets.

Will this be enough to silence the naysayers who have become even more timid about this bizarre stablecoin provider in the wake of FTX’s collapse?

"There's a difference between being generally stable and always being stable," said Acting Comptroller of the Currency Michael Hsu. "What's always stable is Fed money and central bank money. And if you fall into the forever stable category, you don't have to defend yourself publicly."

The fact that stablecoins like Tether need to exist across the board points to clear weaknesses in Bitcoin and other cryptocurrencies. More than a decade later, the original cryptocurrency is still very unstable. In the past 18 months alone, the price of Bitcoin has approached $70,000 twice before falling back more than 65% to a recent $17,000. Daily price swings of 5% or more are not unheard of.

Stablecoins were invented to solve this problem, but cryptocurrency investors have long faced another problem: Most cryptocurrency exchanges, especially those based overseas, are blocked by banks, Doing business in U.S. dollars and other fiat currencies is therefore difficult, if not impossible. Stablecoins live and move on top of various blockchains, just like Bitcoin, avoiding the control of central banks. In the case of USDT, which exists only in digital form, it is pegged to the U.S. dollar.

If stablecoins existing outside of the global banking industry make you uneasy, consider that the world's major stablecoin provider, Tether, is run by a group of shady characters.

Its chief technology officer, Paolo Ardoino, is the spokesperson for Tether. All media information about Tether passes through him. Tether’s chief financial officer, Giancarlo Devasini, is the company’s controlling shareholder and owns an estimated 40% of Tether’s parent company, according to sources familiar with its finances. DigFinex also owns cryptocurrency exchange Bitfinex.

Turin, Italy-born Devasini, 58, was a successful pioneer in the semiconductor market, growing his business to annual revenue of €113 million before he sold it shortly before the 2008 financial crisis, according to his official bio on the Bitfinex website. But a Financial Times investigation in July 2021 found that Devasini's business empire had sales of just €12 million in 2007 and went into liquidation in June the following year. Additionally, one of Devasini's companies, Acme, was sued for patent infringement by Toshiba over the DVD format specification. (Tether says the lawsuit is without merit and does not reach an adverse conclusion.)

Numerous sources claim that Devasini, who once studied to be a doctor, was the mastermind of Tether and played a direct role in issuing Tether tokens for large clients such as Alameda. Devasini's exact location is unclear, with various sources saying he is in the African island nation of Sao Tome and Principe, the Bahamas, Italy and the French Riviera, among other places.

The CEO of Tether is a Dutchman named Jan Ludovicus van der Velde. He owns 20% of the combined entity and lives in Hong Kong, according to sources familiar with Tether's finances. He also avoided interviews and stayed backstage.

If Devasini manages Tether and Bitfinex (incorporated in the Virgin Islands) from behind the scenes, Jan Ludovicus van der Velde is more of a figure responsible for maintaining high-level strategic relationships with banks and regulators. According to Paolo Ardoino, Jan Ludovicus van der Velde has made several trips to Europol since the start of the pandemic to explain how Tether works. Jan Ludovicus van der Velde also helped the company obtain a digital securities issuance license in Kazakhstan and is leading the effort to secure new banking relationships in Europe and Turkey.

In addition to shared ownership, Tether and Bitfinex both have the same CEO, CFO, CTO, and general counsel. The chief operating officer of Bitfinex and Tether is actually the wife of Paolo Ardoino, although she is not listed as a shareholder in documents seen by Forbes. Tether has about 50 employees in total, while exchange Bitfinex has 200.

There are two ways to acquire Tether tokens, known as USDT in cryptocurrency terms. It can be purchased on any of the hundreds of cryptocurrency exchanges around the world that list digital assets, or directly from Tether using Tether’s own controlled smart contracts that run on several different blockchains. The latter method is reserved for loan sharks, and each transaction must exceed $100,000 in USDT. Devasini is said to be involved in these large transactions, such as when Sam Bankman Fried personally called to issue large amounts of USDT for Alameda. Issues can sometimes reach as high as $500 million.

Such a business can be said to be very profitable. In terms of revenue, the issuance and redemption of USDT is an important source of profit for the company. It charges 0.1% per transaction. Forbes estimates that Tether has generated no less than $109 million in fee revenue since its founding in 2014, much of it in the past two years, during which time its market capitalization surged from $5 million to May 2022 of more than US$84 billion.

But the real wealth comes from how Tether invests the billions of dollars it receives to issue USDT. In theory, Tether should simply park customers' funds in cash and Treasuries, fulfilling its promise of reserves backed 1:1 by the U.S. dollar. However, Forbes found that Tether began creating a diversification model of reserve assets as early as 2015.

Why does Tether need to invest in risky assets other than U.S. Treasuries and money market funds? Paolo Ardoino said Tether is obliged to make a profit in order to obtain certain business licenses. “One of the most important things for our company, and what differentiates us from Circle (USDC issuer), is making sure the business model remains profitable,” said Ardoino, who expects the stablecoin company to grow this year. Revenue will exceed $600 million. In the third quarter of 2022, Circle, which operates under the slogan "Transparency and Stability," reported a profit of $43 million on revenue of $274 million - its first profit since its founding in 2018.

As with other stablecoins, the largest portion of Tether’s reserves has always been “cash and cash equivalents and other short-term deposits and commercial paper.” Based on its current reserve classification, 82.45% of its assets are cash and cash equivalents, of which 70% are Treasury securities. The remaining 17.5% is invested in a variety of riskier assets, including secured loans, details of which Tether has long been reluctant to disclose.

Tether has never had a definitive audit of its $66 billion in reserves, and its website only lists so-called certifications, which are snapshots without an accounting firm actually tracking the flow of funds or doing any serious due diligence.

Some of its counterparties include cryptocurrency trading firms Jump Crypto and Cumberland/DRW, according to companies familiar with Tether’s business. Additionally, the company provided an $841 million loan to now-bankrupt cryptocurrency lender Celsius in 2021, secured by Bitcoin. Paolo Ardoino said Celsius' loan has been fully repaid. The company did not say whether the other parties to the transaction were related companies.

In a recent Wall Street Journal article, a company spokesperson said the company itself holds collateral for all outstanding loans.

The rest of Tether's assets (about 4%) are invested in tokens and equity in private cryptocurrency companies, including Blockstream, Dusk Network and Renrenbit. It also invests in ShapeShift, OWNR Wallet and STOKR, LN Wallets and Exordium Limited. Given that the total market capitalization of cryptocurrencies has fallen by 63% this year, these assets have likely taken a huge hit.

While Tether is taking steps to become more transparent, Paolo Ardoino believes that no matter what the company does, it will not satisfy its critics.

“Genesis recently stopped withdrawals. Voyager is a public company, you know, Celsius and BlockFi, it’s a behemoth that’s praised by all parties. Three Arrows, is seen as the consummate trader,” said Paolo Ardoino. “Everyone is always better than Tether.”

Astonishingly, Paolo Ardoino pointed to Tether’s $18.5 million settlement with the New York Attorney General’s Office in 2019 as proof of his company’s enduring power. In that case, Tether secretly used its customers’ collateral to provide an $850 million emergency loan to sister company Bitifinex after the crypto exchange’s Panamanian bank, Crypto Capital, had its own funds seized by government regulators. In response, Tether said at the time: "The loan was to ensure the continuity of Bitfinex customers. It has since been repaid in full, early, including interest. At no time did the loan affect Tether's ability to process redemptions." "

“It’s good for people to ask questions,” Ardoino said, “but the fact that we keep exonerating ourselves and the other side is looking around him, that to me means there’s an ulterior motive.”

Meanwhile, Paolo Ardoino isn’t losing sleep over worrying about how to meet other people’s expectations of how Tether should operate or be disclosed. Tether has no plans to become a public company, and there are not expected to be any changes to its management structure.

For Ardoino, Devasini and van der Velde, the more serious issue is the state of the overall cryptocurrency market, of which Tether is a key liquidity provider. Stablecoins are crucial to active traders, but Tether’s market capitalization has fallen by more than 25% during the cryptocurrency winter. The situation is exacerbated by the fact that interest rates have increased significantly and there are now numerous options outside of cryptocurrencies and DeFi for traders to park their idle cash reserves. USDT yields currently average 2% on major cryptocurrency exchanges.

If cryptocurrencies recover, Tether may see other competitors vying for its position. That includes USDC, which already holds 29.8% of the market and is favored by Wall Street firms like BlackRock and BNY Mellon, in addition to major exchange Binance itself having created its own stablecoin, BUSD. And then there's also the possibility that at some point, a big bank or central bank that's guaranteed by the FDIC will offer a digital dollar.

“We don’t intend to be the largest stablecoin on the market forever. If tomorrow JPMorgan decided to create their JPUSD or whatever, they would overtake us in two seconds,” Ardoino said. "We want people in Turkey, Venezuela, and Argentina to use Tether. The only important thing to us is that our product is used by people in emerging markets and developing countries. They are the ones who really desperately need access to US dollars." people."

(The above content is excerpted and reprinted with the authorization of partner MarsBit, original text link | Source: daiily Planet Daily)

Statement: The article only represents the author's personal views and opinions, and does not represent the objective views and positions of the blockchain. All contents and opinions are for reference only and do not constitute investment advice. Investors should make their own decisions and transactions, and the author and Blockchain Client will not be held responsible for any direct or indirect losses caused by investors' transactions.

This article asks you to borrow "billions of dollars" if you ask! FTX sought help from Tether before going bankrupt but was rejected. First appeared on Blockchain.