Written by Sally Gu, Researcher at OKX Ventures

Primer

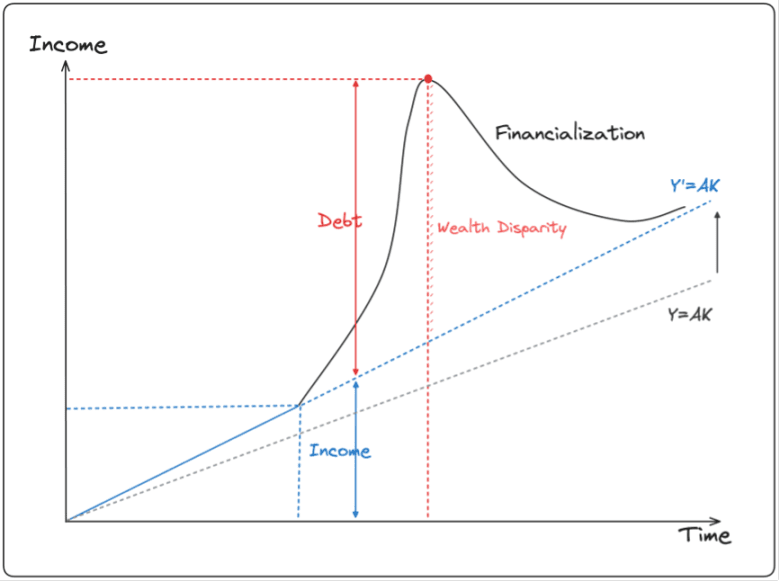

The impact of the epidemic and the Fed's successive interest rate cuts after Powell took over from Yellen have caused the market to reach the largest bubble stage of financial assets since World War II in the past few years under the conditions of high inflation and low real interest rates. However, the Sino-US trade war, the confrontation between Russia and Ukraine, and the rise of populist forces in Europe have fundamentally begun to undermine the foundation of globalization over the past 40 years. The financial wealth effect created by the loose liquidity and high leverage since 2018 is gone forever. Under the trend of inflation at the bottom of social wages and deflation at the top, the excess returns generated by the valuation expansion due to the downward interest rate seem to be irreversibly heading towards mean reversion.

Source:TS Lombard

Source:Bloomberg

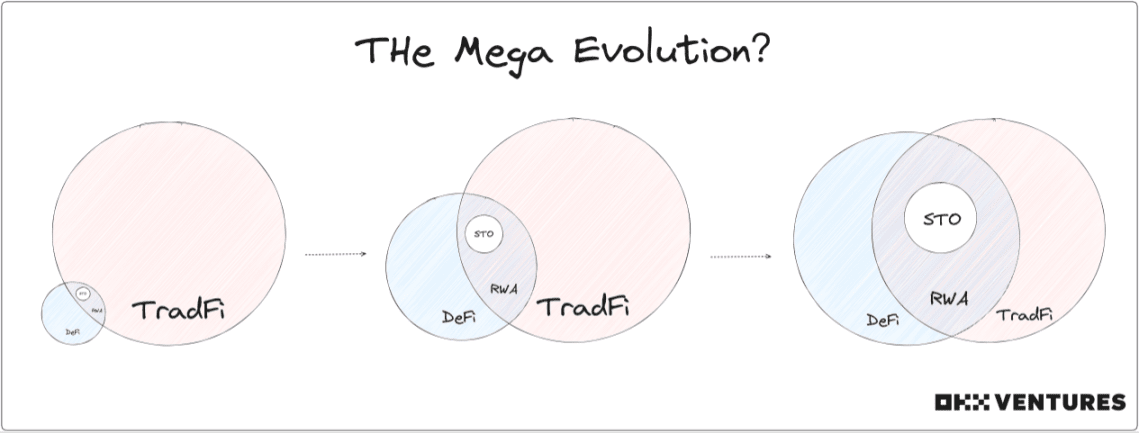

Therefore, after the interest rate hike cycle was prolonged, the long-short end of US Treasury bonds maintained a deep inversion of more than 50BP, and pure virtual financial narratives such as the Metaverse PFP NFT were declining because their intrinsic value could not support their traction. DeFi, or the crypto economy, is moving from virtual to real and embracing real assets and TradFi again. Perhaps this is a natural move during the recession and deleveraging cycle.

In order to further explore the integration and evolution trend of DeFi and TradFi, we have made a simple analysis of the RWA track, which is currently gaining increasing attention and discussion.

TL; DR

logic:

TradFi perspective: reduce transactions, improve transaction transparency and capital circulation efficiency; improve the composability of financial primitives, provide more hedging weapons; activate the funds of potential speculators and institutions

DeFi perspective: supporting and amplifying the DeFi speculative loop; introducing massive liquidity and expanding the DeFi user base; the stablecoin market has been proven

Track development driving force: macro cycle drives capital back to the market, old money and traditional institutions are increasingly interested, and the crypto market needs to attract new investors

Track development obstacles: uncertain regulatory environment, limited traction, limited high-quality underlying assets

Evaluation dimensions: product fundamentals, risk control capabilities, agreement mechanism, partners

Classification:

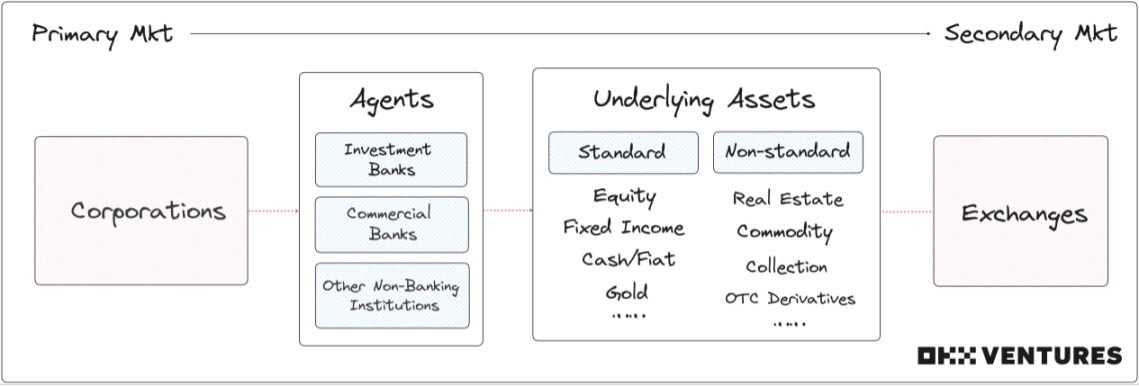

Defined by asset form: Standardized, non-standardized

Defined by major asset categories: legal tender, fixed income (bonds, credit), equity, alternative (real estate, collectibles, commodities)

提及 46 个项目:Centrifuge、ONDO、Maple、OpenEden、BondbloX、FortunaFi、CredeFi、Goldfinch、TrueFi、Defactor、Credix、Clearpool、Bru Finance、Resource Finance、Backed Finance、Sologenic、Swam、AcquireFi、Horizon Protocol、Hamilton Lane、RealT、Parcl、LABS Group、Propy、Atlant、ELYSIA、Tangible、Blocksquare、Milo、Figure、LandShare、Lingo、HOME Coin、Theopetra、EktaChain、Robinland、Homebase、4K、Arkive 、mattereum、Codex Protocol、PAX Gold、Tether Gold、Cache Gold、Agrotoken、LandX

View:

Currently, it is difficult to find PMF for most RWA products: in the short term, it is more of a narrative FOMO, not a real breakthrough innovation or strong growth momentum; pay close attention to the developments of compliance policies in the United States, Hong Kong and Singapore, and control policy risks to a minimum.

Alternative assets & non-standard RWA protocols are emerging: non-standard assets can be put on the chain using erc721/1155, erc20 may not become mainstream in the future. If it is bill NFT, RETIs NFT, collectibles NFT, there is a lot of room for imagination.

Treasury RWA will remain the mainstream, and equity RWA will attract more attention: U.S. Treasury bonds have been recognized by the crypto community; the demand for equity RWA is real, but it faces numerous obstacles in compliance.

The recognition of the crypto community is key, and cooperation with native communities is even more difficult to achieve: the difficulty of fixed-income RWA lies in the connection on the loan side; DeFi DAO members have very different understandings of off-chain assets, and overly complex off-chain assets are difficult for the community to understand.

Points worth discussing and further studying: On-chain ponzi games such as RWA Fi, RWA options trading, etc.; verification of on-chain middleware, SaaS companies, compliant issuers, and loan-matching intermediaries; the separation and coexistence of RWA DeFi and native DeFi.

basic concept

RWA — Tokenization of Real Assets on the Chain

STO —— Corporate Bond Financing

Difference: RWA has a richer product category, spanning the first and second levels, and the yield gradient can be built more extensively

market data

market data

The latest data shows that RWA has climbed to the top 10 in the TVL ranking of the DeFi category, with a year-to-date growth of 257%.

Source:Defillama

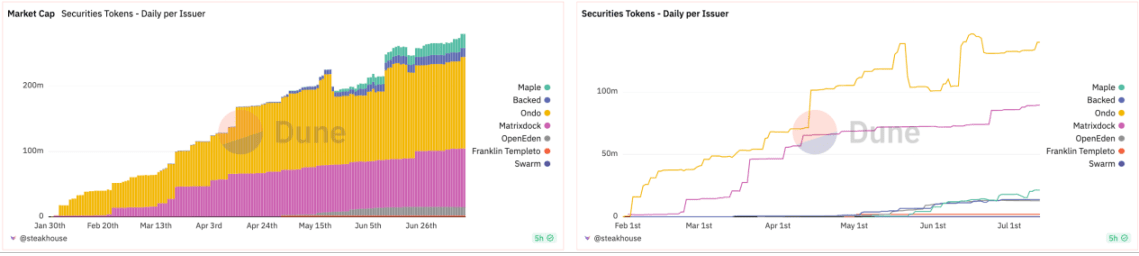

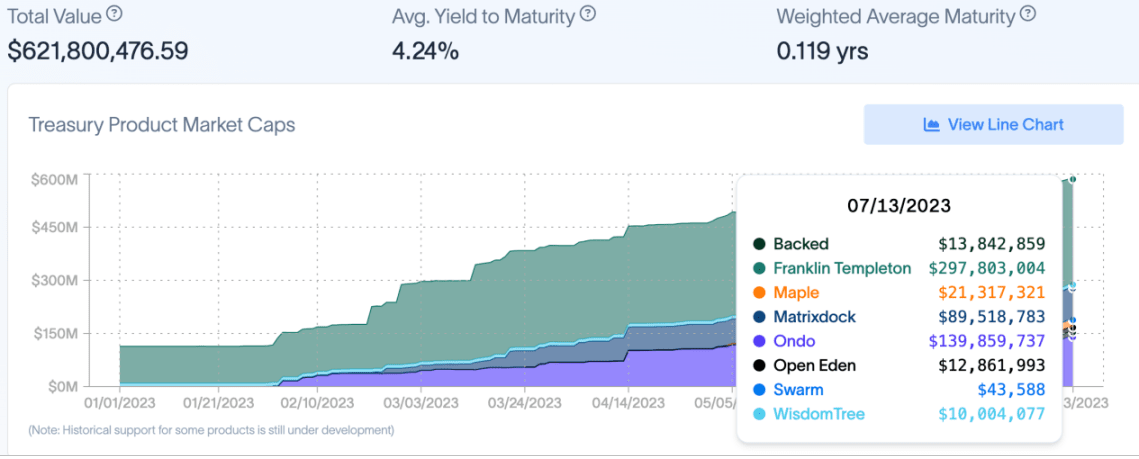

Since January this year, the overall market value and daily issuance of Treasury RWA Token have been rising steadily. Currently, the total market value of the top 7 projects is close to $300M.

Source:Dune

The total value of US Treasury RWA tokens has exceeded $600M. In addition, the number of RWA token holders has jumped from 28k to 40k, an increase of nearly 43%. Nearly 20k of them have held for more than 12 months.

Source:rwa.xyz

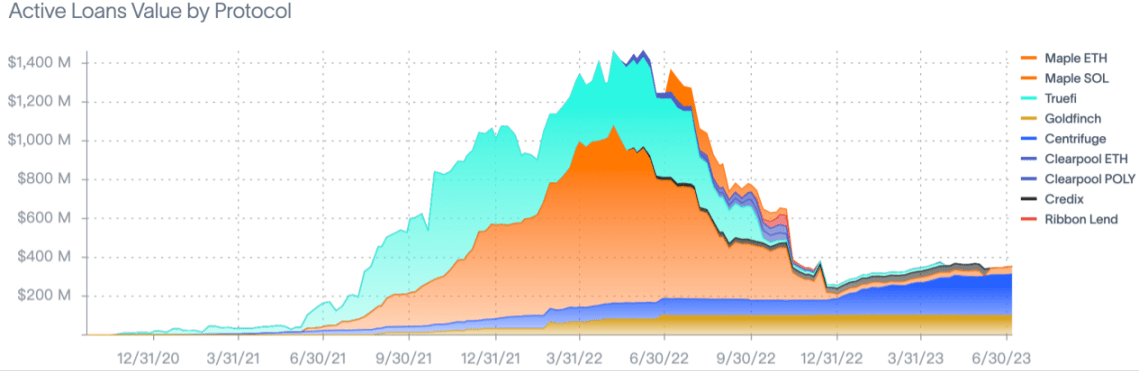

The private credit RWA protocol currently has approximately 1,553 loans, with a total active loan amount of $500M and a total locked amount of approximately $4B. Compared with the total loan amount of $1,500M at its peak last year, there is still a lot of room for growth.

Source:rwa.xyz

Statistics released by MarkerDAO in June show that RWAs continue to account for the vast majority of its stability fees. In May, RWAs accounted for 79.7% of all stability fees generated by the protocol, up 7% from April.

Source: MakerDAO

Track Logic

TradFi-wise

Reduce transaction costs and intermediaries, improve transaction transparency and capital circulation efficiency

Non-liquid assets such as real estate and artworks can be tokenized to disperse ownership and achieve rapid transfer, trading, mortgage and financing in the secondary market.

Heavy investments such as infrastructure, railways, and electrical engineering can be directly issued to quickly recover costs, and SMEs can use tokens for global crowdfunding

On-chain alternative assets & synthetic architecture improve the composability of financial primitives and provide more available hedging weapons

Derive a variety of portfolio paradigms, vertically extend the spectrum of asset products, and diversify the risk exposure of investment portfolios

In a single hybrid fund or structured product, on-chain assets can act as a hedge against traditional assets and currency fluctuations in jurisdictions.

Activate the funds of restricted foreign potential speculators and institutions

Inclusive finance narrative: larger TAM means higher profit margins

The funds that fled from the bank actually flowed back to tradfi in another form.

It further activates the global liquidity of funds and benefits some local institutional investors. The potential result is that it will rapidly aggravate regional wealth and liquidity problems and bring about more brutal social divisions.

DeFi-wise

Supporting and amplifying the DeFi speculative loop

DeFi creates a token speculation market, and the value capture of tokens mainly comes from the protocol's ability to generate revenue from speculative activities.

RWA can shorten this token speculation loop, and the underlying assets have liquidity, debt, collateral and other supports for exchange, which is equivalent to bringing a basic layer supported by traditional assets under DeFi.

Introducing massive liquidity to expand the scale of DeFi users

Simply put, the rules of the game of tradfi are more easily accepted by the mainstream, which helps to lower the learning and entry barriers of DeFi to a certain extent.

The volume and density of institutional funds, the scope of the audience and the exposure they can bear, the sales window channels, the proportion of market participants, and the degree of specialization of tradfi are far higher than DeFi.

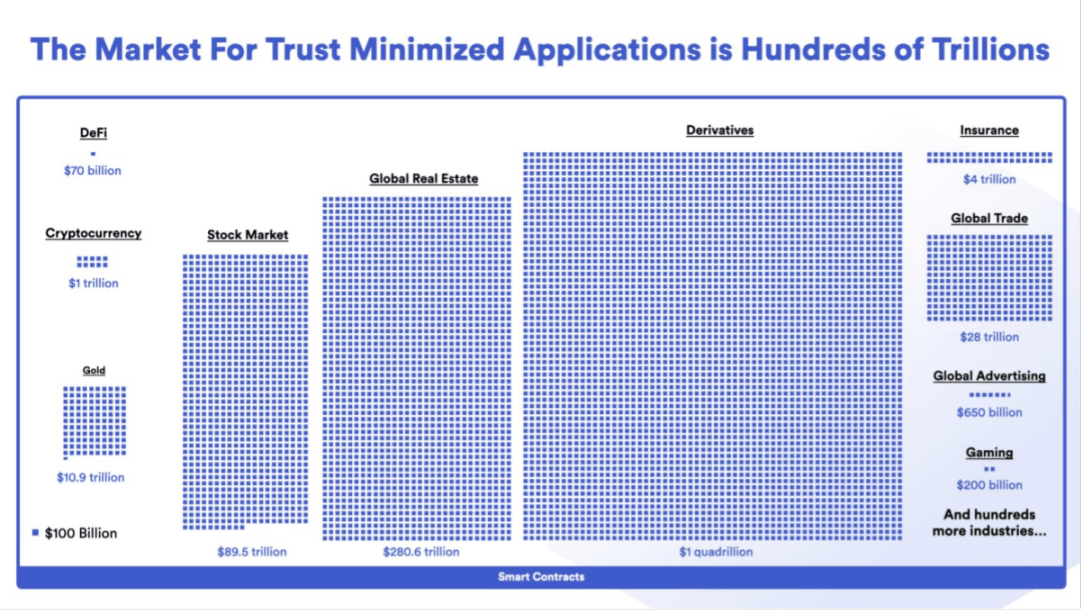

BCG&ADDX research believes that the tokenization market will reach 16 trillion in size by 2023 (including 3 trillion real estate market, 4 trillion listed/unlisted assets, 1 trillion bond and fund market, 3 trillion alternative asset market, and 5 trillion other tokenization market).

According to the most basic calculation by Citi, the combined scale of digital securities and blockchain trade finance could reach 5-6 trillion by 2030.

Source:Chainlink

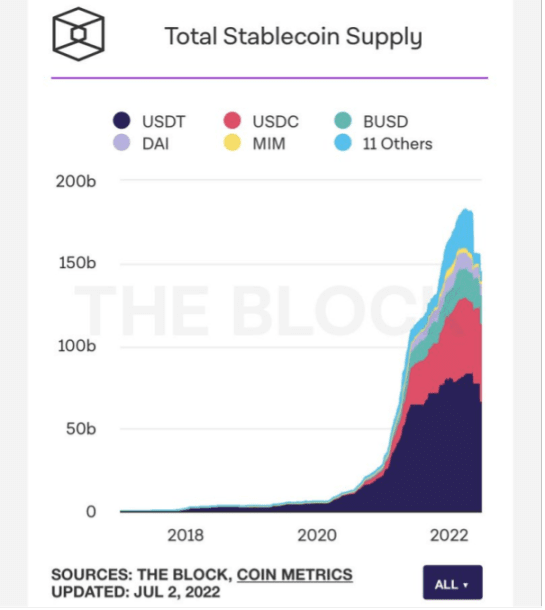

The stablecoin market has been proven

USDC and USDT are essentially RWA with fiat currency as the underlying asset.

2022 Peak Stablecoin Market Value Reaches 180B

Source:The Block

Momentum

The macro cycle drives capital back to the country

Tightened supervision and improved compliance laws

Traditional u-standard funds have more returns, and continued interest rate hikes have raised short-term government bond interest rates to 4% (the latest 2-year rate is 4.64%, a slight narrowing but still high)

Most of the idle money avoided risks after March due to the SVB incident, and is still mainly accumulated in stable assets such as US bonds.

Source: Alliance Bernstein

Old money and traditional institutions are increasingly interested

The launch of BTC ETF also shows that the alpha opportunities in the traditional market are also disappearing, and the mainstream is maintained by beta passive income (not actively seeking to exceed market performance, but only seeking market average returns)

Tradfi faces bottlenecks in its own development and seeks industry change, referring to past Internet + Finance, embracing AI, and fintech Pearl Aladdin

Lao Qian believes that crypto natives lack a complete understanding of tradfi and cannot fully understand the market depth. The RWA track is more suitable for traditional players to explore and layout

The crypto market needs to attract new users

A series of crashes (LUNA, FTX, etc.) have seriously eroded market confidence

On-chain liquidity dries up, NFT plummets

The first and second levels of the crypto-native infrastructure are inverted, and the protocol Lego innovation is boring

Resistance Handicap

Uncertain regulation climate

Taxation, asset definition, license establishment, recovery process and other system links all depend on the local financial policy environment

Digital asset regulation is fragmented in different jurisdictions around the world, and a unified classification standard does not yet exist

The attitudes of the central bank, banks, and the China Securities Regulatory Commission basically determine the life of the agreement, and the probability of thunderstorm is high

Limited traction

Contrary to crypto-native beliefs, PMF cannot be found

Early crypto native users are extremely resistant to centralized regulation and the banking system, seeking independent on-chain DeFi ecosystem development

Most DeFi participants dislike KYC/AML (although zkp solutions can provide privacy protection) and prefer completely permissionless interactions.

DeFi users with high risk preferences look down on the RWA yield. Even if they talk about equity RWA, the yield ratio may not be as good as building a pool at uni (especially now that v4 has introduced hooks to further liberate playability and freedom)

Low risk preference The DeFi user base is not large, and users can choose to directly stake mainstream coins/buy ETFs and receive passive income

Traditional institutions are not in a hurry to enter the market and are still weighing

On-chain liquidity is still tiny compared to traditional finance, and the current market depth is insufficient to create a huge wealth effect. It is only possible that the hot money of off-chain traditional financial players can feed back to the chain, rather than vice versa.

Based on this logic, it is still unknown how much effort traditional institutions are willing to put into exploring a metaphysical alpha arbitrage space, and how much percentage they are willing to allocate on their balance sheets. At present, it is impossible to allocate more than 0.01% on the balance sheet in the short term, which is insignificant compared to other businesses.

After communicating with the heads of traditional secondary funds, most of them said that they would not consider trading on-chain assets or synthetic assets in the short term: first, there are already sufficient substitutes and hedging methods in the traditional stock market; second, due to the background attributes and risk preferences of LPs, it is impossible to allocate too many crypto assets to interfere with their original investment system.

Limited high-quality underlying assets

The product categories of high-quality underlying assets such as US bonds are limited. Niche assets such as New Zealand stocks are not liquid enough and the delivery method is not T+0. Other small-cap stocks, penny stocks and altcoins are not closely related to the macro economy and it is difficult to formulate speculative strategies. It is unnecessary and unlikely to be tokenized.

Tokenizing similar underlying assets means that the barriers to competition for protocols will not be very high, and homogenization trends are likely to occur

The later tracks inevitably become Matthew-like, similar to LSD

Evaluation

1. Product fundamentals

The types of RWA products and yield range provided are differentiated and competitive in the market, and the scope of service operations (what assets are being serviced now, where are such services provided? Are they qualified to provide this service in the long term?)

TAM stickiness, user retention, asset pool depth and liquidity, funding discount rate

Protocol revenue and net profit, token value and circulation efficiency

2. Risk control capabilities

Team: Do you have experience working in traditional investment banks, commercial banks, or securities firms? Do you maintain a good relationship with the local legal system? Do you have a record of illegal activities or a bad reputation in the crypto industry?

Compliance: Is the company subject to local securities laws and regulations (how tolerant is the local policy environment and direction towards crypto? Do regulatory documents clearly define asset attributes or prohibit such assets?), KYC/AML, default settlement, compliance costs, credit assessment

3. Protocol Mechanism

Tokens mapped to real assets need to interact with multiple blockchain ecosystem backends, and building architectures on different chains requires interoperability of protocols.

Is the chain-on-chain method decentralized? What trust minimization mechanism is followed? Is the off-chain cash flow and related mortgage debt information disclosed regularly? What oracle network data operation mechanism is used? How to select nodes?

Can the security mechanism of the protocol effectively prevent information leakage of interactive account addresses, oracle manipulation, hacker attacks, etc.?

4. Partners

Whether to establish cooperation with mainstream DeFi crypto communities such as MakerDAO and Aave / have stable on-chain loan supporters

Whether to choose an experienced and trustworthy third-party institution for on-chain asset custody (eg: SPV control of off-chain collateral disposal rights)

Whether there is long-term cooperation with tradfi intermediaries such as banks and trusts with top reputation, scale and service scope

Underlying asset division

Defined by underlying asset form

Defined by underlying asset form

Standardization (S)

Semi-fungible/fungible, easily tradable assets with financial and monetary value

Public + On-site circulation

Generally regulated by the SEC

Non-standard (N)

Illiquid, non-fungible, hard-to-price, and hard-to-trade assets

Usually circulated in private + over-the-counter markets

More likely to be regulated by the CFTC

A brief overview of US regulatory agencies and their regulatory subjects is as follows:

Defined by asset class

Defined by asset class

The nature of funds determines the behavior of traders, and the trading behavior in the major asset classes determines that the options are different.

The potential user's tolerance range for risk and uncertainty determines their allocation ratio to different asset classes.

1. Fiat RWA

Common: US dollar, euro, yen, pound, renminbi, etc.

Focus on the series: Australian dollar, Canadian dollar, Korean won, Swiss franc, South African rand, Mexican peso, etc.

Key tool: Collateralized stablecoins

Projects: Circle, Tether, Frax, MakerDAO, etc.

The original RWA was a stablecoin project with fiat currency (mainly USD) as the underlying asset, such as Circle's USDC and Tether's USDT.

Transaction costs, channels, and optional categories are currently limited

If more fiat currencies can be issued as on-chain assets in the future, the fiat stablecoins of Russia, Malaysia, etc., which are weakly correlated with stocks and currencies, and Canada, Australia, South Korea, etc., which are negatively correlated, may become a good hedging tool (let’s not discuss the depth issue for now).

2. Fixed Income RWA

2.1 Bonds

Common: national debt (sovereign interest rate debt: US, Europe, Japan, Australia, China), central bank bills, government bonds, corporate bonds, foreign debt, credit bonds, convertible bonds, etc.

Key tools: ETFs, bond derivatives

Projects: Centrifuge, ONDO, Maple, OpenEden, BondbloX, FortunaFi, CredeFi, etc.

Treasury bonds/Treasury bond ETFs are currently the largest RWAs. Due to their low risk, they are usually regarded as safe-haven assets and are the main investment products in the fixed income category.

Despite the unsatisfactory yields, the leading DeFi community is still willing to balance its risk exposure through government and corporate bond RWAs. For example, 500 million DAI have been invested by MakerDAO in the first round of US Treasury RWA purchases at the beginning of the year.

There is still room for RWA in bills, corporate bonds, credit bonds, etc. Project parties can seek differentiated routes based on their own team resources and background advantages.

2.2 Credit

Common: personal loans, corporate loans, structured financing tools, personal housing mortgage loans, car mortgage loans, etc.

项目:Centrifuge、Maple、Goldfinch、TrueFi、Defactor、Credix、Clearpool、Bru Finance、Resource Finance 等

It can open up global credit and provide institutional investors and retail investors with more opportunities to obtain stable returns.

Enterprise loans have largely alleviated the financing pressure of SMEs and made it easier for them to obtain social and government support.

3. Equity RWA

Main markets: America, Europe, Japan, China, Hong Kong, and Macau

Focus on the sequence: some emerging markets of BRICS

Key tools: ETFs, index derivatives, leading stocks in key industries

Common: equity, primary shares (private placement), secondary shares (open market), etc.

项目:Backed Finance、Sologenic、Swam、AcquireFi、Horizon Protocol、Hamilton Lane 等

Individual stocks do not need to pay too much attention to the macro cycle, but more attention to the operating conditions of individual listed companies.

The demand for trading this type of assets is real, but it is greatly restricted by legal issues. BackedFi and other platforms that can achieve 24-hour US stock trading are likely to become a paradise for arbitrageurs.

The “synthetic asset” route combined with cryptocurrencies seems more attractive

4. Alternative RWA

4.1 Real Estate

Common: residential, commercial, etc.

Key tools: REITs

Project:RealT、Parcl、LABS Group、Propy、Atlant、ELYSIA、Tangible、Blocksquare、Milo、Figure、LandShare、Lingo、HOME Coin、Theopetra、EktaChain、Robinland、Homebase etc.

The tokenization of real estate and NFTization provide a convenient form of lending with real estate as collateral. The fragmentation of real estate on the chain is also conducive to retail investors' investment transactions.

The real estate package REITs blockchain solution is already mature, but overall cost control (personnel transportation, property management and maintenance, real estate distribution, residential type) still depends on the project party's ability

There is a tradeoff between underlying asset diversification & globalization of operations and project costs & scalability

4.2 Collectibles

Common: Artwork, jewelry, coins, etc.

Projects: 4K, Arkive, mattereum, Codex Protocol, etc.

Asset types with large single asset amounts but low standardization

It can cut into the more niche and non-standard trendy brand name trading track and create new trading positions, such as traders of famous watches, cars, and bags on the chain

The imagination space of "make dealer as trader" is good

4.3 Commodity

Common: precious metals (gold, silver, platinum and palladium), base metals (copper, aluminum, cobalt, lithium, zinc), energy (crude oil BRENT, WTI)

Focus sequence: iron ore, coal, dairy products, agricultural products, etc.

Projects: PAX Gold, Tether Gold, Cache Gold, Agrotoken, LandX, etc.

The degree of non-standardization is high, and the traceability, title confirmation, pricing and verification on the chain are usually very complicated. The process of the project party finding and packaging assets is too long, which may lead to large cost consumption and make it difficult to achieve rapid growth and expansion.

TAM is relatively limited, niche assets require in-depth consideration, and are only suitable for professional commodity investors.

Agricultural products tend to be in a pure commodity investment framework. Investors who lack traditional commodity investment experience find it difficult to judge the production cycle of cash crops, storage and transportation processes, regional market environment, and the impact of climate and temperature changes.

Crude oil is basically observed as an interest rate factor and is highly correlated with interest rates. Traditional investors can directly purchase mainstream interest rate products and do not see much on-chain demand.

On-chain gold purchases can achieve instant settlement and redemption, which has certain advantages. However, gold can be considered based on bond logic (interest rate + inflation expectations), and investors with large positions can still prioritize the allocation of mainstream US bonds and other RWAs

POV

Long-term planning, small steps, waiting for the wind to come

RWA is likely to be a "necessary evil" for DeFi to expand to the next scale of 10 billion users, but in the short term it is more of a seller's shouting and narrative FOMO, not a real breakthrough innovation or strong growth momentum. For small and medium-sized retail investors, they should still allocate assets according to their own needs.

It is recommended that institutions focus on the long-term layout of 1-2 leading projects with innovative designs. In addition, they should pay close attention to the dynamics of compliance policies in the United States, Hong Kong and Singapore. Only with the coordinated cooperation of tradfi financial institutions can the policy risks of the overall track be minimized.

The obvious trend is that alternative assets & non-standard RWA protocols are emerging

Is it necessary to standardize the underlying assets? In fact, it is not necessarily the case. Non-standard assets can be directly put on the chain using the non-standard protocol erc721/1155. Structured products can even directly use the latest 6551. It is not necessary to use 20. 20 is unlikely to become the mainstream in the long run.

Centrifuge, Fortunafi, etc. have already provided collateralized lending by packaging future income notes as NFTs; emerging protocols for RETIs and collectibles underlying protocols such as 4K that cut into the NFT RWA narrative have a large imagination space. After gaining the trust of the community in the early stage of operation, there is a chance to lead the next wave of trends.

Treasury/U.S. Treasury RWAs will remain the mainstream niche, while equity RWAs are gaining more attention

The mechanism for putting U.S. Treasury bonds on the blockchain is mature and the asset structure is robust. It has been recognized by the crypto community, but most of them have already issued tokens on the platform. The stock market is competitive, and the plate is large but there are no new tricks.

Thickening products such as equity RWA provide on-chain traders with the opportunity to speculate on traditional stocks. The demand is real, but they face obstacles at the compliance level because the influx of funds that are too discrete and untraceable on the chain is likely to disrupt the normal operation of the internal financial systems of various countries.

Currently, most equity RWAs are still only aimed at high-net-worth and ultra-high-net-worth institutional users, and have not played a role in lowering the threshold for retail speculation. There is still a lot of room for development in this area.

The recognition of the crypto community is key. Cooperation with the crypto-native community on the chain is more difficult to achieve than cooperation off the chain.

As far as fixed-income RWA is concerned, it is not difficult to advance off-chain cooperation because it can bear lower borrowing costs. The difficulty lies in opening up the loan side.

Cryptocurrency treasuries such as DeFi DAO have a large amount of loanable funds, but DAO members have very different understandings of off-chain asset collateral, and the project party needs to provide transparent solutions in the specific auditing, underwriting, and off-chain asset tracing processes.

There will be a certain degree of friction between the off-chain tradfi lending compliance process and the DAO governance mechanism. Overly complex off-chain assets are difficult for the crypto DAO community to understand. If community members do not understand or do not want to understand, then the proposal will be shelved or rejected for a long time, and cooperation cannot be achieved. In theory, it is difficult for a pure tradfi background project to buy the trust of the community.

Points worth discussing and further studying:

On-chain ponzi games based on RWA assets are likely to be more suitable for crypto-native exploration, such as RWA Fi, RWA options trading, etc.

Middleware, SaaS companies, compliant issuers that verify assets on the chain, and intermediaries that match borrowers and lenders on the chain, such as IX Swap, Stima, Castle, Curio, etc., are worth paying attention to. Monopoly players may emerge in the future.

It remains to be seen how the regulated RWA DeFi and unregulated native DeFi will be separated and coexist in the future, and what kind of competitive landscape they will present with CeFi.

Conclusion

The enthusiasm of European and American asset management institutions to get involved in the bond market of emerging countries through various means and private financial services has never faded. With the gradual improvement of encryption infrastructure and the trend of huge asset management such as Blackrock regarding BTC as digital gold, it is not difficult to see that the traditional fragmented financial market is also actively seeking better fund utilization scenarios and liquidity efficiency improvement solutions. Tightening supervision actually means the beginning of its serious gaze and governance measurement on encryption. When the vision of the world economy shifting from Keynes to Austria gradually becomes a reality, the tentacles of encryption in the traditional stock, bond and foreign exchange markets will accelerate.

Amidst the shouts of “models will eventually rule the world”, DeFi is whispering about swallowing up all markets.

TradFi may embrace crypto faster than you expect :)