Author: Grace Deng, researcher at SevenX Ventures; Translation: Golden Finance xiaozou

The debate surrounding Lido’s centralization risk has reached a boiling point. While focusing on the risks, we should also pay attention to the related efforts and potential solutions being explored. This article will reveal the full picture of this centralization problem.

1. Centralization Issue

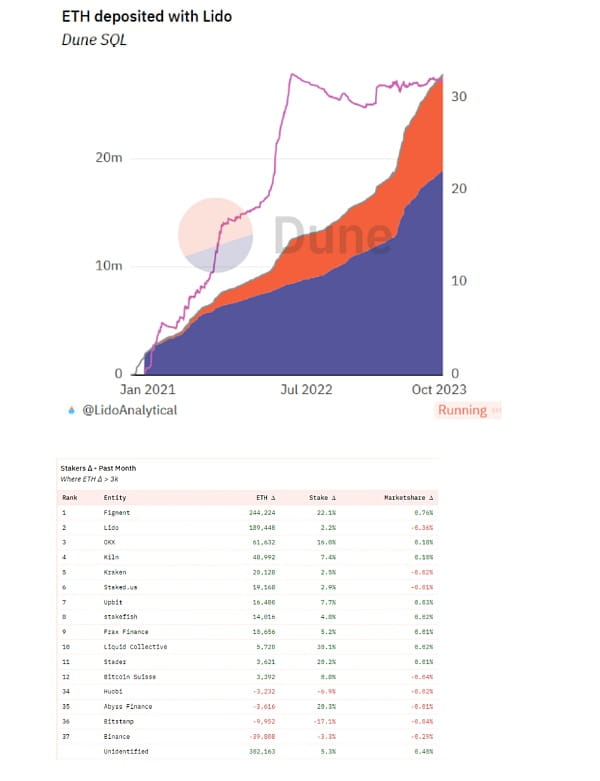

Lido’s market share accounts for almost a third of all staked ETH. With concerns centered around governance attacks, Lido’s continued growth could lead to excessive dominance of stETH (perhaps even more dominant than unstaked ETH).

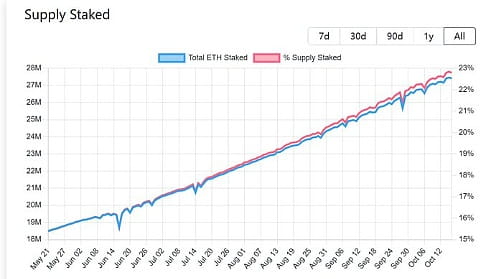

Note: The current ETH supply staked accounts for approximately 23%.

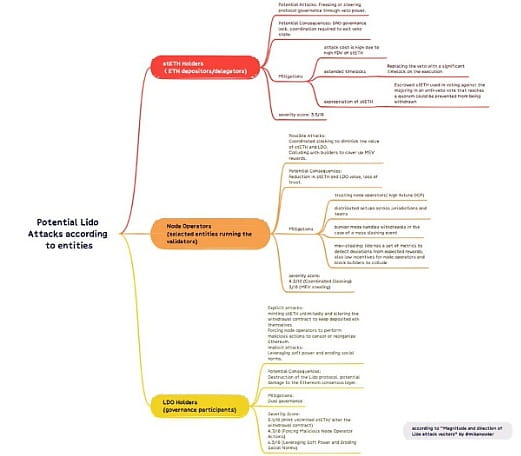

For example, LDO holders (the top 100 wallets control about 95% of LDO) could mint unlimited stETH or change the withdrawal contract and collude with others to keep their ETH deposits. mikeneuder.eth published an article analyzing all potential risks, impacts, and solutions.

stETH holders may abuse their veto power (not initiated) to block government proceedings. Node operators may collude to cause slashing, thereby harming the value of stETH. LDO holders may participate in the above government attacks or use their soft power to erode social norms.

2. The other side of LDO

A typical crude solution is self-limitation, that is, publicly committing to limit oneself from operating more than a certain percentage of validators, whether through coercion or raising fees. The result is: 99.81% of LDOs voted no, and only 8% of LDOs voted in favor.

We cannot oversimplify the centralization problem of decentralized protocols; on the other hand, there are many other factors to consider. Imposing restrictions on one LS solution is likely to create an exchange-dominated situation, which is even worse. Why do I say that? That's because: due to strong network effects and brand effects, the LST market may be a winner-takes-all market. RPL and other decentralized solutions may find it difficult to scale quickly.

Recent data can serve as a good reference: in the past, the growth rate of Lido’s announcement of breaking through 1 million ETH has dropped significantly, but new funds have flowed to centralized exchanges and staking pools rather than other decentralized LSPs (the only ones that broke through 3,000 ETH last month were lido and frax).

3. We are on the right track

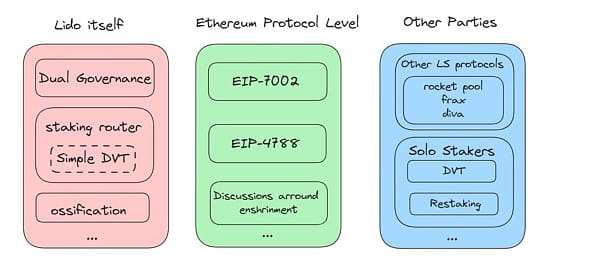

While self-limitation may not be a good idea, it doesn’t mean we should do nothing. Thankfully, things are now moving in the right direction, with many solutions proposed by Lido, Ethereum, and others.

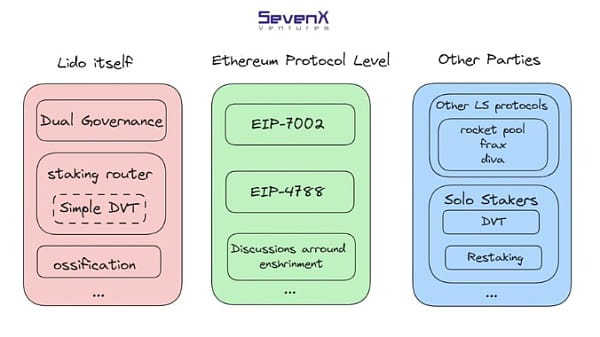

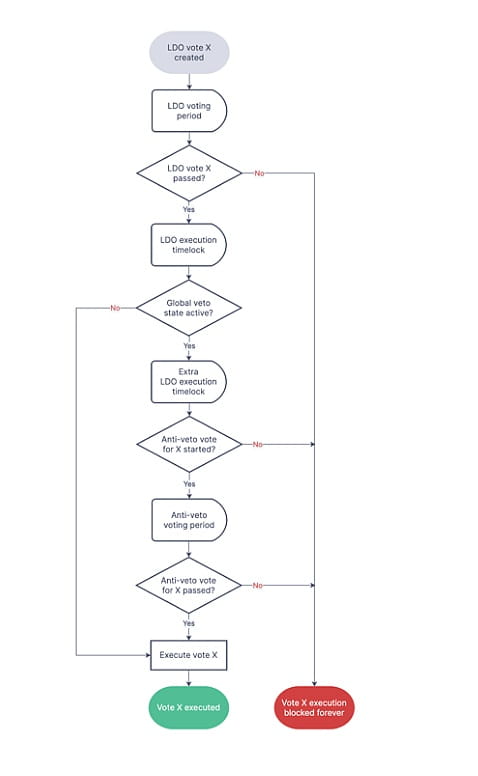

(1) Lido’s dual governance framework

Skozin.eth pointed out that the root cause of the additional risk introduced by Lido governance is the PAP between stakers (delegators) and LDO holders (agents). Lido proposed a dual governance framework to resolve this conflict.

Dual governance adds a time lock after voting and before execution, so that stETH holders can veto decisions and transition governance to an unexecuted state unless the veto is specifically revoked later. stETH holders will have the right to suspend execution.

More details are still under discussion, such as whether Lido should include more governance parties, such as node operators and Ethereum users, and mechanisms to prevent governance "stagnation", etc. The introduction of dual governance will definitely reduce Lido's governance risks.

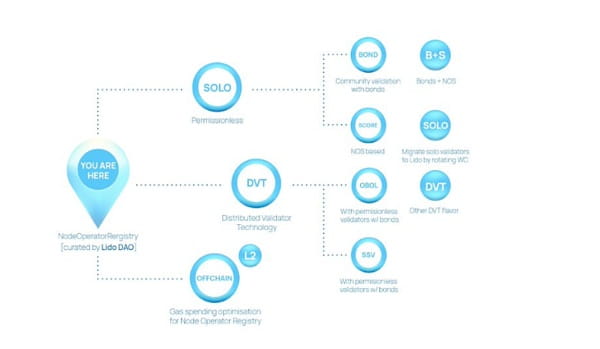

(2) Lido’s staking router

To reduce the risk for node operators, Lido is continually adding more node operators, evaluating their client diversity, geographic and infrastructure distribution, and experience running validators at scale. The number of Lido node operators recently increased to 38.

Additionally, Lido upgraded to v2 in May and introduced the Staking Router, a new modular architecture that allows arbitrary new staking modules to be added and managed. Currently there is only one module, but there will be more eventually.

When a new module is added, it receives all new stakes until a cap is reached. This cap can be increased as reliability is proven. In this LT, the stake router is market driven, where modules express preferences and stake allocation is optimized based on relevant metrics.

LDO holders will be responsible for determining the allocation (cap) of different modules. They will also need to monitor performance and balance risks to maintain the fungibility of stETH.

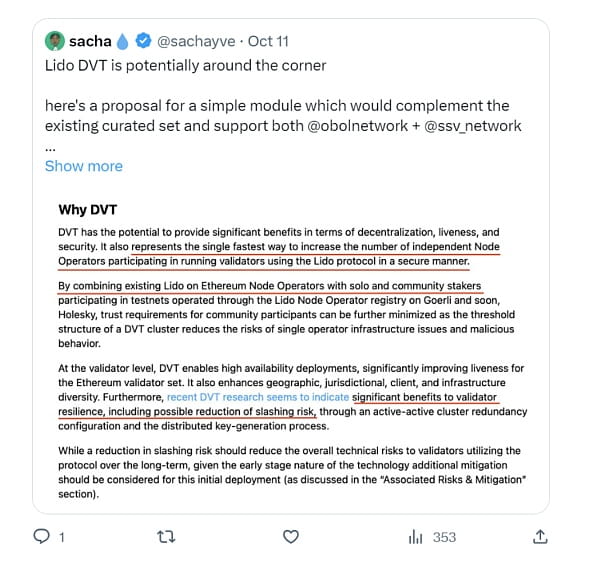

The latest proposal for the staking router is called “Simple DVT” and leverages DVT (Distributed Verification Technology) from Obol Labs and SSV Network: it is named “simple” because the module will be limited to 0.5% of Lido’s stake and will also include coverage plans due to limited testing of DVT.

Although the cap for this module may be increased in the future based on the performance of each group, it is not economically advantageous to initially set a low cap. Therefore, the fee distribution for this module will be 2%/8% instead of 5%/5%.

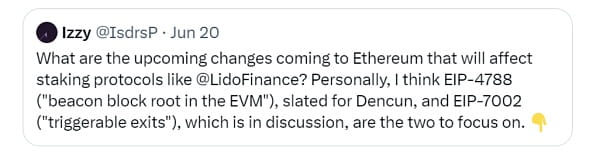

(3)EIP-7002 & 4788

At the ETH protocol level, several upcoming EIPs can help streamline workflows and improve the security of the LS protocol. EIP 4788 will reduce oracle risk.

EIP-7002 enables triggerable exits with exit keys, reducing operational risk for node operators. However, it relies on stETH holders being able to effectively veto malicious exits (if there is a dual governance framework at the time).

(4)Enshrinment

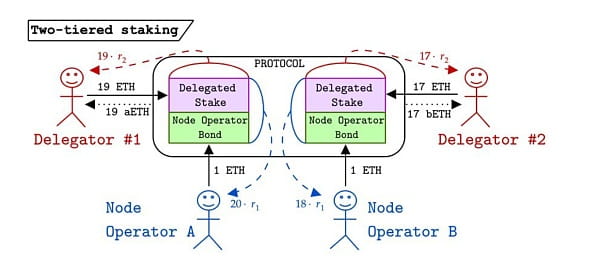

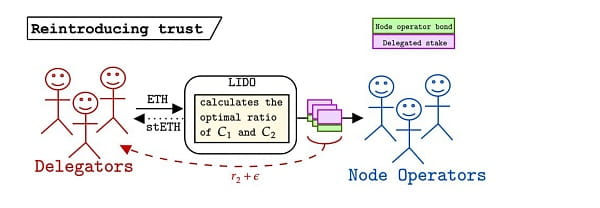

Vitalik's latest article discusses some of Enshrine's in-protocol features that make LS less centralized. Dankrad proposed a two-level pledge similar to the RPL mechanism: only ETH staked by node operators is slashable, and a limited number of LSTs can be issued.

ETH holders receive a risk-free interest rate on the ETH they delegate, and can flexibly switch node operators without waiting time. Since all LSTs are risk-free by design within the protocol, the delegator will only evaluate node operators based on revenue and token utility.

Looking at the benefits and utility, since LST has the same security and r2 within the protocol, ideally downstream DeFi protocols will receive more LST, replacing the winner-takes-all market with an oligopolistic market.

However, node operators may choose to sacrifice profits (r1- ε) to attract more stakers. Delegators may choose to delegate to node operators outside the protocol to obtain higher returns (r2+ ε) at higher risks. As a result, the in-protocol LS mechanism is no longer used, re-injecting trust into the system.

The two-tier staking mechanism is still in its early stages, with unresolved issues such as determining the optimal values for r1 and r2; the potential impact of implementing risk-free LST and achieving 100% ETH staking; and the need for randomly sampled committees to prevent centralization of node operators.

(5) Other LS protocols

Rocket Pool’s future Saturn upgrade could greatly expand permissionless LSPs and potentially reduce node operator bonding requirements exponentially by implementing MetaPools that connect validators and adjusting risk calculations (solving the dilemma mentioned earlier).

Frax Finance's upcoming frxETH v2 decentralizes validators and creates an efficient lending market, achieving dynamic interest rates determined by market forces and utilization, and improving capital efficiency.

Diva = Liquidity Staking + DVT + Cryptoeconomic Mechanism, which allows to operate a node with only 1 ETH. Currently Diva is in the "pre-release" stage, and participants can stake their ETH or stETH to get DIVA token rewards.

(6) Independent Pledger

We can expect the number of independent stakers to increase in the future as re-staking protocols and DVT protocols are implemented. Re-staking protocols such as EigenLayer may increase returns for independent stakers and make running a node from home more attractive.

DVT solutions like Obol Network and SSV Network can lower both the technical and economic barriers to entry for home stakers. Their launch also helps to enhance decentralization and reduce operational risks for LS protocols like Lido and Rocket Pool.

Izzy brings up an interesting point: by combining the low barrier to entry achieved by DVT with better macro (higher ETH prices), the number of independent operators can be greatly increased. In addition, the DVT solution helps reduce operational risks. While these risks are rare, they are not impossible to occur.