Valuation indicators such as price-to-earnings ratio and price-to-sales ratio are not applicable to the underlying public chain (L1) tokens. The company value is the discount of future cash flow, while the blockchain value comes from how many economic (transaction) activities the token holders support. , rather than the proportion of gas fees from trading activities that is drawn by the platform as "profit".

It is equally absurd to use a discounted cash flow (DCF) model to value public chain tokens, because the company’s future cash flows are in the same currency as its stock price, such as USD. However, Solana and Ethereum’s future cash flows are in SOL and ETH, not USD. Therefore, assumptions about the exchange rate for each future period need to be made to arrive at a USD-denominated DCF valuation.

However, this idea first requires calculating the future USD/SOL exchange rate. Tascha Che believes that the underlying (L1) token should be valued as the currency of the "cryptocurrency country".

The larger the blockchain platform, the more it resembles a sovereign economy. Its native token is a real currency, and the currency exchange rate model is more useful than the stock model when valuing L1 tokens.

Using the monetary quantity model to evaluate the token exchange rate,

The formula is: Money supply (M) · Velocity of money (V) = Price (P) · Real GDP (Y)

Assume country A = United States, country B = Ethereum,

ETH/USD will appreciate in the following cases: Ethereum GDP (Y_ETH) grows faster than US GDP (Y_US); US money supply (M_US) grows faster than Ethereum money supply (M_ETH); USD money velocity (V_US) grows faster than ETH money velocity (V_ETH);

Taking the money supply as an example, the massive expansion of the Federal Reserve’s balance sheet since 2020 and the sharp rise in the US dollar price of ETH are examples of this.

Similarly, there should be a one-to-one correspondence between the growth rate of Ethereum GDP (total economic output of Ethereum) and the price of ETH. Although no statistical bureau compiles a "GDP" for the "Ethereum country", GDP growth can be indirectly inferred from the growth rates of transactions, wallets, and total locked value (TVL). The growth of wallets can be considered as an increase in the country's "working population", and the growth of TVL reflects the growth of the financial sector in the economy.

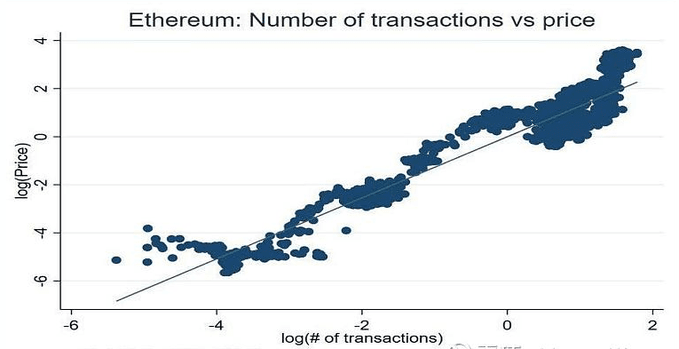

Empirical data confirms the relationship between these variables and the token/USD exchange rate, with a near-linear correlation between trading volume growth and ETH price growth, with a 10% increase in trading volume implying an average 13% increase in price:

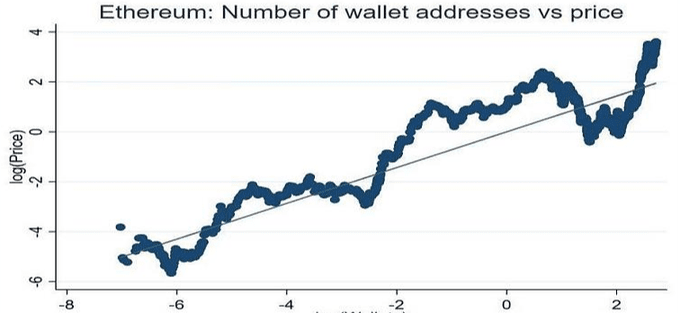

Likewise, a 10% increase in total wallets means an average price increase of 7%:

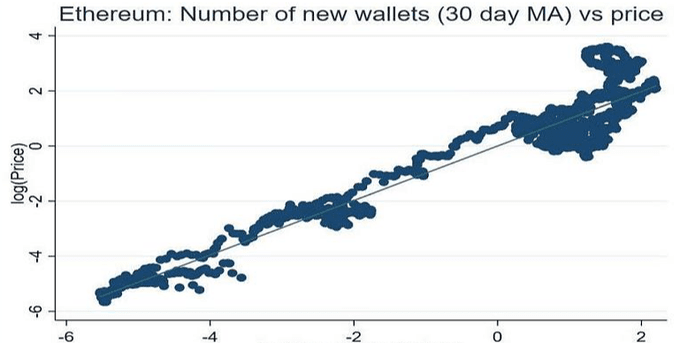

Surprisingly, the acceleration of wallet growth (i.e. the rate of new wallet growth) and ETH price growth have an almost 1:1 relationship:

Software development in the virtual world is like construction in the real economy - a leading indicator of GDP growth, developer activity on L1 platforms is a better predictor of upcoming economic expansion than transactions or wallets.

When searching for “ethereum” and “solana” on Github in May 2021, the repo results returned by the former were 65 times that of the latter.

By October, the multiple had shrunk to 17x — positively correlating with the rapid growth of the “Solana Nation.”

For digital currencies, the above currency exchange rate model does not take into account another key variable: the stability of the blockchain platform’s cash flow, which is very important for the stability of the L1 token.

It is no accident that governments are the monopoly issuers of money.

There have been many private currencies in history, but they never lasted long and were always phased out by government currencies. Among the many problems with private currencies, the lack of a "fiscal basis" is the most serious one. The government can protect the value of its currency through taxation, which is the most stable and almost guaranteed income.

Even if fiat currency is "unbacked", the government can raise resources through taxation and use these resources to buy/sell its currency to defend its value, which can bring confidence to currency holders, which non-government currency cannot. However, it is different now.

By incorporating transaction fees into every economic activity on the platform and using them for token destruction or staking rewards, the currencies of “blockchain nations” are gaining financial backing similar to government currencies.

While these cash flows do not determine the token price, they help keep the exchange rate stable in the long run. But what matters most to the token price is still the GDP growth of the cryptocurrency “country”.

Since web3 is only in its primitive stage, the story has just begun.