Reference reading: "Understand what the CFTC weekly position report is in one article"

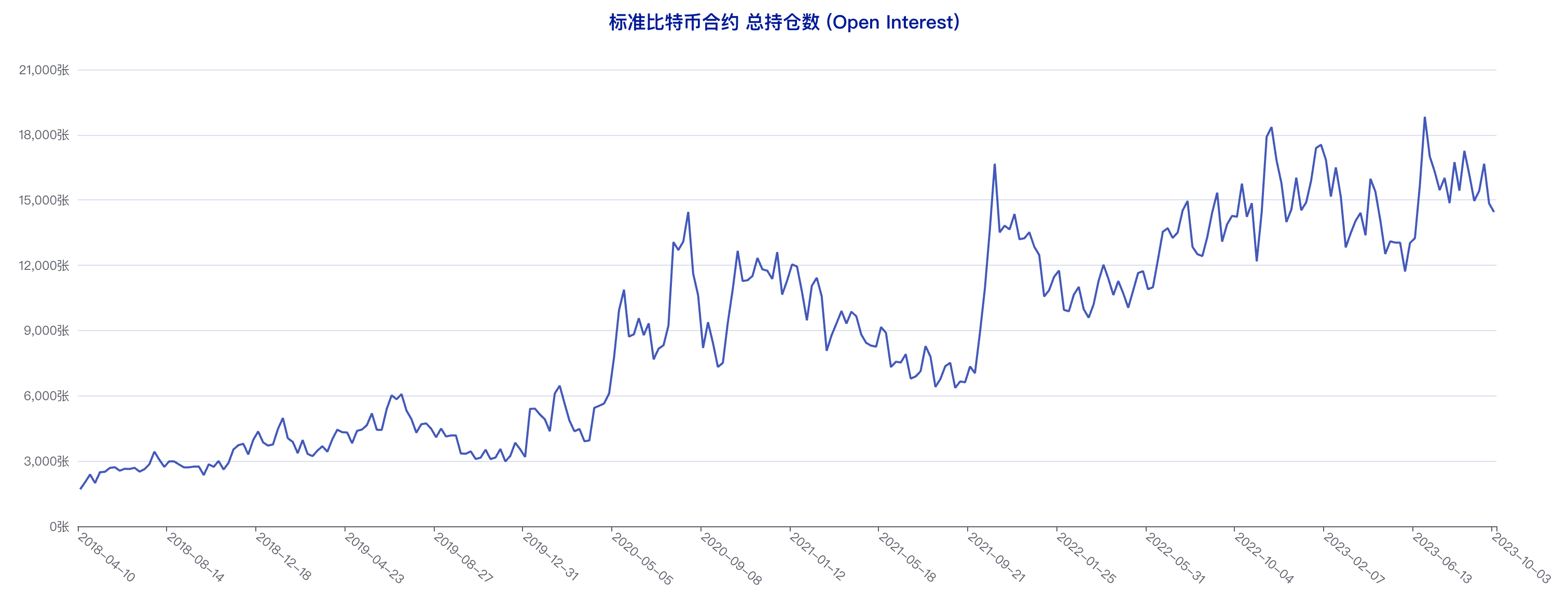

The latest CFTC CME Bitcoin Positions Weekly Report (September 27 - October 3) released on October 7 showed that the total open interest of Bitcoin standard contracts dropped from 14,844 to 14,447. This value has dropped for two consecutive weeks, setting a new low in nearly 16 statistical cycles. However, this value has not changed much compared with the previous statistical cycle, and the market has entered a new round of stability. Against the background of many types of accounts turning short in the previous statistical cycle, whether there are any changes in the market in the latest statistical period is the key point of this weekly report.

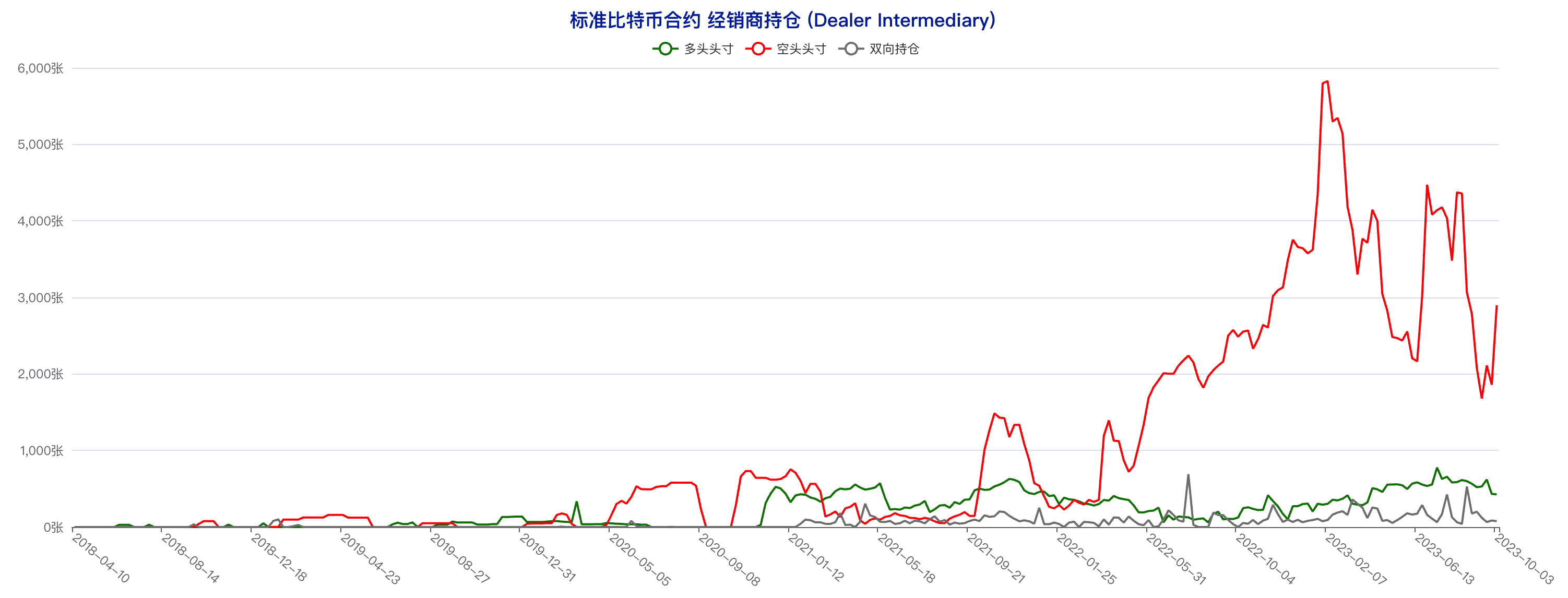

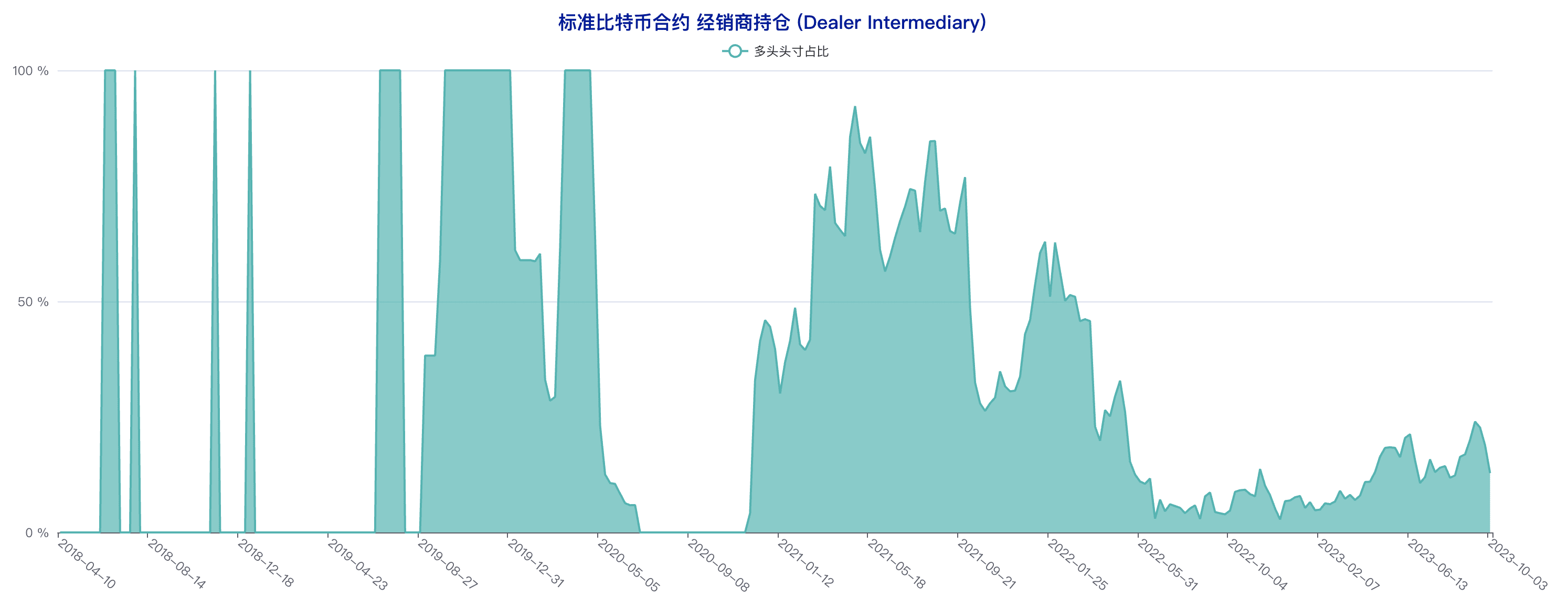

The largest dealer account’s long position decreased from 433 to 427, and its short position increased sharply from 1859 to 2898, which was a 6-week high. Such accounts had a clear net cold adjustment in the latest statistical period. After expressing a certain bearish attitude in the previous statistical period, such accounts increased their short positions significantly in the latest statistical period. Large institutions "ignored" the rebound in the market and expressed a very strong bearish attitude towards the market outlook.

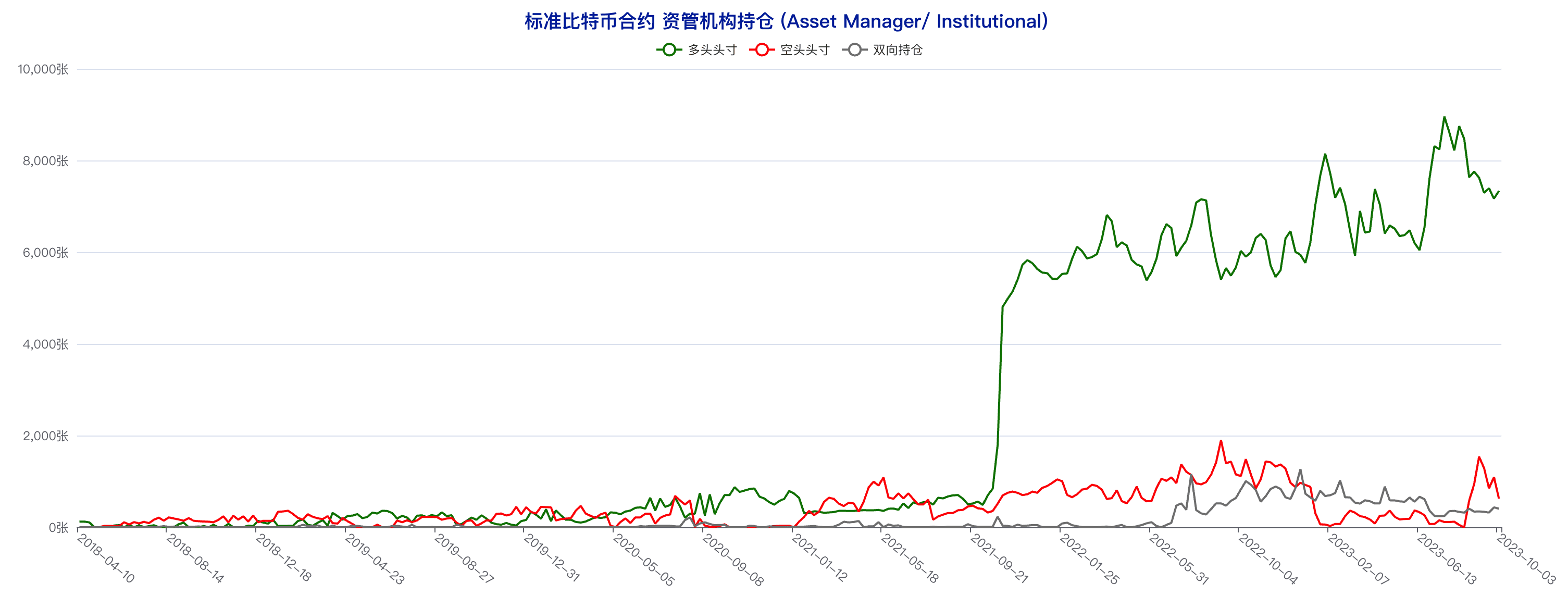

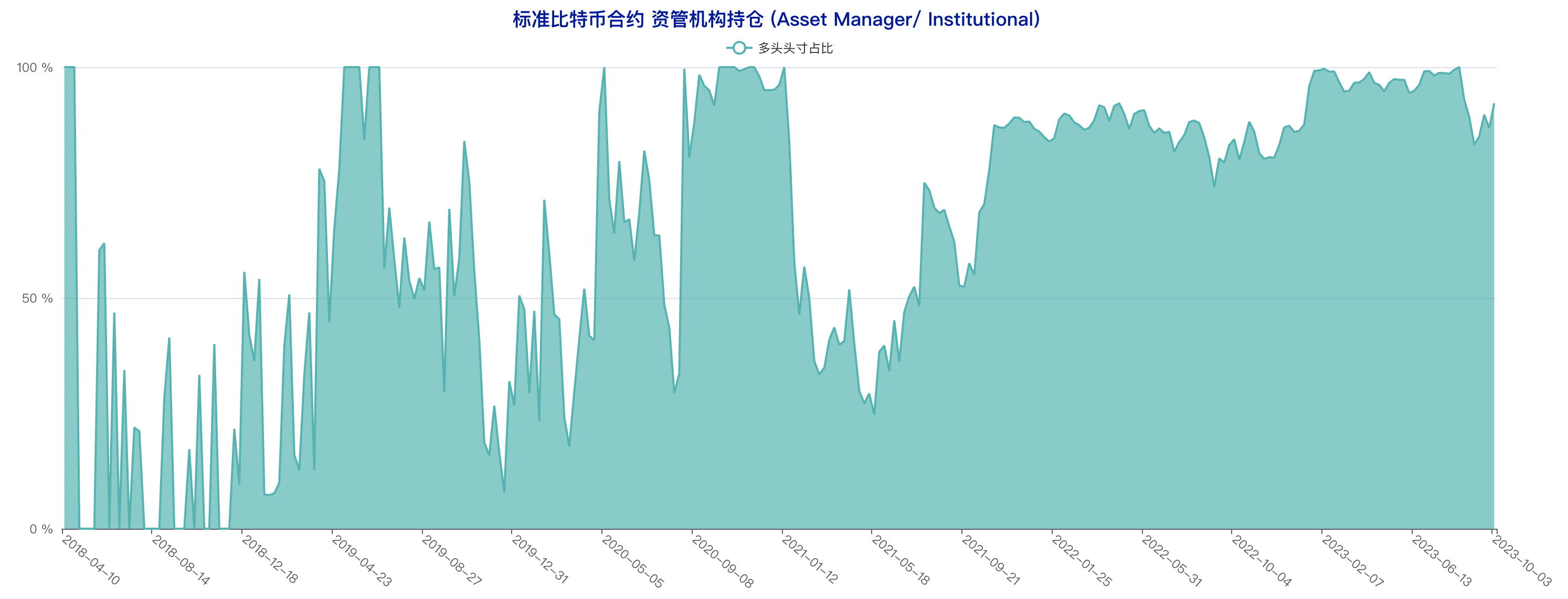

The long positions of asset management institutions increased from 7168 to 7336, and the short positions decreased from 1093 to 623. The asset management institutions conducted clear net long operations in the latest statistical period, and the idea of net cold storage in the previous statistical period was abandoned. Such accounts returned to the bullish situation of the earlier week. The repeated performance of such accounts in recent period shows that they lack clear judgment on the market outlook. The reference value of the net long attitude of asset management institutions is not high at present. After all, such accounts may "overturn" the judgment of the previous statistical period in the next statistical period.

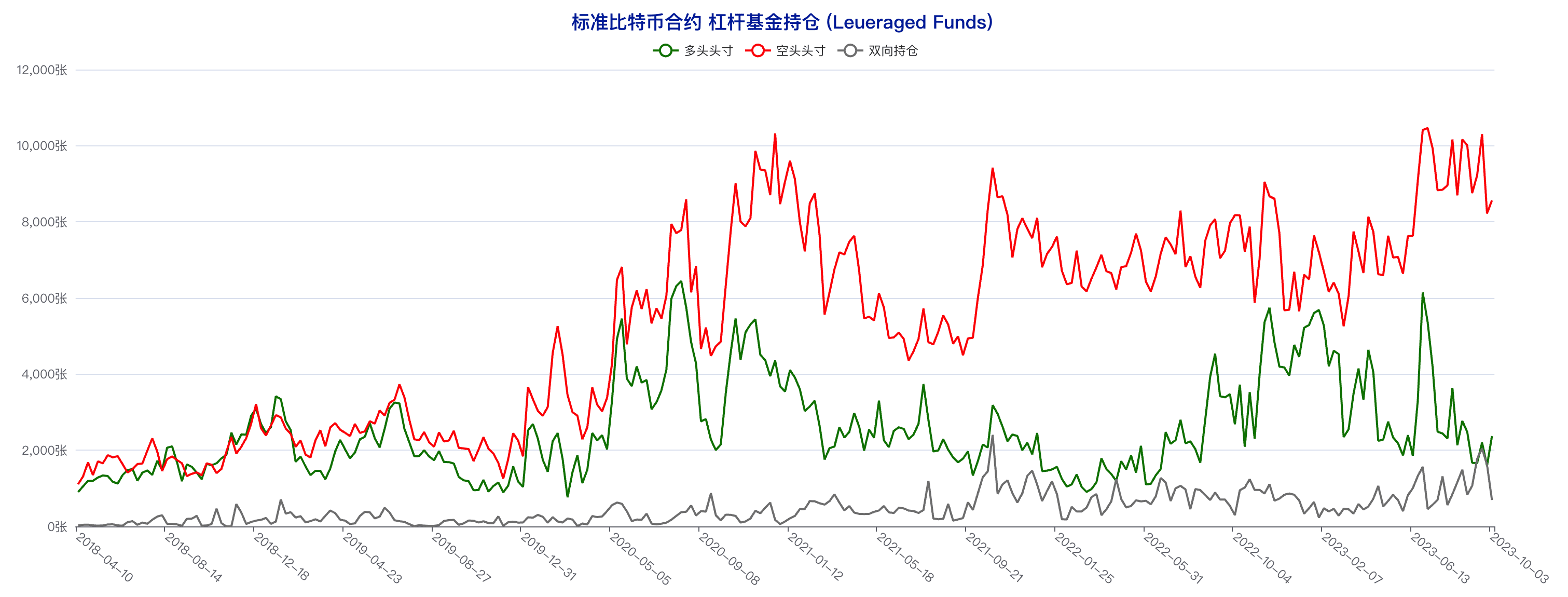

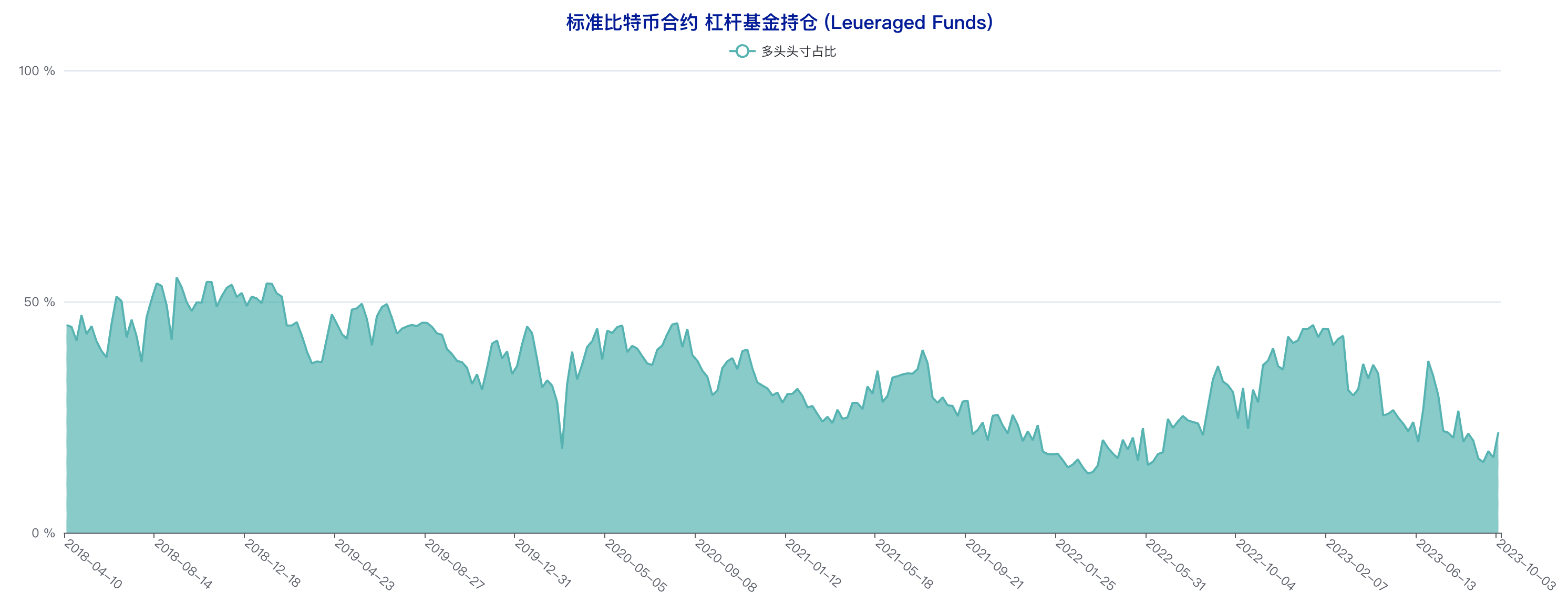

Leveraged fund long positions increased from 1594 to 2373, and short positions increased from 8220 to 8565. This type of accounts increased their long and short holdings simultaneously in the latest statistical period. However, it should be noted that after this round of same-direction adjustments, the proportion of long positions increased significantly and hit a nearly 8-week high. This type of accounts also expressed a bullish attitude in the latest statistical period, which is contrary to the judgment of the previous statistical period.

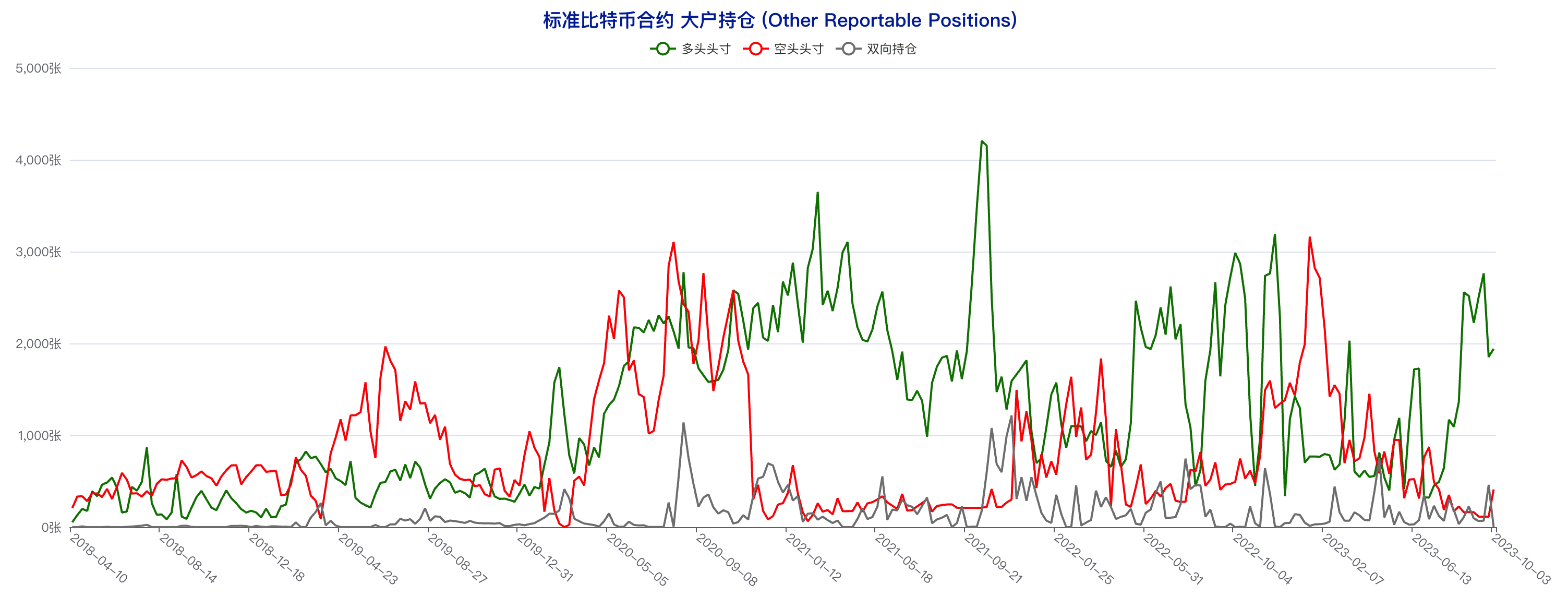

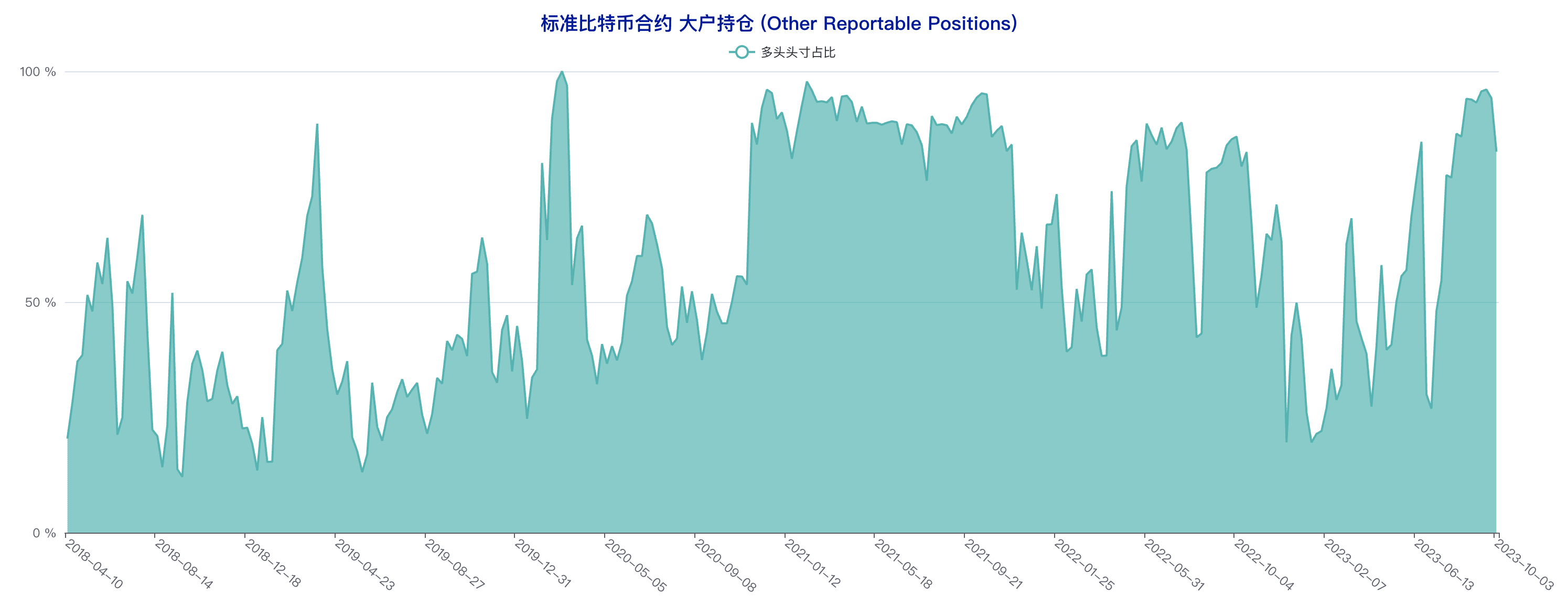

The long position of large accounts increased from 1852 to 1941, and the short position increased from 114 to 410. The trend of the value remaining unchanged for two weeks came to an end, and it directly matched the high point in the past 12 weeks, getting rid of the low point in the past three years. Although the proportion of long positions of large accounts remains relatively high, the overall adjustment of positions in the latest statistical period is short, which also continues the adjustment idea of such accounts in the previous statistical period.

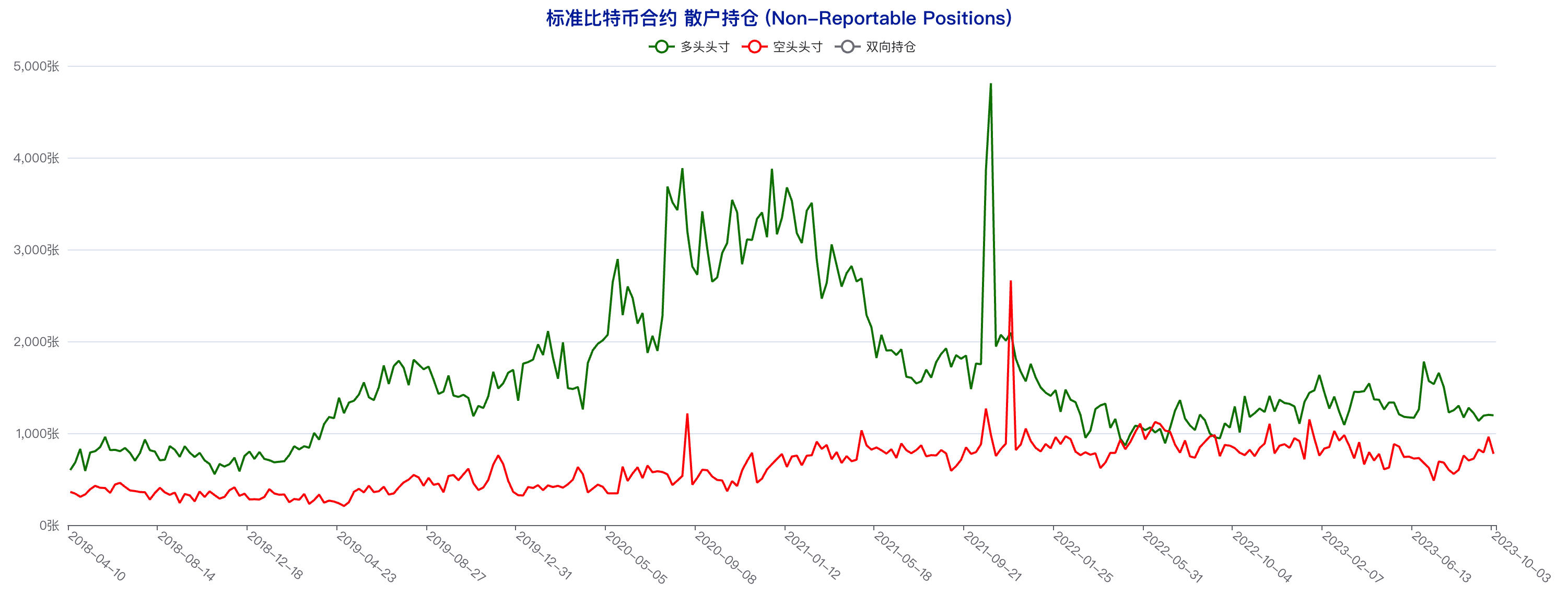

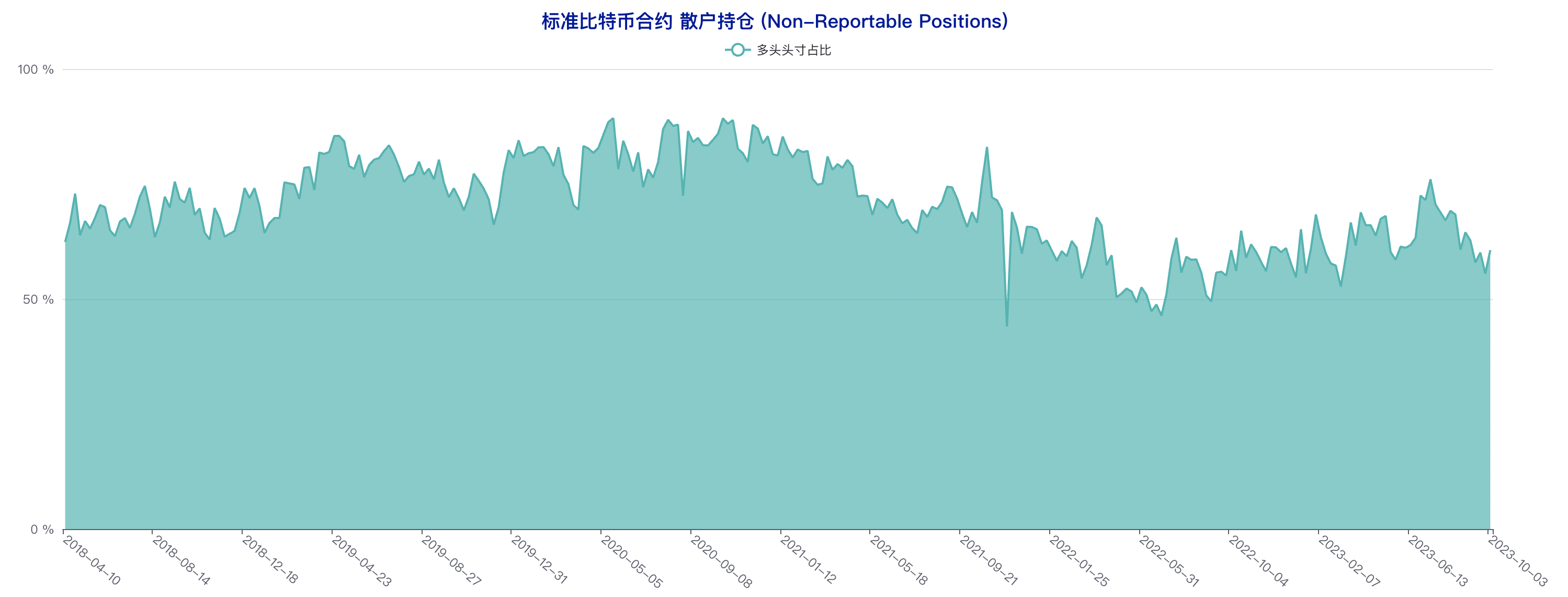

The retail investors’ long positions dropped from 1200 to 1195, and the short positions dropped from 961 to 776. The retail investors reduced their long and short positions simultaneously in the latest statistical period, and the proportion of long positions returned to the level of the earlier week. The retail investors’ long and short judgments also reversed in the latest statistical period, turning from the previous week’s bearish to the bullish side.

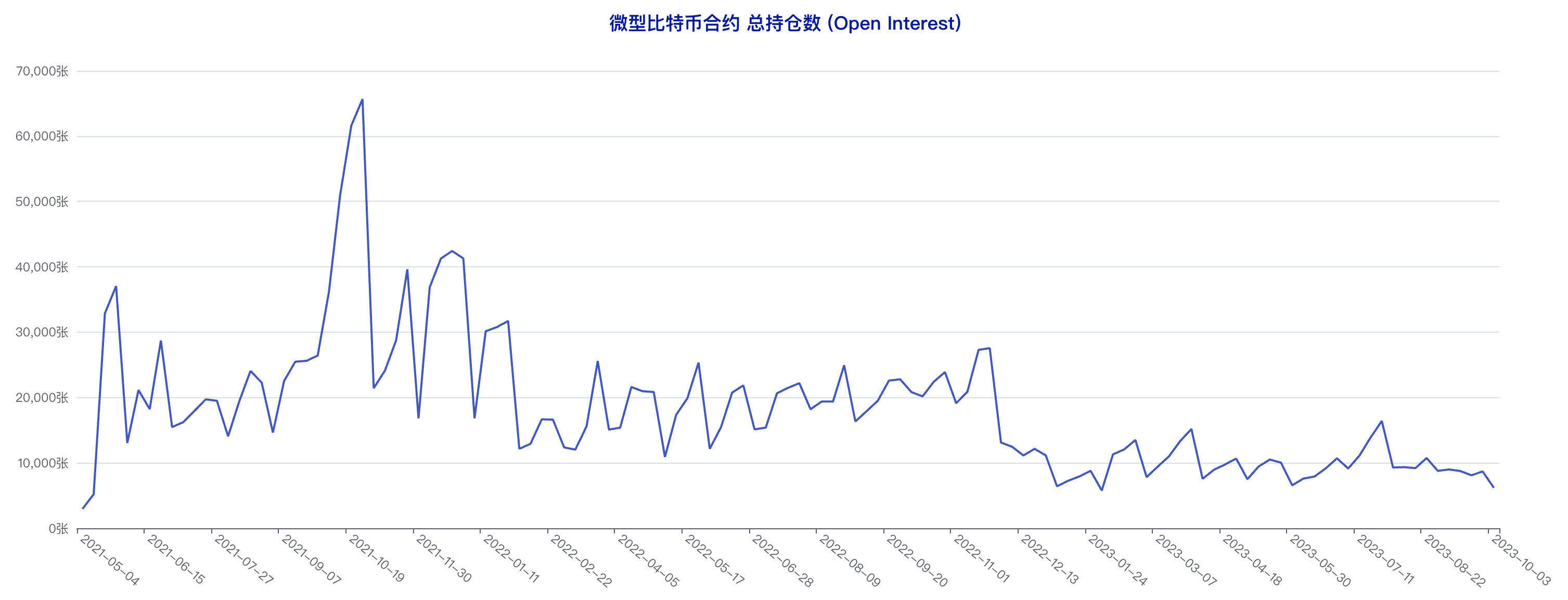

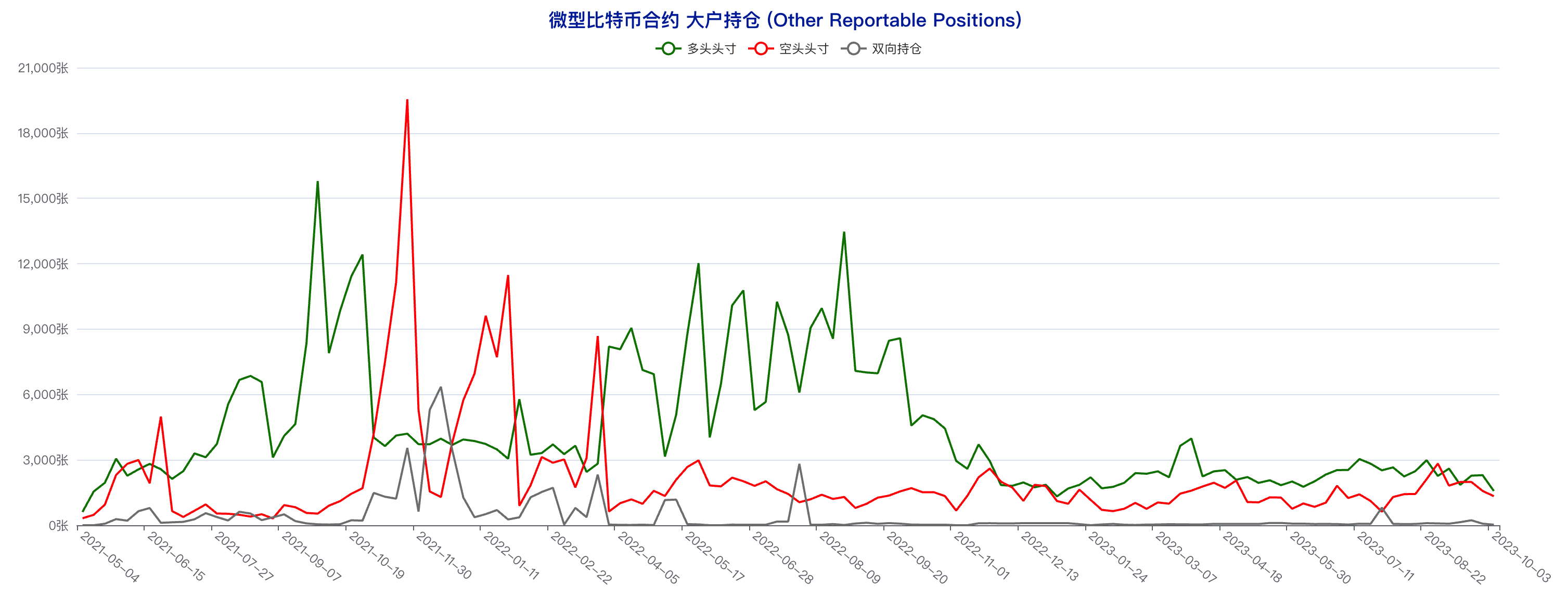

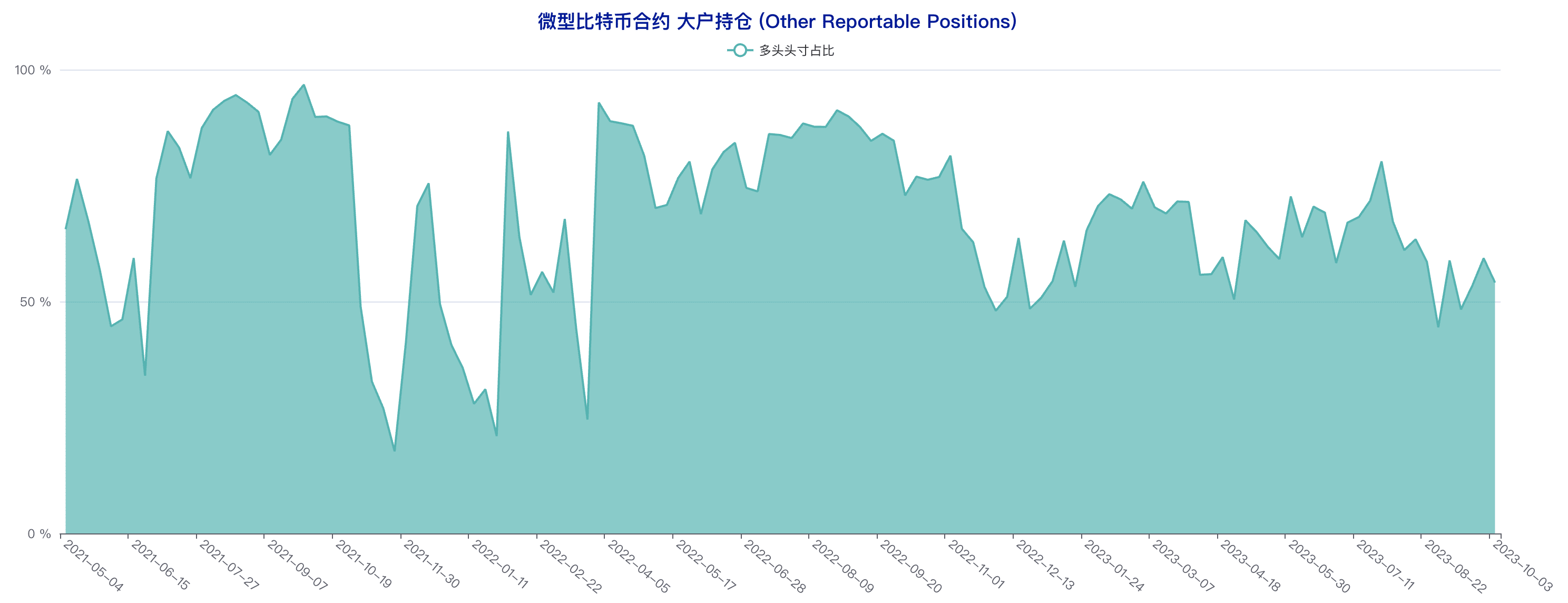

Total open interest in Bitcoin micro contracts fell from 8,690 to 6,193.

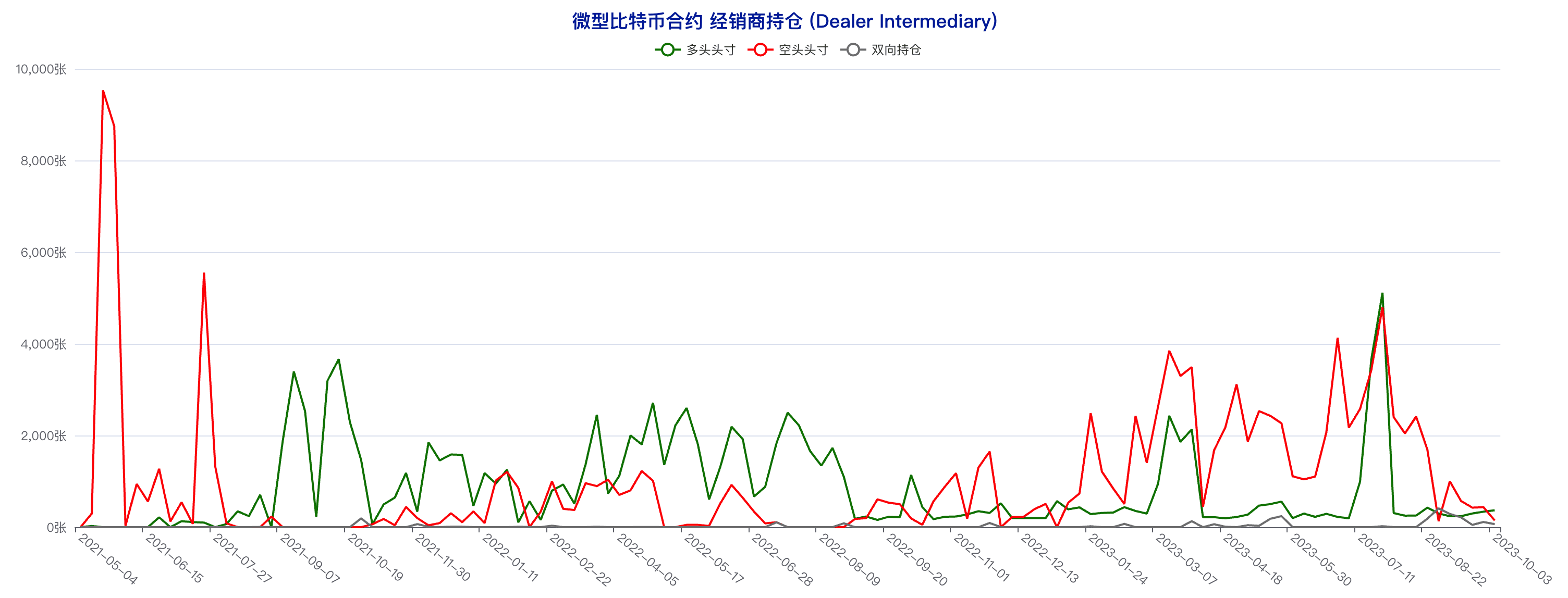

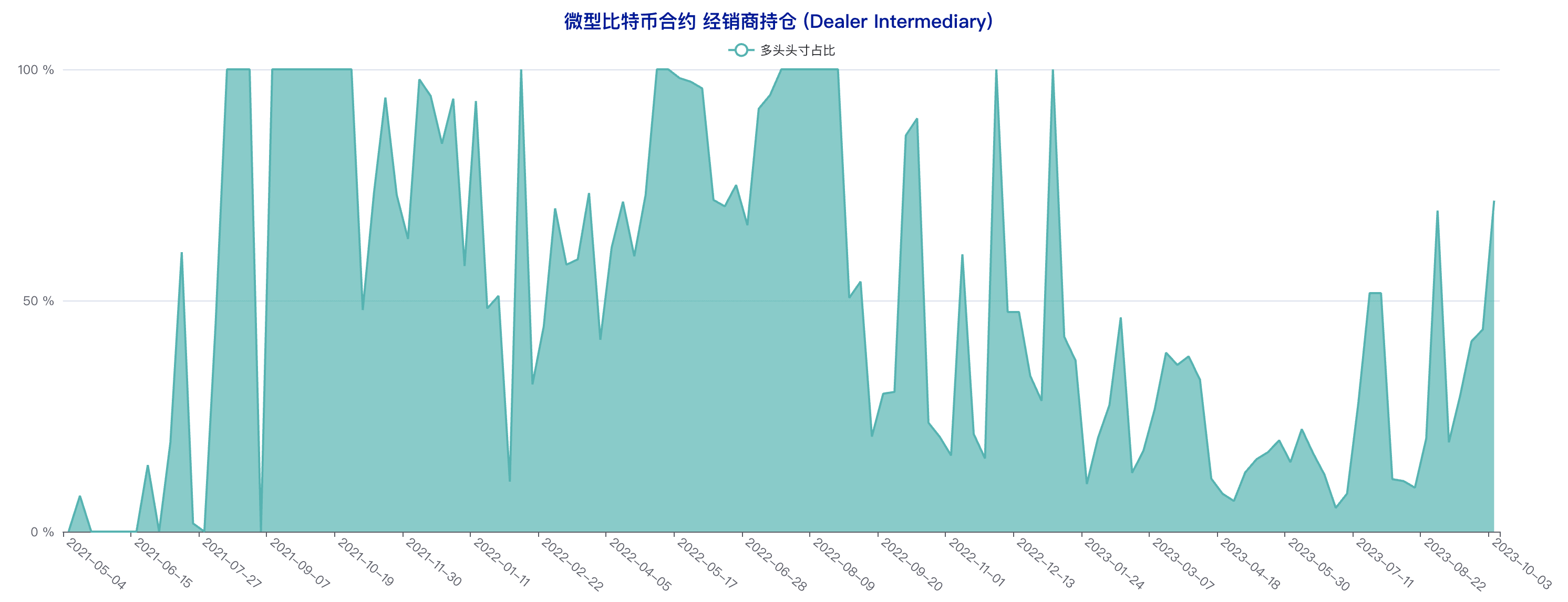

The dealer account’s long position increased from 338 to 368, and the short position decreased from 435 to 146. This type of account has made a net long adjustment in the micro contract, which is a classic risk hedging operation.

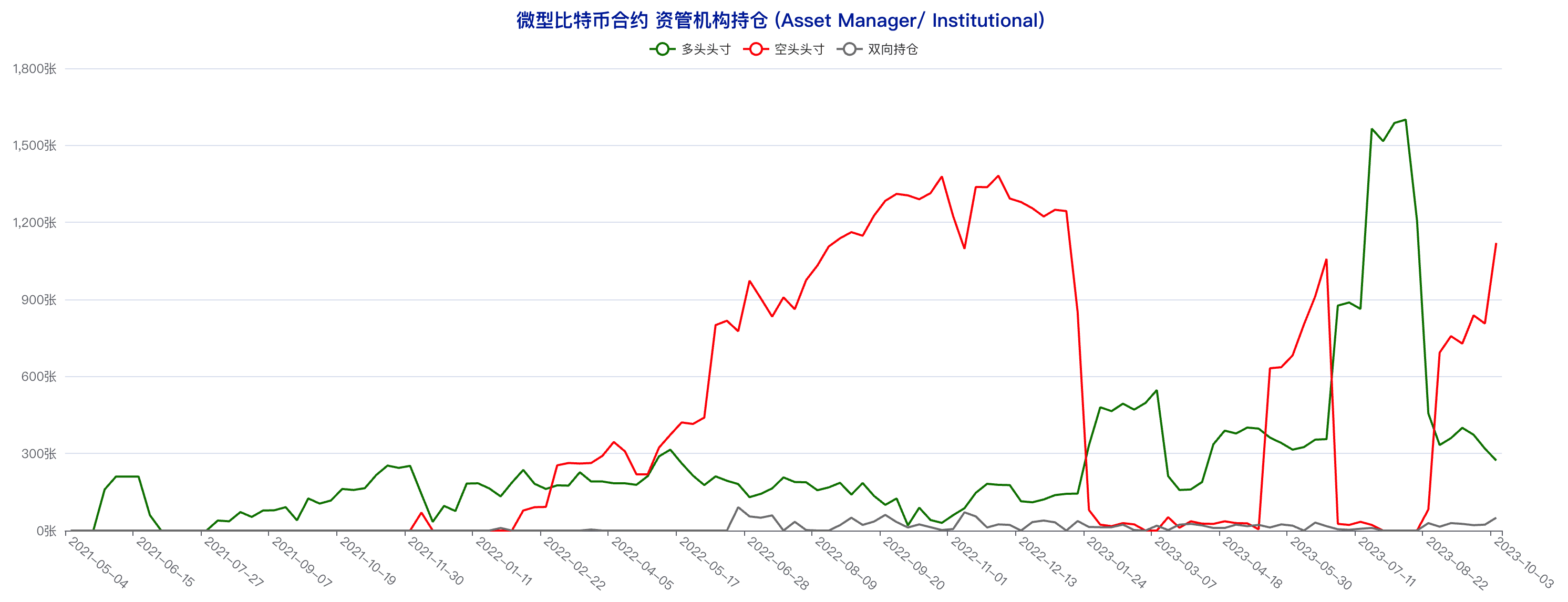

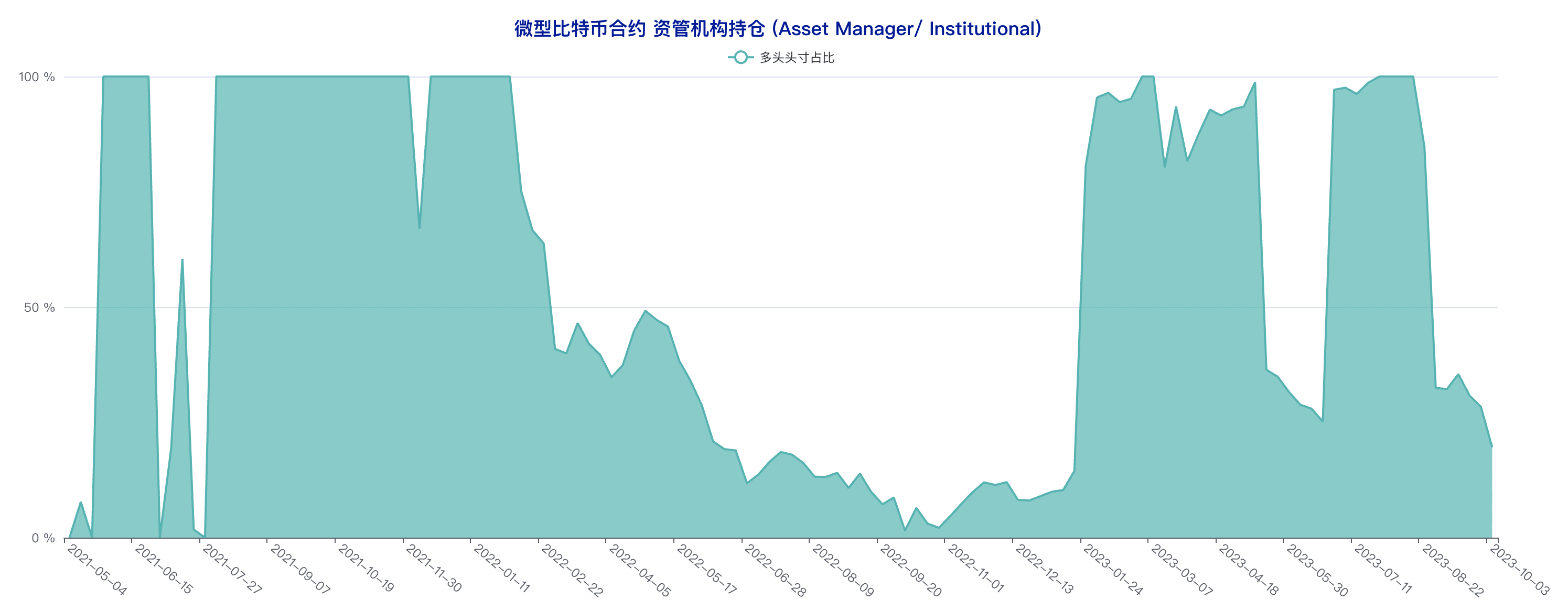

The long position of the asset management institution account decreased from 319 to 273, and the short position increased from 806 to 1120. The asset management institution conducted a net cold position adjustment in the micro contract, which is also a risk hedging operation when combined with the standard contract position adjustment.

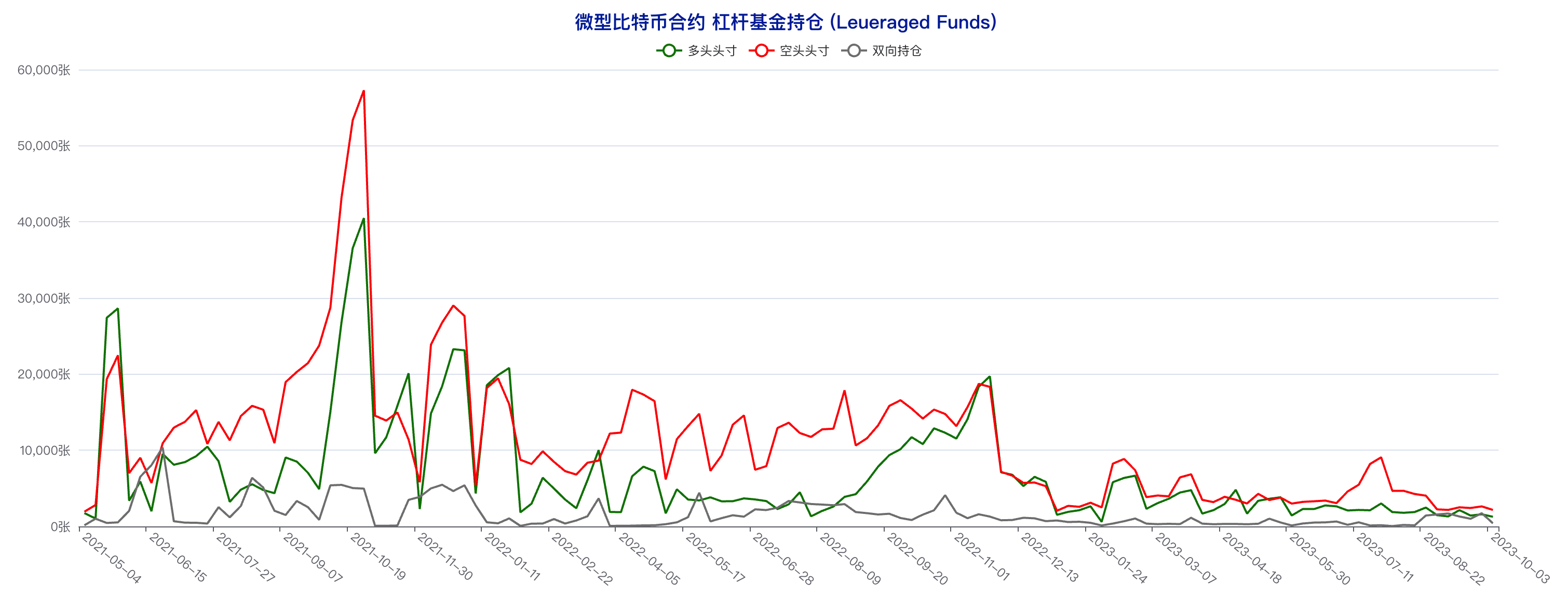

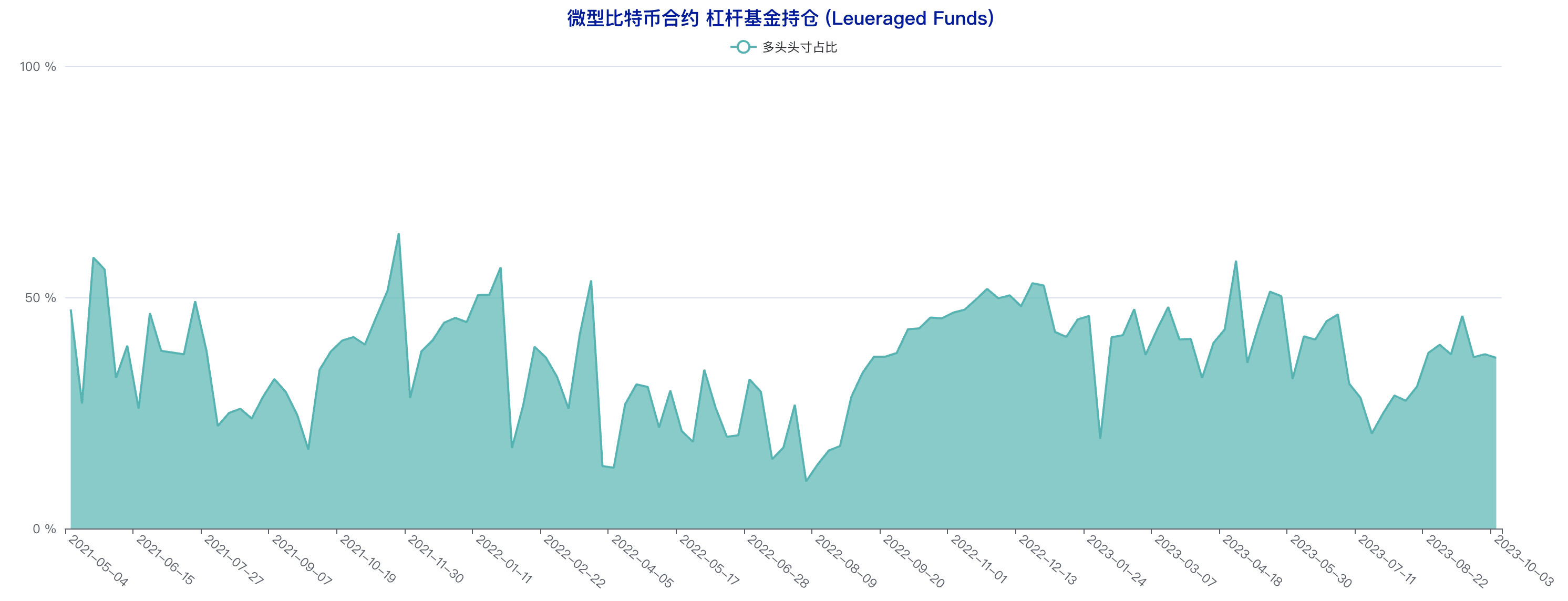

The long position of leveraged funds decreased from 1590 to 1266, and the short position decreased from 2629 to 2163. Leveraged funds reduced their long and short positions simultaneously in the latest statistical period, and the long and short positions remained unchanged. The overall position adjustment of this type of accounts in micro contracts has remained stable in recent times, with a lack of changes and directional preferences.

Large investors’ long positions dropped from 2296 to 1570, and short positions dropped from 1574 to 1333. These accounts reduced their long and short positions simultaneously during the latest statistical period, and the proportion of long positions decreased, slightly consolidating the bearish attitude expressed by these accounts in the standard contracts.

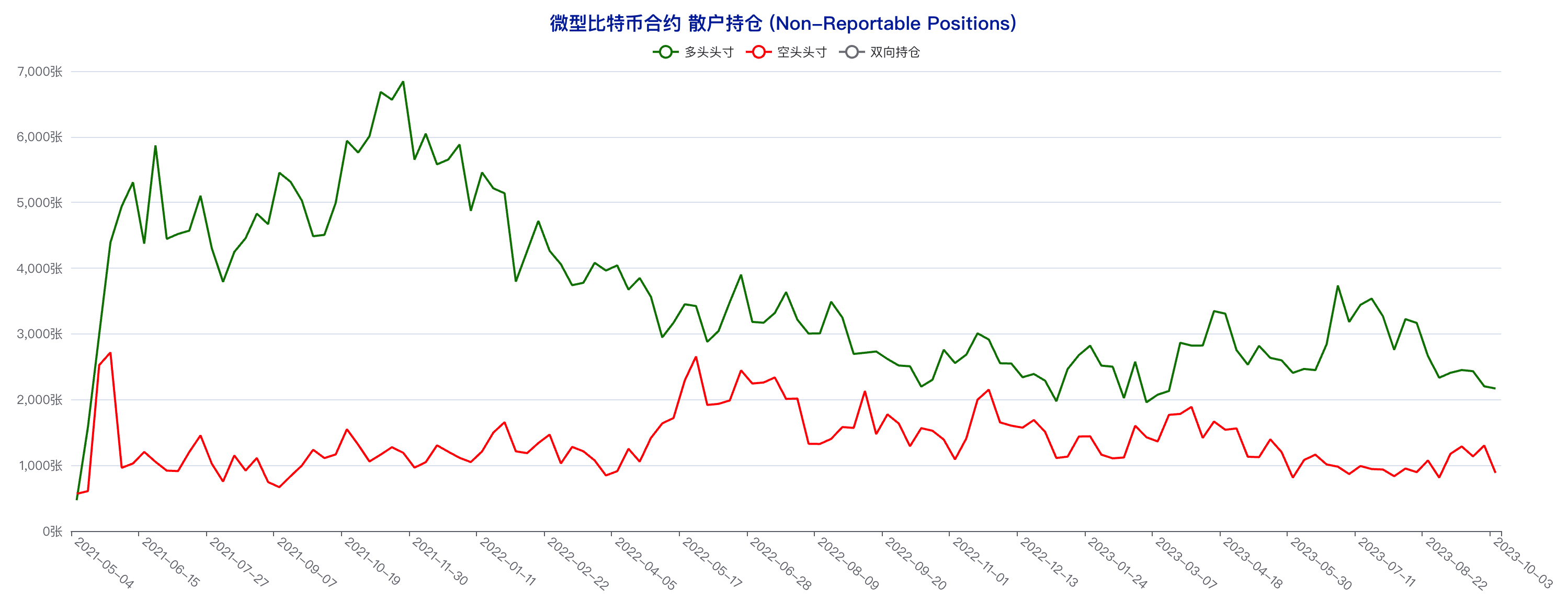

Retail long positions fell from 2202 to 2169, and short positions fell from 1301 to 884.