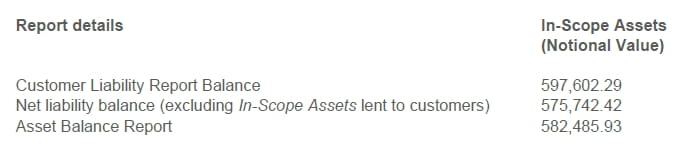

Last week, cryptocurrency holders were concerned that Binance would follow in the footsteps of FTX’s insolvency. The Binance farce originated from a 5-page reserve audit report released by financial audit firm Mazars. The report only audited Binance BTC on selected chains. On the audit date (November 22), a total of 582,486 BTC in assets and 597,602 BTC in customer liabilities were held.

The Mazer audit report has a strict and narrow definition, and after adjustment, it concluded that Binance's BTC assets are safe. But then it raised a wider range of questions: including the method of adjusting the audited BTC assets and liabilities, why only Bitcoin, whether Binance has "liabilities" connected from other chains, whether Binance has over-issued collateral exceeding its underlying assets, etc. Users want to see a comprehensive audit report, but the audit report only audited BTC assets.

The Mazer audit report has a strict and narrow definition, and after adjustment, it concluded that Binance's BTC assets are safe. But then it raised a wider range of questions: including the method of adjusting the audited BTC assets and liabilities, why only Bitcoin, whether Binance has "liabilities" connected from other chains, whether Binance has over-issued collateral exceeding its underlying assets, etc. Users want to see a comprehensive audit report, but the audit report only audited BTC assets.

Mazars’ report at least transparently disclosed some of Binance’s liabilities, which is better than most proof of reserves. But because it ignored all non-BTC assets, it could not fully prove Binance’s financial situation. The audit only proved a small part of Binance’s reserves, not a comprehensive view. But the storm led Mazars to announce that it would stop auditing Binance and its other cryptocurrency clients.

Binance has seen massive outflows worth billions of dollars in the past week, with $4.27 billion withdrawn on December 14 alone. This was partly due to on-chain data from well-known TradFi players such as Jump and Wintermute withdrawing funds from Binance on the 12th. Due to withdrawals and price fluctuations, assets held by Binance fell from $69.5 billion to $54.7 billion;

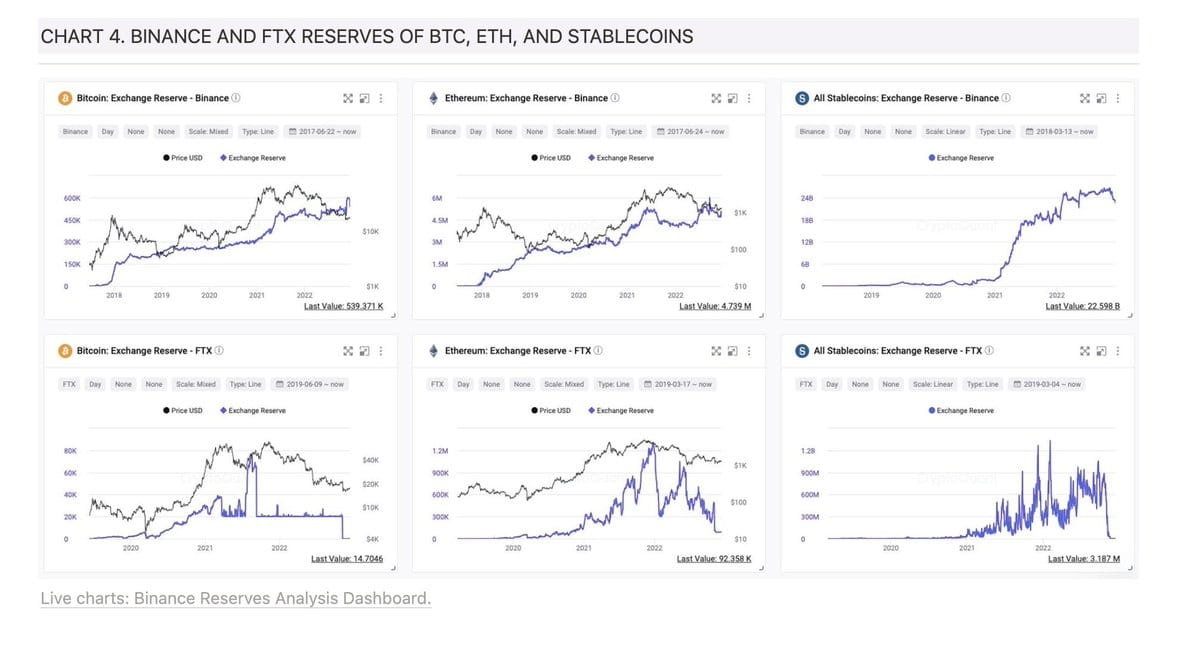

If anything like FTX’s case, Binance will show a drain on its ETH and stablecoin asset outflows to near zero. While there has been a large outflow due to users wanting to avoid any FTX 2.0 opportunities, on-chain data shows that Binance’s stablecoin and ETH reserves are still ~22B and ~5M respectively.

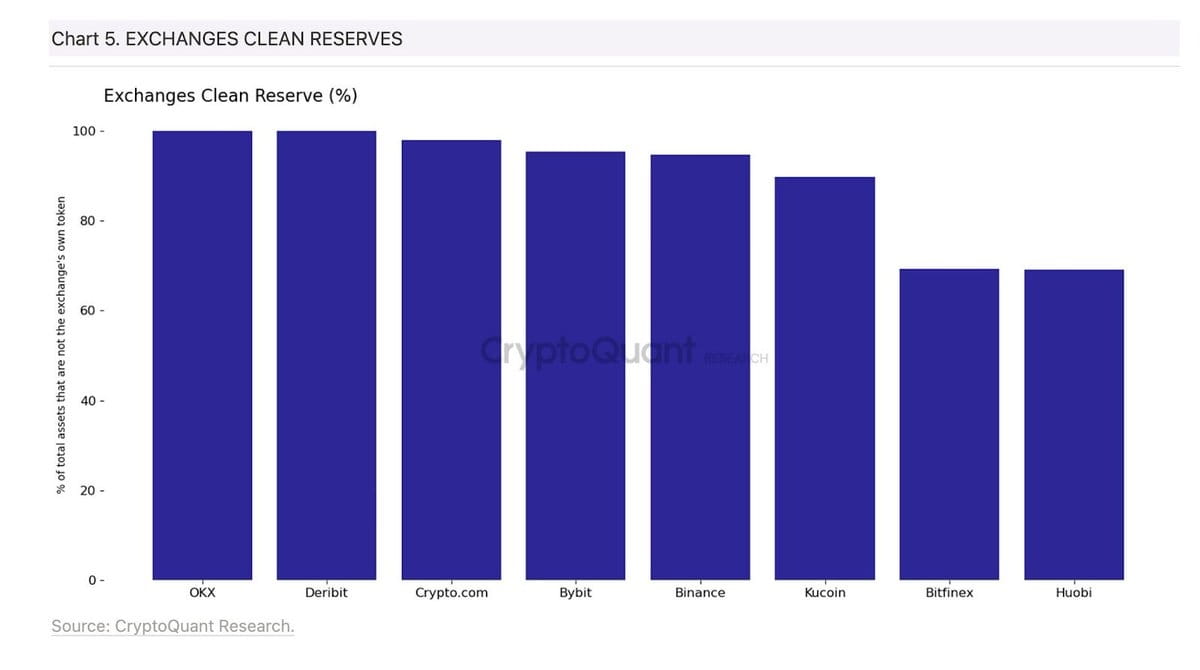

A big reason FTX ran into trouble was also due to the use of its own FTT token for collateralized lending. If Binance’s business was similarly built on its own BNB token, we might have more concerns. Thankfully, only about 10% of Binance’s reserves are made up of BNB, which is roughly the same as most other cryptocurrency exchanges.

BNB also functions differently from FTT. FTT is used for trading discounts on FTX, but if the exchange is about to go bankrupt, FTT will go to zero. BNB is the asset used for verification and payment of transaction fees on the second largest L1BNB Chain by TVL today. The price of BNB plummeted on December 17, but has since rebounded back to around 250.

On-chain indicators all indicate that although Binance is experiencing a degree of "bank run" (although inappropriate), the situation is not as dangerous as imagined. If it is completely 1:1 anchored and holds customer deposits (unlike FTX), then there is no risk even if every user wants to take their money out, just like @heyibinance said, free in and free out.

There will always be problems, risks and doubts about CEX. These problems include that users will always question the ethics of centralized exchanges when facing huge amounts of funds. How centralized exchanges CEX can prove their innocence and build user confidence is an eternal research topic. In addition to having a transparent operating mechanism, centralized exchanges still need to embrace supervision and self-discipline for long-term development. Users must learn to make their own balanced choices between CEX and DEX.

The article references Donovan Choy, the author of Bankless, "Should we be worried about Binance?"