A recent court document revealed details of the cryptocurrencies held by FTX. The document outlines the large payments made to senior executives, including its founder Sam Bankman-Fried (SBF), before the company filed for bankruptcy protection in November, as well as an assessment of the value of various assets currently held by FTX. The value of the cryptocurrencies held by FTX is critical to FTX's creditors, but it can be seen from the documents that the value of some of the cryptocurrencies held by FTX is difficult to value. Elven, as a professional crypto asset accounting platform in the industry, has given some interpretations from the court documents, which will start from the FTX case and provide important information that will help investors and crypto companies:

How much crypto assets does FTX hold?

How does liquidity affect the valuation of crypto assets?

How are pre-ICO tokens valued?

How much crypto assets does FTX hold?

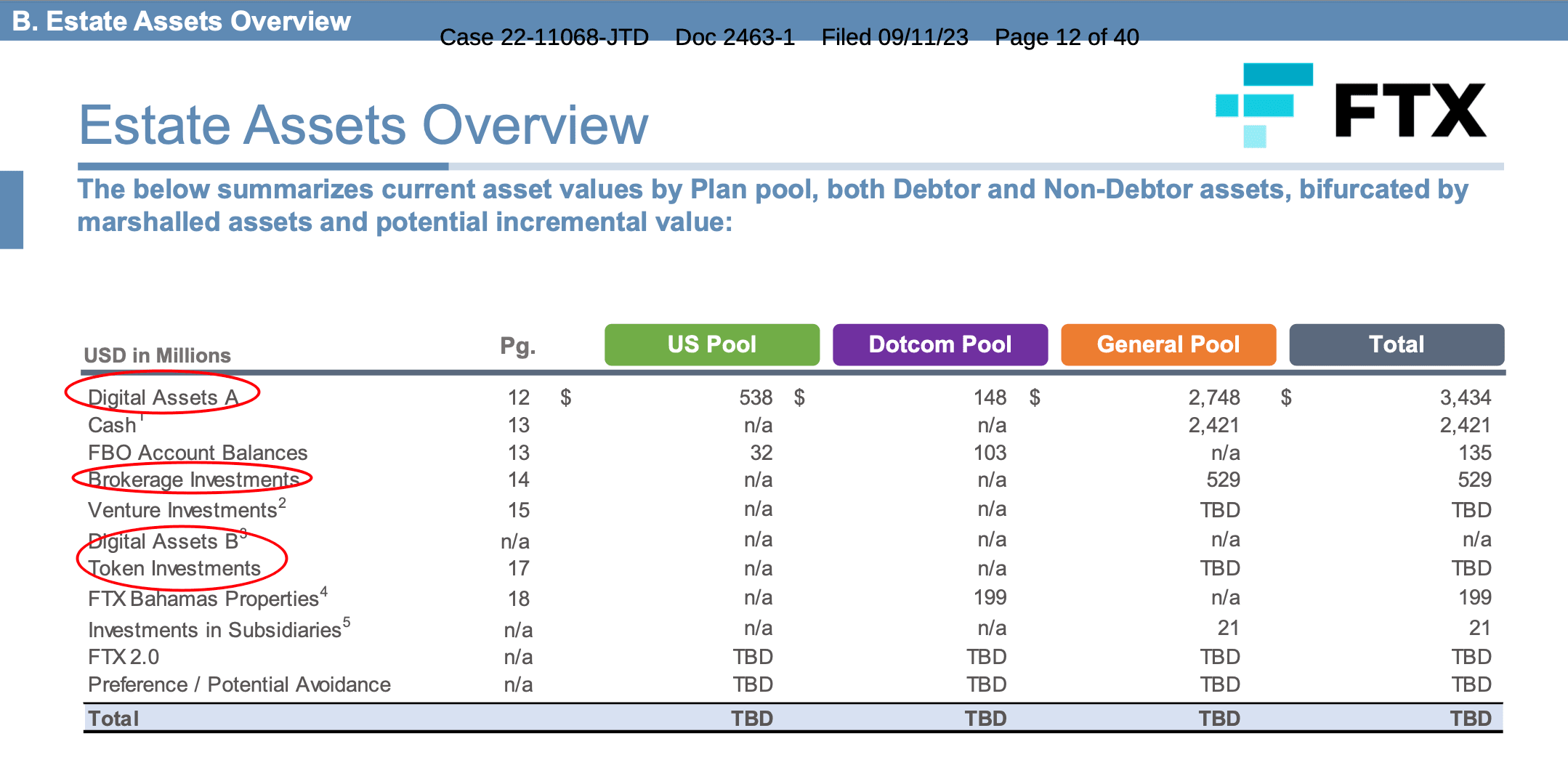

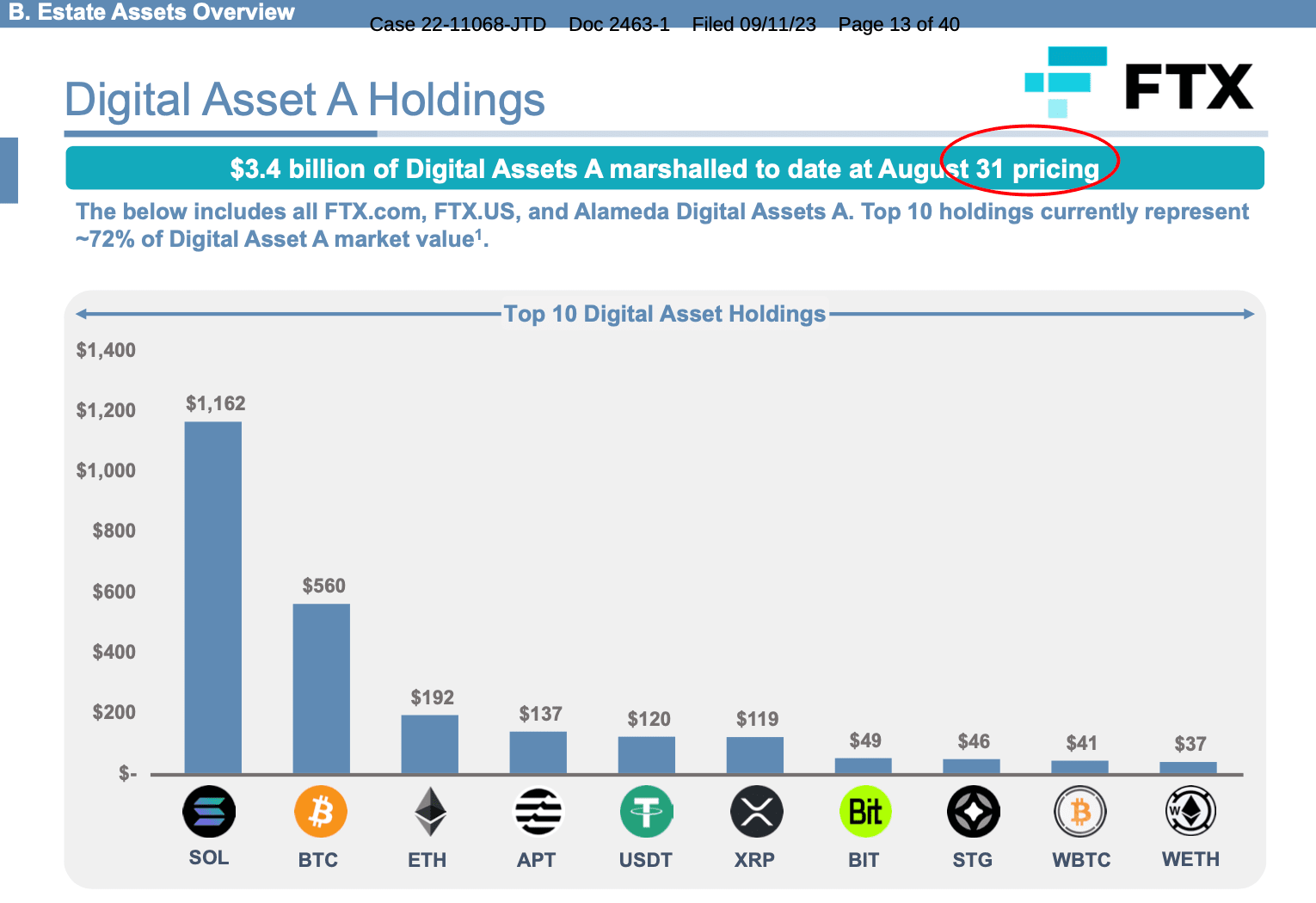

As of August 31, FTX held a total of $3.4 billion in crypto assets, mainly including $1.16 billion in SOL, $560 million in BTC, $192 million in ETH, $137 million in APT, $120 million in USDT, $119 million in XRP, $49 million in BIT, $46 million in STG, $41 million in WBTC and $37 million in WETH. In addition, FTX also holds other tokens with poor liquidity and venture capital with tokens as investment funds.

The chart shows that only "Digital Asset A" and "Brokerage Investment" list accurate valuations. The valuations of "Digital Asset B" and "Token Investment" need to be determined due to their illiquidity. For "Digital Asset A", the valuation is based on the price on August 31. This introduces a key method used to value crypto assets: fair value measurement. What is fair value measurement? According to ASC820-10-20 definition. Fair value is "the price that would be received to sell an asset or transfer a liability in an orderly transaction between market participants on the measurement date." In the new accounting standards update proposed by the FASB, fair value measurement will replace the impairment method for crypto assets. Crypto assets will be listed separately in the balance worksheet and measured at fair value, with changes in fair value included in net income. At the same time, holders of certain types of crypto assets must disclose their holdings in annual and interim financial reports. For example, if you buy 1 Bitcoin at $20,000 on the first day and it drops to $15,000 on the second day, you must record a loss of $5,000. If you increase the price to $25,000 on the third day, you still need to record a $5,000 loss under the impairment method. However, with fair value measurement, you will record a $10,000 gain on the third day. 💡Elven Interpretation The valuation of crypto assets will be more accurately reflected under fair value measurement. If FTX uses the impairment method to evaluate, the valuation of crypto assets will be much lower than the current results. The chart shows the difference in valuation between FTX's impairment method and fair value method.

How liquidity affects the valuation of crypto assets

How liquidity affects the valuation of crypto assets

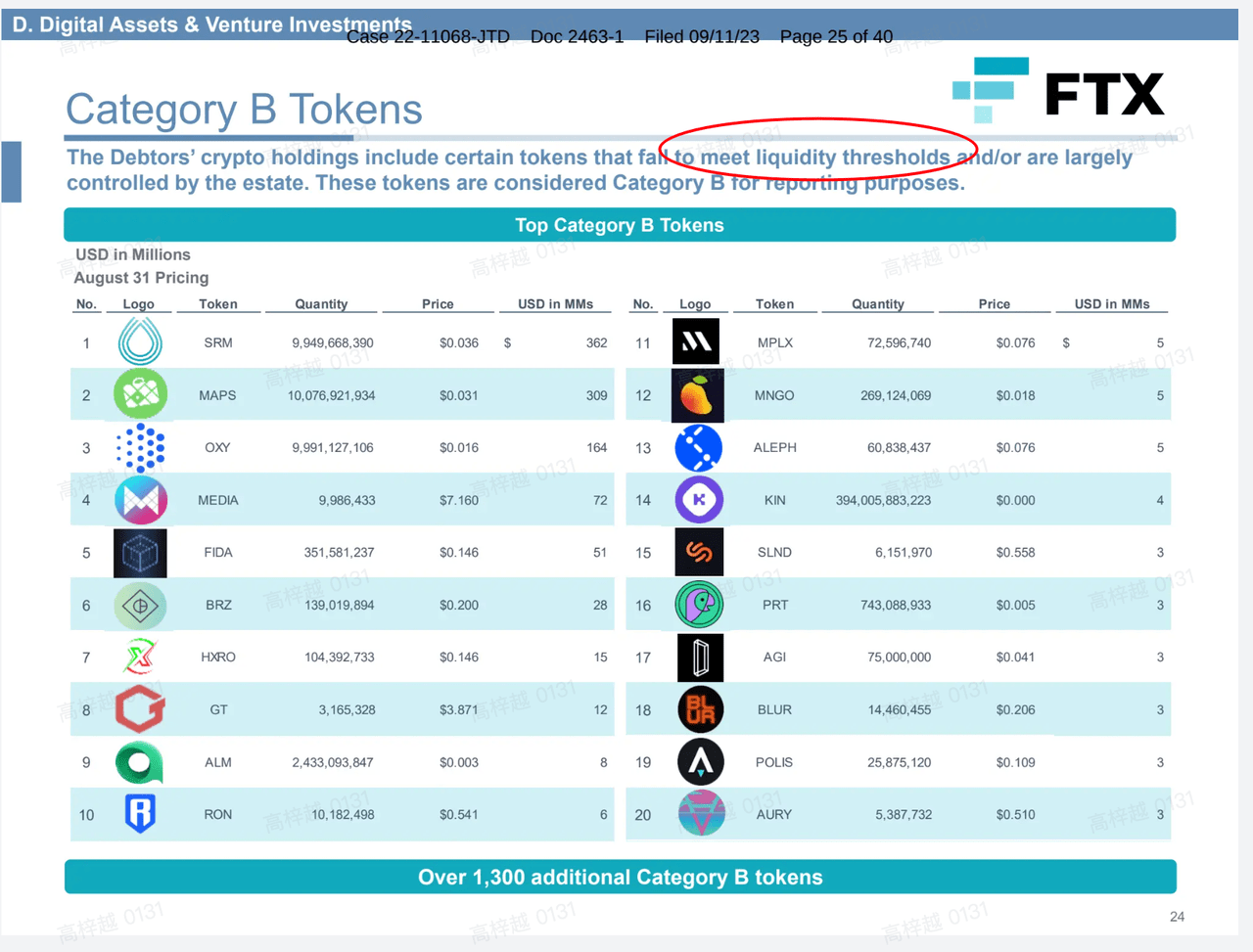

The second key point in the overview is that crypto assets have been divided into “Type A” and “Type B” based on specific liquidity thresholds.

Let’s use Uniswap as another example. When a user wants to trade the first two “Class B Tokens”, a warning is sent to indicate liquidity and false valuation risks. To show the impact of liquidity on asset trading.

💡Elven Interpretation It is important to consider liquidity. Although the liquidity standard is not clearly expressed in the FTX document, we can see that there is a three-level fair value hierarchy according to ASC820-10-35-37:

Level 1: Observable inputs that reflect quoted prices in active markets for identical assets or liabilities

Level 2: Inputs for the asset or liability that are observable, directly or indirectly, other than quoted prices included in Level 1

Level 3: Unobservable Inputs

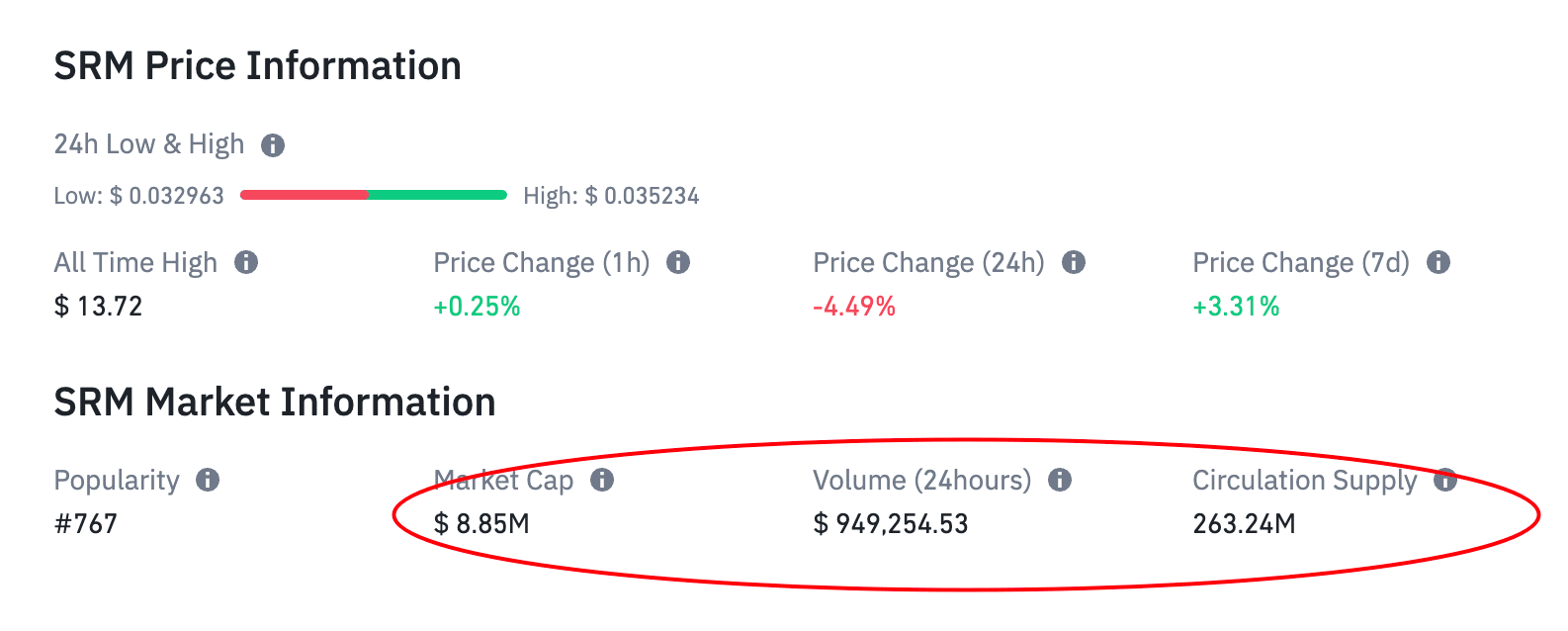

ASC820 prioritizes observable data from active markets, placing measurements that use only these inputs at the highest level of the fair value hierarchy (Level 1). Therefore, the key variable is the existence of an active market. According to the definition of ASC820-10-20, an active market is one in which transactions for an asset or liability occur with sufficient frequency and volume to provide pricing information on an ongoing basis. For scenarios like the FTX case, we recommend referring to market trading volume and the corresponding token holdings. For example, the SRM token has a 24-hour trading volume of about 10% of the market capitalization. It looks like the token is actively traded. However, the current circulating supply of SRM is much less than FTX's holdings, which means that the market's daily trading volume is about 0.2% of FTX's holdings! This problem is called 'clogging' in accounting. It can be described as a specific type of liquidity discount associated with large holders of a particular asset.

We can define "blocking rate" as the ratio of token holdings to the circulating supply in the market. A larger blocking rate reflects holdings that cannot be absorbed by the market at the current value. Different discount levels can be set for different blocking rates to ensure that the fiat assets obtained when the corresponding assets are actually disposed of are close to the estimated value.

How to value pre-ICO tokens

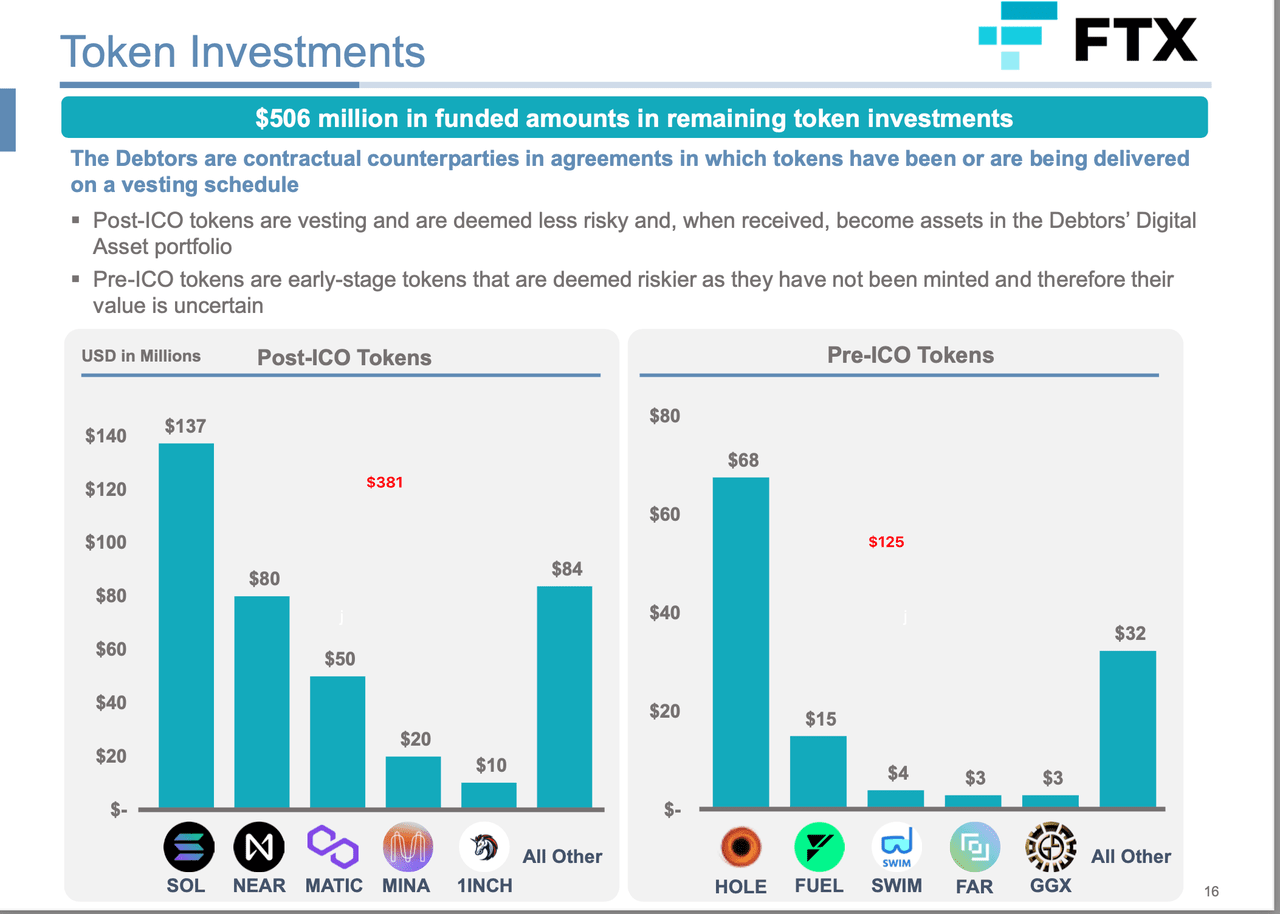

The third key point is token investment, which mentions that ‘the cost basis of $506 million should not be used as an estimate of recoverable value’, which introduces another important concept: cost basis.

What is cost basis? Why is it important? Cost basis refers to the initial purchase price when you acquire a crypto asset. For example, if you purchased one Bitcoin for 20,000USD on day one, your cost basis would be set to 20,000USD. Cost basis forms the basis for calculating profit or loss. The calculation follows a simple formula: Cost Basis - Selling Price (Fair Value) = Gain/Loss Although it is relatively simple to record the cost basis of a specific token, it becomes complicated when users have to manage different cost tranches on different platforms (such as buying multiple different tokens). When users decide to sell your crypto assets, it can become challenging to determine which cost basis to apply to calculate the gain or loss. Selecting one tranche may result in a gain, while another may result in a loss. In the case of FTX, token investments are divided into post-ICO and pre-ICO. Let's take the HOLE token as an example. FTX invested $68 million for a given share of the token, so $68 million is the cost basis of the FTX HOLE token. However, the fair value (i.e., "recoverable value") of the HOLE tokens owned may be much less than $68 million because it lacks liquidity. 💡Elven Interpretation Since there is no available market data to serve as a relevant quote for pre-ICO tokens. In this case, valuation based on future cash/token revenue will be a possible approach. The revenue valuation method has three key elements:

Future income estimates: Estimated cash flows generated over the life of a cryptoasset

Income Generation Period: How long can the token continue to generate income?

Discount rate: 1-the conversion rate of the present value of future cash flows

For example, in this report given by Henley & Partners, the intrinsic value of Ethereum is assessed using the revenue approach. Transaction fees and new token issuance over a 20-year period estimate future annual revenues. When the discount rate is 13%, the intrinsic value would be $2,725. On the other hand, if we use a discount rate of 19.19%, the implied price per ETH would be $1,349. Different assumptions will lead to huge differences in token valuations. RxR Research used the same approach in this article. As we can see, different estimates of the three key elements will greatly affect the revenue approach, especially when the ecosystem behind the token is not as strong as Ethereum.

Trust and Wrapped Tokens

Other valuable details in the report include:

Investments in Garysacle’s Bitcoin and Ethereum Trust are valued separately from “digital assets.”

Wrapped tokens are intended to be “unwrapped and converted into the underlying native tokens as far as possible.” Under the proposed ASU, wrapped tokens will not be within the scope of crypto assets. Therefore, they can only be measured at fair value after unwrapping.

Elven will closely monitor the financial details of the FTX case and continue to track the latest updates to crypto accounting standards. This Friday (09/29) from 5 to 7 pm, Elven will also work with well-known accounting firms in the industry to provide a professional interpretation of FTX's latest developments. At that time, we will conduct a more in-depth discussion based on this article. Readers are welcome to scan the QR code to join our offline activities and online live broadcasts!

About ElvenElven (www.elven.com) is a professional digital asset financial management software. Elven provides one-stop financial solutions for project parties, exchanges, OTC, DAO, etc., and provides financial management platform, financial consulting and auditing, asset certification and other services, and is committed to making on-chain finance clearer and more worry-free.