2022 is gradually coming to an end, the sky is shrouded in haze, the mud and sand are all mixed together, and the naked swimmers are clearly visible.

In the gaming track, in the cold winter, both capital and people are voting with their feet, moving towards sub-tracks and projects that have a solid demand foundation and can deliver products.

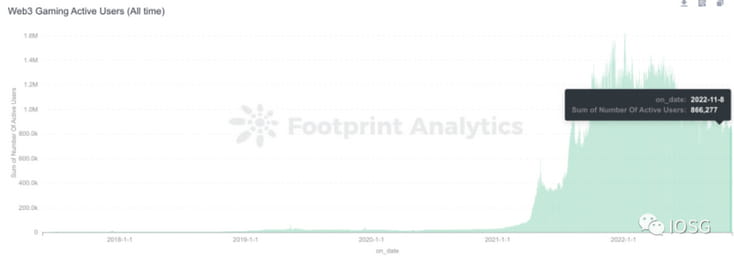

User number

Let’s first look at the user trend of web3 games. It is worth noting that different projects have different degrees of on-chain, different modules that interact with smart contracts, and different projects have different tolerance for multi-account freeloaders. The number of users obtained through on-chain data can only be used as a reference.

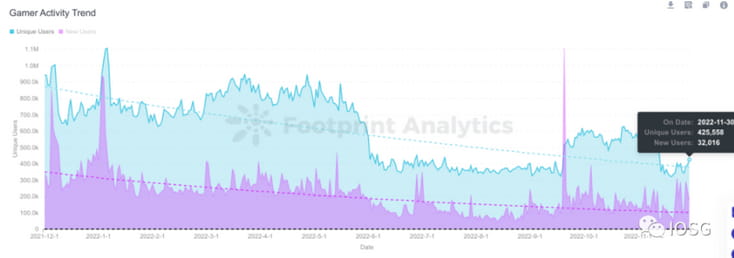

Total active wallets:

Number of deduplicated wallets:

In terms of the overall number of users, the number of wallet addresses is around 800,000, but the number of independent wallets is only about 400,000.

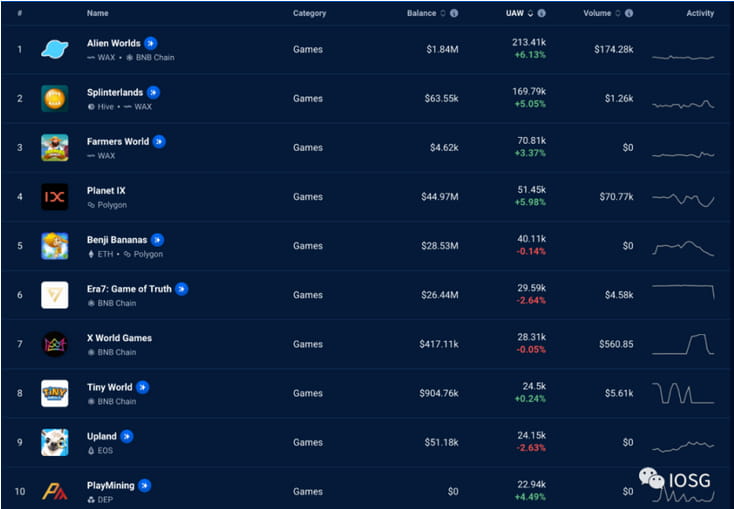

From the perspective of active address projects on the chain, Alien World & Splinterland account for about 50% of the number of addresses, and the active level is about 200,000. However, compared with the recent popular games such as Beacon, the number of real active players is about 6,000. Gamefi's player portrait is still mainly multi-account wool party or multi-account wool party\scientist. It is difficult to draw a directional conclusion from the horizontal comparison of data, so this article intends to change the idea and see which track is relatively favored by talents and capital.

This article sorts out and compares the financing trends and talent flows of web3 games in Q3 2022. In this cold winter, how are capital and talent choosing? (Financing data source: messari funding data, filters: gaming)

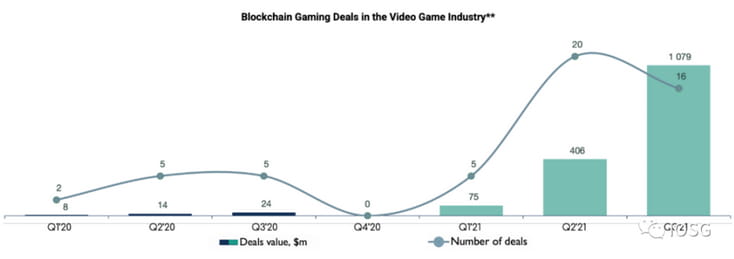

Blockchain Gaming Funding in Q3 2021

Before sorting out the financing trends in Q3 2022, we can first compare it with the situation in the same quarter of 2021. In the same period last year, web3 gaming financing was very hot, with a total financing amount of 1 billion US dollars in 22 projects, while the total financing amount in Q1-Q2 was only 1.5 billion. The total financing amount in Q3 increased by 3,400% year-on-year, and the number of financing projects increased by 400% year-on-year.

In terms of financing volume, most projects are concentrated in the seed round (~55%), and the deal size is relatively small (~3m/deal). The financing amount of the seed round accounts for 4% of the total financing amount in 2021 Q1-Q3.

Investors are willing to participate in projects through private token sales in the early stages, but overall, capital remains cautious about a new product form.

In terms of financing amount, 70% of the amount came from 11 projects in Series A/B, of which the most famous were Sorare's $728 (series A+B), Forte's $185m (series A), Mythical Games' $75m (series B), and Immutable's $60m (series B). Other series B projects that received much attention included Animoca Brand's ~140m financing.

Overall, in Q3 2021, platform and infrastructure projects have gained the favor of capital, and they are considered to be the cornerstone of future blockchain games. Game studios and pure game projects have also received some attention as a whole, but the overall deal size is much smaller.

Because game projects have a long development cycle and their business models have yet to be verified, infrastructure platform picks and shovels projects received a steady stream of funding last year. But from another perspective, if everyone is selling shovels, no one will actually dig for gold.

Therefore, at the end of 2021 and the beginning of 2022, projects focusing on game content began to enter the industry's field of vision. Compared with the previous generation of GameFi projects, we began to see more traditional game practitioners in the resumes of entrepreneurial teams, and there are also teams transferred from traditional game studios. According to the project budget (which to some extent reflects the team's direction choice), it can be roughly divided into the following categories:

1) Developers with small budgets but big ambitions:

Rooniverse, Playmint, First Light Games, Blockstars, Village Studio, Genopets, Galaxy Fight Club, Crypto Raiders, Gallium Studios, Heroes of Mavia, Horizon Blockchain Games, Lucky Kat Studios, pixion etc.

The team portrait is a pure crypto native team, or from the other end - some medium and light game studios / traditional game practitioners who started businesses in the slowdown of web2 growth. They understand the industry they originally worked in, and deeply understand the workload of game development + web3 integration, so they will wisely choose relatively simple propositions, tend to create some small and beautiful NFT games, mostly hypercasual categories, with relatively low development costs.

For example, choose a pixel art style project portal fantasy

The advantage of this type of project is that the game product testing and development progress is ahead, and they can spare enough energy to polish the web3 part. Based on the current development progress, as far as the author's experience is concerned, the blockchain-related experience of this part of the project is the smoothest.

Although most web3 attributes remain at the level of "making some game assets into NFTs and adding a dual-token model", there are occasionally some eye-catching fusion innovations, such as using crypto to transfer value at low loss to create glass root esport's Fableborne:

2) 2A Budget Developer:

Laguna Games, Big Time Studios, Faraway, Azra Games, Metatheory, LavaLabs, Upland, Sipher, Illuvium, Gunzilla Games, Klang Games, Playful Studios, Iskra, Joyride Games, Gameplay Galaxy, etc.

In terms of team portrait, it is more of a team with both crypto and gaming capabilities. The core team has a certain background in medium and heavy games, and understands the pain points of the previous generation of GameFi, such as poor gameplay, unattractive graphics, and insufficient content support. Therefore, they began to get involved in some medium and heavy categories, focusing on improving the quality of games. Most of them are still in development.

These projects have better graphics and richer game content than the previous generation. During the past GameFi hype, this group of players who mastered the crypto game scripts continuously released art materials and conducted community/nft sales, which whetted the appetite of players and the market and gained considerable support.

However, when switching to the product development stage, many projects also find that the propositions they have chosen may be beyond the capabilities of the current team. Currently, only a few projects are delivering phased products on schedule.

3) AAA Budget Developers:

Mythical Games, Shrapnel, Star Atlas, Sky Mavis, Sorare, Yuga Labs, Dapper Labs, The Sandbox, Animoca Brands, Limit Break, Xterio

This group of developers usually have a background in web2 studios or have a record of successful web2 products, and are the darlings of capital. They aim high and usually follow the model of platform + content / infrastructure + content.

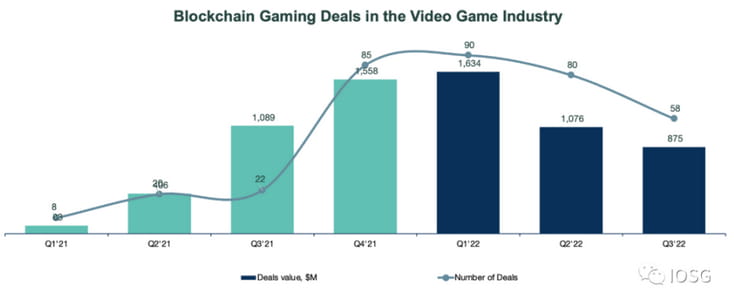

Blockchain Game Financing 2022 Q3 Bin Q3 2022

Blockchain Game Financing 2022 Q3 Bin Q3 2022

Looking back at Q3 of 2022, the financing situation has changed dramatically. Due to the macro-environmental issues, the financing amount of web3 gaming in Q3 showed a negative year-on-year growth for the first time. Although the overall financing volume in Q3 of 22 increased by 260% year-on-year (58 vs 22), the overall financing amount did decrease by 19% ($875m vs $1.1b). On a month-on-month basis, both the financing amount and the number of financings also decreased.

In Q3 2022, approximately 69% of the financing volume and 36% of the financing amount were concentrated in the seed round. The A round accounted for 14% of the financing volume and 20% of the financing amount, and the B round accounted for 5% of the financing volume and 38% of the financing amount. Overall, the data shows that the deal size of the seed round has shrunk ($7m in Q3 22 vs $12m in Q1 22), and projects that raised seed rounds in 21 have begun to raise A rounds (average round size between $20-$25m)

On the one hand, as the track matures, investors are more confident in betting on early-stage projects in the track. On the other hand, with the emergence of more content-oriented studios (which rely more on the investment logic of traditional games), the strategy of diversifying investments and avoiding single-point risks of investing in a single game is becoming more and more popular.

About 1/3 of seed rounds were above $7m deal average, with Animoca Brands Japan, Klang Games, Xterio, and Meta World raising seed rounds above $30m. Almost all series A rounds were above $10m, with Gunzilla Games, Iskra, and Planetarium Labs raising A rounds above $30m. The remaining deal value was made up of two B rounds, Limit Break's $200m and Animoca Brands' $110m.

Among the many financings, the most shining one is the original Machine Zone (MZ was acquired by Applovin in 2020). The team's Limit Break has a project valuation of 1.8 billion. 200 million pre-launch financing is very rare even when the market is hot. Behind the success of MZ is the mature methodology of the SLG team to engage and monetize whales (the big R in SLG). With this mature methodology, Limitbreak is familiar with how to let the whales of web3, as owners, better participate in the community's insights and more elegantly realize the value of whales.

Machine Zone:

Overall, the web3 gaming financing market has entered a new stage. The companies that are favored by investors are no longer platform-based and infrastructure-based projects, but studios that are capable of eventually landing engaging content products. Infrastructure and platforms are more of the solutions that content-based companies bring with them (perhaps to adapt to the preferences of token funds and increase valuations?).

But this does not mean that investors have lost interest in infra companies. It is just that there are many more roads than cars now, the supply and demand of infrastructure projects are unbalanced, and there are still not enough hit content projects. Neither developers nor players have yet discovered new demand points.

In general, the Infra landscape is moving towards a stage of maturity. Whether it is gaming layer 3, wallet, gaming marketplace, or gaming SDKs, for games, there is a certain surplus of existing Infra projects. They are beginning to draw clear boundaries and start to compete fiercely for market share in their respective segments.

Interestingly, when I asked the entrepreneur of a certain game why he chose infra company A instead of B, and whether there were any technical considerations behind it, the answer I got was often, "Because they reply to messages instantly."

It is foreseeable that when the price and technology of the solution can no longer help the infra project gain an advantage, the game infra will begin to compete with "soft power" such as BD capabilities, customer service quality, IP inventory, etc.

Migration of web2 gaming talent to web3

After talking about the trends of capital, let’s take a look at talents:

For a long time, regarding web3 games, traditional game players have been wondering why gaming insiders have not been involved in web3 game companies and web3 games. Whether it is developers, publishers, or channels, there has always been a strong wait-and-see sentiment.

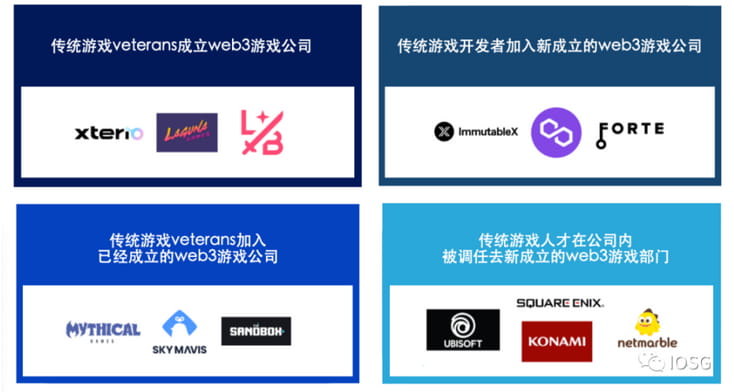

In the blink of an eye, it is now Q3 of 2022. I think that on the one hand, the wait-and-see attitude of the traditional gaming industry, which has suffered from regulation, towards web3 is completely understandable. On the other hand, whether players admit it or not, this wait-and-see attitude is disappearing. As the most intuitive manifestation, the migration of traditional gaming industry talents to web3 has appeared. This migration can be summarized into four forms:

1. Traditional game industry leaders set up web3 game companies (xterio, laguna games, limit break etc.)

2. After quitting traditional games, join an established web3 game company (mythical games, sky mavis, forte etc.)

3. Traditional game developers join newly established web3 game companies (immutable, polygon, forte, etc.)

4. Traditional game talents are transferred to newly established web3 game departments in traditional game companies (Ubisoft, Square Enix, Konami, Netmarble)

If we look at the recruitment situation of some target companies in the industry:

Both the migration method and recruitment data reflect that talents prefer companies with high-quality content production capabilities.

The migration of talent will be slow but continuous. For the industry, this not only means that web3 games will become more fun, but also means that the industry will not face the dilemma of reinventing the wheel. Industry experience and practice, including traditional game industry R&D pipeline management solutions, game prototype iteration methodology, publicity and promotion methods, etc., will be the most fertile nutrients on the newly opened up farmland.

A simple fantasy: In addition to the Ponzi-like economic system, will there be a more fun and sustainable economic model around the commercialization and operation system of traditional f2p games' non-氪-small氪-medium r-large r?

Summarize

Although the number and amount of financing have further shrunk in Q3 due to the general environment, it is undeniable that the track is maturing. The author predicts that the performance and talent flow in Q3’22 will only be an indicator. In the foreseeable future, financing activities/talent flow will only return to rationality.

This is a rectification of the market. When the tide recedes and some hot concepts in the hype phase are verified/falsified, investors and projects will only choose to bet on them more wisely, and builders will also move towards areas that have not yet been occupied and can carry real user needs.

Although it is a cliché: to meet the real user needs and the most daily usage scenarios, all content products will eventually return to the rationality of content being king.