Written by: PSE Trading Analyst, @Yuki

Under the general environment of the Federal Reserve's interest rate hike, the United States has entered the "high interest rate era". In the face of the continued rise in U.S. Treasury yields, the low-risk returns in the DeFi world are obviously somewhat stretched. The crypto market has fallen into a dilemma of one-way outflow of funds into the traditional financial market.

"Introducing real-world asset returns into DeFi" will become an important measure to retain on-site funds and attract external funds. Based on this, the crypto market will refocus on the RWA (Real World Assets) concept that appeared in 2020, trying to explore the best way for funds to circulate between traditional financial markets and crypto markets through different business models.

This article will start from the most suitable underlying assets for RWA in the short and medium term, and sort out and analyze the existing RWA business models in the crypto market.

1. Exploration of RWA underlying assets

1.1 Track Background & Current Situation

At present, although the total market value of the crypto market remains around 1 trillion US dollars, there is a lack of stable low-risk income sources in the market. Only ETH-based liquidity pledge based on the PoS mechanism has been recognized and supported by funds in the market. This also indirectly illustrates the inevitability of the rise of LSDFi.

According to data from ultrasound.money, Ethereum has generated 1.4 million ETH of staking rewards since it switched to PoS, and its current staking rate is only 22.03% of the total supply. This means that Ethereum has become an interest-bearing asset with a 5.3% (Staking Rewards/ETH staked) interest rate, which has brought the market a basic income of $2.4 billion (ETH was $1,720 per coin at the time of writing this article).

Then, following the same idea, RWA tokenization is to directly map the "equity value" of various assets in the real world to the blockchain in the form of digital currency, giving the "equity value" transaction and circulation attributes. In other words, RWA introduces the income of real assets into the encryption industry, and can be used as the real income of U-based assets to inject better liquidity and vitality into the entire market.

Currently, the scale of stablecoins in the entire crypto industry is around $74.3 billion, but most of the stablecoins pegged to the U.S. dollar (U-based assets) do not have stable real returns (compared to ETH's 5% staking return). If RWA can bring the same level of real returns to U-based assets (close to 5% annualized), it can stimulate further growth in the scale of stablecoins in addition to generating $3.7 billion in basic returns each year.

According to rwa.xyz statistics, the cumulative borrowing volume of existing RWA private credit agreements is only more than 500 million US dollars (MakerDAO is not included in the statistics), and the scale of tokenized US debt is only 640 million US dollars (indirect introduction model is not included in the statistics), totaling less than 1.2 billion US dollars.

Taking short-term Treasury Bills as an example, the average interest rate announced by the U.S. Department of the Treasury on July 31 this year was 5.219%, with an overall scale of $4.769 trillion. If RWA can introduce this part of the income into the crypto market, it will ideally generate a revenue scale of $248.89 billion. For the crypto industry, which has an overall market value of only $1 trillion, this flood of liquidity will irrigate the entire industry and revitalize it.

The report released by BCG and ADDX also predicts that global tokenized assets (such as real estate, stocks, bonds, and investment funds) will grow to 16.1 trillion US dollars in 2030, bringing more effective attention to the crypto market.

In summary, RWA is still in its early stages of development, but it has great potential. Just as the real returns of ETH-based assets triggered the wild growth of LSDFi, RWA can also serve as the real returns of U-based assets to drive the incremental development of the entire crypto market.

The crypto market has also keenly sensed the huge potential behind RWA, and DeFi OG projects led by MakerDAO and Compound are actively planning to enter the market.

1.2 Best underlying asset in the medium term: bonds

Since RWA needs to tokenize traditional off-chain assets, the choice of underlying assets will become the core issue. The reason is that the underlying assets have an inseparable and important impact on the complexity and flexibility of subsequent tokenization, and the difficulty of asset management and risk management.

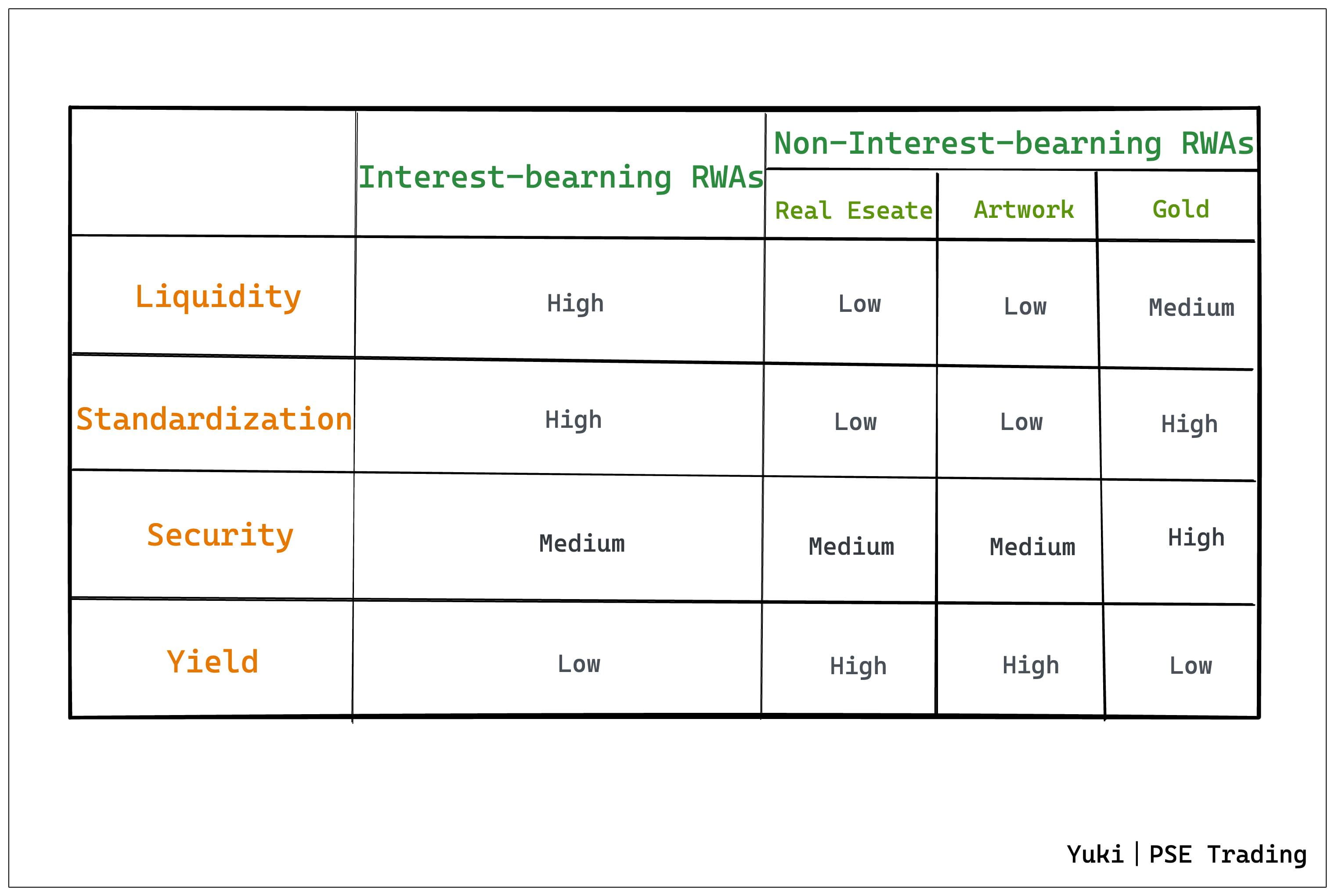

Based on the above logic of "RWA as the real return of U-based assets in the crypto market", the author directly divides the underlying assets of RWA into two categories:

Interest-bearing RWA (similar to ETH after switching to PoS): bond assets, mainly short-term US Treasury bonds or bond ETFs

Non-interest-bearing RWA (similar to ETH in PoW): real estate, art, gold, etc.

On this basis, taking into account the liquidity, standardization, security, and yield of the underlying assets, we can find that although interest-bearing RWA (mainly bonds) may lag behind non-interest-bearing RWA (real estate and art have a higher yield ceiling) in terms of yield, it has obvious advantages in terms of more important liquidity and standardization. Only underlying assets with better liquidity and higher standardization can support the large-scale application and expansion of RWA.

In addition, interest-bearing RWAs are similar to interest-bearing assets based on ETH. Even if the yield on the underlying assets is not high, stable "interest-bearing" can further improve the composability of the protocol layer, thereby promoting more DeFi innovations.

In summary, the author believes that the best RWA underlying assets in the medium term are debt assets mainly based on short-term US Treasury bonds or bond ETFs. Its interest-bearing properties not only perfectly meet the crypto market's desire for low-risk sources of income, but also its good liquidity and high degree of standardization are conducive to the large-scale application of RWA.

Therefore, below, the author will conduct an in-depth discussion on the "business model" level of representative RWA projects based on U.S. Treasuries or bond ETFs as underlying assets.

2. RWA business model based on US Treasury bonds/bond ETFs

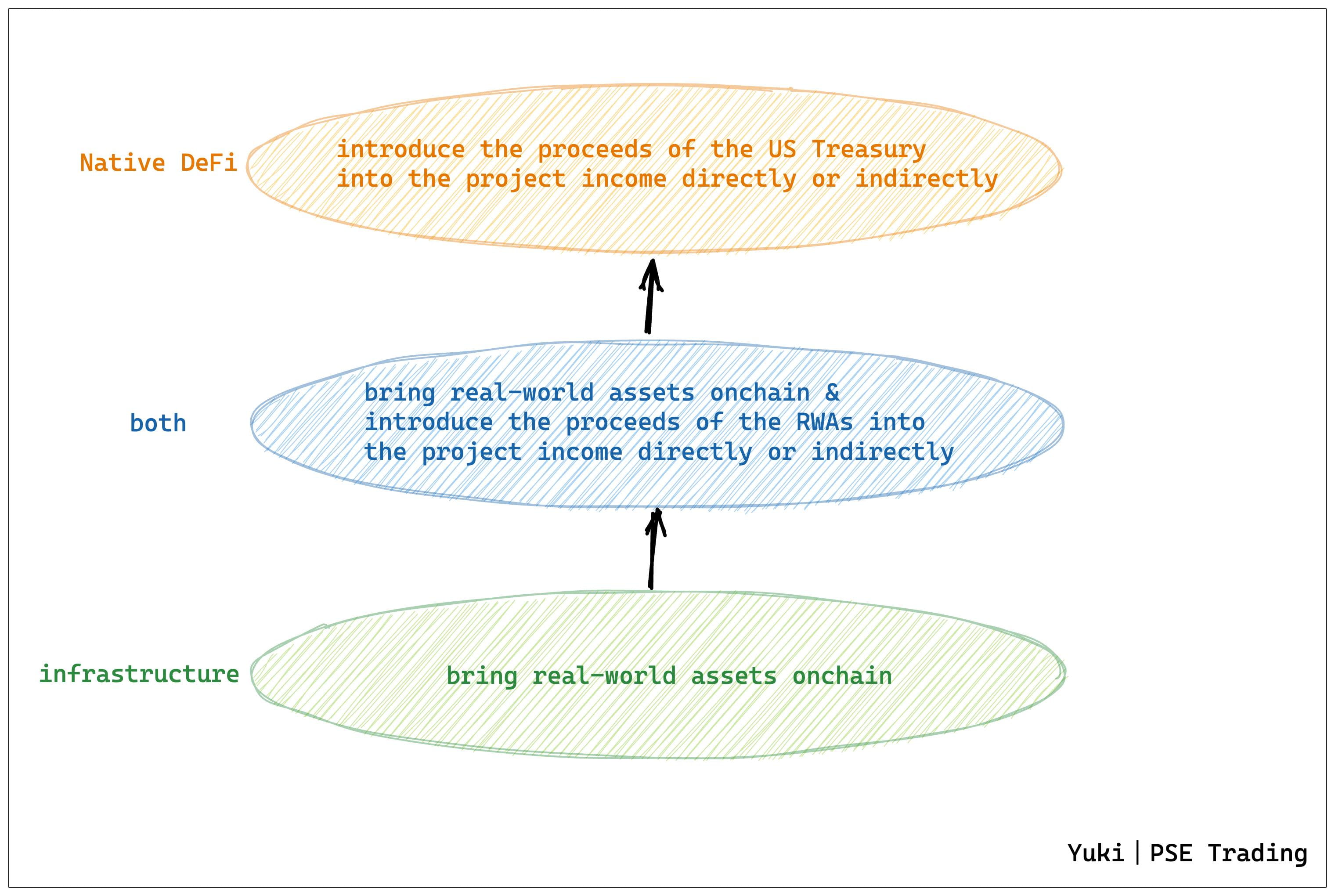

Starting from RWA with U.S. Treasuries as the underlying asset, we can find that the current mainstream RWA has three layers of business models, namely:

Underlying infrastructure business: responsible for the on-chain of US Treasury bond RWA

Middle-layer hybrid business: responsible for the on-chain transfer of U.S. Treasury RWA and the introduction of U.S. Treasury income into DeFi

Upper-level DeFi business: Directly or indirectly introduce U.S. debt revenue into project revenue

The difficulty and flexibility of RWA tokenization corresponding to the three-tier business model, as well as the customer groups they target, are very different.

Specifically, the RWA tokenization business, which is mainly operated by the underlying infrastructure, does not need to directly contact C-end users, but takes B-end projects as the main customer base. The step of "creating an on-chain representation of off-chain real-world assets" not only needs to solve the identity problem between on-chain and off-chain, but also needs to consider the security of assets, regulatory risks and implementation costs. This type of business is often the most difficult and complex, but it is also an indispensable part of RWA.

As upper-layer DeFi native applications, they do not have to consider the "tokenization" event itself, but can directly or indirectly introduce RWA income based on the completed RWA tokenization. Most of the methods are to choose to cooperate with infrastructure projects or build DeFi products based on RWA tokens. Therefore, they are also mostly directly facing C-end users.

The middle layer is a combination of the two. While they realize the tokenization of RWA, they also create suitable on-chain products for their own RWA tokens to directly introduce RWA income and integrate into the DeFi world.

Generally speaking, any project involving RWA tokenization business has stricter KYC requirements. On the one hand, this is due to security and regulatory requirements, but on the other hand, it is contrary to the core of DeFi's free spirit, and invisibly raises the entry threshold of RWA.

2.1 Underlying Infrastructure: RWA Tokenization

An essential step in bringing real-world assets onto the chain is to encapsulate the assets so that they are presented in digital form on a compliant basis, while retaining important information about the assets, such as value, ownership, term, etc. The importance of this business is equivalent to laying a solid foundation for building a building.

2.1.1 Business Model 1: SPV Tokenization

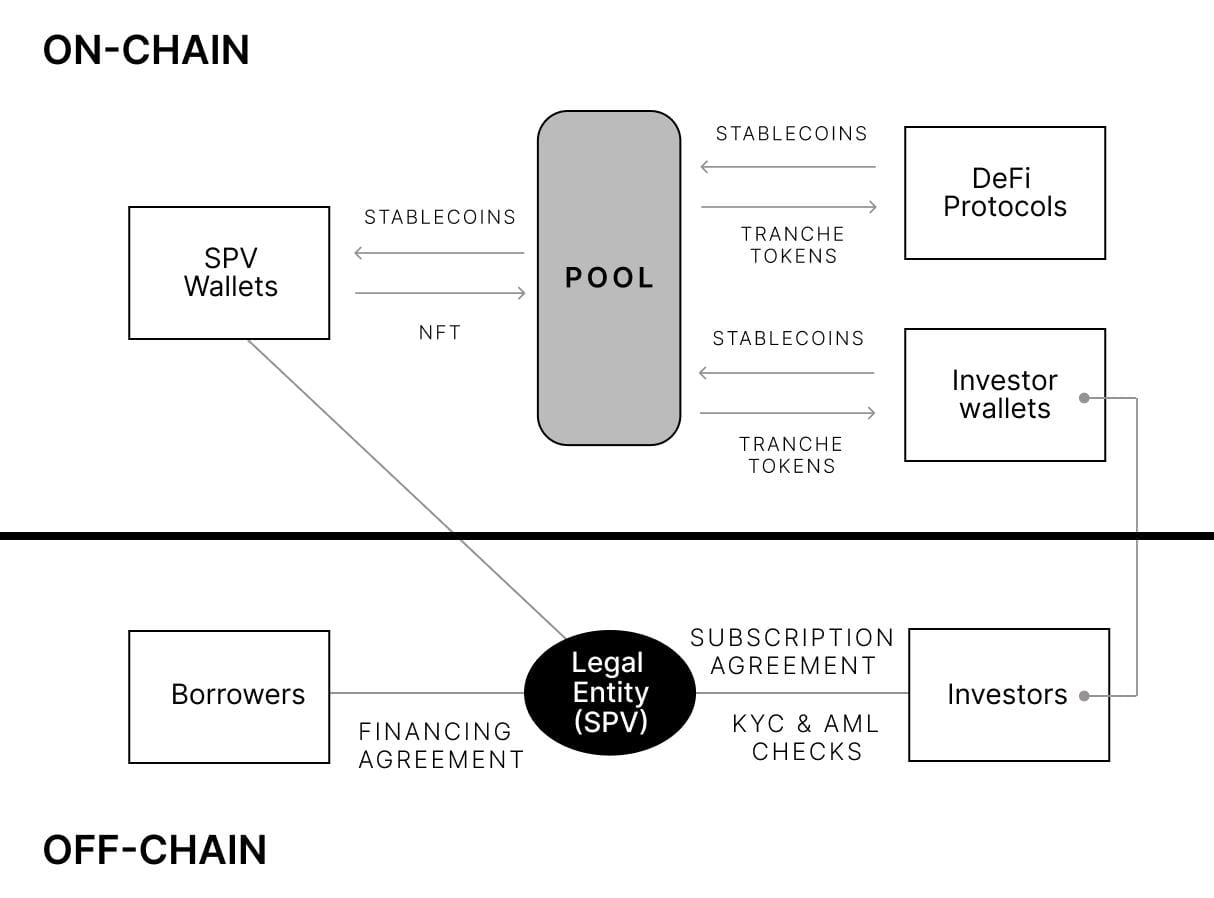

The most mainstream way to realize RWA tokenization is to refer to the idea of asset securitization, establish a special purpose vehicle (SPV) to hold the underlying assets, and realize control, management rights and risk isolation.

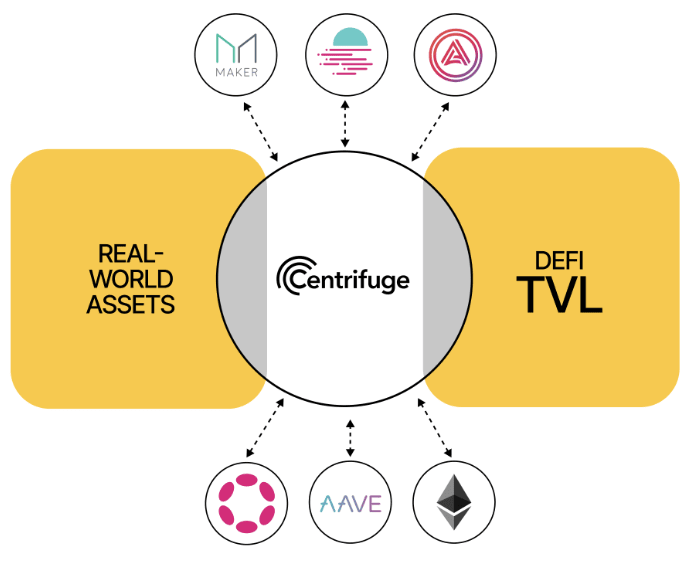

Representative project: Centrifuge

Centrifuge

Although Centrifuge is an RWA lending protocol, its SPV tokenization path has important implications for many DeFi protocols to implement RWA. Centrifuge Prime, which it launched, is also intended to provide a technical and legal framework for DAOs to invest in RWAs.

MakerDAO and New Silver issued the first RWA002Vault through Centrifuge as early as February 2021. Since then, the introduction of RWA on a larger scale has been based on the SPV tokenization path.

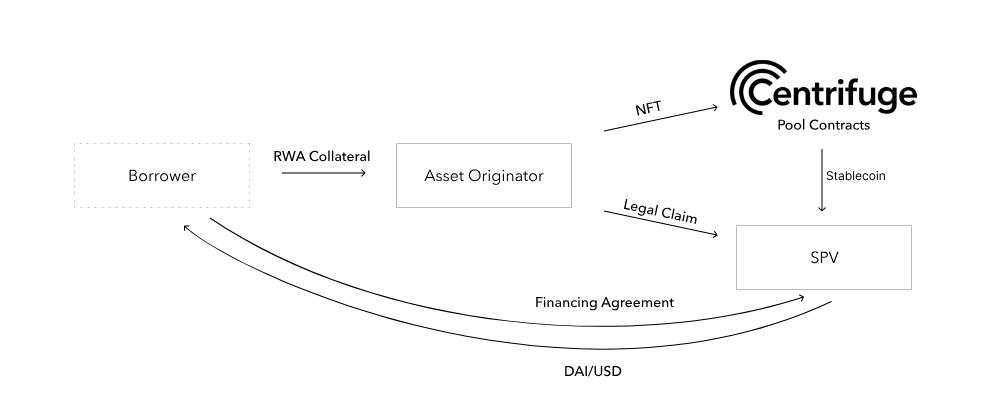

Centrifuge’s RWA business model implementation path is as follows:

The Asset Originator sets up a legal entity for each pool, namely the SPV. The purpose is to isolate financial risks and provide funds for specific RWA as the underlying asset of a specific Centrifuge pool;

Borrowers tokenize off-chain assets into NFTs through AO (underwriter) and use them as on-chain collateral;

The borrower enters into a financing agreement with the SPV and requires the AO to lock its NFT in a Centrifuge pool tied to the SPV;

After the NFT is locked, DAI is extracted from the Centrifuge reserve and transferred to the SPV wallet. The SPV wallet then converts DAI into US dollars and transfers it to the borrower's bank account through a bank transfer.

The borrower repays the financing amount plus financing fees on the NFT maturity date. The repayment method can be directly repaid on the chain with DAI, or transferred to the SPV in US dollars. The SPV converts US dollars into DAI and pays it to the Centrifuge pool. After full repayment, the locked NFT will be returned to the AO and destroyed.

Although Centrifuge has adopted SPV risk isolation and worked with Securitize to put a lot of thought into KYC/AML compliance verification, its RWA asset pool still has some bad debt problems. According to rwa.xyz data, Centrifuge has a total of \(13,210,882 in defaulted loans, accounting for 3.01% of the total loan amount (\)438,341,921).

2.1.2 Business Model 2: Tokenization of Fund Shares

Another common way to tokenize RWA is to launch a compliant fund based on short-term U.S. Treasury bonds, record the fund's transaction data on the chain, and tokenize the fund shares.

Representative projects: Superstate, Franklin Templeton

Superstate

Robert Leshner, the founder of Compound, announced the establishment of a new company, Superstate, in June to officially enter the RWA market. Superstate plans to launch a fund based on short-term government bonds and has submitted relevant application materials to the SEC, awaiting approval. It is worth noting that Robert Leshner himself has a background in the U.S. Treasury Department, so he has certain advantages to some extent.

Superstate's RWA business model implementation path is as follows:

Superstate launches funds based on U.S. Treasuries and government agency securities for U.S. residents;

Users subscribe to the fund and become shareholders of the fund;

Shareholders can convert their fund shares into corresponding tokens and keep records on Ethereum;

Fund share token holders need to register their addresses as the fund’s whitelist. Non-whitelist addresses cannot be traded.

The official records of the fund transfer agent are still managed in book-entry form. When the on-chain records conflict with the off-chain records, the fund manager will update the on-chain records based on the off-chain records.

Franklin Templeton

Franklin Templeton, a listed fund management company with over one trillion U.S. dollars in assets under management, has a business model similar to Superstate for implementing RWA. It also launched the government money market fund Franklin OnChain U.S. Government Money Fund - FOBXX on the Stellar chain in 2021 through the "tokenization of fund shares". The unit shares of the fund are represented by BENJI tokens.

2.2 Intermediate mixing layer: RWA tokenization + interoperability with DeFi

Compared with the bottom layer, the business model of the RWA project in the middle layer has an additional part that is directly connected and circulated with DeFi. Similar to the "self-production and self-sales" model, the design from the bottom layer to the upper layer can be determined by the user, which is more convenient for expanding the project scale while controlling risks. However, since the tokenization process of US debt still needs to comply with strict legal regulations, KYC is still unavoidable.

2.2.1 Business Model 3: Fund Share Tokenization + DeFi Protocol

Representative project: Ondo Finance

Ondo Finance

Ondo Finance uses an exemption issuance method to serve institutional users. The exemption issuance has more stringent requirements for users, and they need to meet the requirements of "qualified investors" and "qualified buyers" defined by the SEC.

Ondo’s RWA business model implementation path is as follows:

Users invest USDC (or other stablecoins) into Ondo’s fund products and receive a corresponding number of fund tokens;

Ondo converts the stablecoins into U.S. dollars (custodied by Coinbase) and then keeps them in a bank account;

Then buy U.S. Treasury ETFs through Clear Street, which has brokerage and custodian qualifications;

When these underlying assets earn a yield, that yield is reinvested to purchase more assets, thus automatically compounding;

At any time, if a user wants to redeem his USDC, the corresponding fund tokens will be burned and then USD will be received.

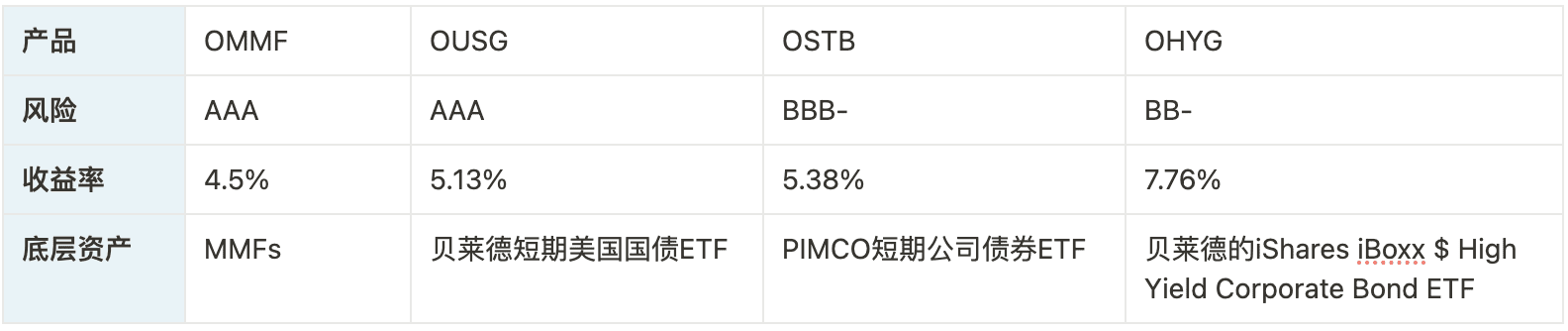

Ondo currently offers four RWA products for US users, backed by different underlying assets, providing diverse options for investors with different risk preferences.

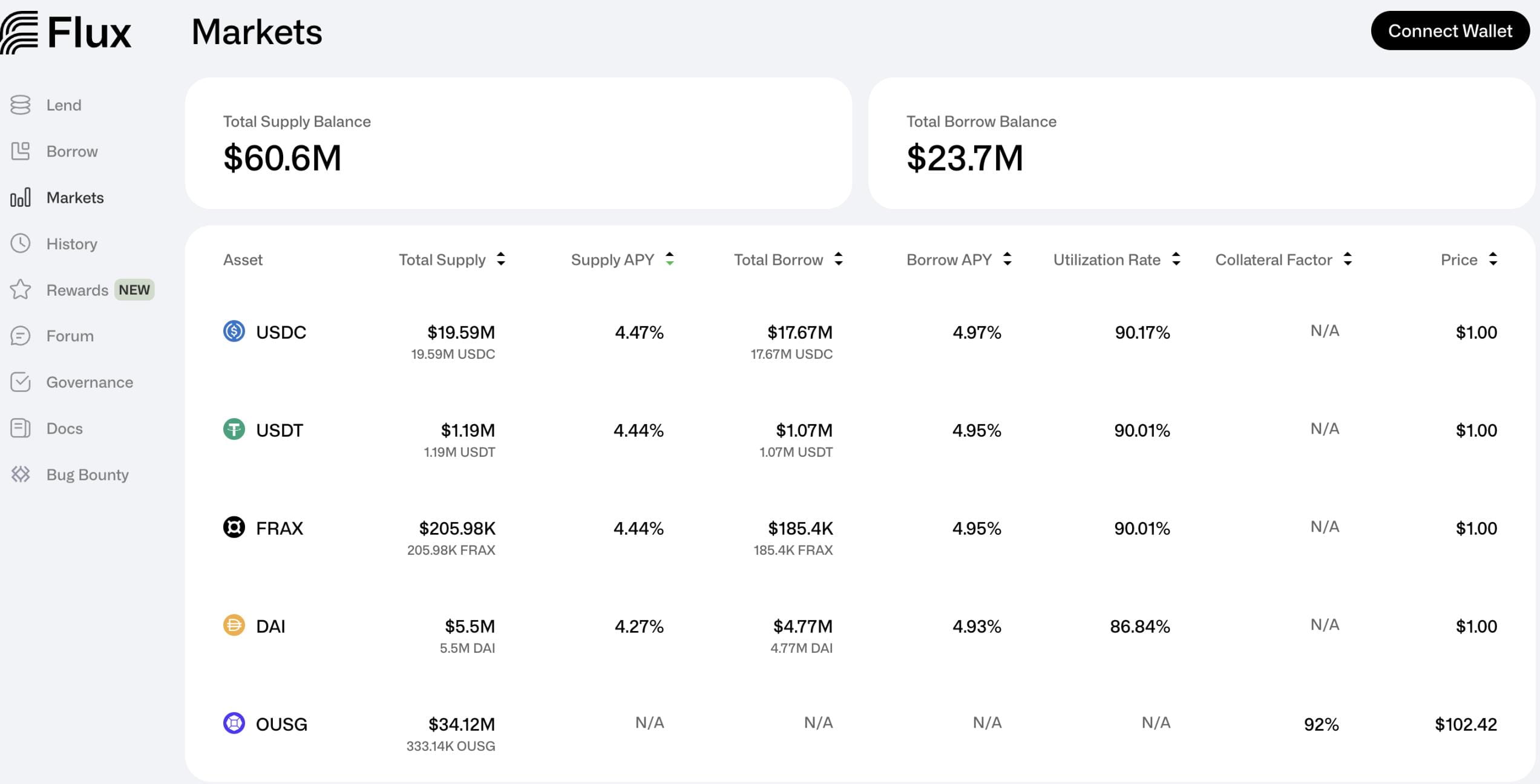

The largest fund is OUSG. In order to expand the use of OUSG, Ondo has developed its own decentralized lending protocol Flux Finance. OUSG holders can use Flux to pledge OUSG and borrow stablecoins such as USDC, DAI, and Frax.

Flux itself has no KYC restrictions, but it uses a whitelist liquidation mechanism. The significance of Flux is to help Ondo further connect RWA to the native DeFi world and strive to create an "ecological closed loop".

For non-US users, Ondo plans to launch a new USDY product, a tokenized note backed by short-term US Treasury and bank demand deposits. Users can transfer USDY on-chain 40-50 days after purchasing it.

2.2.2 Business Model 4: SPV Tokenization + DeFi Protocol

Representative projects: Matrixdock, Maple Finance, Kuma Protocol

Matrixdock

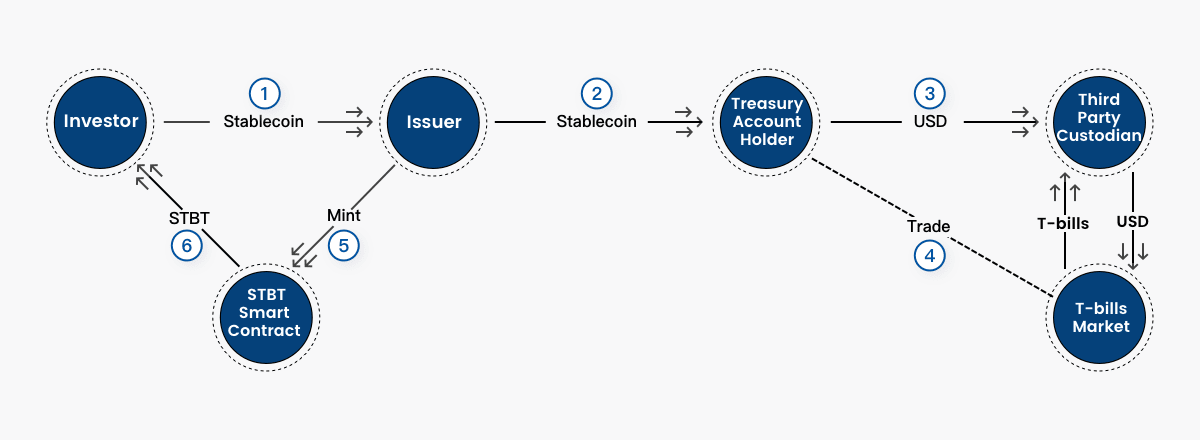

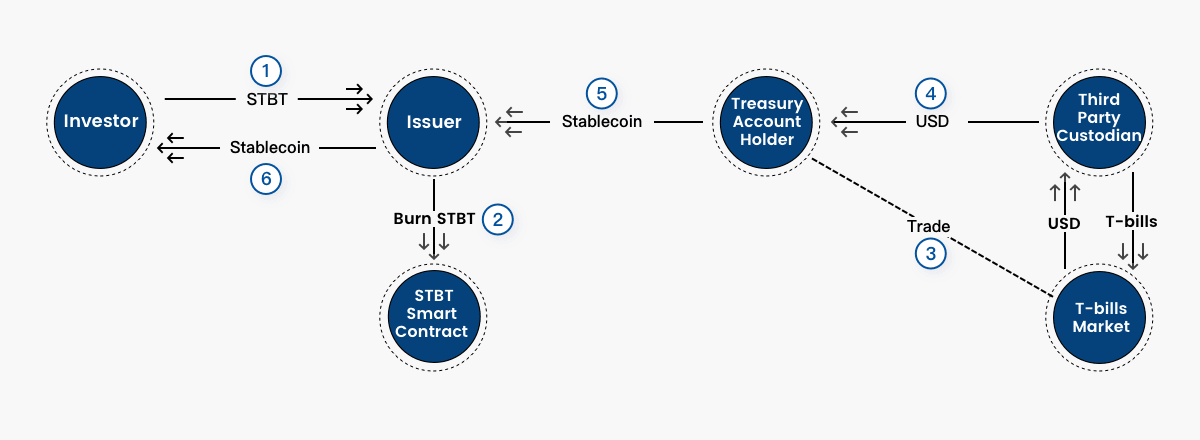

Matricdock is an on-chain bond platform launched by Matrixport, which has launched the STBT (Short-term Treasury Bill Token) product based on short-term US Treasury bonds. STBT is an ERC 1400 standard token, which redefines the interest base every working day, and the underlying assets are US Treasury bonds and reverse repurchase agreements due within 6 months.

The implementation path of Matrixdock's RWA business model is as follows:

Matrixport’s separate SPV serves as the STBT issuer;

Investors deposit stablecoins into SPV, and SPV mints a corresponding amount of STBT through smart contracts;

The SPV converts stablecoins into fiat currency through Circle and pledges its US Treasury bonds and cash assets to STBT holders;

The legal tender is entrusted to a qualified third party for custody, and the qualified third party custodian purchases short-term debt maturing within six months through the U.S. debt trading account of a traditional financial institution, or invests in the overnight reverse repo market of the Federal Reserve;

STBT holders have first priority repayment rights over the physical asset pool.

It should be noted that only investors who have passed KYC can invest in Matrixdock's products, and STBT is only allowed to be transferred between whitelisted users, including STBT in the Curve pool. The decentralized RWA lending protocol T Protocol has built a fund pool with STBT for unlicensed investment in US bonds.

Maple Finance

Maple Finance was once an unsecured lending project based on RWAs, but the high risk of the unsecured lending model left Maple with a huge bad debt of more than 50 million US dollars. So in April this year, Maple changed its mind and launched a new cash management pool (similar to the Matrixdock model), allowing non-US qualified investors and entities to directly participate in US debt investment through USDC. The implementation path of the RWA business model is similar to that of Matrixdock, so I will not go into details here.

It is worth noting that Maple recently completed a $5 million financing, which will be used to promote the expansion of its lending division Maple Direct. Maple Direct aims to provide customers such as DAOs and web3 companies with a simplified on-chain access to U.S. Treasury yields.

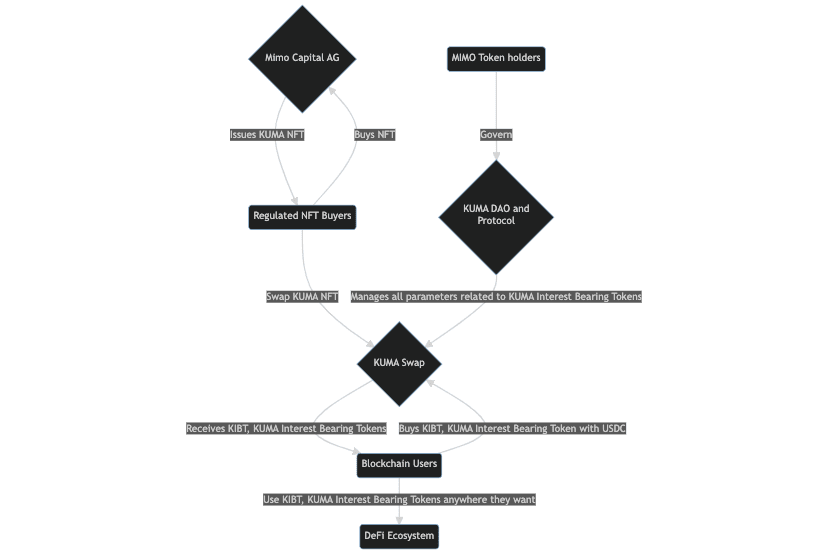

And Protocol

Kuma Protocol is an RWA protocol launched by Mimo Labs, which introduces RWA income into DeFi by issuing KIBT, an interest-bearing token supported by regulated NFTs. Currently, Kuma only accepts NFTs backed by sovereign bonds (US Treasury bonds).

In essence, KIBT is an interest-bearing stablecoin, and its balance will increase as the interest of the underlying assets increases. The significance of KIBT is that "users can invest it in the defi world while enjoying the interest of the underlying RWA."

Kuma Protocol’s RWA business model implementation path is as follows:

Mimo Labs established an SPV: Mimo Capital AG, and issued KUMA NFTs backed by sovereign bonds;

Users purchase KUMA NFTs with stablecoins, and then pledge NFTs through KUMA Swap to mint interest-bearing tokens KIBT;

KIBT is a rebased ERC20 token. There are currently two types of KIBT:

For KIBT associated with KUMA NFTs backed by 740-day Euro sovereign bonds, it is named EGK

For KIBT associated with KUMA NFTs backed by 1-year US sovereign bonds, it is named USK

The key to Kuma Protocol is to expand the use cases and liquidity of its interest-bearing token KIBT. The project is still in its early stages, and its feature of not requiring KYC is its biggest highlight at this stage.

2.3 Upper layer: DeFi with RWA income

As upper-layer DeFi native applications, they do not need to consider the "tokenization" event itself and the potential risks of KYC when conducting RWA business. Instead, they can directly or indirectly introduce RWA income based on the completed RWA tokenization. The implementation path is mostly to cooperate with infrastructure projects or build DeFi products based on RWA tokens.

2.3.1 Business Model 5: Indirectly Introducing RWA Revenue

DeFi native applications want to develop RWA business, generally there are two ideas: one is to build projects directly based on RWA income, the other is to indirectly introduce RWA income as protocol income. The most successful "indirect introduction" model is MakerDAO.

Representative projects: MakerDAO, Frax Finance

MakerDAO

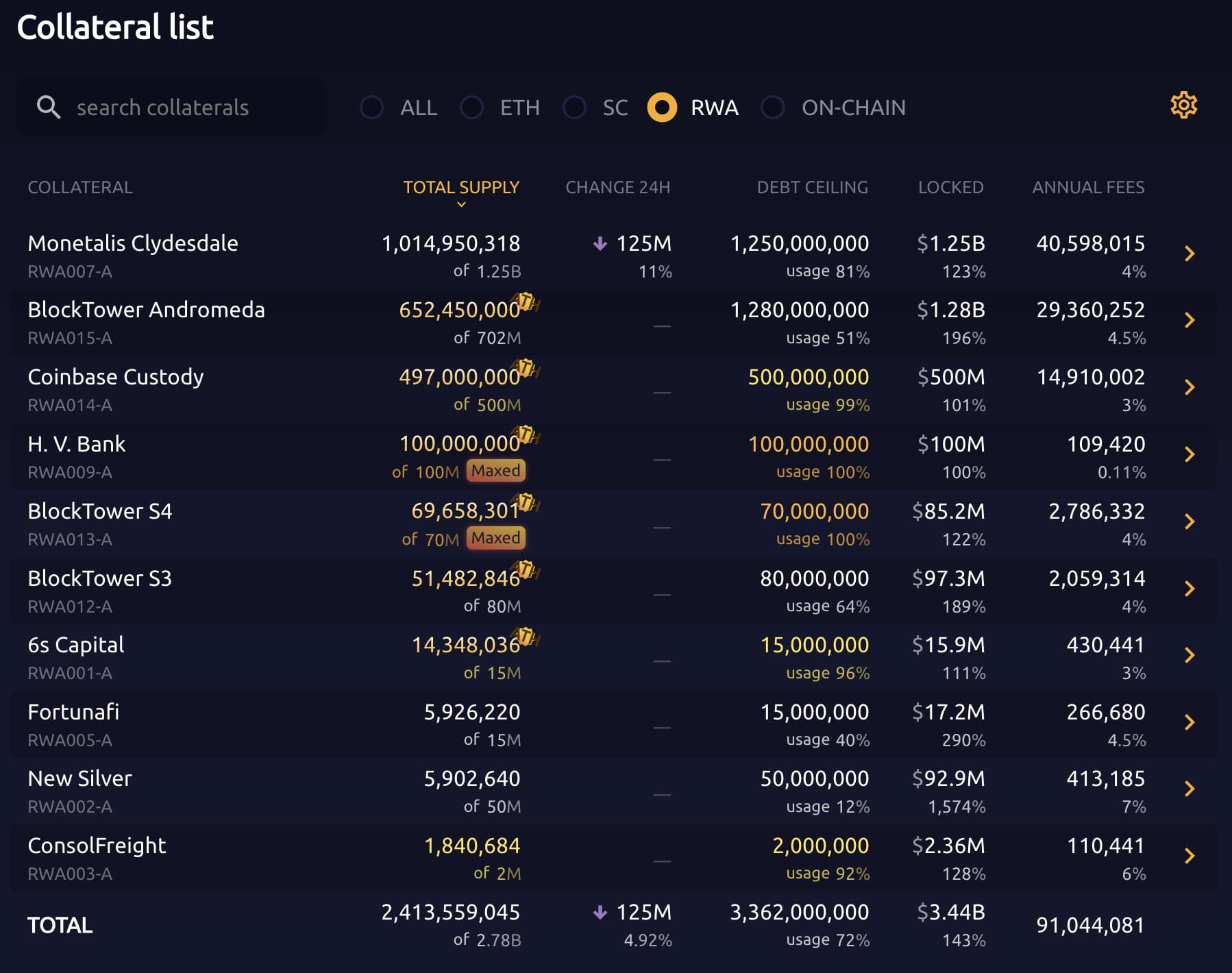

Although Dai has a volume of billions, it has never been able to break through a larger scale. For this reason, MakerDAO co-founder Rune proposed to introduce RWA as a transition. According to MakerBurn data, MakerDAO has now introduced a total of 10 RWA projects, with $2.413 billion in assets as collateral. These RWA assets contribute more than 50% of MakerDAO's revenue. The rise in DSR interest rates is also inseparable from RWA revenue.

The largest RWA asset currently held by MakerDAO is Monetalis Clydesdale, which was formed by the MIP65 proposal proposed by Monetalis founder Allan Pedersen in January 2022.

The purpose of MIP65 is to use some of the stablecoins held by MakerDAO to obtain more stable returns by investing in highly liquid, low-risk bond ETFs.

Monetalis Clydesdale’s RWA business model implementation path is as follows:

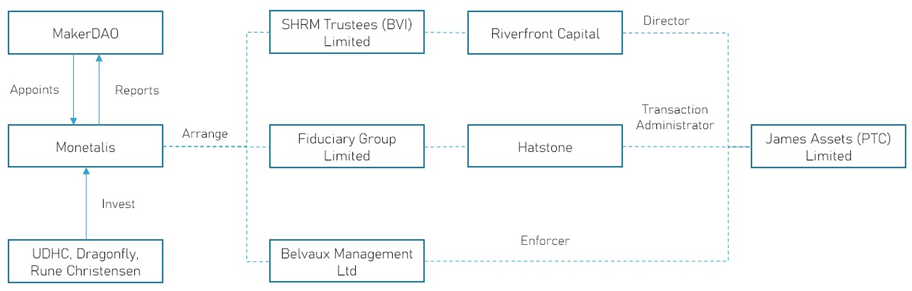

After MakerDAO votes, it entrusts Monetalis as the executor to report to MakerDAO regularly;

As the project planner and executor, Monetalis designed a complete BVI-based trust structure (as shown below) to achieve synergy between on-chain and off-chain.

All MakerDAO MKR holders are the overall beneficiaries and issue instructions on the purchase and disposal of trust assets through governance;

Coinbase provides exchange services for USDC and USD;

The funds are invested in two types of ETFs: Blackrock’s iShares US\( Treasury Bond 0-1 yr UCITS ETF and Blackrock’s iShares US\) Treasury Bond 1-3 yr UCITS ETF;

The income from the U.S. Treasury ETF belongs to MakerDAO, which then distributes the protocol income to DAI holders by adjusting the deposit rate of DAI.

Although this complex and feasible trust structure indirectly introduces U.S. debt income into MakerDAO, it also comes with high expenses, including initial fees and subsequent ongoing fees paid to relevant institutions to maintain the operation of the trust. As the scale of RWA gradually expands, MakerDAO needs to explore a feasible way with lower costs.

Frax Finance

Sam, the founder of Frax Finance, recently made it clear that Frax V3 will enter the RWA track and launched a proposal on the governance forum to expand the RWA business through FinresPBC. The implementation path (according to the proposal) is nothing more than setting up an SPV off-chain to hold RWA assets and converting the proceeds into revenue for the protocol itself to expand the scale of FRAX stablecoins.

Obviously, after MakerDAO has proved that the RWA path is feasible, more and more old DeFi projects will follow suit and find reasonable risk-free returns for idle funds in the treasury. In addition, for stablecoin projects such as Frax, if they want to increase their market share, RWA returns are indeed an opportunity that cannot be missed.

2.3.2 Business Model 6: Directly Introducing RWA Revenue

Representative projects: T protocol, AlloyX

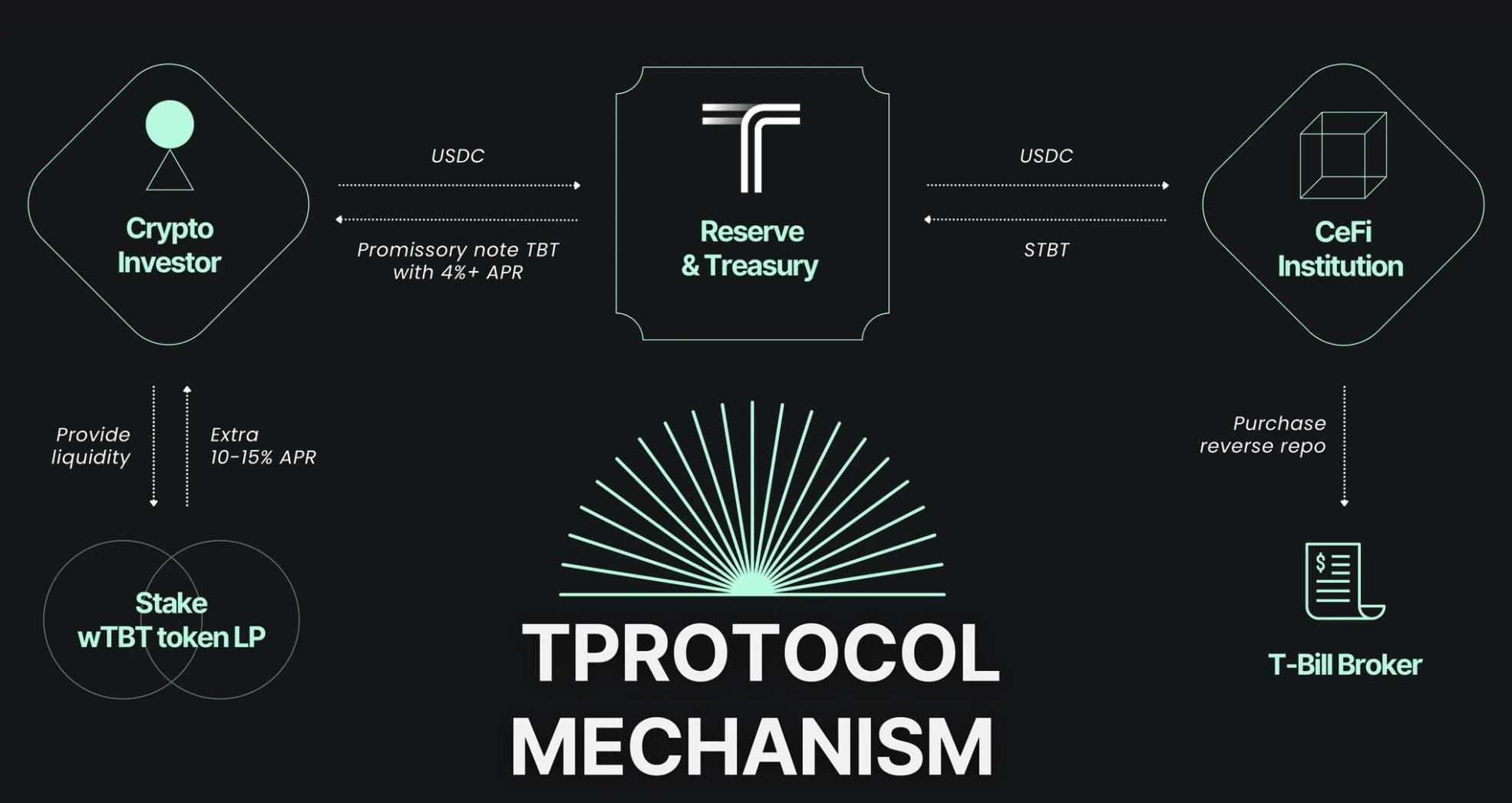

T Protocol

T Protocol is an RWAFi protocol based on STBT issued by MatrixDock. The project hopes to remove the whitelist restrictions of STBT through token packaging, realize permissionless U.S. Treasury token products, and lower the threshold for U.S. Treasury investment for users.

The implementation path of T Protocol’s RWA business model is as follows:

T Protocol launched TBT, which is a packaged version of STBT. TBT uses the rebase mechanism to issue US Treasury yields, and the price is anchored at $1.

Investors put USDC into T Protocol, which mints TBT and obtains deposit certificates rUSTP;

T Protocol purchased STBT through its partners, that is, MatrixDock pledged STBT and borrowed USDC;

rUSTP accumulates income in the form of rebase, and rUSTP can be exchanged with the protocol stablecoin USTP at a 1:1 ratio;

T Protocol exchanges USDC from the curve liquidity pool (suitable for small transactions) or exchanges USDC with MatrixDock through OTC (suitable for large transactions) and returns it to the user.

The idea of T Protocol is to become an intermediary between non-Matrixdock users and Matrixdock, lowering the threshold for investors and making U.S. bond yields more seamlessly enter native DeFi. T Protocol's KYC-free strategy may become mainstream in the future, and its issued TBT may also be a potential competitor to stablecoins.

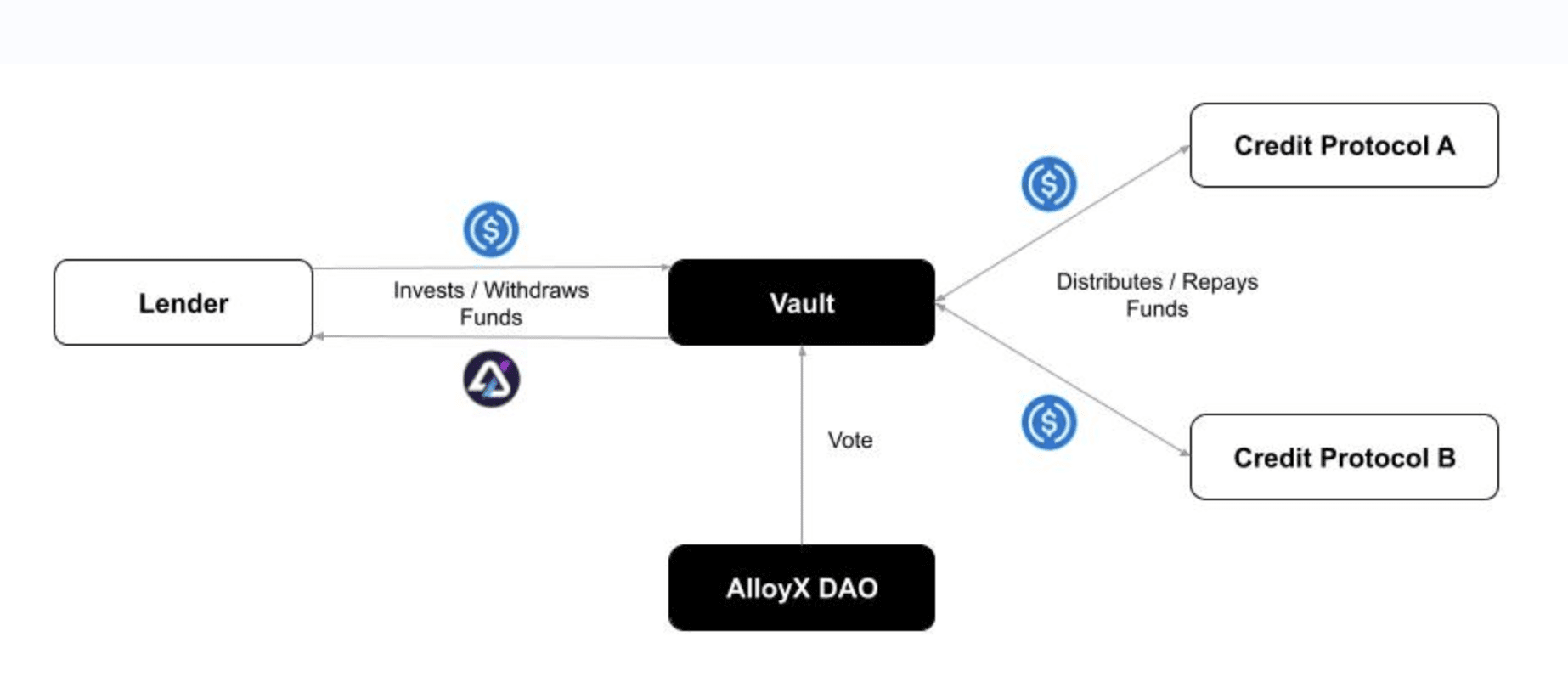

AlloyX

AlloyX is a DeFi protocol based on RWA, which mainly provides investors with different composable investment strategies by integrating other credit protocols. AlloyX has integrated protocols such as Credix, Goldfinch, Centrifuge, Flux Finance, and Backed Finance.

AlloyX's RWA business model implementation path is as follows:

AlloyX decides on specific investment strategies through DAO voting and launches corresponding treasury products;

Lenders provide funds to treasury products in the form of USDC, while receiving treasury tokens based on a floating exchange rate and earning returns;

Lenders can exchange Treasuries tokens back to USDC.

The most special thing about AlloyX is that it integrates many credit agreements, which can flexibly allocate user funds to different agreements to maximize returns, minimize risks, and have super composability. However, the problem also comes from the integration of third-party credit agreements. Once the credit agreement defaults (AlloyX cannot guarantee the security of the credit agreement), AlloyX investors will bear greater risk exposure.

3. Thoughts and Conclusions

There can be many underlying assets for RWA, but the most suitable for the crypto industry at present must be bonds (mainly short-term US bonds and ETFs). Compared with real estate, art, gold and other assets, bond underlying assets have the strongest comprehensive advantages in terms of standardization, liquidity, and tokenization costs.

Therefore, in the short and medium term, the RWA direction with bonds as the underlying assets deserves more attention. With the goal of establishing U-standard interest-bearing assets within the crypto market, it can be found that U.S. Treasury RWA has its own risk-free returns in the era of high interest rates, which perfectly meets the needs of the market.

Based on U.S. Treasury RWA, there are currently three mainstream business models, namely the underlying infrastructure business, the middle-layer hybrid business, and the upper-layer DeFi business. The three-layer business models correspond to the difficulty and flexibility of RWA tokenization and the customer groups they target. However, considering the legal regulatory risks and development ceiling, the ceiling of the upper-layer DeFi business is higher. Putting U.S. Treasury RWA on the chain is only the first basic step, but exploring the composability around the "interest-bearing attribute" and native DeFi is a more worthy direction to explore. There are different attempts on the market, such as stablecoins based on U.S. Treasury RWA and permissionless lending.

In the long run, RWA will become an important carrier for completely connecting TradFi and DeFi, forming liquidity interoperability, zero (low) threshold capital conversion, and value sharing.