TL;DR

1. Among the four staking methods, Pool Staking, led by Lido Finance, dominates the ETH staking landscape, accounting for 36.6% of the total staked ETH market share. This is due to the accessibility, versatility, and unique advantages of liquid staking derivatives (LSDs).

2. The diverse LSD ecosystem consists of the following sectors: DVT infrastructure, pool staking protocols, LSDFi protocols, re-staking, and MEV yield sharing. These sectors address challenges, promote decentralization, and optimize yields for stakers, contributing to the continuous growth of the LSD market.

3. The LSD market has substantial growth potential, which could be driven by low current ETH staking participation, infrastructure development, and the application of staking rehypothecation, contributing to a more decentralized and robust ecosystem with ample opportunities for future expansion.

4. The key factor of LSD market growth is the ETH staking ratio which only has 15% now. With the assumptions of bear, base, and bull cases, which use 38%, 51%, and 70% for ETH staking ratio respectively, the LSD market demonstrates the possibility of high three digit growth in mid-term, and a potential seven digit growth in five years.

5. The enhanced Beta returns from the LSD sector, as evidenced by the price behavior of key protocols’ tokens, along with the increasingly stable stETH peg, indicate that the LSD ecosystem is rife with both Beta play and Alpha-seeking opportunities. These prospects are particularly attractive to investors with medium to high risk tolerance.

1. The ETH Staking Landscape

There are four primary methods for staking ETH in PoS:

Solo Staking, which demands users to run their own validator node by depositing 32 ETH and meeting hardware specifications. Though this method offers maximum control and safety, it is resource-intensive for most users;

Staking as a Service (stSaaS), offered by third-party validator node operators, requiring users to stake 32 ETH while professional operators manage the process, making it less demanding.

Pool Staking, facilitated by liquid staking protocols, pools deposited ETH and delegates it to trusted node operators. Users receive a corresponding amount of LSD tokens representing their staked ETH.

CEX Staking, provided by exchanges like Coinbase or Kraken, is the simplest staking method, not requiring an on-chain wallet. However, it bears the highest centralized risk.

Compared to other major networks that also adopt PoS, Ethereum has a relatively low staking ratio. As per stakingrewards.com, other chains exhibit staking ratios between 40% and 70%. Ethereum’s lower ratio can be partially attributed to the withdrawal restriction that prevented users from accessing their staked ETH before the Shanghai Upgrade, which was completed in April and the relatively young staking infrastructure.

Pool staking has emerged as the dominant method for ETH staking due to its less demanding nature and versatile use cases, capturing 36.6% of the total ETH-staked market share, as reported by the Dune Analytics dashboard. A further analysis reveals that Lido Finance leads the pool staking/LSD sector, holding a 73% market share in the LSD sector. Lido’s success can be attributed to being backed by premier institutions like a16z and Paradigm and its first-mover advantage, which has established two strong competitive moats: economies of scale and high liquidity for stETH. The former grants Lido a fee advantage with node operators, while the latter provides stETH holders with greater flexibility for their LSD tokens in the DeFi ecosystem. These unique advantages are difficult to replicate. Additionally, the LSD market exhibits monopolistic characteristics, with the top five LSD protocols accounting for over 97% of the liquid staking market share.

2. The Origin of Liquid Staking Derivative(LSD)

The advent of Liquid Staking Derivatives (LSD) originates from “The Merge,” an Ethereum upgrade transitioning the network from Proof of Work (PoW) to Proof of Stake (PoS). This shift replaces miners with validators who stake ETH to secure the network. However, obstacles like high staking thresholds (32 ETH), hardware requirements, and withdrawal restrictions before the Shanghai Upgrade have deterred potential stakers. This led to the creation of LSDs, tokens representing staked ETH, issued by protocols like Lido Finance, Rocket Pool, and Frax Finance, or centralized exchanges such as Coinbase and Binance. These liquid tokens can be transferred or utilized in other DeFi applications. LSDs fall into two categories: rebasing, like stETH, which allocates staking rewards by increasing token quantity and reward-bearing, like rETH or wstETH, which distributes rewards through token value appreciation. As LSDs address staking barriers and capital inefficiency, the LSD market has experienced significant growth since 2023 and became one of the major DeFi narratives.

To gauge the beta return potential for LSD, we can use the price changes of core protocols’ tokens. From the chart, we can see that during major market rallies or downturns, such as the market crash on May 19th, the last bull rally, and the subsequent bear hit, tokens like $LDO and $RPL showed similar price actions to $BTC, indicating that the beta of LSD was identical to the overall market at the time. However, as the Merge approached, both $LDO and $RPL experienced significant rallies from July 2022 to September 2022, while $BTC was still struggling. This marked the onset of the LSD sector’s rise. Then starting from 2023, with the approach of the Shanghai Upgrade, not only $LDO and $RPL, but the entire LSD sector has seen another sector bull rally, further establishing this emerging sector as a central long-term narrative for DeFi and elevating its potential beta. After the Shanghai Upgrade, uncertainty around withdrawals was eliminated, marking a milestone for the LSD sector.

One of the most significant risks for LSDs is the loss of peg. We can use stETH, a representative LSD token, as an example to survey the history of LSDs’ peg and infer if LSDs will lose their peg in the future. The chart shows that when stETH was first introduced, the peg was extremely volatile, ranging from nearly an 8% discount to a 4% premium. However, as adoption increased and liquidity began to accumulate around stETH, the peg gradually stabilized to a consistent -1.5% for a year. The consistent discount for stETH was largely due to the uncertainty surrounding withdrawals at the time.

Market events such as the LUNA-UST incident and the crumble of FTX triggered panic-induced irrational market movements, causing stETH to temporarily lose its peg. However, the size of the discount was consistently decreasing with each event, suggesting growing market confidence in stETH.

With the completion of the Shanghai Upgrade on April 12, 2023, withdrawal uncertainty was eliminated, further stabilizing the peg. While I believe that major LSDs like stETH are unlikely to experience as significant a loss in peg as before, smaller LSDs with less liquidity and a lesser established brand may face a significantly higher peg risk. Therefore, caution should be exercised when holding LSDs with a smaller user base.

The development of the Liquid Staking sector can largely be characterized by the progress of key entities such as Lido, Rocket Pool, Frax Finance, Coinbase, and Binance. Lido, as the first mover in the space, quickly captured a significant market share. After about a year, Rocket Pool entered the scene with a more decentralized mechanism, gradually chipping away at Lido’s dominance.

Centralized exchanges like Coinbase and Binance, recognizing the considerable market potential of the LSD sector, launched staking services. With their extensive user bases and user-friendly interfaces, they were able to quickly gain traction. Frax Finance, however, carved out a significant market share amidst this fierce competition by utilizing its governance voting resources to offer higher yields, thereby sparking the onset of the yield war in the LSD sector.

It’s notable that post the Shanghai Upgrade, the TVL in on-chain protocols has been steadily increasing while the TVL in centralized exchanges has been gradually declining. This shift can likely be attributed to the regulatory risks that centralized exchanges face.

3. The State of LSD Market

Born with “The Merge” and growing alongside “Shapella,” the LSD market has evolved from a service sector into a diverse ecosystem catering to stakers, yield farmers, and DeFi degens. The LSD market consists of five sectors: infrastructure powered by Distributed Validator Technology (DVT), pool staking protocols, LSDFi protocols, re-staking, and MEV yield sharing protocol.

Current pool staking services face challenges such as custodianship of user funds and centralized node operator risks. DVT offers a solution by acting as a multi-signature wallet for validator nodes. It employs four core mechanisms:

Distributed Key Generation, which divides the validator private key into multiple parts and each operator owns a single portion of the private key(KetShare).

Shamir’s Secret Sharing, enabling private key reconstruction with a predefined threshold of KeyShares.

Multi-Party Computation, allowing operators to perform decentralized computation without reconstructing the complete private key on a single device.

Istanbul Byzantine Fault Tolerance, which selects the leading node at random.

These mechanisms contribute to a more secure and resilient network while significantly reducing slashing risks. Prominent DVT protocols include SSV Network and Obol Network.

The pool staking service sector is dominated by Lido Finance, Rocket Pool, and Frax Finance. Lido leads the market with a 73% share, attributed to its previously mentioned advantages. Rocket Pool, the second-largest protocol, holds around 7% of the market share. It distinguishes itself through a permissionless node operator onboarding mechanism, enabling anyone with 8 ETH and a minimum of 2.4 ETH worth of $RPL to become a node operator, thereby lowering entry barriers and promoting decentralization.

Frax, one of the fastest-growing LSD protocols, ranks third in total value locked (TVL). It has achieved high growth by offering above-average yields for stakers. After depositing, users receive frxETH, which can be further staked to obtain sfrxETH or provided to Curve’s frxETH/ETH pool to earn $CRV, $CVX, and $FXS. However, ETH staking rewards are forgone, being allocated to sfrxETH holders instead. sfrxETH holders earn higher yields with extra rewards from frxETH, while frxETH liquidity providers benefit from Frax’s substantial voting power in Curve and Convex, enhancing LP rewards.

LSDFi refers to DeFi products or protocols based on LSD and can be divided into the following categories:

Lending platforms, like Aave.

Yield aggregators, such as Yeran Finance, 0xACID, and bestLSD.

Yield protocols, including Aura Finance, unshETH, LSDx Finance, and Pendle Finance.

Index products, represented by Index Coop.

Service products, such as Cian, DeFi Saver, and Instadapp.

CDP protocol, like Lybra Finance.

Most LSDFi protocols aim to maximize LSD yields by sourcing external yields or utilizing leverage.

Re-staking, a concept introduced by EigenLayer, has become a central narrative in the LSD market. Essentially, re-staking involves taking already staked capital and staking it once again, thus adding additional slashing conditions to the capital.

This concept is significant from two perspectives. First, for PoS chains such as Ethereum, system security is directly proportional to the amount of staked capital, which is limited. Each time a new system emerges, capital becomes increasingly fragmented. Second, for applications like bridges, oracles, and roll-ups, securing substantial capital can be challenging, making it difficult to establish a secure system.

For instance, suppose Application A decides to provide services on the Ethereum network but encounters issues establishing its own security network. In such a case, Application A can participate in EigenLayer’s contract, specifying its reward and slashing mechanism. Restakers can then deploy their already staked ETH or LSDs to EigenLayer, securing Application A in a similar manner to how they secure the Ethereum network.

As more and more restakers participate in the EigenLayer contract, EigenLayer effectively pools the security provided by stakers. This process allows for a consolidated security service for network participants.

Re-staking addresses the issues by pooling fragmented capital or security and providing applications with a new approach to network bootstrapping. EigenLayer facilitates users in re-staking their LSD tokens, amassing security resources, and extending them to these applications. As a result, users garner additional rewards, the efficiency of capital utilization within the entire ecosystem is elevated, and applications save time and effort in building their security measures. This synergy creates a situation beneficial to all parties involved.

Maximal Extractable Value (MEV) refers to the maximum value that can be extracted from block rewards and gas fees by validators through altering transaction sequences. MEV is often exploited by arbitrage bots using strategies like sandwich attacks(front-running), negatively impacting retail users. Consequently, several protocols aim to address this issue, one of which is Manifold Finance.

Manifold Finance utilizes its SecureRPC to offer a service called OpenMEV, redistributing MEV profits. The protocol plans to launch mevETH, sharing the MEV yield with stakers and providing an additional yield source. This development could further promote the growth of the LSD market.

4. Growth Drivers

We believe that the potential for LSD market growth can be attributed to following factors: low current ETH staking participation, infrastructure development reducing slashing risk, staking rehypothecation encouraging re-staking activity, potential for institutional inflow based on stable ETH staking yield, and the “yield wars” where platforms attract users by offering extra yields.

4.1 Low Current Participation

As previously mentioned, the current ETH staking ratio is significantly lower compared to other chains, which have ratios 2–5 times greater than Ethereum.

It is reasonable to infer that the ETH staking ratio has considerable upside potential and virtually no downside. The current underwater ratio for stakers is 72.4%, and the Shanghai Upgrade has eliminated withdrawal uncertainty, making a decreased staking ratio scenario in the future highly unlikely. Additionally, data from the Dune shows that ETH staking activity continues to grow and has experienced a steep increase following the Shapella upgrade.

4.2 Infrastructure Development

The development of core infrastructure like DVT is a vital factor contributing to the growth of the LSD market. DVT’s primary benefit is the significant reduction of slashing risk. Slashing can negatively impact the ecosystem, causing staking activity to concentrate in larger pools or protocols, as smaller entities are more adversely affected when slashing occurs. By mitigating slashing risk, DVT enhances staking performance and improves the staking efficiency of liquid staking protocols, fostering a more decentralized environment. As DVT gains widespread adoption, the network becomes more resilient, and the LSD market grows stronger.

4.3 Staking Rehypothecation

The re-staking narrative introduced by EigenLayer holds significant potential, as it can create a flywheel effect within the LSD ecosystem. Utilizing the pooling security of EigenLayer, projects, and applications can minimize the cost of building a security infrastructure, attracting more developers. As adoption increases, rewards for users participating in re-staking also grow. The yields can be further enhanced with LSDFi protocols, leveraging DeFi’s compounding composability, ultimately driving more re-staking activity.

4.4 Institution Inflow

Despite facing risks such as network and slashing risk, the yield from ETH staking is still seen as the closest measurement for the risk-free or benchmark rate in the Ethereum ecosystem since it is arguably the most stable yield source on Ethereum which will promote the development of cryptocurrency asset pricing theory, then could potentially trigger the next wave of institutional adoption.

When compared to the risk-free rate in traditional finance, like the yield on a 10-year Government bond, the ETH staking yield carries more uncertainty. Additionally, the US Government Bond Yield is currently at a high point in recent years, making the ETH staking yields less attractive in comparison. However, government bond yields are likely to decrease over time, and the crypto market could enter a bullish phase in the future again. As a result, ETH staking could become more attractive.

For institutional investors, BTC and ETH are often the first choices and a stable yield like that from ETH staking aligns well with their needs. At this juncture, a bull rally for the LSD sector could occur, spurred on by significant capital inflows.

4.5 The Yield Wars

The underlying yield for ETH staking is the same across all platforms; therefore, the most effective way to attract users is by providing extra yields. Frax Finance is a prime example, as its liquid staking product offers additional yields, resulting in rapid growth over the past few months. Yields in the LSD market can be categorized as follows.

4.5.1 Vanilla ETH Staking

This basic staking yield is uniform across different protocols, leading users to choose reputable platforms like Lido Finance and Rocket Pool, as their LSDs have greater liquidity in DEXes and more use cases in the DeFi landscape.

4.5.2 Leverage Lending

Leverage lending involves using money market protocols like Aave to perform looping and earn leveraged yields on LSD positions. The risk of this method is liquidity issues during de-leveraging. Actual pool liquidity may be smaller than it appears, as leverage inflates liquidity. When large positions exit, a rush to leave may result in inadequate liquidity, creating a downward spiral.

4.5.3 Governance Incentives

Frax Finance effectively uses its voting power in Curve to direct more rewards to its frxETH/ETH pool. Another notable example is Yearn Finance’s yETH. As Yearn holds more voting power in Curve, the protocol is likely to provide higher yields. However, Yearn and Frax do not directly compete since yETH’s underlying assets comprise a basket of LSDs, including frxETH. Thus, yETH serves as a yield-enhancing product for Frax’s users.

4.5.4 Aggregator

An intriguing aggregator example is bestLSD, an LSD yield aggregator protocol that aims to maximize yield by combining real yield with liquid staking. By auctioning the protocol’s governance tokens in exchange for yield-bearing tokens such as GLP, veCRV, and veVELO, bestLSD can provide boosted yields to its users.

4.5.5 Yield Trading

Pendle Finance enables users to trade yields by splitting yield-bearing assets like LSD into Principal Tokens (PT) and Yield Tokens (YT). Through Pendle, users can execute several strategies:

Locking Yield: Users buy PT and redeem the underlying token at maturity. Profits result from the discount when buying, effectively locking in the yield.

Long Yield: Users buy YT when the implied APY is undervalued.

Yield Trading: Users speculate on the dynamics between the underlying APY and the implied APY of specific yield-bearing assets.

In short, Pendle allows users to increase capital efficiency by managing yield.

4.5.6 Structured Products

Structured products are customized investment instruments comprising various financial assets, such as fixed income, derivatives, equities, and commodities. These products cater to tailored risk-reward profiles and offer benefits like principal protection and yield enhancement. As LSD can be viewed as a fixed-income position, protocols like Shield provide LSD-structured products by combining LSD and options strategies. The protocol offers two types of LSD staking: Aggregate Staking and Option-Boost Staking. Aggregate Staking deposits staked ETH into Curve’s pool, generating LP rewards in addition to the underlying LSD yield. Option-Boost Staking, built upon Aggregate Staking, allocates staking rewards to an options strategy called Wedding Cake, increasing yield potential while protecting the principal.

5. Market Value Prediction

The growth of the LSD market value is heavily dependent on the expansion of the ETH staking percentage, in addition to other factors such as the growth of the LSD market share and fluctuations in the ETH price. Given the more mature staking conditions of other PoS chains, we can conduct a forecast by employing a combination of comparable and scenario analysis.

Scenario analysis is a method used to assess the potential impact of various factors that could influence future results of a project/investment. Given the dynamic nature of the crypto industry and the emerging status of the LSD sector, this method helps to accommodate uncertainty and fluctuation in potential growth, provideing a broader perspective of possible outcomes.

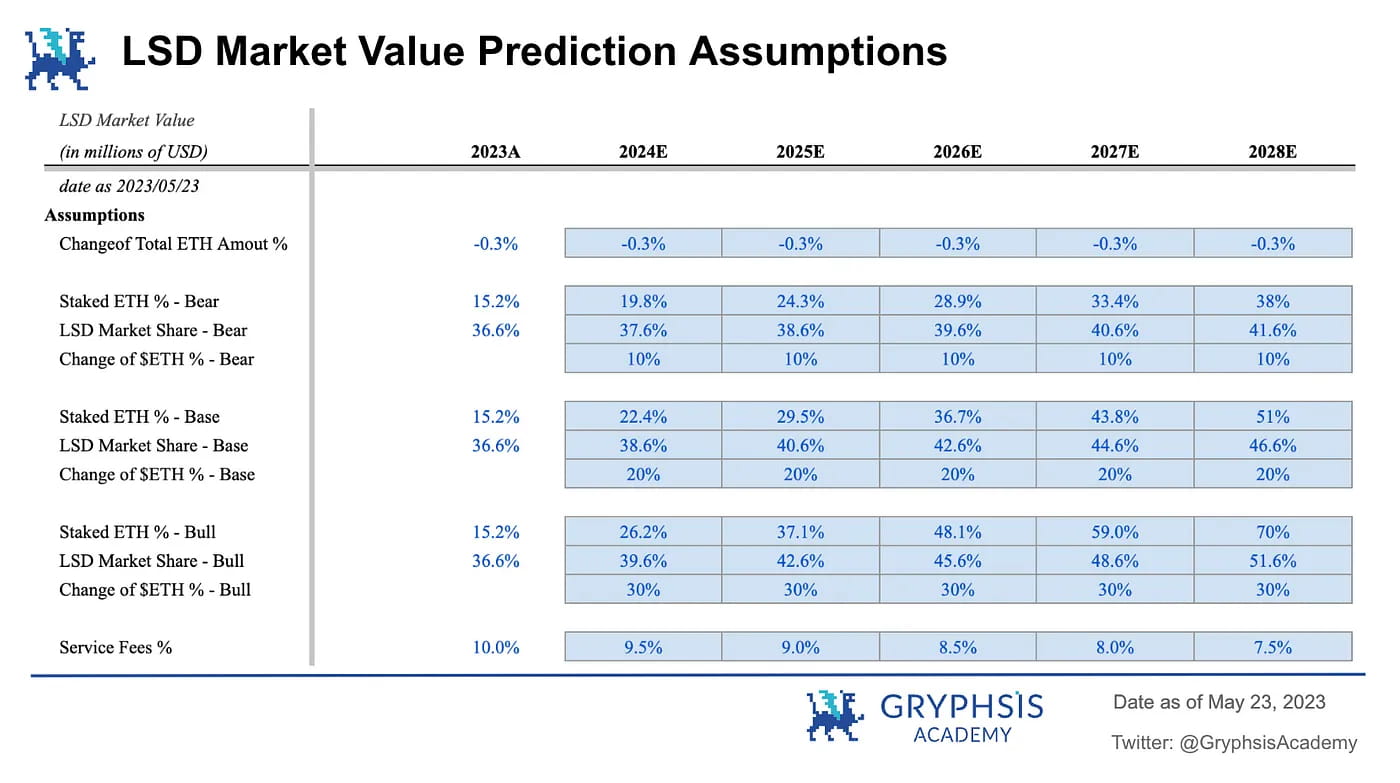

5.1 Assumption

The forecast is founded on a set of core assumptions. These premises signify the primary elements influencing the expansion of the LSD market value and are adjustable in our market value prediction model. Below is an overview of these assumptions along with detailed explanations for each.

Change of Total ETH Amount %: Change of Total ETH Amount % is how many ETH is in circulation. Post-Merge, Ethereum has become a non-inflationary asset, expected to deflate in the coming years. Therefore, this model uses Ultra Sound Money’s ETH supply growth rate projection (-0.3%) for this metric. The projection is based on the dynamic interplay between PoS rewards for stakers and the burn rate. Even if the number of validators increases in the upcoming years, potentially inflating the reward emissions, gas burning is likely to continue. Given the supply growth rate remains deflationary in the current market state, this model uses a -0.3% supply growth rate projection for the next five years.

Staked ETH Percentage: Staked ETH percentage is the most significant factor impacting the market value growth as it directly affect the potential growth of the circulating LSDs amount. The increased of staking ratio will be driven by the low current participation and the ETH staking rewards, which is higher than those of other networks, indicating that the network can accommodate a substantial number of additional stakers before equilibrium is reached. To account the uncertainty, the models uses bear, base, and bull cases to give a more comprehensive estimation.

Bear case: ETH staking ratio grows to the same as Polygon, which has a relatively lower staking ratio compare to other PoS chains. This suggests the demand for staking could be lower than initially anticipated.

Base case: ETH staking ratio reaches parity with the median ratio of other PoS chains. This implies that Ethereum’s staking ratio has significant growth potential and may increase at a faster rate than some other PoS chains, despite its comparatively shorter existence in the PoS mechanism landscape.

Bull case: ETH staking ratio grows to match Solana, the current leader in staking percentage. This suggests that Ethereum has the potential to become the single most dominant blockchain network. Despite its already widespread adoption, this scenario hinges on the continued surge in cryptocurrency adoption worldwide.

LSD Market Share: The market share of LSD is another fundamental factor in evaluating market value. With its benefits, including low entry barriers and diverse use cases, pool staking is projected to showcase sustained growth. The model designates 1%, 2%, and 3% for bear, base, and bull scenarios respectively. However, this projection is relatively conservative. The appeal of pool staking could be amplified as the LSD market continues to evolve, particularly within the LSDFi sector.

Change of ETH Price: Change of ETH Price: The fluctuation in ETH price plays a significant role as it can directly influence users’ propensity to stake their ETH. As the price rises, confidence in ETH’s future strengthens, leading to more active participation in staking activities. Additionally, price escalation could stimulate the expansion of the DeFi market, potentially unveiling more LSD earning opportunities. The model designates changes of 10%, 20%, and 30% for bear, base, and bull scenarios, respectively. In the base scenario, we assume that the ETH price would reach approximately $4,603 in five years, matching the peak price of the last bull market. This assumption reflects a modest market growth coupled with a certain degree of price recovery. The ETH price in the bull scenario would reach $6,800 in five years, aligning with other bullish projections that foresee substantial growth in both LSD and overall crypto adoption. Thus, the ETH price should be capable of surpassing its previous all-time high.

Service Fee: While not directly incorporated into the construction of the forecast model, the service fee plays a crucial role in exhibiting the potential of the LSD market. The profitability of protocols is a fundamental factor, particularly with the advent of the “Real Yield” narrative. The model employs a starting point of 10%, the rate levied by Lido. As competition intensifies, it is expected that this rate will decrease. Therefore, the model assumes a gradual reduction of 0.5% each year over the next five years.

5.2 Prediction

Base Scenario: Based on these factors, the base case result projects a possibility of substantial three-digit percentage growth in the mid-term, with a potential for reaching six-digit growth over the next five years.

Staked ETH Projection: Following the construction of the model, the projection of staked ETH emerges as the primary result. The outcomes suggest that even under the most conservative scenario, the amount of staked ETH could still witness a growth of 250% in five years. Furthermore, in an optimistic scenario, this figure could rise to as much as 560%, underscoring the immense potential of this emerging sector.

Service Revenue Projection: Comparable to the projections for staked ETH, the service revenue estimate also displays remarkable potential. Even under the bear case scenario, the service revenue could still realize close to 300% growth. In the bull case scenario, this value could skyrocket to 1564%. This impressive potential profitability suggests a high likelihood of the emergence of robust ‘real yield’ protocols within the sector.

Probability Weighted Market Value: To wrap up the forecasting, the model amalgamates the outcomes of the three scenarios, assigning a 50% weight to the base case, and 25% each to the bear and bull cases. This methodology helps determine the potential upside of the LSD market value growth over the next five years. The results signal a remarkable seven-digit growth in market value, underlining the substantial potential of this emerging sector. However, it’s important to note that achieving high staking percentage conditions might not be as straightforward as it seems, and growth in LSD market share may take time. The market will eventually reach an equilibrium influenced by multiple factors, necessitating extensive observation under various market conditions.

6. Core Protocols

6.1 DVT

SSV Network and Obel Network are the two major players of the DVT sector. Both of them are dedicated to decentralized the ETH staking. SSV is building a decentralized, open-soure ETH staking network powerd by the DVT. SSV is the fastest developeing DVT protocol as it is close to mainnet lauch and Lido has joined the SSV pilot program. SSV is also the only DVT protocol that has launched its native token.

Obel Network is a protocol aiming to foster trust minimized staking via multi-oprator validation. Obol has two core features, DV Launchpad and Charon. DV Launchpad is used for the facilitation of distributed validator keys generating among remote users. Charon is a GoLang-based HTTP middleware used for facilitating collaboration between Ethereum validator clients, transforming them into a cohesive, distributed validator network. On January 2023, Obel has completed a funding round of 12.5M co-led by Pantera Capital and Archetype, with participation from Coinbase Ventures, Nascent, BlockTower, etc.

6.2 Pool Staking

Lido Finance and Rocket Pool currently dominate the pool staking sector within the Liquid Staking Derivatives (LSD) market. As the market continues to grow, it is likely that these two protocols will maintain their leading positions. However, it is crucial to recognize that the DeFi landscape is constantly evolving, with new competitors emerging to challenge the incumbents.

Rocket Pool has larger potential for growth due to its current market share. On the other hand, Lido Finance’s strong moats may help it stay ahead of the competition, but it is essential to be prepared for the possibility that its market share may gradually decrease as new competitors enter the space.

6.3 LSDFi

Aura Finance is an important LSDFi protocol to watch in the evolving landscape of the LSD market. Liquidity is the lifeblood of LSD protocols. Without liquidity, a protocol’s LSDs may fail as the peg between LSD and ETH can’t be maintained, which would make it unappealing to hold. Before Shapella, the liquidity war for the LSD market started on Curve Finance, with protocols like Lido and Frax fighting for deeper liquidity for their LSD pools. Now, a new battlefield has emerged on Balancer. Four of the top 5 pools on Balancer are LSD-related pools, indicating that the protocol has become another main trading venue for LSDs.

To sustain their liquidity pools on Balancer, similar to the Curve example, protocols will need to gain voting power by accruing veBAL. Like Convex is to Curve, Aura Finance is the yield optimizer for Balancer. As the LSD market continues to develop, the position of Aura Finance will become increasingly critical.

7. Idea Expression

7.1 Beta Play

Given its significance to the industry and considerable potential for market value growth, the LSD sector can be an excellent choice for risk-averse investors seeking moderate returns. One approach is to emulate the strategy of Exchange Traded Funds (ETFs) and construct a portfolio comprising different LSD-related tokens. ETFs have been one of the most popular investment approaches for retail investors in traditional finance, given their diversification benefits, low cost, and stable Beta returns. Since picking tokens and timing the market can be challenging for most retail investors, this method is an effective way to capitalize on the growth of the LSD sector.

Two common ways to build an ETF-like portfolio are Market Capitalization-weighted and Equal-Weighted methods. The former allocates the weights of each token proportional to its total market value, reflecting market consensus but potentially overexposing large projects. The latter assigns the same proportion of the portfolio to each token, increasing the potential returns but possibly leading to overexposure to riskier protocols. Based on their risk tolerance, investors can decide on the weighting method and the LSD sectors they should include in their portfolios.

7.2 Alpha Seeking

For investors with a high tolerance for risk, and who are seeking alpha, the LSD market also offers numerous opportunities. Based on the current landscape, pool staking is already mature, while infrastructure and re-staking are still in their nascent stages. Hence, LSDFi might be the area to prioritize.

As protocols vie for market share, they are enhancing yields, potentially leading to ponzinomics opportunities reminiscent of those during the DeFi Summer. The potential returns could be substantial, but this approach necessitates diligent sector observation and prudent risk management. It’s crucial to keep in mind that high-risk investment strategies are not suitable for everyone, and one should always consider their personal risk tolerance and investment goals before diving in.

8. Outlook

The future of the Liquid Staking Derivatives market appears promising, as it is expected to continue growing and evolving. Key sectors to monitor include the underlying infrastructure, LSDFi, and re-staking protocols, which are still underdeveloped compared to traditional pool staking.

Although the growth potential seems significant, numerous factors contribute to this expansion. It is essential to closely follow the market to assess its current state and potential future direction. For now, based on current trends, we can maintain an optimistic outlook for the overall LSD market.

References

Bankless, EigenLayer: the Harbinger of Restaking(2023)

LD Capital, Stability and High Growth of LSD(2023)

@Wayne24699837, https://twitter.com/wayne24699837/status/1637165157939056642?s=61&t=dLproOHuQ34C-TwIawjowA

Declaration

This report was written by @BC082559, a trainee of @GryphsisAcademy, and guided by @CryptoScott_ETH and @Zou_Block, mentors of Gryphsis Academy. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Gryphsis Academy or the organization that requested the report. Readers do not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report. This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results.