For traders in the global market, the past week can be described as a 'Game of Ice and Fire.' One moment, the market was anxious about the impact of artificial intelligence on employment; the next moment, the sudden outbreak of conflict in the Middle East completely dominated the headlines.

Tonight (March 6) at 21:30, the highly anticipated U.S. February non-farm payroll report will be released as scheduled. However, on this special 'non-farm night,' everyone's attention must be divided, closely watching the smoke billowing over the Persian Gulf. As a geopolitical black swan collides with the economic data gray rhino, the Federal Reserve's monetary policy is facing an unprecedented dilemma of being 'caught in the middle.'

One, the 'gunfire' and 'oil fire' in the Strait of Hormuz.

One, the 'gunfire' and 'oil fire' in the Strait of Hormuz.

Just before the non-farm data is released, the situation in the Middle East escalates once again.

● On March 5 local time, Hezbollah claimed to have used guided missiles to hit the gathered Israeli Defense Forces. Even more alarming for the market is that the Iranian Revolutionary Guard announced it has launched missiles hitting a U.S. tanker in the northern Persian Gulf, clearly drawing a red line: prohibiting U.S., Israeli, and European vessels from passing through the Strait of Hormuz.

● The Strait of Hormuz, the 'great artery' of global energy, means that any slight disturbance will directly translate into 'war premiums' in oil prices. Since the outbreak of the conflict, international oil prices have risen nearly 20%, with WTI crude briefly surging to $77 and Brent crude nearing the $85 mark.

● On the surface, this appears to be a military strike; in reality, it is the 'oil fire' that ignites the inflation fuse. The surge in energy prices is like 'high blood pressure' in the economic field, causing the Federal Reserve, which just saw a glimmer of cooling hope, to become tense instantly. After all, according to estimates by the International Monetary Fund (IMF), every 10% increase in oil prices will push global inflation up by 0.4 percentage points.

Two, the Federal Reserve's 'zero interest rate cut' script: from 'possible' to 'mainstream'.

● If a week ago, the market was still debating whether there would be two or one interest rate cuts this year, now, a more extreme scenario is taking center stage — a year of 'zero interest rate cuts', and even reignited expectations for interest rate hikes.

● Data from the Atlanta Fed as of Wednesday revealed this shocking expectation reversal: traders are betting that the probability of the Federal Reserve maintaining interest rates unchanged before the end of the year has soared to 25%, up from 17% the day before the conflict broke out. Among all sub-scenarios, 'holding steady' has become the most probable outcome. More extremely, the market even believes that the probability of a rate hike has risen to 16%, doubling from 8% last Friday.

● This abrupt change in sentiment directly ignited the bond market. U.S. Treasuries, as a safe-haven asset, faced rare selling, with the 10-year Treasury yield once soaring past 4.1%, completely overturning the traditional logic of 'safe-haven funds pouring into U.S. Treasuries'. Dongfang Jincheng analysts pointed out that the core reason lies in the market's concern has rapidly shifted from 'risk aversion' to 'inflation defense'. In the face of input inflation caused by rising oil prices, investors demand higher yields to compensate for future losses.

● Richmond Fed President Barkin's speech was like a cold shower for the market. He pointed out that the recent strong employment, combined with sticky inflation and the Middle East conflict, could further push prices up, changing the 'risk outlook' faced by the Federal Reserve. Fed Governor Bowman also bluntly stated that the labor market is stabilizing, supporting the decision to maintain interest rates at the next meeting.

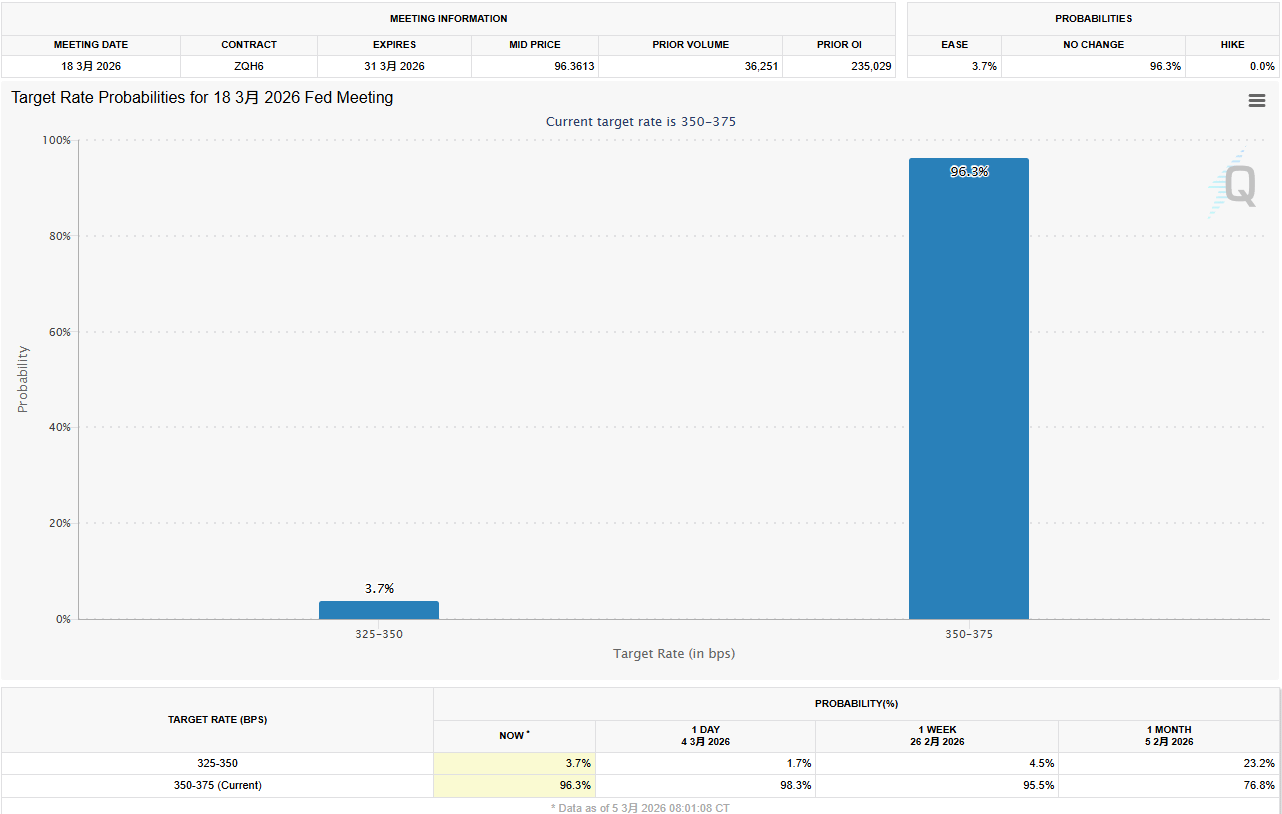

● Currently, the CME's FedWatch tool shows that the probability of maintaining interest rates unchanged in March has exceeded 97%. That once-coveted 'March rate cut' has basically been declared dead under the double pressure of war and data.

Three, the 'data trap' of 'non-farm night': could weakness actually be a good sign?

In such a tense geopolitical atmosphere, tonight's non-farm data seems somewhat 'misaligned'.

The market generally expects that February's increase in non-farm employment will slow significantly to around 60,000 (with some expectations at 59,000), far below January's 130,000, while the unemployment rate is expected to remain at 4.3%. The ADP report released on Wednesday showed that U.S. businesses added 63,000 jobs in February, slightly exceeding expectations, but still indicating that hiring activities are concentrated in healthcare, education, and other few industries, with growth not being widespread.

There exists an interesting 'data trap':

● If the data is too strong (such as an increase of over 100,000): combined with previously strong inflation, the market will further strengthen the expectation of a 'no landing', and with rising oil prices due to the Middle East, the Federal Reserve will not only refrain from cutting rates but may even be forced to discuss the dire situation of 'hiking rates again'. This would be a significant blow to risk assets.

● If the data is moderate or even weak (such as in line with expectations or lower): it may instead become the 'lifeline' for the market. A cooling employment report can at least prove that the economy is not overheating, allowing the Federal Reserve to still have reasons to interpret the current 'wait-and-see' stance as 'observation', rather than being forced to shift to tightening.

Ben Ayers, a senior economist at Nationwide Insurance, expects hiring to be weaker, with only an increase of 40,000, reflecting the current environment of 'low hiring, low layoffs'.

Four, besides the data, also keep an eye on these two details.

In addition to the headline numbers, tonight's analysts will also focus on two other key points:

● The breadth of employment: January's strong performance was mainly driven by healthcare and social assistance. If February's hiring can expand to more industries, it indicates strong endogenous economic momentum; if it remains concentrated in a few sectors, caution should be taken regarding the fragility of the recovery.

● Unemployment rate for specific groups: Comerica Bank's Chief Economist Bill Adams pointed out that the unemployment rates of Black individuals and young people often serve as leading indicators of a weakening labor market. These two data points fell back in January, and if they can continue to improve in February, it will be a real 'stabilizer' for the labor market.

Five, Yellen's warning and the worst-case scenario.

● Regarding the current situation, former Federal Reserve Chair Yellen provided a rather pessimistic assessment: this conflict could both raise U.S. inflation and slow economic growth. This is the classic 'stagflation' risk — the monster most feared by central banks.

● Natixis economist Hodge pointed out that if the conflict de-escalates quickly, the impact on oil prices will be limited; but if the conflict expands and drags on, with oil prices rising to and maintaining above $120, the U.S. economy could turn negative, and unemployment rates could rise. At that point, the Federal Reserve may instead be forced to cut rates quickly to respond to the recession — but this will signal trouble for the economy, rather than being a good sign for the market.

● Tonight, whether the non-farm data is 60,000 or 130,000, it is highly unlikely to enable the Federal Reserve to raise the flag for a rate cut in March. Until the gunfire in the Strait of Hormuz ceases, 'pause' will be the Federal Reserve's only and helpless choice. For investors, rather than guessing the data, it may be more important to fasten their seatbelts and embrace an era of high volatility driven by geopolitical factors.