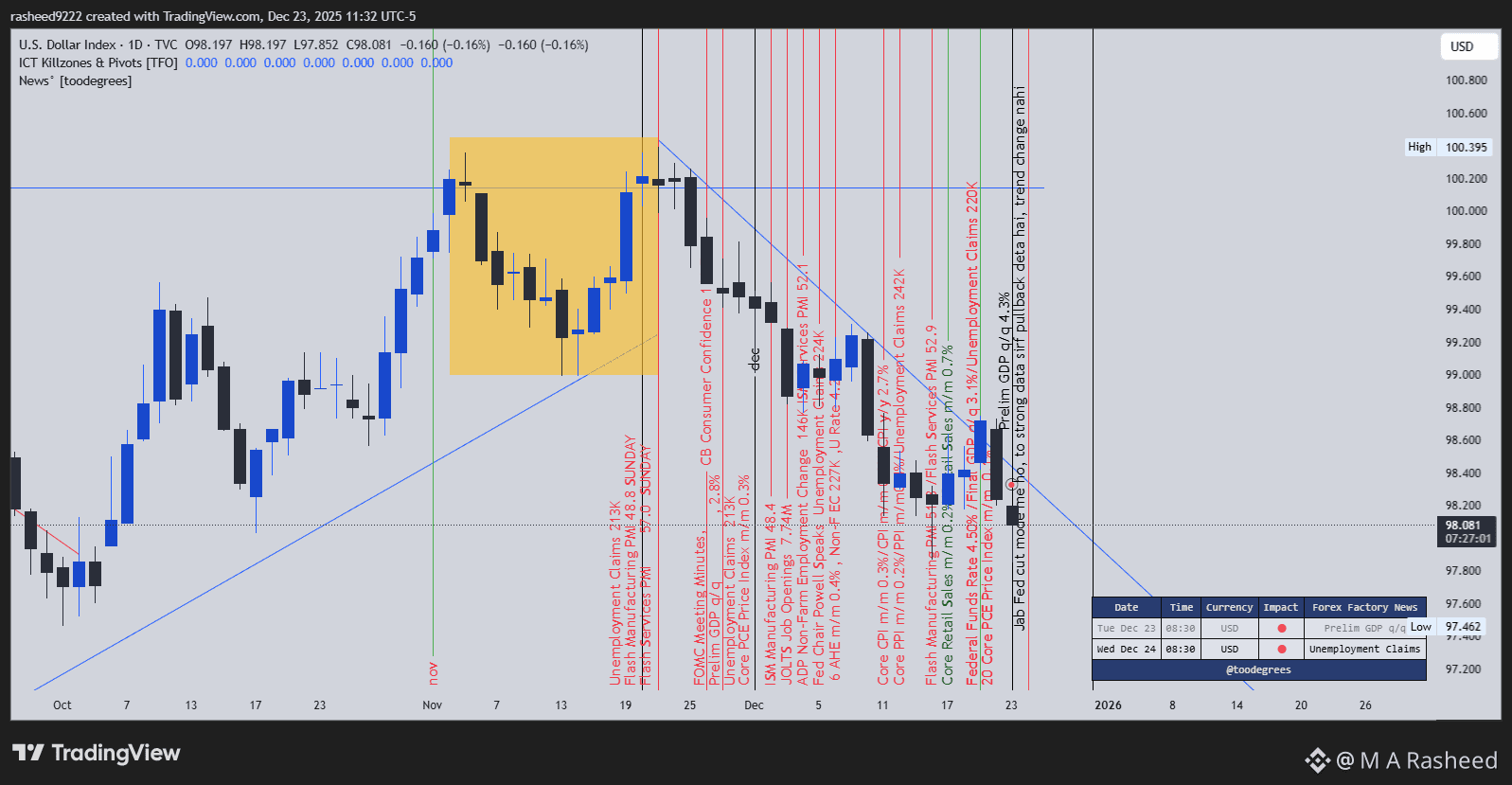

US Preliminary GDP (q/q) came in strong at 4.3%, showing that economic activity remains resilient.

However, markets are currently driven more by inflation trends and Federal Reserve policy than by GDP alone.$USD

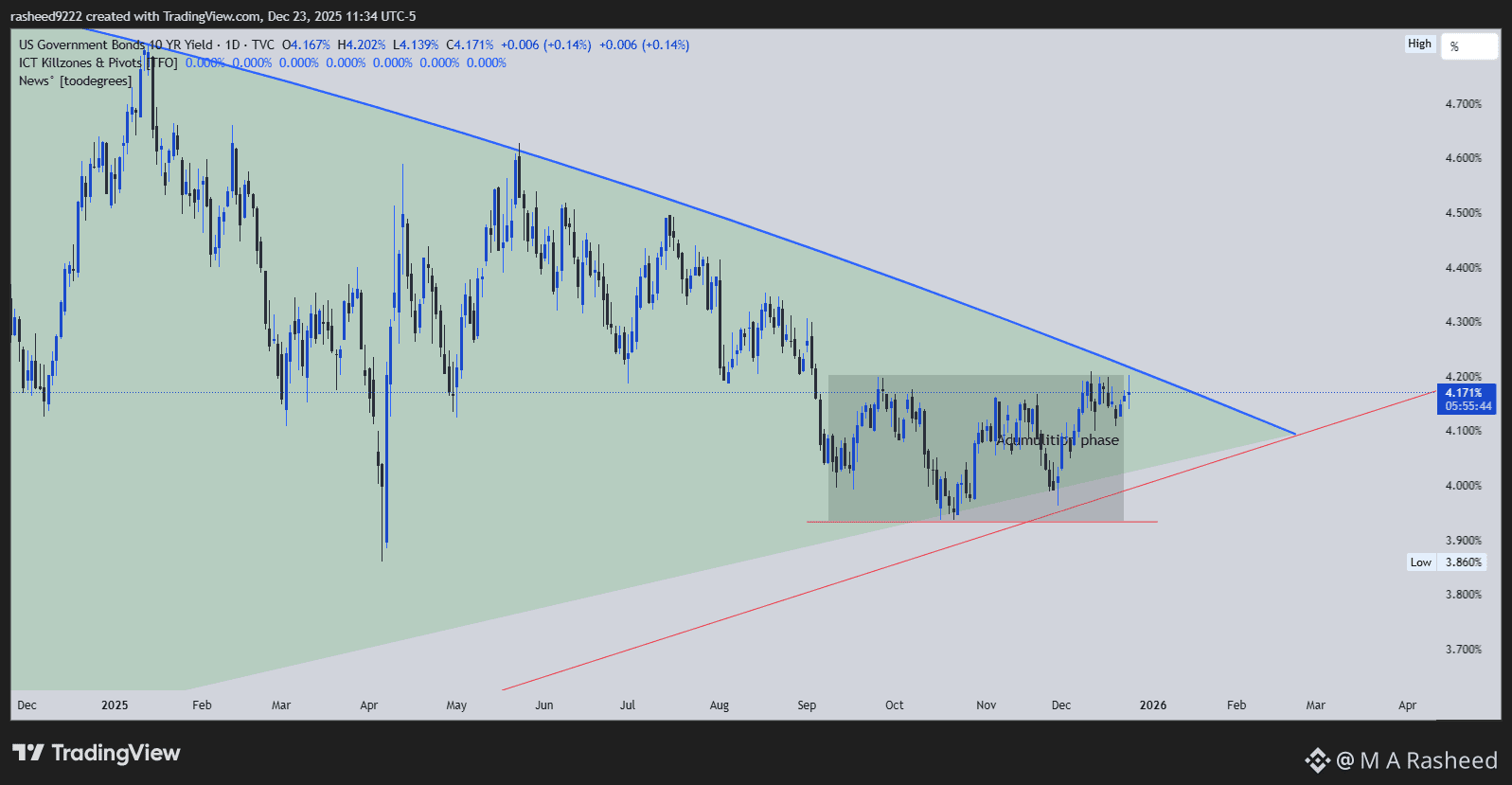

Inflation indicators (CPI/Core PCE) continue to cool, and the Fed’s tone remains dovish and data-dependent, with the policy rate around 4.5%. This keeps bond yields under downward pressure.

Despite strong GDP data, the US Dollar has only seen short-term bounces, not a trend reversal. When positive data fails to lift the USD sustainably, it signals underlying weakness.

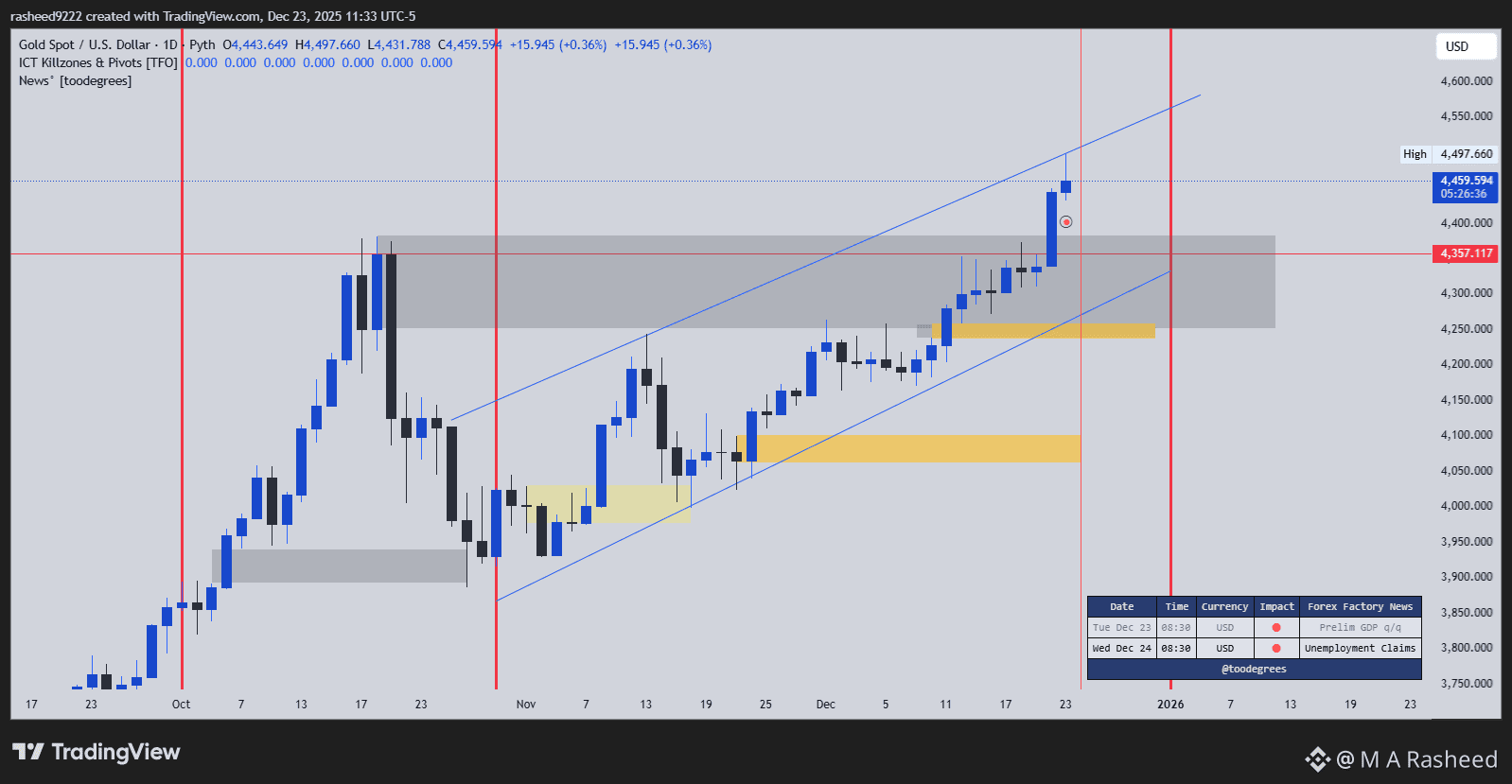

As yields fall and the USD softens, Gold remains supported, with buyers stepping in on pullbacks. The broader bias for Gold stays bullish.

Market Conclusion

Strong GDP = short-term support only

Falling inflation + Fed easing = main trend driver

Yields ↓ → USD ↓ → Gold ↑

Market direction is driven by Fed policy and inflation, not GDP headlines alone.

Markets appear to be prioritizing forward-looking policy expectations over backward-looking growth data.

This content is for educational purposes only and not financial advice.

#TrumpNewTariffs #CPIWatch #economy #GOLD #USGDPUpdate

Do you think Fed policy will continue to outweigh growth data into year-end?