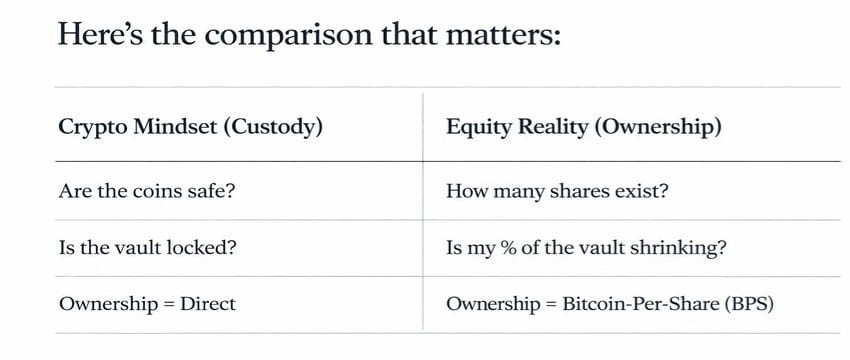

⬆️ The wrong mental model

Most investors think like crypto holders (direct ownership = safety), but in stocks, what matters is the number of satoshis per share (satoshis per share or BTC-per-share)

If the company buys additional Bitcoin at a rate of 10% but issues new shares at a rate of 20%, your share decreases despite the increase in total holdings

_ Dilution equals selling Bitcoin indirectly

Since 2020, diluted shares increased from 124.5 million to 364.8 million (growth ~193%), while the Bitcoin share per share grew ~3.5 times (from ~56,600 to ~195,700 satoshis).

But this "magic" depends on selling shares at a large premium (premium) above the Bitcoin value (NAV)

In Q4 2025, holdings rose ~5% but shares ~8%, so BTC-per-share decreased by 2-3% for the first time, despite buying more.

Issuing shares at a discount (less than NAV) = selling Bitcoin at an economic loss.3. The new layer: Perpetual preferred shares (Perpetual Preferred)

In 2025, Strategy issued preferred shares (STRK and STRF) worth ~8.39 billion dollars, with annual dividend obligations ~700+ million dollars (8-10%).

Annual software revenues ~468 million only, meaning a deficit ~232+ million annually.

The solutions: Selling Bitcoin (breaks the HODL promise)

Issuing additional common shares (dilution)

Consuming the cash reserve (~1.44 billion, runs out in ~6 years approximately)

Common shareholders are now paying high yields to preferred investors (senior claims).

_ There is no "liquidation price" but the danger is real

No secured debts or margin that forces immediate sale, but the danger is the slow death spiral: The premium disappears → stock price ≤ NAV

The need to pay dividends and debts → issuing cheap shares

Decline in BTC-per-share → panic → bigger decline → more dilution.

It happened partially in 2022 (the stock reached 0.7× NAV).

_ The three-amplifier system (that breaks down)

Stock performance depends on: Bitcoin price

BTC-per-share growth (accretive issuance)

Expansion/contraction of the premium

In a rising market: the amplifiers compound → big outperformance

In a falling/sideways market: they reverse → catastrophic underperformance

In Q4 2025, the second amplifier broke ⬇️

⬆️ The essential numbers Total Bitcoin growth: 10.1×

Shares growth: 2.9×

BTC-per-share growth: 3.5× (for long-term holders)

Current premium: ~0.94× NAV (below value)

Average Bitcoin cost: ~$76,052 (current price ~$72,000 → losses on recent purchases) ⬇️

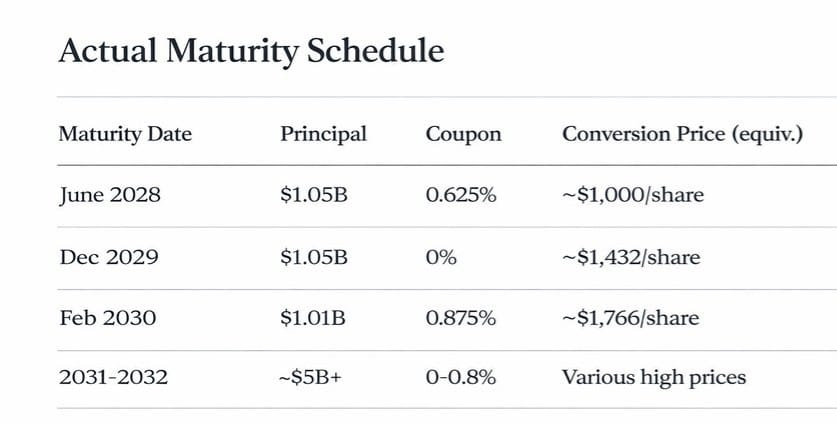

⬆️ The ticking debt clock

Convertible debts ~8.2 billion, first maturity June 2028 (30 months).

If Bitcoin does not rise enough: either cash repayment (burns the reserve), refinancing at higher interest, or issuing shares (massive dilution).8. Governance

Saylor controls 68% of the votes with only 6.3% of the economic ownership (Class B shares). His decisions (like issuing more preferred) cannot be challenged. Shareholders have no real voice.9. The four scenarios Roaring bull ($150K+): big outperformance (2-3× Bitcoin performance)

Moderate bull ($100-120K): performance close to Bitcoin with slight drag

Sideways/flat ($60-80K): underperformance 10-20% due to dilution and costs

Bear ($40K-): losses 60-75%+ (historical beta 3-4×)

1_ The comparison and common illusions

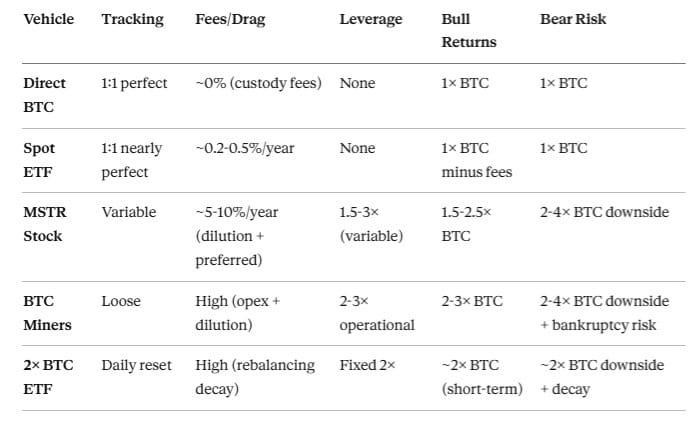

Strategy is not a 2× ETF (fixed and transparent). It is variable and discretionary leverage (human-managed), with debt risks, dilution, and concentrated governance

The illusions: "As long as they don't sell Bitcoin = no loss" → dilution reduces your share.

"Debt doesn't matter if Bitcoin rises" → timing and magnitude matter

"Like 2× ETF" → completely different

_ The only important number

Follow BTC-per-share on saylortracker monthly ↩️

It rises → the model works

It is flat → neutral

It falls → dilution dominates (as happened Q4 2025)

The conclusion and advice

Strategy is not "safe Bitcoin" or "tax-improved". It is a high-risk bet on: Fast rise of Bitcoin

Saylor's perfect execution

Continuation of the premium and open markets

It succeeded amazingly 2020-2024 (3.5× growth in BTC-per-share), but the premium collapsed, and the model stopped/broke in 2025

If you want simple 1:1 exposure → buy Bitcoin or spot ETF

If you want leverage → understand that you are sitting at a poker table run by Saylor, and the chairs may decrease even if the pot grows

The decisive question: Does your Bitcoin share increase or decrease over time? 🤔

#Saylor #SaylorStrategy #WhenWillBTCRebound #JPMorganSaysBTCOverGold