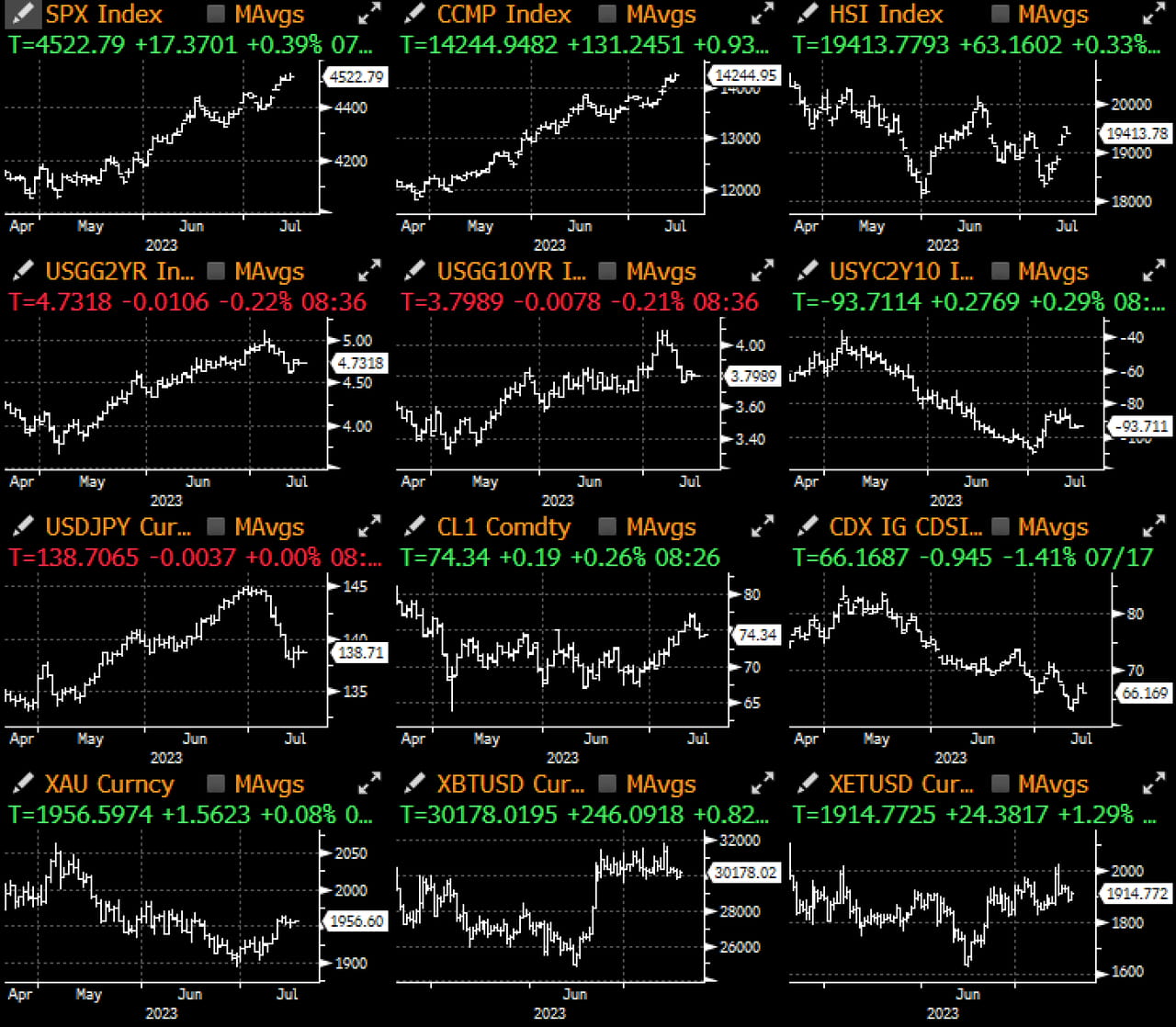

Markets are settling into full summer liquidity with Japan closed for holidays, and HK markets closed due to T8. NY markets were similarly quiet with fixed income volumes at half of normal, and markets hovering close to their Friday levels with a net risk-on bias. Another weak set of Chinese data (Q2 GDP @ 6.3% vs 7.3% expected) hurt European sentiment early on, but all was forgotten as soon as the US market walked in.

US rates dropped by ~5bp across the curve today while equities enjoyed another rally led by tech and growth names, versus rotations out of real estate and utilities. Secretary Yellen added to the risk-positive mood as she stated that while "slow growth in China can have some negative spillovers for the United States", but the US's labour market continues to be strong and she expects that the Fed is on a "good path" to bring down inflation without a major weakening in the labor market, and that the US would be able to avoid a recession.

US Financial Conditions eased materially in the past week again, thanks to the large rally in US bonds as well as a continued risk-on move in US equities as well as the trade weighted USD. Furthermore, US economic data has clearly been surprising to the upside along with a palpable improvement in the current activity data, leading to a corresponding improvement in Q2 GDP estimates.

The US economic calendar will be quiet this week except for retail sales today, with activity likely to continue falling off with Fed speakers entering blackout, and a lack of near-term Tier-1 data that's likely to change the dis-inflationary course the market has settled comfortably into.

However, just as the econ data calendar is fading, the earnings calendar will kick up a few notches with the rest of the large banks due to report this week, while Tesla and Netflix will vanguard the tech earnings after the market close on Wednesday.