The moment you realize you cannot buy a one-dollar coconut with a phone full of crypto is strangely sobering. You can move millions on-chain, interact with complex protocols, and verify transactions globally. Yet, when faced with a real-life purchase, you are powerless. That gap reveals the biggest weakness in crypto today: it still does not work naturally in daily life.

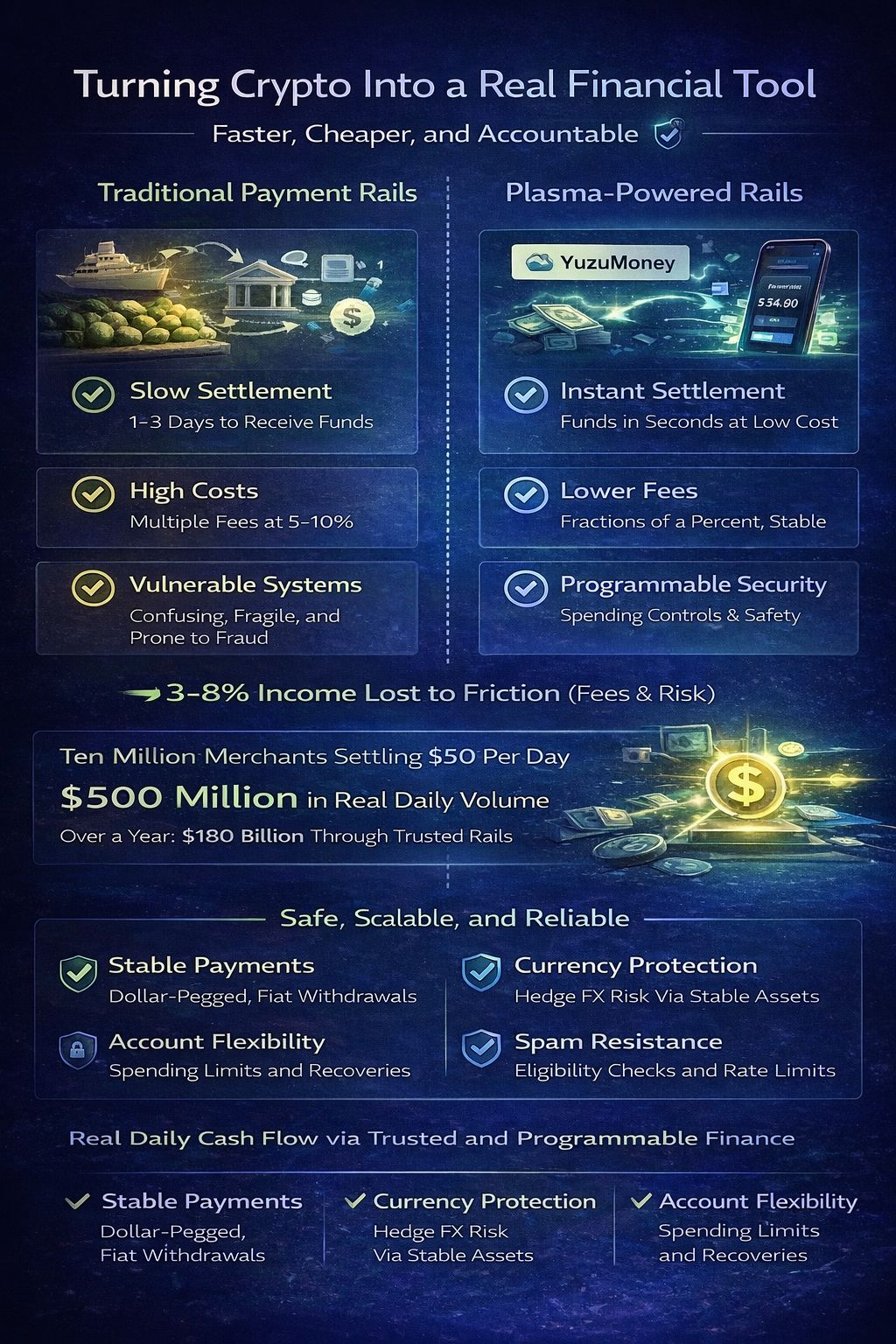

Across Southeast Asia, most small merchants rely on cash. Not because they love it, but because it settles instantly, requires no explanation, and never fails. At the same time, cash is expensive. Exchange spreads, slow settlements, theft risk, and lack of yield quietly eat into profits. Many small businesses lose between three and eight percent of their income to financial friction every year. Over time, this becomes a structural disadvantage.

Most blockchains were never designed to solve this problem. They optimized for visibility, speculation, and capital storage. They focused on how much value could be locked, not how often value could move. Payments were treated as secondary features. As a result, everyday commerce remained disconnected from on-chain systems.

Plasma approaches this from the opposite direction. Its core idea is that stablecoins should behave like real money. Transactions must be fast, predictable, and cheap. Users should not need to manage gas tokens or understand network mechanics. Payments should feel boring and reliable, just like using a card or a banking app.

Through integrations such as YuzuMoney, merchants can receive digital dollars, convert them into stablecoins, hedge against currency risk, and withdraw through banking rails. Instead of waiting days for settlement, they receive funds in seconds. Instead of losing money to intermediaries, they retain more of their earnings. This turns crypto from a speculative asset into a working financial tool.

Traditional cross-border payments illustrate the difference clearly. A small exporter sending or receiving funds internationally may wait several days and pay multiple layers of fees. On Plasma-based rails, the same transaction can settle almost instantly with minimal cost. Faster settlement improves cash flow, inventory management, and wage payments. Over time, these efficiencies compound.

Another overlooked factor is reliability. Many projects promise “free” or “gasless” transactions without sustainable controls. They collapse under spam and abuse. Plasma limits sponsorship through eligibility checks and rate controls. This discipline mirrors how successful payment networks operate. Stability matters more than marketing.

According to its whitepaper, Plasma also emphasizes account abstraction and programmable security. This enables spending limits, recovery mechanisms, and device-based authorization. For ordinary users, this means safety without technical anxiety. Losing a phone does not mean losing everything. Payments become manageable instead of risky.

If this model scales, the numbers become meaningful. Ten million merchants settling fifty dollars per day would generate half a billion dollars in daily volume. Over a year, that is more than 180 billion dollars in real economic flow. Even minimal infrastructure fees on that activity create long-term sustainability.

Plasma is not trying to replace major blockchains. It is trying to replace inefficient settlement systems that were never designed for mobile-first economies. Its competition is correspondent banking, remittance networks, and fragmented payment rails.

When you can finally buy a coconut with digital dollars without thinking, crypto will have crossed its most important threshold. At that point, it will stop being a niche technology and start being infrastructure. And infrastructure is where lasting value is built.