WAL: Bearish Tape, Still Tradable Flow

If you’re looking at WAL right now and thinking “why is this thing bleeding when the narrative is data + AI?”, you’re not crazy. As of the latest prints, WAL is around ten cents, down roughly high single digits to low teens on the day depending on venue, with about ~$165M in market cap and roughly ~$18–$19M in 24h volume. That combo matters because it tells you people are still trading it even while it’s getting sold. That’s usually where the interesting stuff hides.

Walrus Isn’t “Another Storage Coin”

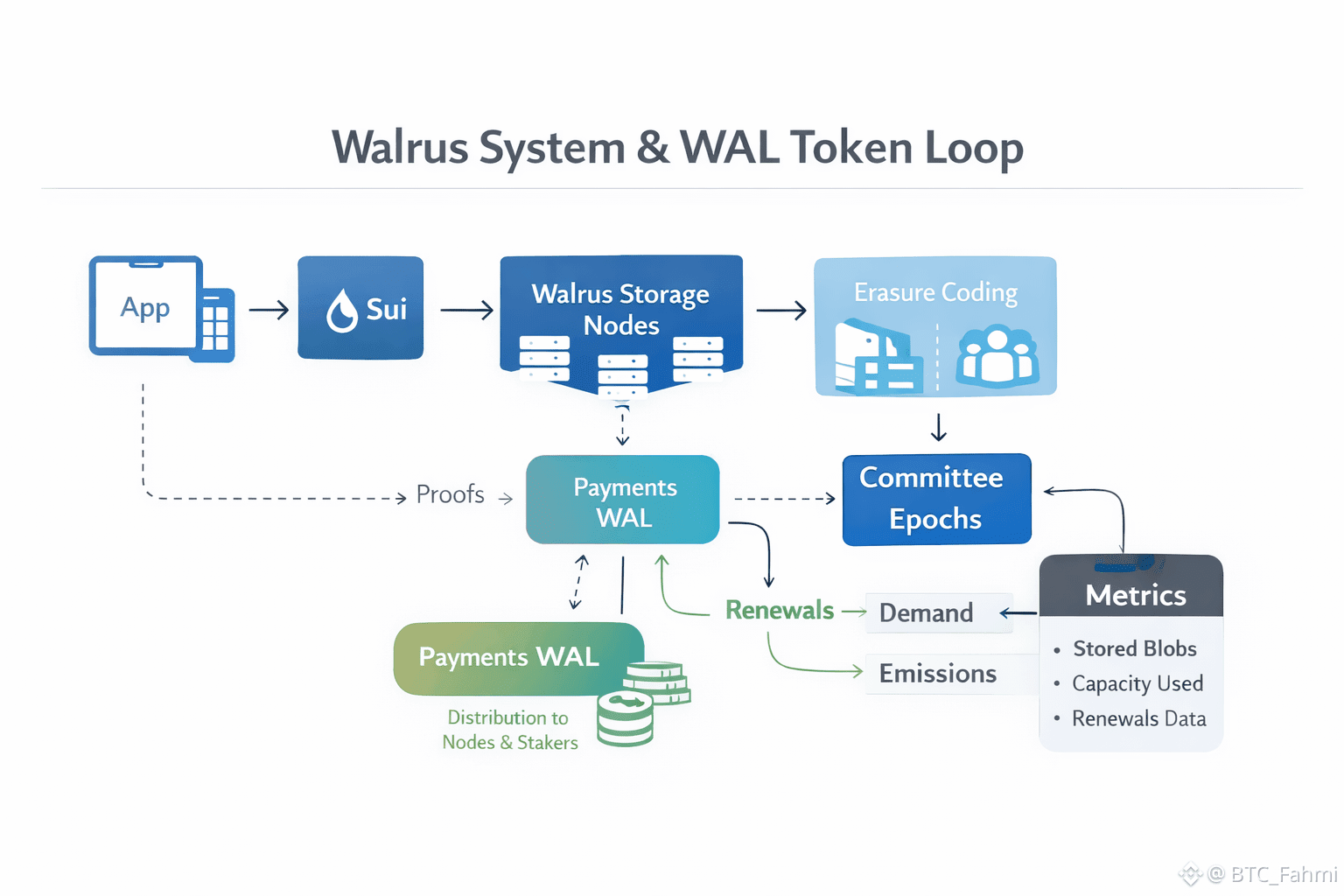

Now here’s the thing. Walrus isn’t trying to be “another storage coin.” The pitch is programmable decentralized storage, meaning the storage lifecycle is tightly integrated with Sui as a control plane, so apps can treat storage more like a composable onchain primitive than a separate offchain service with a bunch of trust assumptions. The core idea is simple: store big unstructured data as blobs across a decentralized set of storage nodes, prove it’s available, and let smart-contract logic drive who can write, who can read, how long it persists, and how payments and incentives flow.

Why This Is an App-Layer Bet in Disguise

I care about that distinction because most “decentralized storage” trades like a broad, slow thesis. Walrus is more like an app-layer bet wearing a storage costume. If Sui keeps attracting consumer apps, gaming, social, AI-agent stuff, anything that needs lots of media and user-generated content, those teams eventually hit the same wall: putting data on-chain is too expensive, and putting it on a traditional cloud makes your product easy to deplatform, easy to censor, and easy to break when the account gets flagged. Walrus is basically saying, “fine, keep the heavy data off-chain, but keep the control, proofs, and economics on-chain.”

The Part That Matters: Erasure Coding + Committee Security

Under the hood, Walrus leans hard into erasure coding and a committee-based design. Think of it like taking a file, chopping it into many pieces with redundancy, and spreading those pieces across a set of nodes so you don’t need every node to be honest or even online to reconstruct the data. In the research framing, the system operates in epochs with an elected storage committee sized to tolerate Byzantine behavior, basically the classic “n = 3f + 1” style assumption where you can survive up to f malicious nodes. That’s the boring part that actually matters, because it’s what makes “my data didn’t disappear” a property you can reason about instead of a vibe.

Token Design: Real Demand vs Circular Demand

On the token side, the part I watch isn’t “number go up.” It’s whether the payment design creates real, non-circular demand. Walrus positions WAL as the payment token for storage, and explicitly tries to keep storage costs stable in fiat terms so users aren’t forced to speculate just to store data. Fees are paid upfront for a fixed period, then distributed over time to storage nodes and stakers. If that mechanism works as advertised, WAL demand becomes tied to actual stored data and renewals, not just staking theatrics.

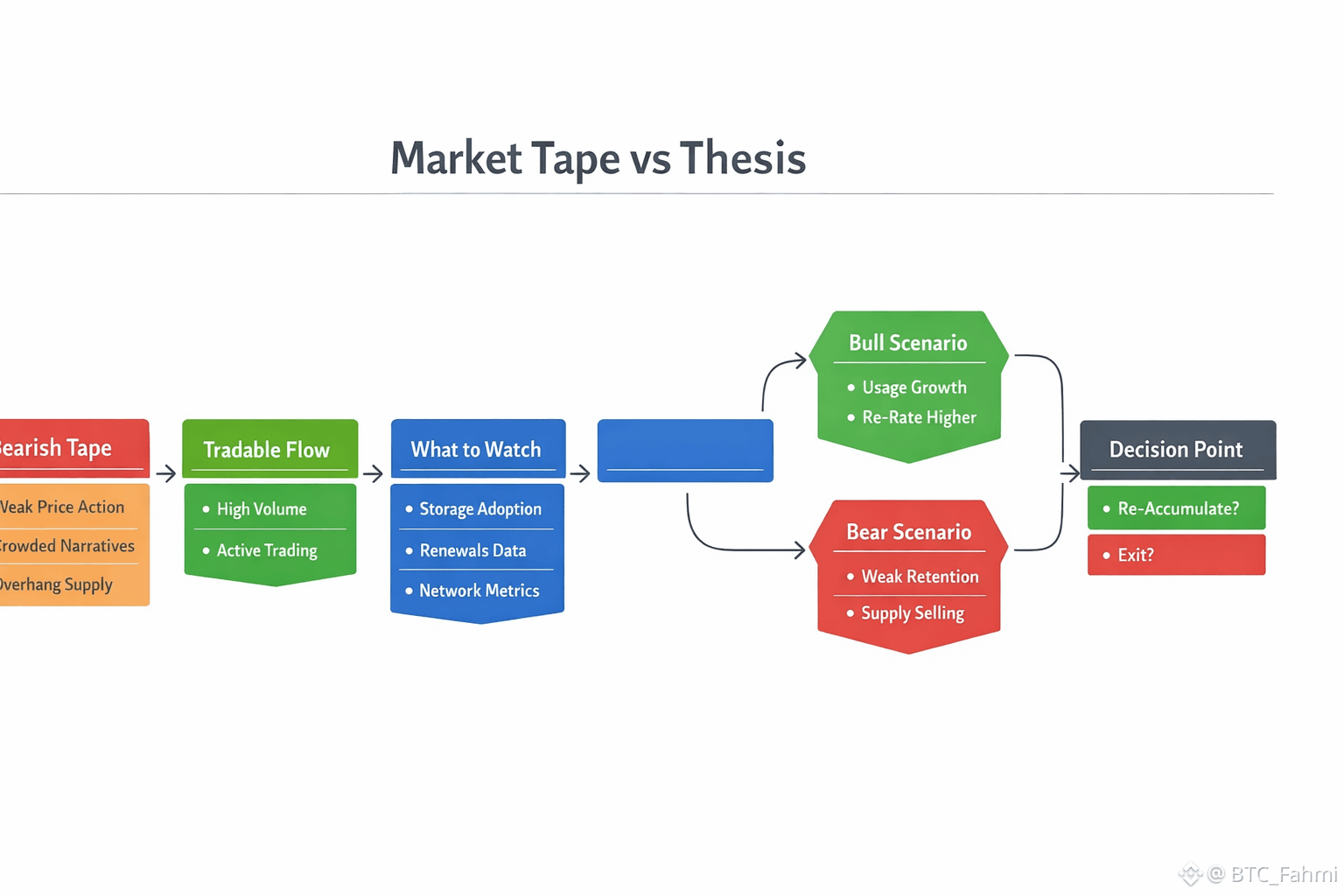

So Why Is the Market Still Leaning Bearish?

So why is the market still leaning bearish? Because storage narratives are notorious for taking longer than traders want. It’s easy to announce integrations. It’s hard to show that people are paying for storage month after month, renewing it, and building businesses on top of it. Also, WAL launched into a world where the “AI data” narrative is crowded, and you’re competing not just with Filecoin or Arweave, but with the blunt reality that AWS is cheap, familiar, and one credit card away. Walrus wins when teams value censorship resistance, composability with Sui, and provable availability enough to accept a new workflow.

Emissions, Rewards, and Overhead Supply

There’s also a very real supply and incentive overhang in any network like this. Storage networks need nodes, nodes need rewards, and rewards usually mean emissions. If WAL is sliding while volume stays decent, part of that can be organic derisking plus reward recipients selling. And if you zoom out, WAL has been way higher before, with an ATH around $0.758 in mid-May 2025 according to some trackers, so plenty of holders have overhead supply and a reason to sell into strength.

Bull Case: Usage-Linked Re-Rate (But It Must Be Earned)

The bull case is straightforward, but it has to be earned. Walrus went live on mainnet on March 27, 2025, and it’s tied closely to Mysten and the Sui orbit, plus it raised serious money (reported around $140M) which means it has runway and attention. If the network starts showing clear growth in stored data, renewals, and paying apps, you can justify a re-rate from “speculative infra token” to “usage-linked commodity.” With the current ballpark market cap (~$165M), it wouldn’t take fantasy numbers to move it. If WAL captured even a modest slice of storage spending from a handful of consumer apps that ship real volume, the market starts modeling recurring fees, not just hype.

Bear Case: Great Tech, Weak Retention, No Sticky Demand

But I’m not ignoring the bear case, because it’s obvious and it’s nasty. The bear case is that Walrus becomes a cool technical layer that developers like, but users don’t directly pay for, or they pay once and churn. Or Sui app growth disappoints, and then Walrus is fighting the broader storage incumbents without its home-field advantage. Or the economics don’t create sticky demand and instead mostly recycle incentives. In that world, WAL just trades like a risk-on alt that bleeds when liquidity dries up.

What I’m Watching: Metrics That Are Hard to Fake

If you’re trading this, what would actually change my mind in either direction is pretty concrete. I want to see network-side traction that’s hard to fake: growth in blobs stored and total capacity used, evidence of renewals (not just one-off uploads), a healthy and stable storage node set, and signs that apps are integrating Walrus as a default storage backend instead of a marketing checkbox. On price, I care less about one green candle and more about whether sell pressure compresses over weeks while usage metrics climb. If usage climbs and price still can’t catch a bid, that usually means supply dynamics are heavier than people admit.

Bottom Line: When Numbers Start Disagreeing With the Tape

Big picture, Walrus is an interesting bet because it’s trying to make data programmable in a way that fits how onchain apps actually work. If you get that right, storage stops being a side service and starts being part of the product logic. If you don’t, it’s just another token with a nice website and a long wait for demand. Right now, the tape says the market is skeptical. Your job is to watch whether the underlying numbers start disagreeing with the tape.