For a while, “buy the Mag 7” felt like a single trade.

It isn’t anymore.

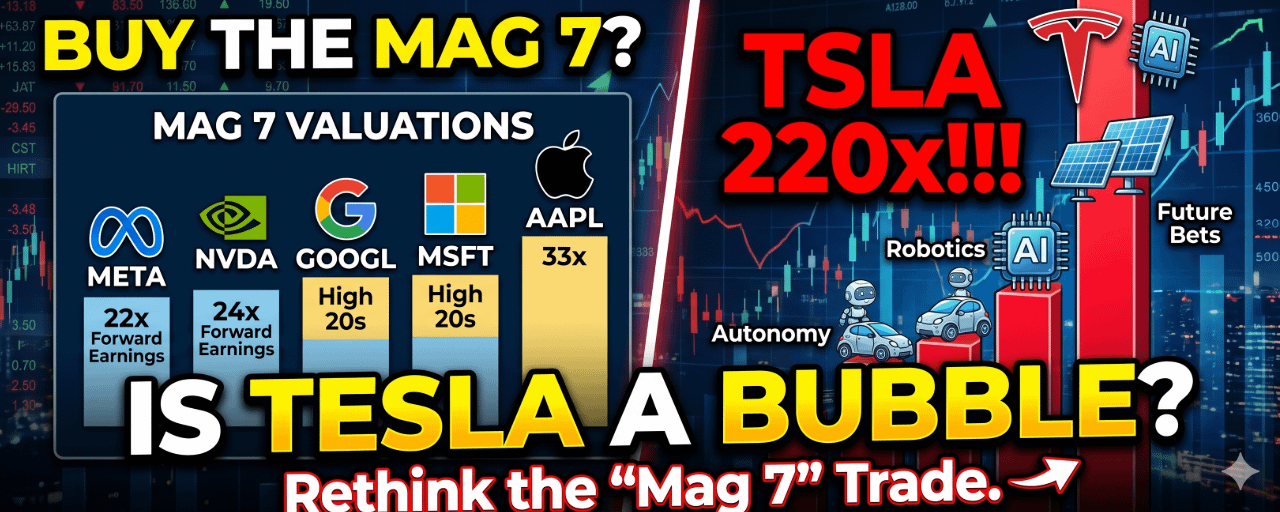

Look at the valuations.

META trades around 22x forward earnings. NVDA sits near 24x. GOOGL and MSFT are in the high 20s. Even AAPL, at roughly 33x, can at least lean on its margins and cash machine status.

Then there’s Tesla.

Around 220x forward earnings.

That’s not just expensive—it’s in a completely different category.

The rest of mega-cap tech is being priced on current earnings power plus AI upside. Tesla is being priced almost entirely on what investors believe it might become.

That distinction matters.

GuruFocus estimates Tesla’s intrinsic value at $286.58, while the stock recently traded above $420. That’s a serious gap if you trust traditional valuation models.

Wall Street looks split too.

UBS sees downside. Morgan Stanley has taken a more cautious stance. Wedbush remains bullish—but even the bull case depends heavily on autonomy and robotics becoming real businesses, not just narratives.

And then there’s the insider activity.

Tesla CFO Vaibhav Taneja sold shares recently. Insider selling alone doesn’t automatically mean trouble—executives sell for plenty of reasons—but when a stock is already trading at extreme multiples, people notice.

That’s really the core issue here.

Tesla may absolutely grow into today’s valuation if autonomy works at scale.

But if it doesn’t?

There’s far less room for error here than with the rest of the Mag 7.

The bigger point: investors need to stop treating the Magnificent Seven like one asset class.

They’re seven very different companies with very different valuation risks.

Hot take: if the AI trade cools and growth expectations reset, Tesla probably has the hardest landing.

Which Mag 7 name looks most overvalued to you right now?

#PostonTradFi #MagnificentSeven #stockmarket #TradFi #TSLA