If you bought gold $XAU above $5,000 or silver #XAG above $90 and are now watching your portfolio turn red, the pressure feels real.

Gold fell from $5,600 to $4,900. Silver collapsed from $121 to $75 in days.

Headlines synchronized instantly. Bubble. Foolish. Sell before it’s too late.

Before reacting, separate volatility from structural damage.

They are not the same thing.

1.CORRECTIONS IN A BULL MARKET ARE NOT SYSTEM FAILURE

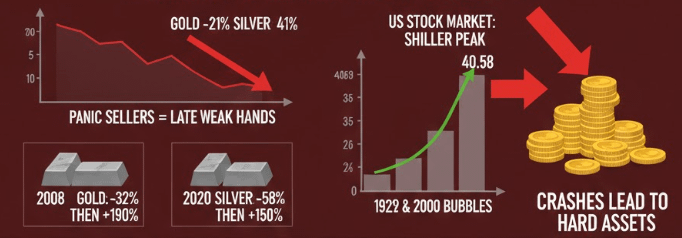

In 2008, gold fell 32% — from above $1,000 to $680.

Three years later, it reached $1,900.

In 2020, silver collapsed to $12. Within 18 months, it traded near $30.

Today’s drawdowns — gold down 21%, silver down 41% — feel extreme.

Historically, they are cleansing events.

Bull markets require liquidation phases. Excess leverage must be removed. Weak positioning must be transferred.

What looks like collapse is often inventory redistribution.

2.EQUITY VALUATIONS ARE AT GENERATIONAL EXTREMES

The Shiller PE ratio of the U.S. stock market sits near 40.58.

In 140 years, it exceeded this level only twice: 1929 and 2000.

Both preceded systemic equity collapses.

When valuation detaches from earnings reality, reversion is inevitable.

Historically, capital fleeing equity bubbles rotates into hard assets.

Gold and silver are not momentum trades.

They are counterparty-risk exits.

3.SOVEREIGN TRUST IS FRACTURING

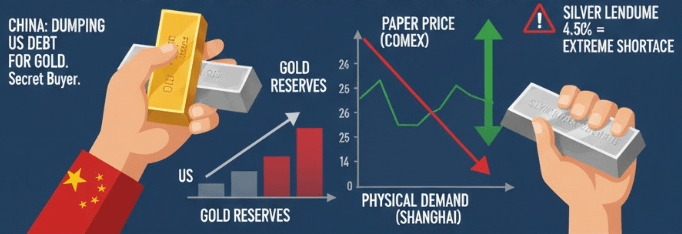

Chinese regulators have reportedly instructed domestic banks to reduce exposure to U.S. Treasuries over repayment risk concerns.

When the world’s second-largest economy questions U.S. sovereign debt stability, this is not noise.

It is structural doubt.

If capital exits sovereign bonds, it must relocate.

Historically, that relocation favors gold $PAXG .

While retail investors are pressured to liquidate, central banks continue accumulating.

The asymmetry is consistent.

4.PAPER PRICES DECLINE — PHYSICAL STRESS INCREASES

Screen prices are falling.

Physical tension is rising.

London silver lease rates recently surged toward 4.5%, signaling sourcing difficulty for deliverable metal.

The iShares Silver Trust recorded trading volumes exceeding $40 billion in a single peak session.

Dead markets do not produce liquidity wars.

Derivative markets can suppress price temporarily.

They cannot manufacture metal.

5.PRICE MOVED — THE THESIS DID NOT

Gold rebounded strongly from the $4,400–$4,600 zone.

Institutional support is visible.

Major banks continue projecting long-term targets above current levels.

Silver remains structurally above its multi-decade breakout threshold.

Volatility does not invalidate a regime shift.

It tests conviction.

6.FEAR TRANSFERS WEALTH

Large institutions accumulate during stress.

Retail investors distribute during panic.

This cycle repeats because emotion is predictable.

U.S. fiscal deficits remain structurally unsustainable.

Currency debasement continues.

Geopolitical instability persists.

None of these drivers have reversed.

Only price has moved.

CONCLUSION: PANIC IS A TOOL — DATA IS A STRATEGY

Headlines amplify fear because fear generates volume.

Volume generates liquidity.

Liquidity benefits those prepared to absorb it.

Before selling into noise, ask one structural question:

Has the macro thesis broken — or has volatility done its job?

Markets punish reaction.

They reward analysis.

🔔 Insight. Signal. Alpha.

Hit follow if you don’t want to miss the next move!

*This is personal insight, not financial advice.