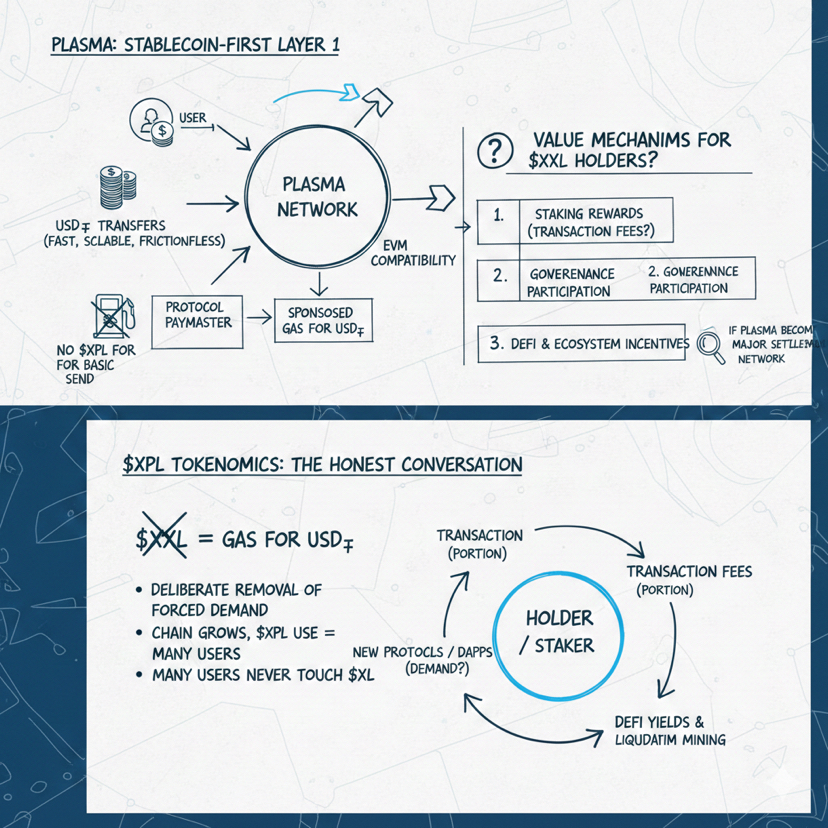

Plasma is basically trying to flip the usual crypto script. Instead of forcing everyone to hold the native token just to move around, it’s building a stablecoin-first Layer 1 where the “normal action” is sending dollars, fast, at scale, without friction. The docs lean into that idea through EVM compatibility, payment-focused design, and a protocol paymaster that can sponsor gas for specific USD₮ transfer calls so users don’t need to hold XPL just to do a basic send.

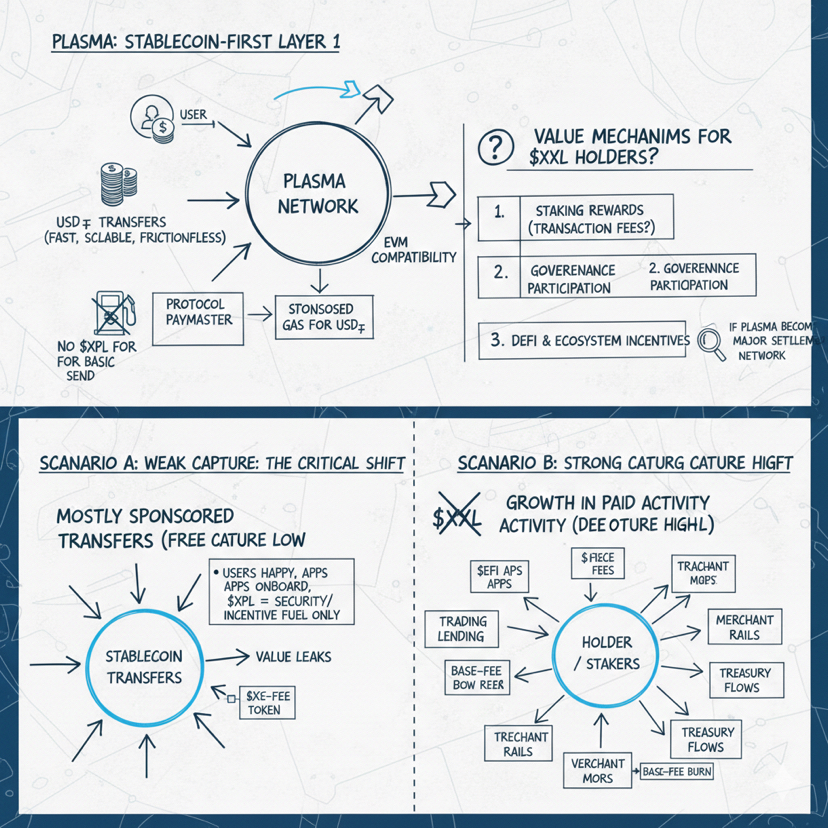

And that’s where your question gets interesting, because the tokenomics story here isn’t the usual “token = gas, therefore demand.” Plasma is deliberately removing that forced demand for the most common stablecoin action. The chain can grow in users and transfer volume while many of those users never touch $XPL at all. So the real tokenomics conversation becomes more honest and more brutal: if Plasma becomes a major stablecoin settlement network, what mechanisms actually route value back into $XPL holders and stakers?

On paper, the ownership map is clear. Plasma describes an initial supply of 10 billion $XPL, distributed as 10% public sale, 40% ecosystem and growth, 25% team, and 25% investors. That immediately tells you what kind of token this is: it’s not a token where the public float dominates the story early. The long-term outcome depends heavily on how ecosystem incentives are spent, how unlocks roll out, and whether real usage grows faster than supply entering the market.

The unlock structure reinforces that. Plasma’s FAQ states non-US public sale participants receive tokens at mainnet beta launch, while US participants have a 12-month lockup ending on July 28, 2026. Team and investor allocations follow a three-year path with a one-year cliff, meaning a large chunk becomes available after that first year, then continues unlocking monthly. The ecosystem and growth allocation is the big “engine room” bucket: Plasma says 8% of total supply unlocks immediately at mainnet beta launch, then the remaining 32% unlocks monthly over the following three years.

Now zoom out and feel what that implies in real life. In the early phase, Plasma has a huge incentive budget that can push adoption—liquidity programs, launch partners, developer grants, campaigns, integrations. That’s not necessarily a bad thing. It’s how networks bootstrap. But it creates a simple test: are users and builders staying because the chain is genuinely useful, or because there’s an incentive drip feeding activity? If the second one dominates for too long, the token can suffer even while the chain looks “active.”

So what creates real demand for $XPL if basic stablecoin sends can be sponsored? Plasma’s own design points to two main sources: security demand and fee economics. Security demand is the staking story—$XPL is meant to be the asset that secures the network through validators, with staking rewards eventually turning on alongside external validators and delegation. Fee economics is the part people usually miss: Plasma says it uses an EIP-1559 style model where base fees are burned. That’s the value capture valve. If the chain evolves into a real onchain economy where lots of activity is fee-paying—apps, DeFi, settlements, more complex contract calls—then usage can translate into burn pressure, which benefits holders by reducing supply growth.

But the burn thesis only matters if meaningful fees exist. Plasma’s “zero-fee USD₮ transfers” are not a marketing slogan; they’re implemented through a paymaster that’s restricted to transfer and transferFrom, backed by eligibility checks and rate limits, and funded by the Plasma Foundation—meaning gas is covered at the moment of sponsorship and users aren’t reimbursed later. That’s a very deliberate setup: it makes the most common payment action feel free, while keeping the door open for the rest of the ecosystem to generate fee-paying activity.

This is where value can either flow into XPL Or leak around it. If Plasma becomes mostly a giant stablecoin transfer rail and a large share of activity remains inside those sponsored flows, then you can get massive adoption with surprisingly weak direct token capture. The stablecoin moves, users are happy, apps onboard, but the token’s role is mostly security narrative and incentive fuel. On the other hand, if Plasma becomes the base layer where stablecoin-native apps actually live—trading, lending, settlement logic, merchant rails, payroll, treasury flows—then the chain starts producing consistent fee-paying demand, base-fee burn becomes real, validators earn more from usage, and staking demand becomes less about emissions and more about protecting valuable flows.

So the clean answer to your question—“if this ecosystem grows, does the token actually capture value?”—is: yes, but only if growth shifts from “free sends” into “paid activity around the sends.” Plasma’s design is basically saying: we’ll remove friction to pull stablecoin volume in, then capture value from the economy that forms around that volume through staking and fee/burn mechanics.

And that’s the real separator. Empty projects talk about supply numbers. Real tokenomics asks: where does value land when things go right? For Plasma,XPL wins if it becomes the security backbone and fee sink of a stablecoin-native economy, not just a token that exists next to stablecoin transfers.