by Alex Xu, Research Partner at Mint Ventures

June 20, 2023

This Clip delves into the battle between the premier decentralized exchanges (DEXs) within zkSync, a rapidly expanding Layer2 ecosystem. The clip aims to address the ensuing questions:

What makes the zkSync and its DEX ecosystem noteworthy for investors?

How is the current landscape of DEX projects operating on zkSync?

In the face of fierce competition, how do these rival projects measure up in terms of product quality and edge, and who is most likely to claim the vanguard?

It's worth noting that the perspective provided here is reflective of the author's and the team's view at the time of publication. There may be errors and different opinions, hence this piece is purely intended for discussion. We openly invite rectifications if any inaccuracies are found.

1. What makes the zkSync and its DEX ecosystem noteworthy for investors?

zkSync: A Prominent Competitor in the Layer2 Arena

Layer2 blockchain protocols have been in the spotlight in 2023.

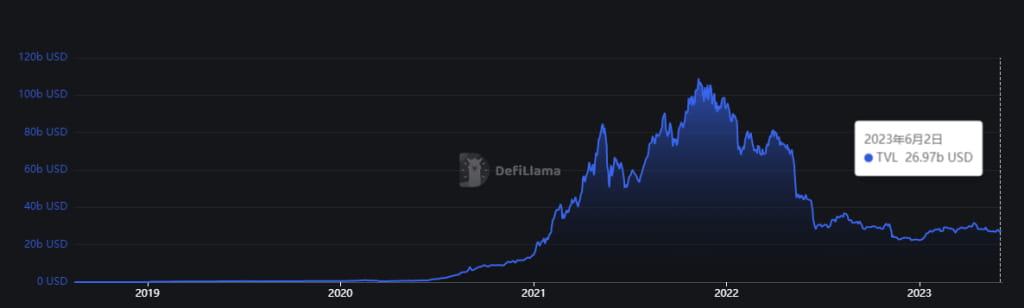

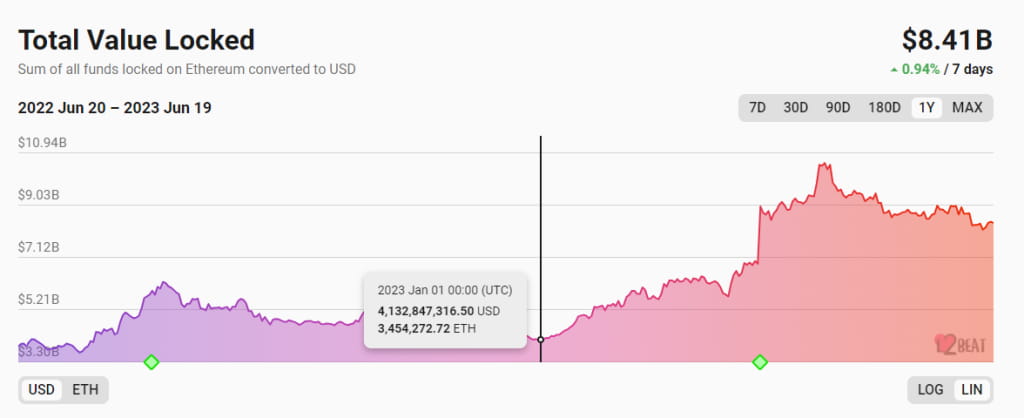

While the total value locked (TVL) in various public chains epitomized by Ethereum stagnates, the TVL within Layer 2 has witnessed an accelerated growth curve, breaching new boundaries.

Source: DefiLlama

Source: L2BEAT

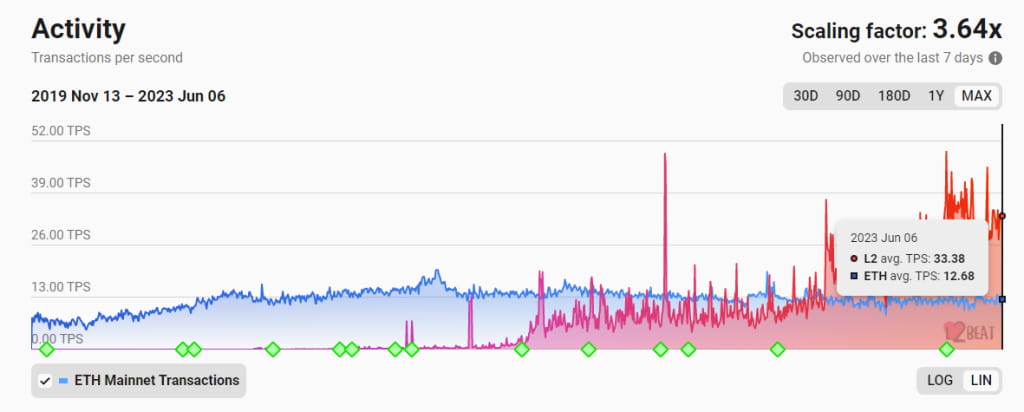

This trend is backed by buoyant on-chain activity. From October 2022 onwards, Layer 2 protocols have outstripped the Ethereum base layer in terms of aggregate transactions per second (TPS), revealing a surge in Layer 2 activities this year. At present, the actual TPS of the Layer 2 network is nearly threefold that of Ethereum, a figure predicted to surge further.

As shown in the following graph, it presents a comparative analysis of TPS on Layer 2 and Ethereum.

Source: L2BEAT

Furthermore, the impending Ethereum Cancun-Deneb upgrade in October is expected to significantly slash the cost of Layer 2, potentially triggering a more substantial migration of users and applications towards Layer 2.

In terms of competitive landscape, L2, similar to L1, has a strong network effect fuelled by users, developers, and capital. This momentum is only outpaced by stablecoins within the Web3 ecosystem, manifesting a highly pronounced first-mover advantage.

In the arena of Optimistic Rollups, Arbitrum and Optimism are distinguishing themselves as potent contenders. Potential new entrants might include industry behemoths like Coinbase, leveraging the Optimistic Rollups Stack. However, it's doubtful that many fresh entrants will make a significant impact in the short term.

The competition within the ZK-Rollup projects is just beginning to simmer. Being the long-term strategic direction of the Ethereum Foundation and Vitalik Buterin, ZK-Rollup is poised to carve a significant niche in the escalating Layer 2 battleground. Post the Arbitrum airdrop earlier this year, zkSync is the subsequent Layer 2 airdrop project eliciting substantial anticipation, with its TVL and active users continually on the upswing. In less than three months since its launch, zkSync has climbed up the ranks to become the third largest Layer 2 in terms of TVL, trailing only Arbitrum and Optimism. It has also positioned itself as the most substantial ZK-Rollup project in terms of TVL and user base. Currently, the zkSync ecosystem is transforming into a more diversified environment, hosting DeFi infrastructure and meme-based projects such as Cheems.

In summary, zkSync gets a head in the race for ZK-rollups Layer 2 scaling solutions.

Dexs: Infrastructure for User and Funds

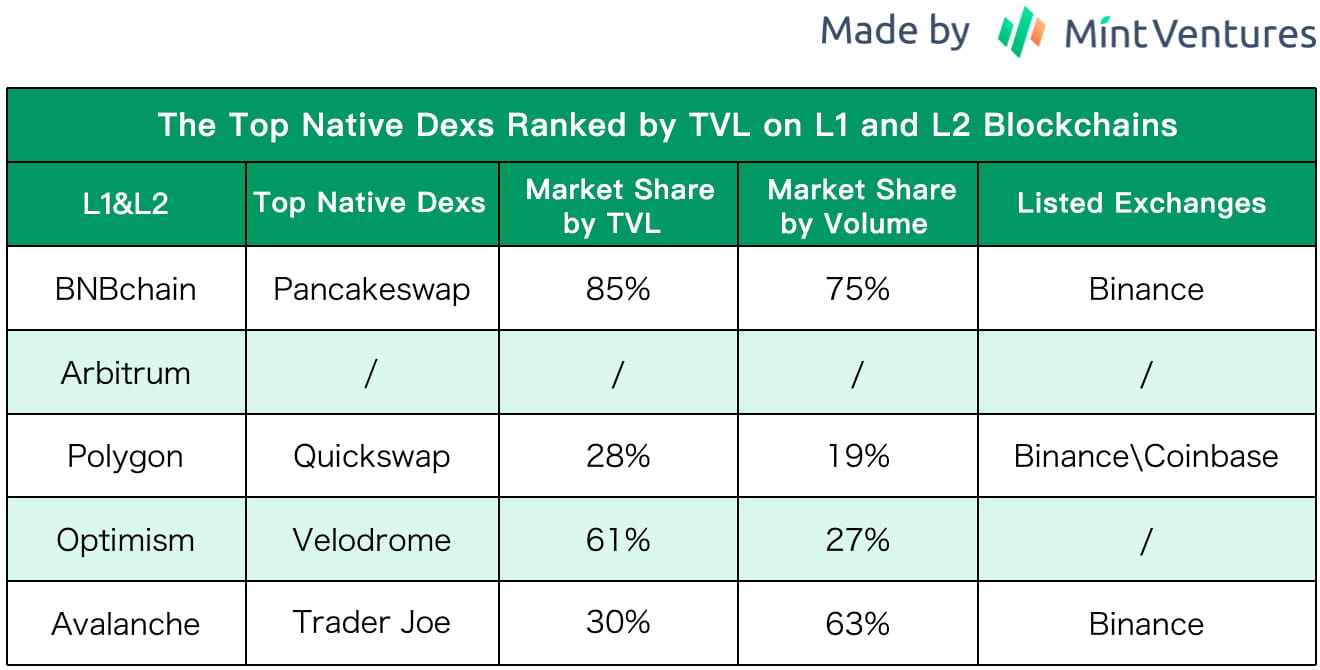

Decentralized exchanges (DEXs), lending protocols, and stablecoins form the basic financial triumvirate of both Layer 1 and Layer 2 ecosystems. However, an examination of previous Layer 1 and Layer 2 projects reveals a typical pattern: each chain generally houses a singular dominant "native DEX". This classification of "top-tier" is granted if at least one of the following benchmarks is met:

Business metrics such as Total Value Locked (TVL) and trading volume significantly outpace rivals, commanding at least a 50% market share.

Tokens have been listed on famous trading platforms such as Binance.

Source:Defillama, Last Updated Time: June 6th, 2023, Made by Mint Ventures

Being the leading DEX on its chain presents several competitive advantages:

Enhanced brand prominence renders it the go-to platform for users to trade and provide liquidity, thereby boosting its credibility.

Business advantages that make it more appealing to other partners, positioning it as the prime choice for liquidity deployment or cooperative launchpad operations.

Greater visibility as a leading DEX, resulting in more frequent mentions and citations across various business rankings, news, and research reports, thereby securing more organic exposure and natural traffic.

A cross-side network effect advantage stemming from dominant liquidity and trading volumes.

Utility tokens are more likely to secure listings on leading centralized exchanges (Cex), thereby attracting liquidity premiums and a wider user base.

In its relatively early stage, the Layer 2 ecosystem, zkSync, is experiencing growth spurts in users, TVL, and developers. The market structure across different tracks is yet to crystallize. Established brands on other chains have not completed cross-chain integration (such as Uniswap V3 and Aave), offering native projects additional time to compete and consolidate their standings.

However, the future DEX landscape of zkSync will likely echo that of other Layer 1 or Layer 2 ecosystems, with one native DEX reigning supreme, or potentially taken over by Uniswap V3.

The looming million-dollar question then is: who will rise to become zkSync's future leading native DEX?

2.The Panorama of zkSync DEXs

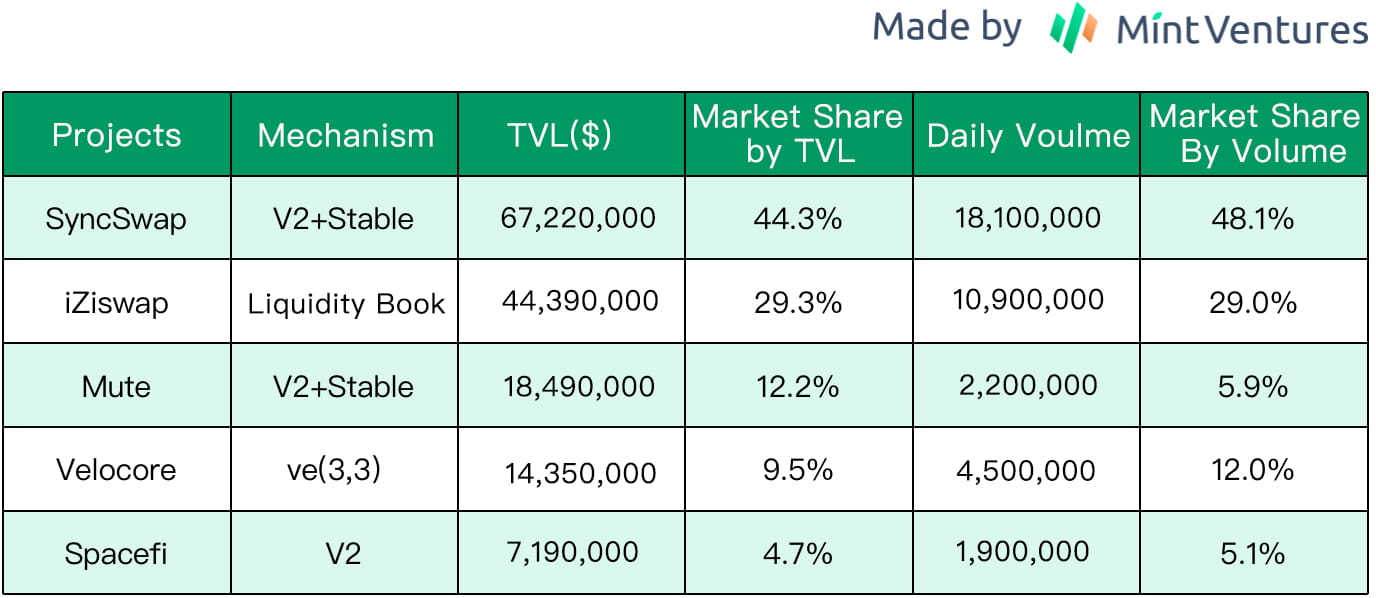

Presently, the zkSync ecosystem boasts an array of DEX projects, each leveraging diverse mechanisms. Nevertheless, based on business data, we're witnessing a trend towards market share consolidation.

Source:Defillama and Official Docs

Last Updated Time: June 6th, 2023, Made by Mint Ventures

*The market share is calculated by using the sum of the Top5 Dexs as the denominator.

From a business perspective, three of the top 5 DEXs - namely SyncSwap, Mute, and Velocore - are deploying the V2 dynamic pool + stable pool model. Notably, Velocore also incorporates a ve (3,3) mechanism akin to Velodrome, propelling its liquidity market operations.

However, when it comes to total value locked (TVL) and trading volume, the current front runners within the zkSync ecosystem are SyncSwap and iZiswap. Consequently, the most likely contender to clinch the top DEX position in the future is anticipated to be one of these two.

3.Syncswap vs iZiswap

In the following section, we'll conduct an evaluation and comparison of the principal features of these top-tier DEXs within the zkSync ecosystem. Our assessment will cover mechanism design, business metrics, tokenomics, and team composition.

3.1Syncswap

3.1.1 Mechanism Design

Pool Type

In general, SyncSwap does not notably diverge in terms of innovative DEX product mechanisms. It utilizes the popular multi-pool mechanism of ve(3,3) projects. At the moment, it primarily consists of the Classic Pool, modeled on Uniswap v2 (which is chiefly suitable for trading pairs with substantial slippage) and the Stable Pool, modeled on Curve (which is apt for trading pairs with low slippage).

SyncSwap’s Pools, source: https://syncswap.xyz/pools

Fees

Syncswap refers to its fee mechanism as "Dynamic Fees", However, this does not reflect the traditional dynamic fee mechanism we're familiar with, where the volatility of the asset price directly influences the fee rate to offset the liquidity provider's impermanent loss. A more fitting term for SyncSwap's mechanism might be "customizable fees". Specifically, dynamic fees consist of four facets:

Variable Fees: The variable fees allow fees to be separately adjusted for different pools. The maximum fee tier is 10%.

Directional fees: The directional fees allow a liquidity pool to have custom trading fee tiers in different directions (buy or sell). For example, for one XXX/USD liquidity pool, the fee tier of buying XXX can be 0.1% while the fee tier of selling XXX can be 0.5%.

Fee discounts: Stakers can enjoy fee discounts. The more tokens have been staked, the higher the discount ratio is.

Fee delegates: With fee delegation, it's possible to delegate the trading fee of specific pools to partner ecosystem projects dynamically in a democratic way.

Therefore, it is evident that SyncSwap's "Dynamic Fees" are not precisely "dynamic" but offer a high degree of customization.

3.1.2 Business Performance

We've taken a comprehensive approach to assess SyncSwap's business performance, scrutinizing four key aspects: trading volume, user count, liquidity, and trading fees (LP fees and protocol revenue).

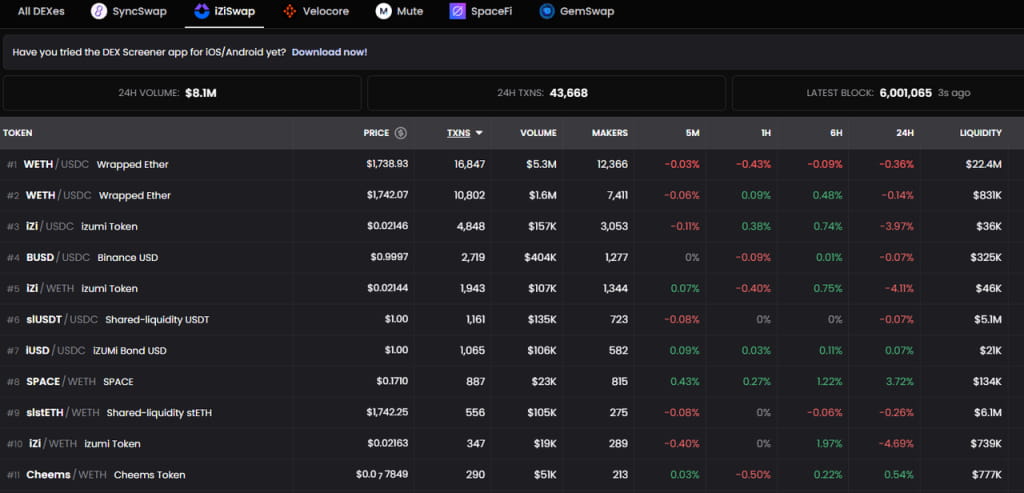

Trading Volume and User Base

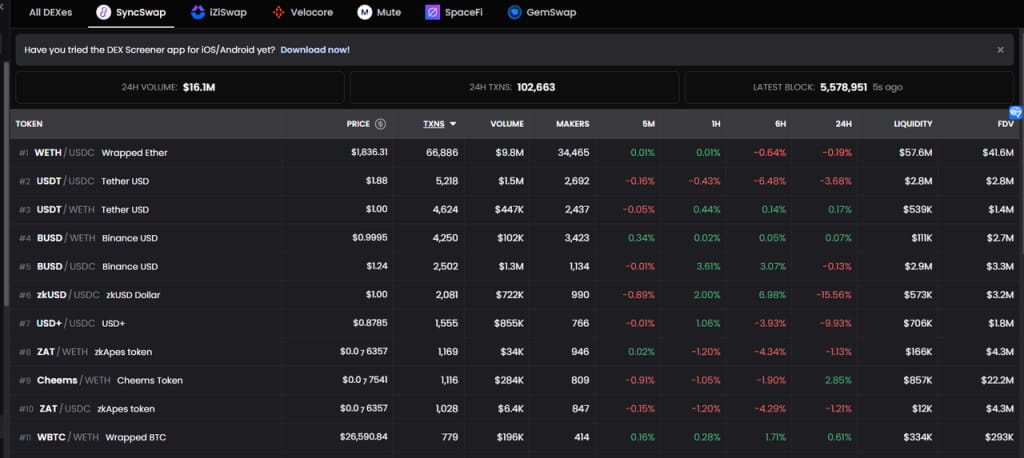

SyncSwap doesn't provide a fully encompassing trading volume dashboard. By leveraging on-chain data, we've calculated SyncSwap's 7-day and 30-day trading volumes. The trading volume over the past 30 days (from May 8th to June 7th, 2023) amounted to $431,351,415, resulting in an average daily trading volume of $14,378,380. The 7-day trading volume (from June 1st to June 7th, 2023) hit $103,743,812, yielding an average daily trading volume of $14,820,544.

These trading volume figures closely align with the 24-hour trading volume statistics provided by Dexscreener and the official 24-hour trading volume stats from various Pools.

24-hour trading volume on SyncSwap, Source: https://dexscreener.com/zksync/syncswap

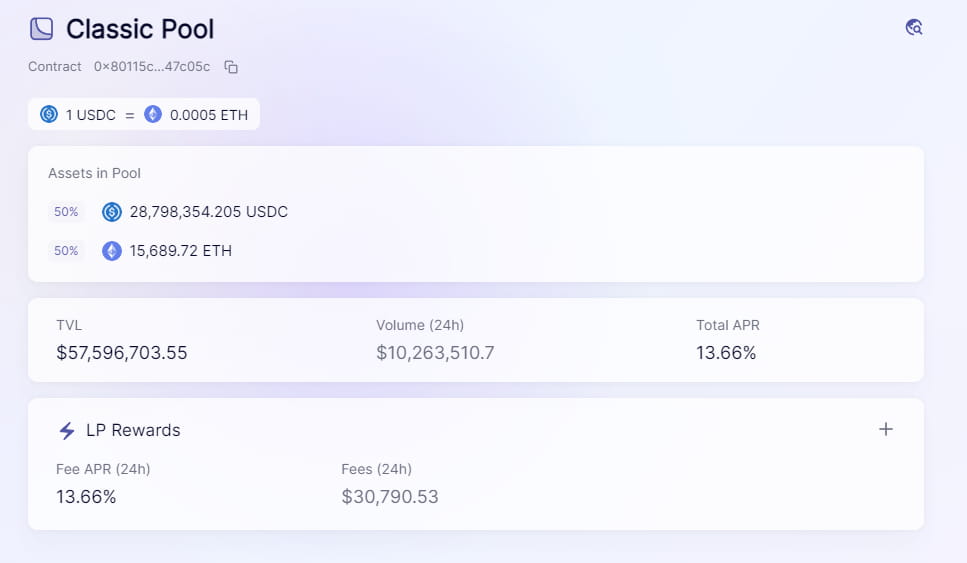

Top1 Pool on Syncswap with daily volume amounting to $10 million, source: https://syncswap.xyz/pool

In terms of trading volume composition, SyncSwap is predominantly led by the ETH-USDC pool, which accounts for a significant majority share of 60.8%. Stablecoins trail behind, and trading volume of zkSync’s native asset comprises less than 5% of the total volume.

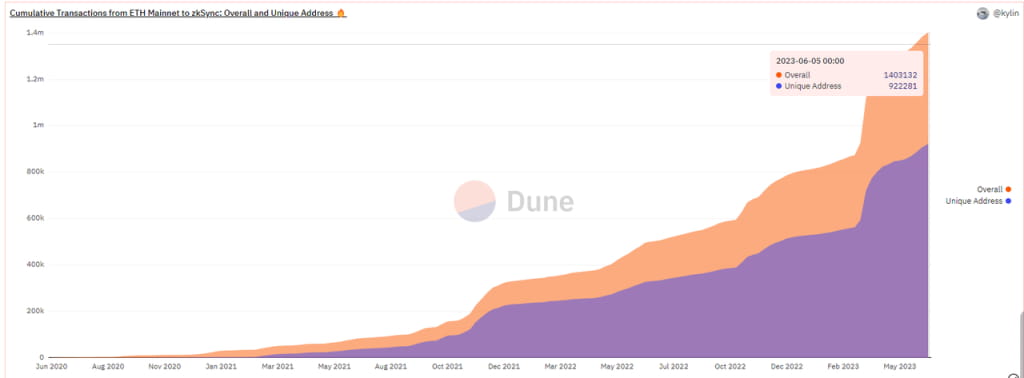

Relying on on-chain data, SyncSwap's monthly active addresses from May 8th to June 7th, 2023, tallied up to 843,692, and the weekly active addresses from June 1st to June 7th stood at 247,814. As of June 5th, the count of unique addresses on zkSync reached 920,000, suggesting that nearly 91.4% of addresses have engaged with SyncSwap within a month.

Source: Dune.com

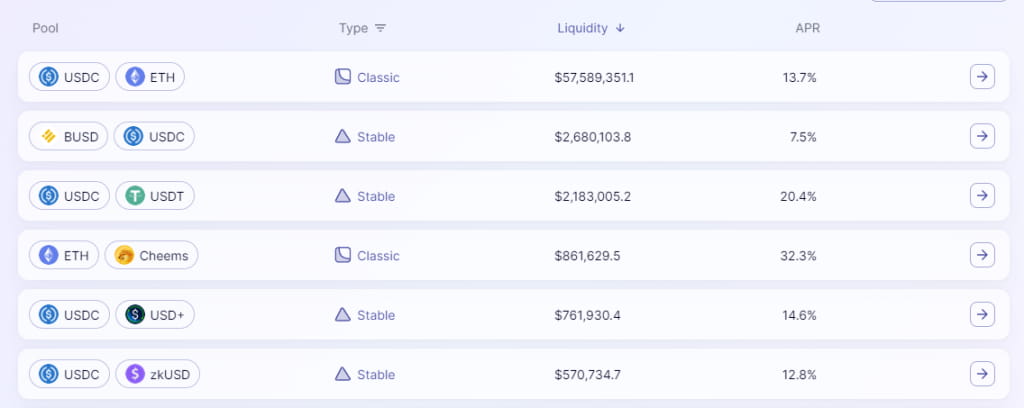

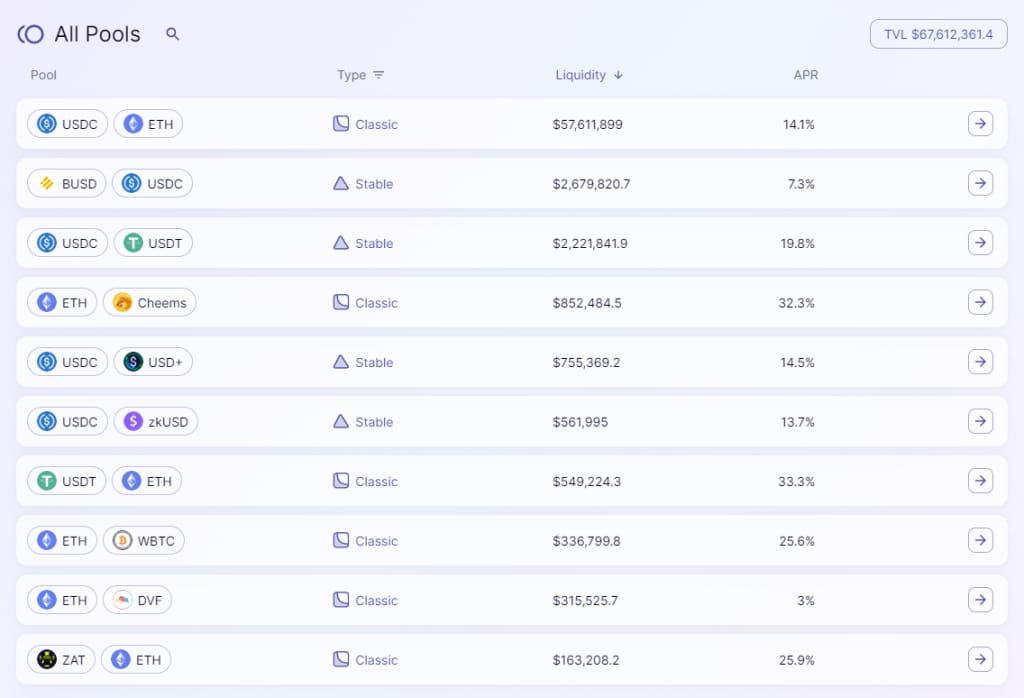

Liquidity

SyncSwap's total liquidity amounts to $67,610,000. The ETH-USDC Pool leads with $57.61 million, constituting a whopping 84.5% of the total liquidity.

Source: https://syncswap.xyz/pools

In terms of the top 10 pools sorted by liquidity, the non-stablecoin native assets of zkSync, Cheems (meme coin), and ZAT (NFT), represent a relatively modest 1.5%.

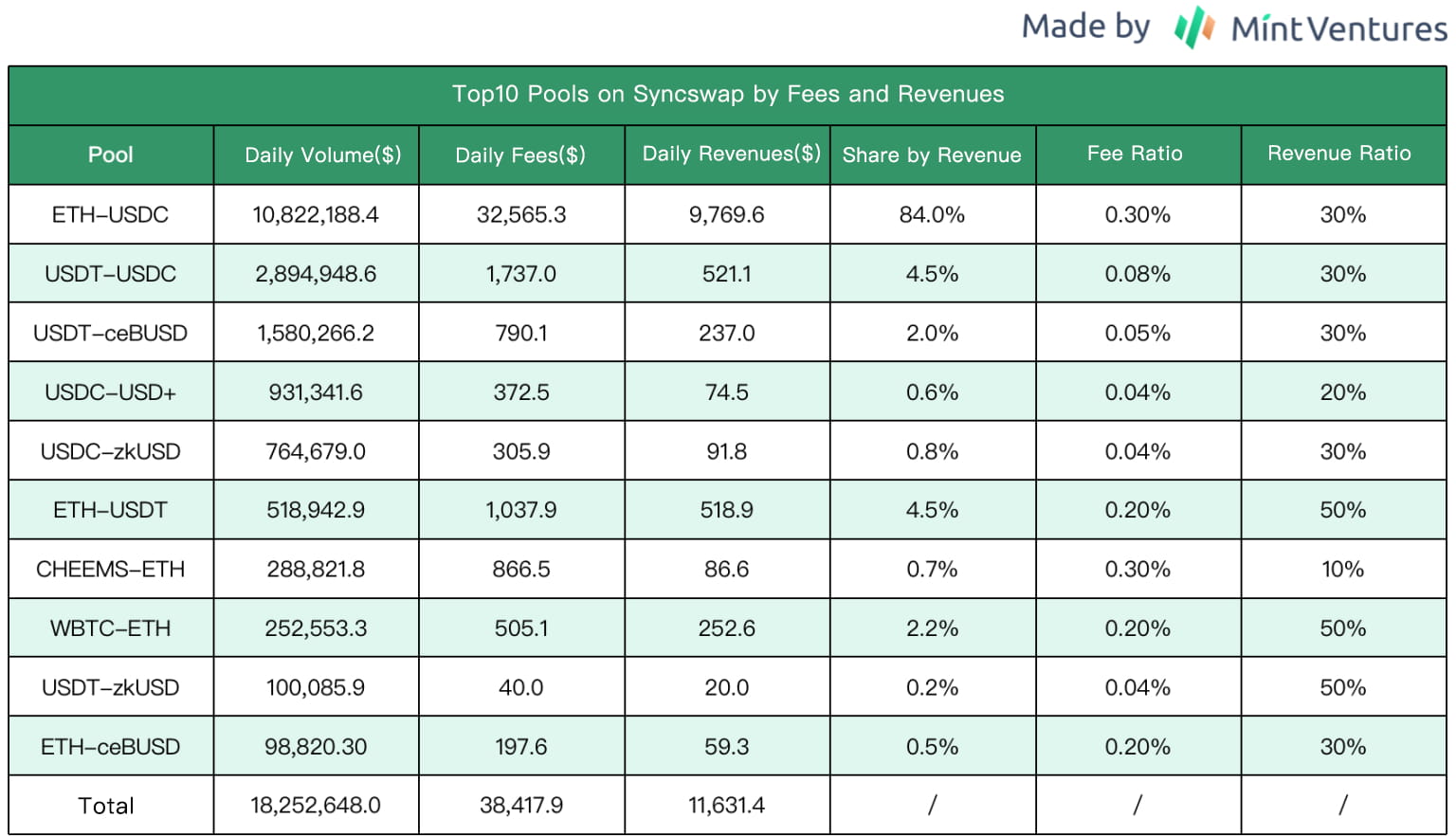

Fees and Revenues

We've performed a statistical analysis of the protocol revenue of the top 10 pools by trading volume on SyncSwap as of June 9th. Data is sourced from SyncSwap's official website, and the table was compiled by Mint Ventures on June 9th, 2023.

Source:SyncSwap, Last Updated Time: June 9th, 2023, Made by Mint Ventures

According to the data, it's clear that the protocol revenue from ETH trading pairs dominates, accounting for 90.6% of the total, making it the major source of fees and revenue. Also, SyncSwap's fee-share ratio for Cheems and USD+ (a stablecoin issued by Tangible) stands at a relatively low 10% and 20% respectively, passing the lion's share of revenue to liquidity providers (LPs). This strategy vividly underscores SyncSwap's intent to draw in more liquidity.

An interesting point to note is that SyncSwap has yet to issue tokens or roll out liquidity or trading incentives, making it a rare breed in the DeFi landscape capable of generating positive returns. This fact is closely linked to the reality that neither zkSync nor SyncSwap have launched their own coins yet, and many airdrop hunters have thus interacted with them.

3.1.3 Tokenomics

Syncswap, though it has not officially launched its token, has already unveiled some details about it. Named SYNC, the total token supply is pegged at 100 million.

In terms of token functionality, Syncswap has drawn some inspiration from Curve's ve model. Holders are required to stake SYNC to get veSYNC to gain token utility, which includes:

Voting powers

Protocol fee dividends

Fee discount

When it comes to the specific unlocking mechanism, Syncswap deviates from Curve. veSYNC can be converted back to SYNC tokens after 6 months. Additionally, it supports partial vesting - 50% of tokens can be converted back to SYNC after 20 days, and the remaining 50% continue to vest linearly until the end of the full vesting duration.

Despite this, SyncSwap's Tokenomics remain partially undisclosed, with details such as token distribution, emission plans, and whether a ve model is employed to guide token pool emissions, etc., still under wraps. Nevertheless, based on the project's overall mechanisms, SyncSwap appears to align more with a ve(3,3) Dex project model.

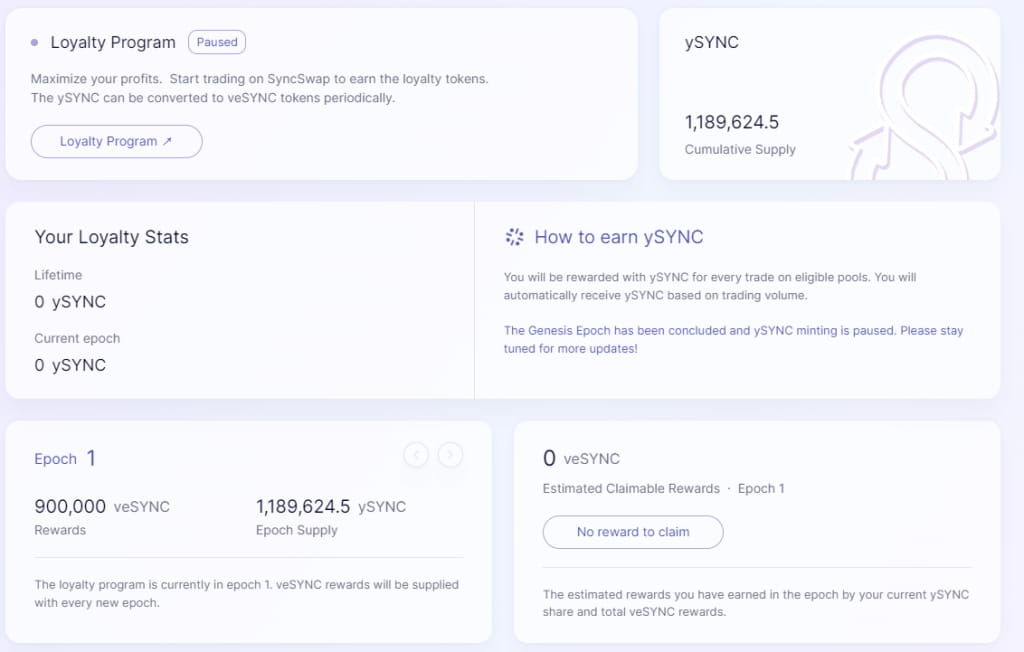

Even though the SYNC token has not been listed yet, SyncSwap has already rolled out a token incentive initiative dubbed the "Loyalty Program". This program primarily incentivizes the fees generated by specific trading pairs, similar to trade-mining.

Source: https://syncswap.xyz/rewards

The Loyalty Program rules include:

Only trades conducted via eligible trading pairs qualify for ySYNC rewards. The reward amount is tied to volume – the higher the trading fees generated, the more ySYNC tokens users receive.

Earned ySYNC can periodically be converted into veSYNC tokens. The number of ySYNC tokens received equals the trading fees contributed by the user.

The Loyalty Program operates in epochs. Typically, each epoch lasts for 24 hours, with the exception of the genesis epoch which spans one month.

Traders are rewarded with ySYNC, which can be converted into veSYNC tokens. If users wish to sell, they must first unstake their veSYNC.

The genesis epoch of the Loyalty Program ran from April 10th to May 10th this year, providing a total reward pool of 900,000 veSYNC. The final amount of ySYNC received by participants was 1,189,624.5, implying that users paid a total of $1,189,624.5 in trading fees on eligible trading pairs during this period. Consequently, the associated cost of acquiring each veSYNC was $1.32.

However, the Loyalty Program is currently paused, having run only for the initial epoch.

3.1.4 Teams and Financing

As of now, the Syncswap team remains anonymous, and details such as team size and the identities of team members are not disclosed. Additionally, there is no available information regarding any fundraising or financing activities related to the project.

3.2 iZiswap

3.2.1 Mechanism Design

iZiSwap is a product of iZUMi Finance, a DeFi protocol that offers a unique service known as Liquidity as a Service (LaaS). It spans across various blockchains and has conceived iZiSwap, a decentralized exchange crafted to offer robust liquidity solutions. The suite of services that iZUMi Finance delivers currently includes:

LiquidBox, an innovative liquidity reward service that harnesses the power of Uniswap V3's concentrated liquidity mechanism. This tool permits liquidity providers to deposit their liquidity within virtually any desired price range.

iZUMi Bond, a financing solution for projects reminiscent of traditional finance's convertible bonds.

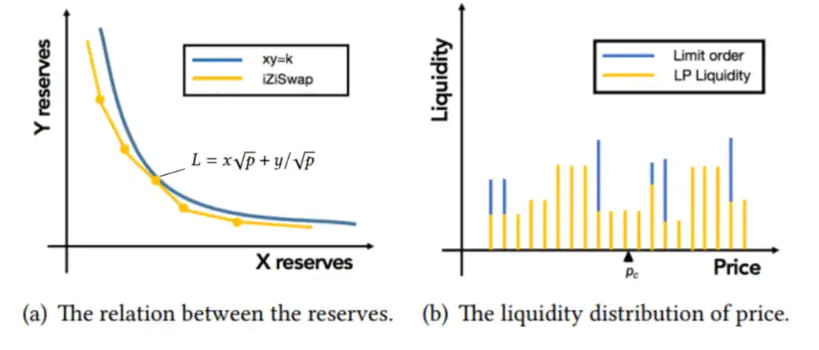

Within the burgeoning landscape of the zkSync ecosystem, iZiSwap stands out, marking its territory by incorporating a Discretized Concentrated Liquidity (DL) mechanism into its Automated Market Maker (AMM) model, coined DL-AMM. This innovative approach departs from the well-trodden path of the constant product formula typically used in AMMs. Instead, the DL-AMM model disperses liquidity across various discrete price points, each adhering to the constant sum formula, L = X * √ P + Y / √P.

These discrete price points are ingeniously interlinked to form an all-encompassing AMM price curve, bearing a striking resemblance to the Uniswap curve as depicted on the left side of the following diagram.

Source: https://assets.iZUMi.finance/paper/dswap.pdf

The DL-AMM bifurcates liquidity into two distinct types: LP (Liquidity Provider) liquidity and Limit Order liquidity. These two forms of liquidity are merged and spread over various price ranges, as illustrated on the right side of the diagram.

iZiSwap utilizes a dual-token liquidity model for its pools. It reimagines limit orders as one-sided liquidity inputs from a trader, breaking away from the norm of dual-token inputs from an LP. Upon reaching the target price of the order, the tokens are swapped and the transaction is finalized, marking a departure from Uniswap V3's system where one-sided liquidity can mimic a limit order within a narrow price range but reverts to the original token if the price swings back to its starting point.

Not content with merely pushing boundaries, iZiSwap has also ventured into the development of a trading interface, known as iZiSwap Pro, that mirrors a traditional order book. This user-friendly interface provides users with a trading experience akin to a centralized exchange (CEX), replete with familiar trading tools in a decentralized setting.

Source: https://iZUMi.finance/trade

Drawing parallels to iZiSwap's novel point-based liquidity distribution, DeFi protocol Trader Joe unveiled its Liquidity Book (LB) in November 2022. Like its counterpart, LB disperses liquidity point-wise, with the liquidity at specific price points governed by a constant sum formula as opposed to the traditional constant product formula.

For an in-depth exploration of Trader Joe's approach and its wider implications, I recommend diving into my research piece, “Riding the Wave of Arbitrum: A Deep Insight of Trader Joe's Fundamentals and Future Outlook”.

It is plausible that Trader Joe drew inspiration from iZUMi's groundbreaking work on DL-AMM. In November 2021, iZUMi released a research paper titled "iZiSwap: Building Decentralized Exchange with Discretized Concentrated Liquidity and Limit Order," detailing the mechanics of DL-AMM. This was followed by the launch of iZiSwap on the BNBchain in May 2022, both milestones preceding Trader Joe's Liquidity Book (LB) rollout. Notably, Trader Joe paid homage to iZUMi, referencing their work in their V2 whitepaper.

Beyond the DL-AMM concept, iZUMi introduced LiquidBox, a liquidity reward service that harnesses the concentrated liquidity mechanism. Unlike traditional liquidity mining incentives inspired by Uniswap V2, where users stake LP tokens to earn token rewards distributed evenly across all price ranges, incentive schemes based on concentrated liquidity models, such as Uniswap V3, DL-AMM, and LB, are significantly more intricate.

Consider this hypothetical situation: An LP contributes $1000 in liquidity within a narrow price range of $95 to $105 for a token priced at $100. Simultaneously, another LP delivers an equivalent amount of liquidity but within a much broader range of $10 to $20, effectively setting one-sided pending orders. The first LP's liquidity is utilized far more efficiently than the second's. As such, employing a reward system like Uniswap V2, which distributes rewards uniformly based on the liquidity value, would not suit this context.

LiquidBox serves as a platform where liquidity providers can deposit assets and earn incentives. However, from the perspective of incentive providers - typically project operators and iZUMi - the obtained liquidity can be segmented across various price buckets to fulfill specific liquidity needs.

LiquidBox offers three different liquidity allocation options, mutually agreed upon by the project operator and iZUMi:

One-sided Mode: In this model, the tokens deposited by users aren't added to the pool but are separately staked. This approach reduces the quantity of tokens in the pool, curbing resistance during price surges. The other half of the assets, often represented by valuable tokens (ETH or stablecoins), are assigned to the lower price side, bolstering buy-side pressure when prices tumble. This setup can aid in achieving the dual impacts of "fueling token purchases and cushioning token sales" for the project. For users, if the token price escalates, they can avoid experiencing an impermanent loss from "selling all the way up." However, if the token price plummets, because the tokens weren't sold at a high price, users might face amplified impermanent losses due to the price dip. This model can be seen as a market-making mechanism encouraging users to stake tokens and deter sales, under a shared (3,3) market-making arrangement.

The comparison between One-sided model and Uniswap V2, Source: iZUMi

Fix Range Mode: This is a simple strategy that incentivizes liquidity within a predefined price range. It's particularly useful for encouraging stablecoins and wrapped assets.

Incentives of Fix Range Mode,Source: iZUMi

Dynamic Range Mode: In this model, users engage in liquidity mining by providing liquidity within a range of (0.25Pc, 4Pc) around the current price (Pc). The breadth of the price range can also be specified by the projects, such as (0.5Pc, 2Pc). The benefit of this model is the enriched liquidity around the market price range. However, if the token price witnesses significant swings beyond the initial range set by the user, they may need to frequently withdraw and redeposit their LP, bearing impermanent loss in the process. This could incur high operational costs.

Notably, in current practice, all active LiquidBoxes have chosen this dynamic model.

Furthermore, LiquidBox supports both Uniswap V3 and iZiSwap LP for staking incentives, and most of the existing incentive pools operate on the zkSync network.

3.2.2 Business Performance

Trading Volume and User Base

Utilizing on-chain analytics, a performance comparison can be drawn between iZiSwap and SyncSwap over an identical period. Over the past 30 days, from May 8th to June 7th, 2023, iZiSwap has accumulated a total trading volume of $195,025,494. This reflects an average daily trading volume of around $6,500,849. Its 7-day trading volume, from June 1st to June 7th, 2023, amounted to $60,007,769, thereby representing an average daily trading volume of approximately $8,572,538.

These statistics align consistently with the 24-hour trading volume figures reported by Dexscreener and the official 24-hour trading volumes for each individual pool.

Source: https://dexscreener.com/zksync/iziswap

Source: https://analytics.iZUMi.finance/Dashboard

Similar to SyncSwap, the ETH-USDC pair emerges as a significant driver of trading volume on iZiSwap, accounting for 85.8% of the daily trading volume. This is followed by trades involving stablecoins and iZiSwap's native token, IZI.

On-chain data also indicates that the monthly active addresses for iZiSwap, from May 8th to June 7th, 2023, reached 301,993, while the weekly active addresses, from June 1st to June 7th, 2023, stood at 102,938. These figures suggest that iZiSwap's active addresses represent approximately 35-40% of the active addresses observed for SyncSwap.

Liquidity

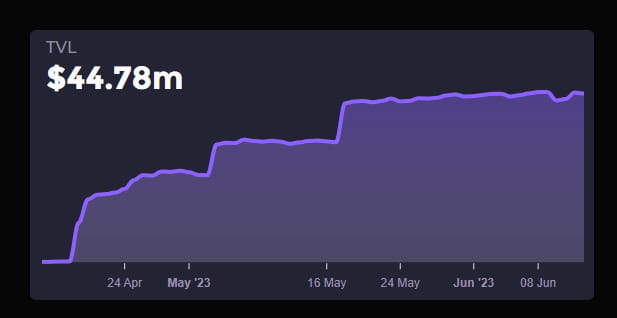

There is a notable discrepancy between the official liquidity statistics cited by iZiSwap and the data released by Defillama. According to iZiSwap's own dashboard, the platform's liquidity currently stands at a robust $44.78 million, while Defillama quotes a considerably lower figure of $25.95 million.

Liquidity disclosed by iZiSwap official

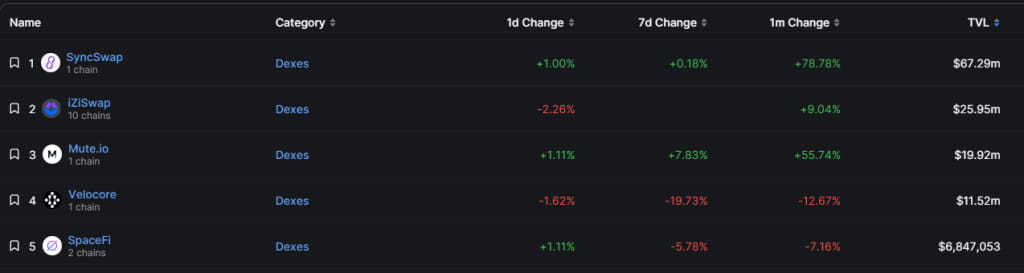

zkSync’s Top Dex by TVL, source: Defillama

This discrepancy can be attributed to the fact that a significant proportion of iZUMi-issued stablecoins and wrapped assets in iZiSwap's official liquidity calculations. These include instruments such as iUSD, a bond-financed stablecoin, and slstETH and slUSDT, cross-chain wrapped assets collateralized by ETH.

However, in the current DeFi landscape, the successful promotion of self-issued stablecoins and wrapped assets can be challenging due to tepid user acceptance and mainstream DeFi platforms' reluctance to embrace them. This can be attributed to the inherent risks associated with accepting assets issued by third parties. Additionally, according to iZUMi, certain assets like slstETH are still under development and have not been officially launched. As such, for a more reliable comparison, it would be more accurate to base the TVL on the data reported by Defillama.

Upon discounting the TVL of self-issued stablecoins and wrapped assets, iZiSwap's TVL appears to be quite comparable to that of SyncSwap, with the ETH pool accounting for 86.8% of the total.

As for liquidity incentives, iZiSwap currently operates several mining pools utilizing LiquidBox on zkSync, all of which employ a dual incentive model, rewarding liquidity providers with both project tokens and IZI tokens.

Source: https://iZUMi.finance/farm/iZi/dynamic

An examination of the current dual token rewards reveals that the projects themselves contribute the bulk of the total token rewards intended for liquidity incentives. However, in certain pools, the value of IZI tokens surpasses that of the project tokens due to a decline in the latter's price.

As of June 14, 2023, the total volume of IZI tokens available as liquidity incentives across the eight LiquidBox pools on zkSync is approximately 60,180 per day, equivalent to around $1,208 in value.

Fees and Revenues

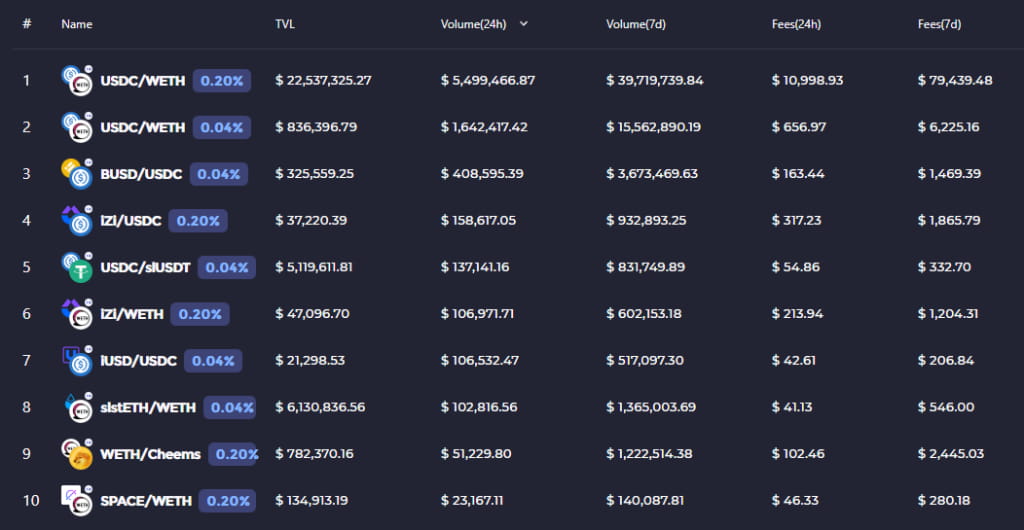

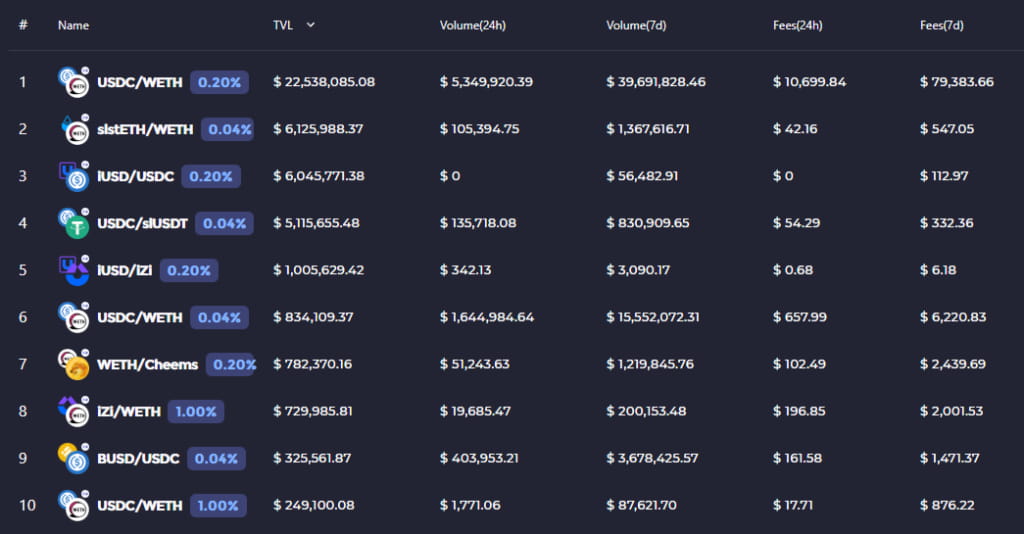

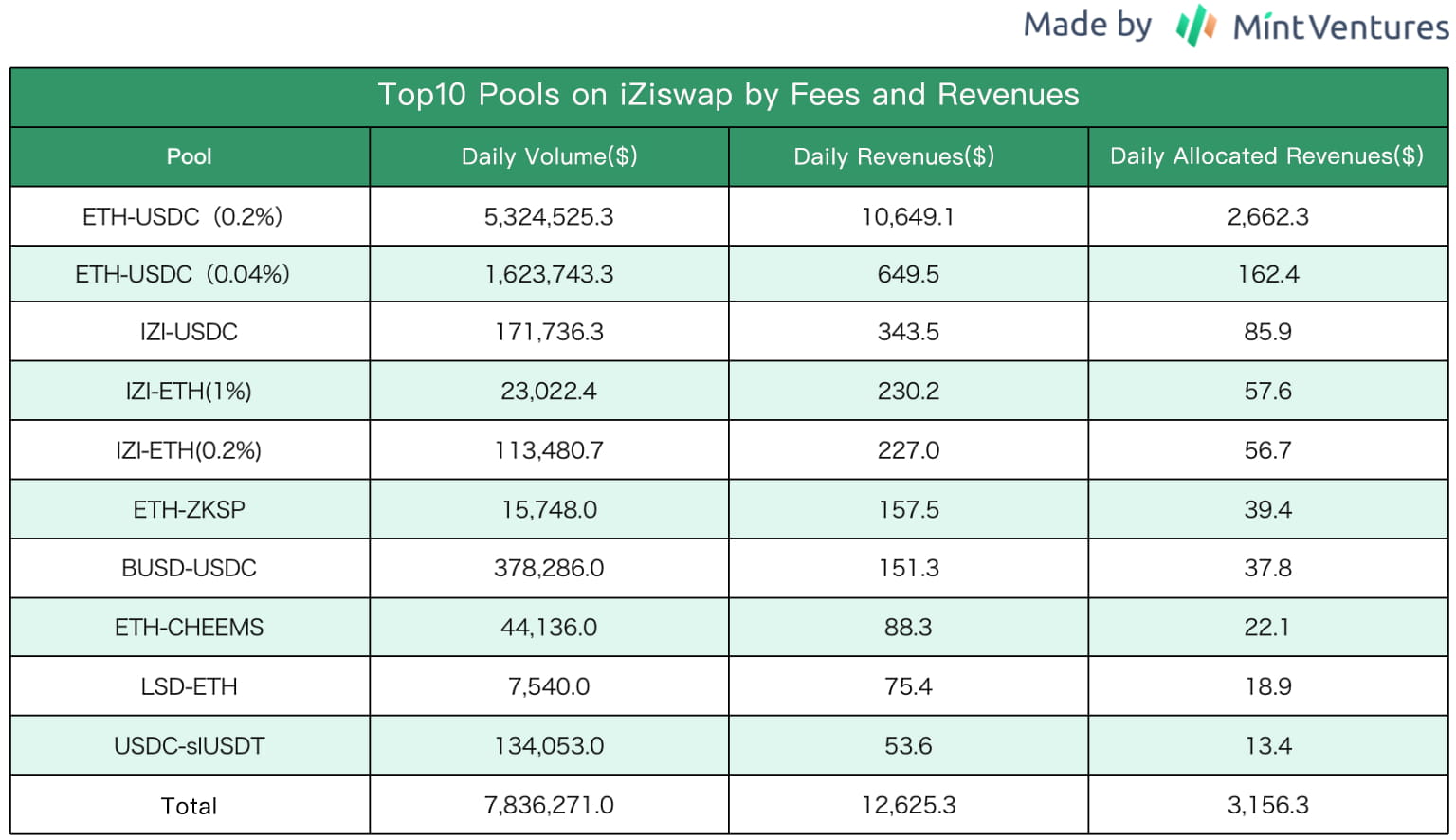

iZiSwap's dashboard provides a comprehensive view of the fees and revenues associated with each pool. Here, I present a ranking of the top 10 pools based on weekly fees and revenues.

Source:iZiSwap, Last Updated Time: June 6th, 2023, Made by Mint Ventures

Source:iZiSwap, Last Updated Time: June 6th, 2023, Made by Mint Ventures

*Daily Allocated Revenues refers to the revenue allocated to $IZI Holders, and it's equivalent to 25% of the fees.

When contrasting iZiSwap's daily allocated revenue with SyncSwap's, we find that iZiSwap's stands at $6,312.5, which is substantially lower than SyncSwap's $11,631.4. However, a closer look at the tokenomics reveals that half of this revenue is earmarked for iUSD buybacks and market fund allocation, effectively leaving only 12.5% of fees to be distributed to IZI token holders. This is an important consideration to bear in mind when evaluating pool returns on iZiSwap.

3.2.3 Tokenomics

Operating as a key subsidiary within the expansive iZUMi ecosystem, iZiSwap has rapidly emerged as a pivotal revenue stream. With a robust trading volume and an optimistic outlook for future expansion, iZiSwap's operations on the zkSync network have emerged as the most significant and dominant component of its operational strategy.

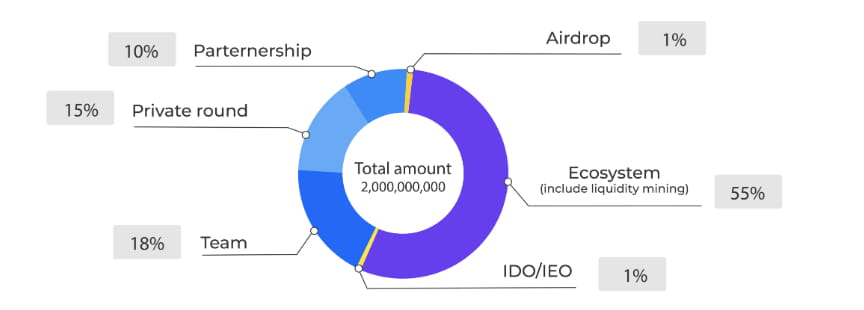

Total Supply, Distribution and Circulation

The native token of the iZUMi is IZI, with a total supply of 2 billion tokens distributed across multiple networks, including Ether, BNBchain, Polygon, Arbitrum, and zkSync.

The token distribution and vesting schedule for IZI is as follows:

Source: https://docs.izumi.finance/tokens/tokenomics

According to data from CoinMarketCap (CMC), out of the total 787,400,000 IZI tokens that have been unlocked, a noteworthy portion — to the tune of 276,091,843.3 IZI tokens — are currently in staking.

Token Utility

The IZI token, as envisioned, is intended to serve three core functions:

Governance Voting: IZI tokens have been designed to serve as voting assets, enabling holders to participate in deciding the distribution of token emissions. As of now, however, this particular feature is still under development and has not been fully activated.

Staking Rewards: IZI token holders stand to gain from staking rewards. Specifically, 25% of the IZI tokens that are repurchased from the trading fees generated on iZiSwap are allocated to staking rewards.

Yield Boosting: Similar to the boost mechanism employed by Curve, IZI stakers are presented with an opportunity to boost the LiquidBox pool APR up to 2.5x.

The inherent value of a DEX token operating under the ve model typically stems from two primary sources:

Governance: This is related to the capability of directing liquidity. It's evaluated based on the liquidity value of the respective DEX. The value is also affected by the liquidity acquisition requirements of other projects operating on the same blockchain.

Revenue sharing: Token holders are entitled to a proportion of the protocol's generated revenue.

Currently, iZiSwap's governance voting is still in the developmental phase. Furthermore, half of the shared fees (50%) is allocated to the bond buyback module, which may place a potential cap on the intrinsic value of the $IZI token.

3.2.4 Team and Financing

iZUMi Finance, as revealed by Rootdata, was founded by Jimmy Yin, a Tsinghua University graduate. The project team currently has over 20 members.

According to disclosures from Rootdata, iZUMi Finance has undergone four rounds of financing so far:

November 2021: In its seed round, iZUMi Finance raised $2.1 million, reaching a valuation of $14 million.

December 2021: The firm completed a Series A round, valuing the project at $35 million.

May 2022: iZUMi executed a convertible debt financing round through Solv Protocol, accumulating $30 million earmarked for liquidity operations.

April 2023: iZUMi raised an additional $22 million in the form of a fund through Solv Protocol, which was also designated for liquidity operations.

It's interesting to note that the two latest rounds of financing by iZUMi didn't involve direct token sales. Instead, the project raised capital through bond issuances and funds. These resources are not only deployed for operational expenses and team expansion, but also for liquidity operations, including market-making. The generated revenue can then be used for both the team's salary requirements and to finance returns on the funds raised.

3.3 Conclusion

In the race for dominance in the zkSync-based DEX market, SyncSwap and iZiSwap have adopted different strategies, with SyncSwap adhering to a more traditional approach in product and system design, offering modest but effective innovations. On the other hand, iZiSwap has ventured into more distinctive product explorations, although the efficacy of these in driving user growth and asset accumulation remains to be seen. From a business metrics standpoint, SyncSwap currently enjoys a definitive advantage in terms of Total Value Locked (TVL) and trading volume. The anticipated token distribution and project airdrops have generated significant interest in SyncSwap, resulting in lower operating costs compared to iZiSwap, which still grapples with daily token incentive expenses.

However, a common hurdle that both contenders face is the limited number of zkSync's native projects with substantial traction, given its relatively recent emergence as a layer2 solution. Consequently, the bulk of the liquidity and trading volume for both DEXs is still tied to ETH.

Looking forward, it is expected that an increasing number of native projects will make their debut on zkSync. The burning question remains, however, as to where these projects will choose to launch their initial liquidity - the commercially superior SyncSwap or the more mechanically innovative iZiSwap? This adds an intriguing layer to the existing competition. Adding to the mix, Uniswap announced in October 2022 its plan to launch V3 on zkSync, which could potentially disrupt the market at any moment, further amplifying the competitive pressure.

It is an exciting time for the industry, and we look forward to monitoring these developments closely.