إخلاء المسؤولية: امتثالًا لمُتطلبات لائحة تنظيم أسواق الأصول الرقمية (MiCA)، تخضع العملات المستقرة غير المصرح بها لقيود مُحددة للمُستخدمين في المنطقة الاقتصادية الأوروبية. لمزيد من المعلومات، يُرجى الضغط هنا.

إخلاء المسؤولية: هذه الصفحة من الأسئلة الشائعة مُعدة لأغراض تعليمية وتثقيفية فقط. ولا تعتبر شروطًا قانونية أو اتفاقية قانونية من أي نوع بين المستخدم وبين منصة Binance (بينانس). ولا يجوز اعتبارها نصيحة مالية أو قانونية أو أية نصيحة متخصصة أخرى. قد تكون المعلومات الواردة في هذه الصفحة قديمة. للاطلاع على الشروط القانونية المطبقة على خدمات تداول العقود الآجلة والخيارات، يُرجى الرجوع إلى شروط الاستخدام، وقواعد منصة التداول (بما في ذلك إجراءات منصة التداول) وقواعد التسوية(بما في ذلك إجراءات التسوية)، والتي تدخل حيز التنفيذ في 5 يناير 2026. سيتم أيضًا تحديد شروط وأحكام إضافية في مواصفات العقد المُطبقة على عقد المشتقات ذي الصلة.

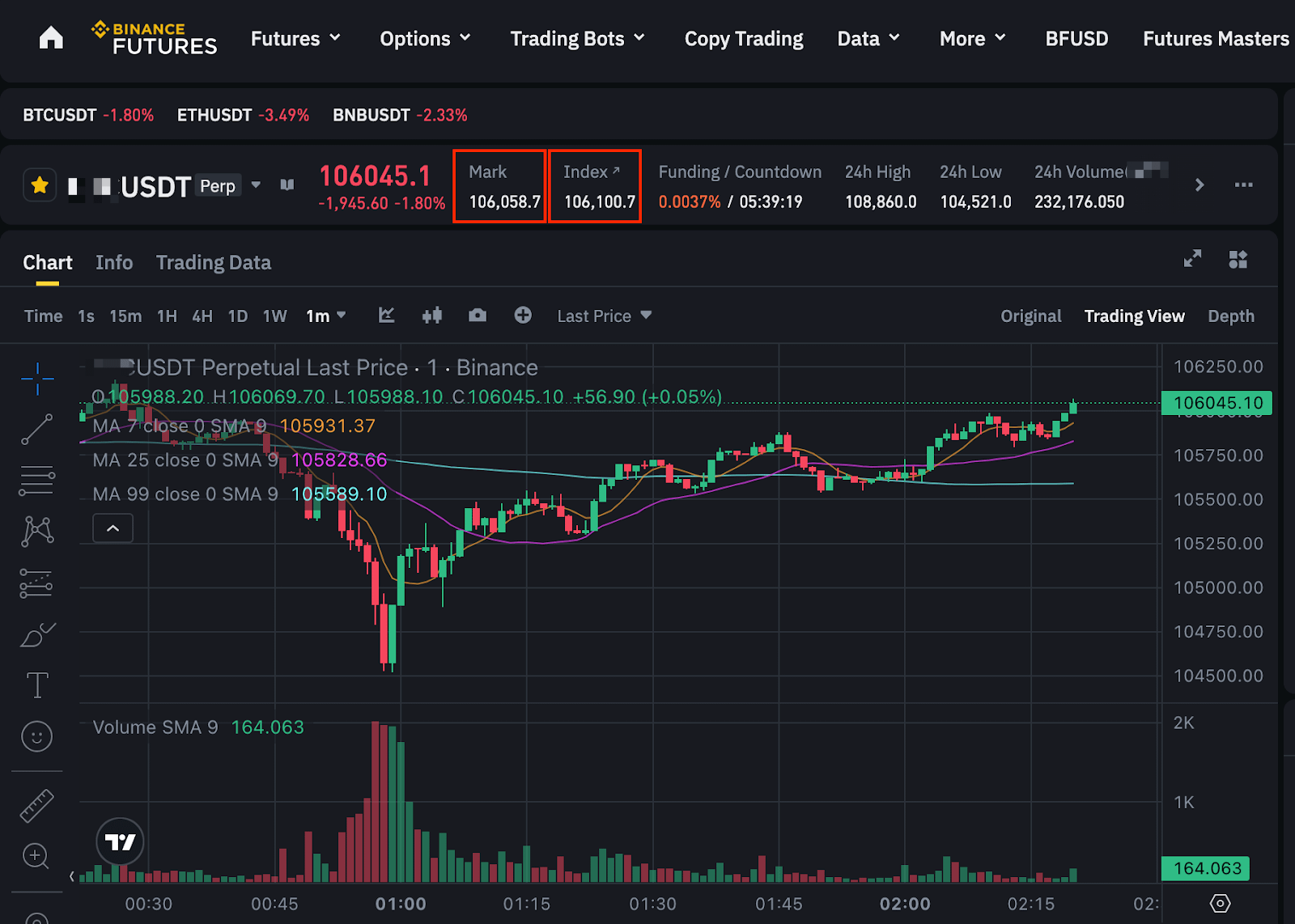

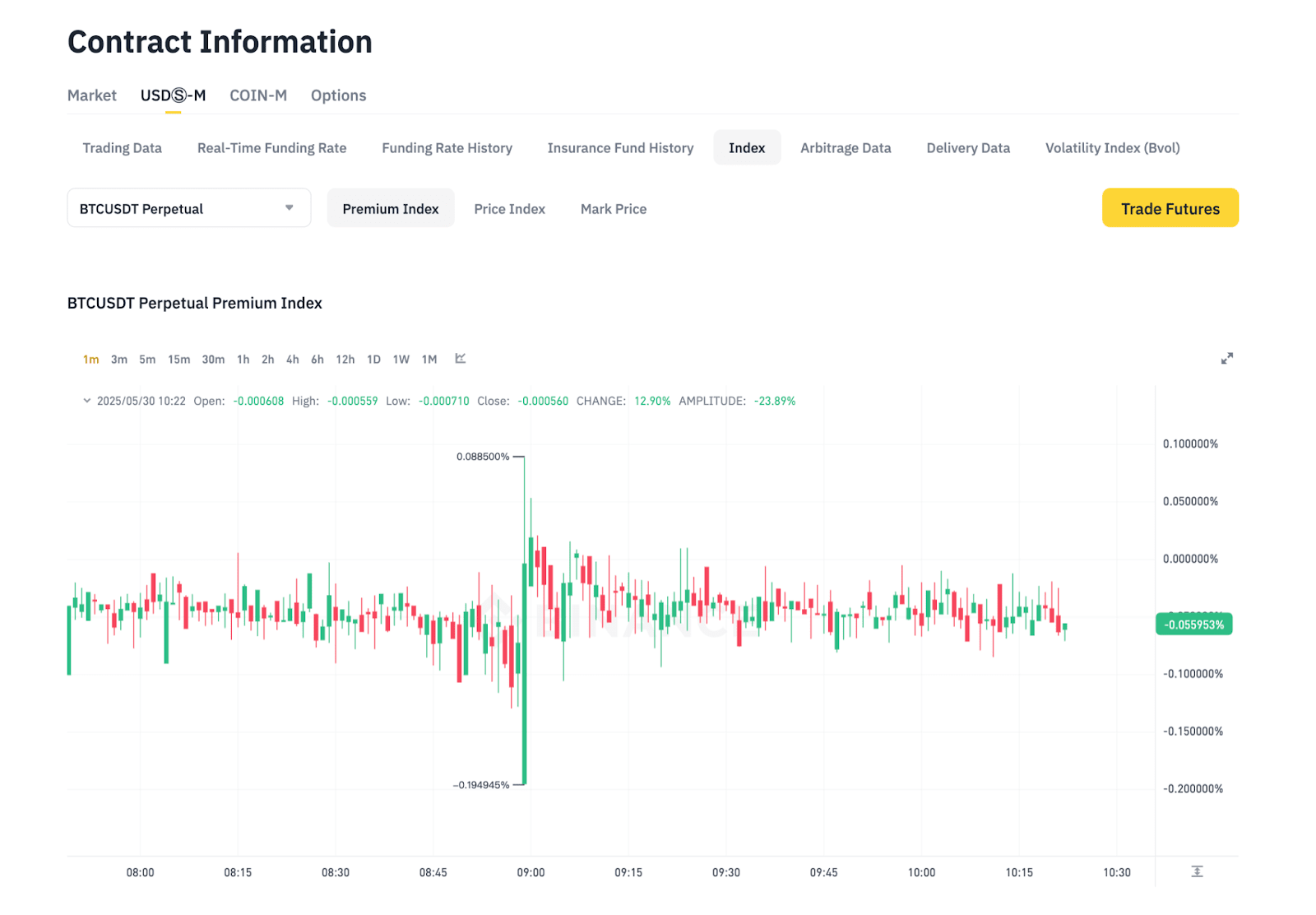

السعر العادل هو آلية تُستخدم في تداول عقود العملات الرقمية الآجلة لضمان تسعير العقود الآجلة على نحو عادل ودقيق.

أما مؤشر السعر فيُستخدم في الحد من المخاطر التي تنشأ من تقلبات الأسعار والتلاعب بالسوق من خلال تقديم نقطة مرجعية أكثر ثباتًا. وبدلًا من استخدام السعر الأخير للأصل، يضع مؤشر السعر في الحسبان سعر الأصل عبر عدة منصات تداول.

لمعرفة المزيد من المعلومات حول أوجه الاختلاف بين السعر العادل والسعر الأخير، يُرجى الرجوع إلى ما الفرق بين السعر الأخير والسعر العادل للعقود الآجلة؟

يتحدد السعر العادل لأحد العقود على منصة Binance للعقود الآجلة بناءً على عدة عوامل، من بينها السعر الأخير للعقد، وسلسلة العرض1 والطلب1 من قائمة الطلبات، ومُعدل التمويل، والمتوسط المُركّب للسعر الفوري للأصل على المنصات الكبرى لتداول العملات الرقمية.

يُستخدم مؤشر السعر لحساب السعر العادل وهو مبني على المتوسط المُرجّح للسعر الفوري للأصل عبر المنصات المتعددة لتداول العملات الرقمية.

يعد مؤشر السعر هو المكون الرئيسي للسعر العادل، ويمثل قيمة المتوسط المُرجح للأصل الأساسي عبر منصات التداول الفورية الرئيسية، مما يعكس القيمة السوقية العادلة للعقود الآجلة من خلال تجميع الأسعار للحد من مخاطر التقلب والتلاعب. يتم تحديث مؤشر السعر باستمرار لمراعاة أي تغييرات في السعر الفوري للأصل أو ترجيحات منصة التداول المُستخدمة في الحساب.

على منصة Binance (بينانس)، يتضمن مؤشر السعر لعقود USDⓈ-M الآجلة الأسعار من مجموعة كبيرة من منصات التداول مثل: Binance - KuCoin - OKX - HitBTC - Gate.io - MEXC - Coinbase - Kraken - Bitget - Bitfinex, Bybit - PancakeSwap (سلسلة BNB) - Uniswap (Ethereum) - Raydium (Solana) - Aster. السعر الأخير لعقود Binance الآجلة يُضاف أيضًا كأحد مكونات مؤشر السعر كما تحدده منصة Binance (بينانس) وفقًا لتقديرها الخاص من وقت لآخر.

اعتبارًا من 10-02-2025، ستكون مُكوّنات منصات PancakeSwap (سلسلة BNB)، وUniswap (Ethereum) وRaydium (Solana) متاحة في العقود المُدرجة من 10-02-2025 فصاعدًا، وتخضع للتوفر واستقرار تغذية الأسعار.

تحتفظ منصة Binance (بينانس) بالحق في تغيير مكونات مؤشر السعر من وقت لآخر دون إخطار.

يمكنك استعراض معلومات مؤشر السعر في الوقت الفعلي هنا.

مؤشر السعر = مجموع (نسبة الترجيح المئوية لمنصة التداول (أ) * السعر الفوري للرمز على منصة التداول (أ) + نسبة الترجيح المئوية لمنصة التداول (ب) * السعر الفوري للرمز على منصة التداول (ب) +...+ نسبة الترجيح المئوية لمنصة التداول (ن) * السعر الفوري للرمز على منصة التداول (ن))

حيث:

ملحوظة: في حالة تقلبات الأسعار الشديدة أو الانحراف الشديد عن مؤشر السعر، ستتخذ Binance (بينانس) تدابير حماية إضافية تشمل، على سبيل المثال لا الحصر، تغيير مكونات مؤشر السعر واستخدام متوسط سعر مكونات المؤشر متقلبة الأسعار.

تطبق Binance (بينانس) إجراءات حماية إضافية للحماية من ضعف أداء السوق أثناء تعطل منصات التداول الفورية أو مشكلات الاتصال:

على سبيل المثال، إذا كان متوسط سعر مؤشر BTCUSDT في منصة التداول (أ) هو 20,000 USDT وانحرف السعر بنسبة +7%، فسيتم تحديد الحد الأقصى عند 20,600 USDT (أي 20,000 * 1.03). وعلى العكس، إذا كان الانحراف -6%، فستكون قيمته المحسوبة 19,400 USDT (أي 20,000 * 0.97). وسيحدث هذا التعديل فورًا بعدما يتجاوز السعر الفوري حد انحراف السعر هذا. وسيُعاد تعديل قيمة السعر الذي تحسبه منصة التداول إلى قيمته الأصلية بمجرد تراجع قيمة السعر ضمن نطاق حد الانحراف البالغ 3% من متوسط سعر جميع مصادر الأسعار. غير أن هذه القاعدة لا تنطبق على بعض المؤشرات المحددة.

| الرمز | حد الانحراف |

| BNBUSDC | 1% |

| BNBUSDT | 1% |

| BTCUSDC | 1% |

| BTCUSDT | 1% |

| BTCUSD1 | 1% |

| ETHUSDC | 1% |

| ETHUSDT | 1% |

| SOLUSDT | 1% |

| USDCUSDT | 1% |

| XRPUSDT | 1% |

يمكنك الرجوع إلى أحدث مرجع لمنصة التداول حول مؤشر السعر للحصول على تحديثات في الوقت الفعلي.

ملحوظة:

يوفر السعر العادل تقديرًا أفضل للقيمة "الحقيقية" للعقد مقارنةً بأسعار العقود الآجلة الدائمة، حيث إنه أقل تقلبًا على المدى القصير. وتستخدم منصة Binance (بينانس) السعر العادل لتجنب عمليات التصفية غير الضرورية ومنع أصحاب النوايا السيئة من التلاعب بالسوق.

على منصة Binance للعقود الآجلة، يتم حساب السعر العادل لعقد ما بناءً على عدة عوامل، وتشمل هذه العوامل السعر الأخير للعقد الآجل، وسلاسل العرض1 والطلب1 من قائمة الطلبات، ومُعدل التمويل، والمتوسط المُركّب للسعر الفوري للأصل الأساسي على المنصات الكبرى لتداول العملات الرقمية.

يرتبط حساب السعر العادل ارتباطًا وثيقًا بمعدل التمويل، والعكس صحيح. ونظرًا لأن الأرباح والخسائر غير المحققة هي العامل الرئيسي في بدء عمليات التصفية، فمن الضروري أن يكون حسابها دقيقًا لمنع عمليات التصفية غير الضرورية. يمثل الأصل الأساسي للعقد الدائم القيمة "الحقيقية" للعقد، ويُعتبر مؤشر السعر – متوسط الأسعار من الأسواق الرئيسية – بمثابة المكون الأساسي للسعر العادل.

السعر العادل = متوسط (السعر 1، السعر 2، سعر العقد)

حيث:

على سبيل المثال، إذا تحددت فترة التمويل لتكون كل 8 ساعات وكان آخر رسم تمويل قد فُرض منذ ساعتين، فسيكون الوقت حتى التمويل القادم 6 ساعات.

ملحوظة: يتم تبادل رسوم التمويل بين أصحاب صفقات الشراء والبيع، حيث تعمل Binance (بينانس) كوسيط محايد في المعاملة.

المتوسط المتحرك (على أساس 30 ثانية) يُحسب كمتوسط 30 نقطة بيانات على مدى فترة 30 ثانية. تُحسب نقطة البيانات كل ثانية واحدة من خلال أخذ مُتوسط أسعار العرض والطلب ثم طرح مؤشر السعر.

المتوسط المتحرك (على أساس 30 ثانية) = مجموع [(Bid1_i + Ask1_i)/2 - PI_i] / 30

حيث:

يُرجى الرجوع إلى مؤشر السعر لكل عقد من عقود USDⓈ-M الآجلة لمزيد من التفاصيل.

إذا كان السعر 1 < السعر 2 < سعر العقد،، سيُستخدم السعر 2 بمثابة السعر العادل.

ملحوظة 1: يُرجى العلم أن السعر العادل قد ينحرف عن السعر الفوري خلال ظروف السوق المتطرفة أو الانحرافات في مصادر الأسعار. وفي مثل هذه الحالات، ستتخذ Binance (بينانس) إجراءات وقائية إضافية، مثل حساب السعر العادل = السعر 2.

ملحوظة 2: عندما يُظهر السعر العادل حركة كبيرة وسريعة بشكل غير طبيعي في أي اتجاه خلال فترة زمنية قصيرة، تحتفظ منصة Binance (بينانس) بالحق في وضع الرمز في وضع التقليل فقط للحفاظ على استقرار السوق وسلامة الأسعار.

أثناء ترقيات النظام أو فترات التوقف، عندما يتم إيقاف جميع أنشطة التداول مؤقتًا، سيواصل النظام احتساب السعر العادل باستخدام المعادلة القياسية. لكن سيتم تعيين المُتوسط المُتحرك (على أساس 30 ثانية) في السعر 2 إلى 0 حتى يعود النظام إلى وضعه الطبيعي.

المتوسط المتحرك (العرض1 + الطلب1) / 2 - مؤشر السعر)، تُحسب كل ثانية على مدار فترة 30 ثانية.

السعر العادل قبل 25-09-2020، الساعة 07:29:59 (UTC) = مؤشر السعر + المتوسط المتحرك (على أساس 30 ثانية)

السعر العادل في 25-09-2020، الساعة 07:30:00 - 07:59:59 (UTC) = متوسط مؤشر السعر، ويتم احتسابه كل ثانية بين 07:30:00 و07:59:59 (UTC) في يوم التسليم.

السعر العادل = متوسط أسعار التداول في آخر 10 ثوانٍ، يتم حسابه كل ثانية.

إذا كان هناك أقل من 21 سعرًا للمعاملات في فترة 10 ثوانٍ، فسيستند متوسط مؤشر السعر إلى أسعار آخر 20 معاملة.

سيتم تحويل العقود الآجلة الدائمة في فترة تداولات ما قبل السوق إلى عقود آجلة دائمة قياسية بمجرد التوصل إلى مؤشر سعر مستقر من سوق التداولات الفورية (وفقًا لتقدير منصة Binance (بينانس)). خلال فترة الانتقال، سينتقل السعر العادل تدريجيًا من السعر العادل لتداولات ما قبل السوق إلى حساب السعر العادل القياسي (السعر العادل = متوسط (السعر 1، السعر 2، سعر العقد)).

وظيفة التداول لن تتأثر أثناء فترة الانتقال، ولن يتم إلغاء الطلبات والصفقات المفتوحة.

السعر العادل = متوسط (السعر 1، السعر 2، سعر العقد)

يرجى الملاحظة: قد توجد اختلافات بين هذا المحتوى الأصلي باللغة الإنجليزية وأي نسخ مترجمة (قد تكون هذه النسخ من إنتاج الذكاء الاصطناعي). يُرجى الرجوع إلى النسخة الإنجليزية الأصلية للحصول على أدق المعلومات، في حال وجود أي اختلافات.