Summary

Markets rebounded as expectations for a December Fed rate cut surged from lows of ~30% to ~85%, pushing BTC back above US$90K and S&P 500 +2.8%.

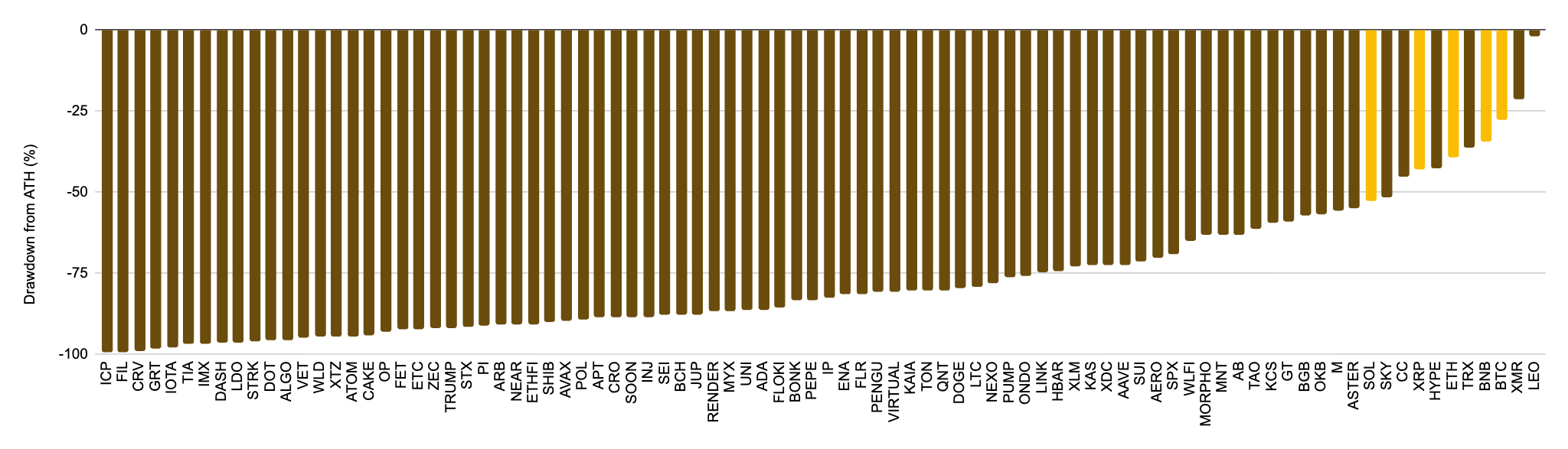

Altcoins recovered, though breadth remains uneven, with 79 of the top 100 tokens still more than 50% below their ATHs after several weeks of drawdowns.

The cycle’s key liquidity drivers (stablecoins, ETFs and DATs) have slowed in recent weeks, making renewed momentum important for broader capital rotation and sustained upside. Newly launched altcoin ETFs, however, have still recorded modest net positive inflows so far, now over US$1.3B.

The liquidity backdrop remains supportive, but near-term direction now hinges on the December FOMC decision and any developments around the next Fed chair, both of which will guide policy expectations into year-end.

Market Overview

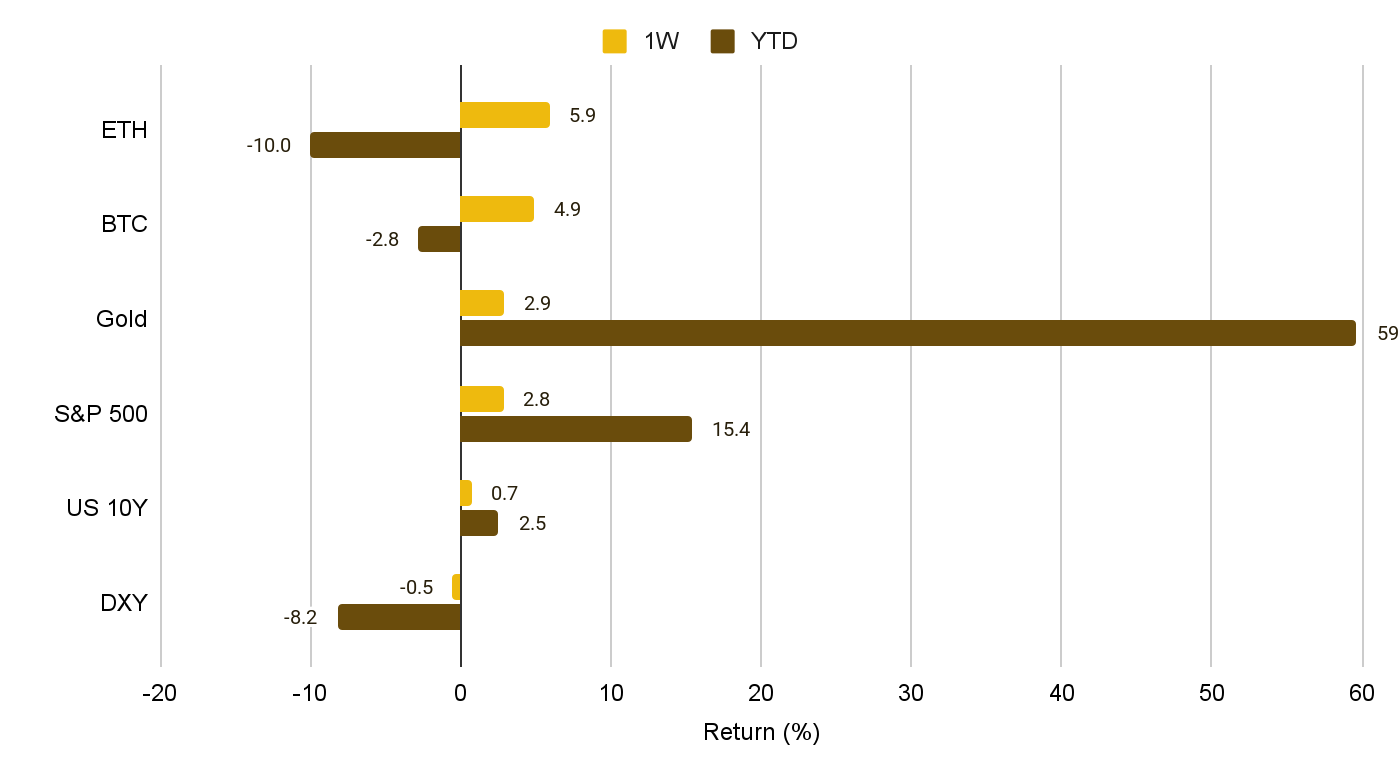

Markets rebounded this week as clearer macro signals emerged, driven by rising expectations of a Fed rate cut in the final FOMC meeting of the year. Rate-cut odds have climbed to ~85%, up from lows of 30% last week, and this shift has been reflected in a softer DXY and lower U.S. treasury yields. BTC moved back above US$90K, up 4.9% on the week, while the S&P 500 gained 2.8%. Although the rebound suggests markets have temporarily set aside concerns about an AI-driven bubble that weighed on risk assets earlier, the broader tone remains cautiously positive. Activity was limited, however, as volatility and volumes declined during a quiet U.S. market Thanksgiving-shortened trading week.

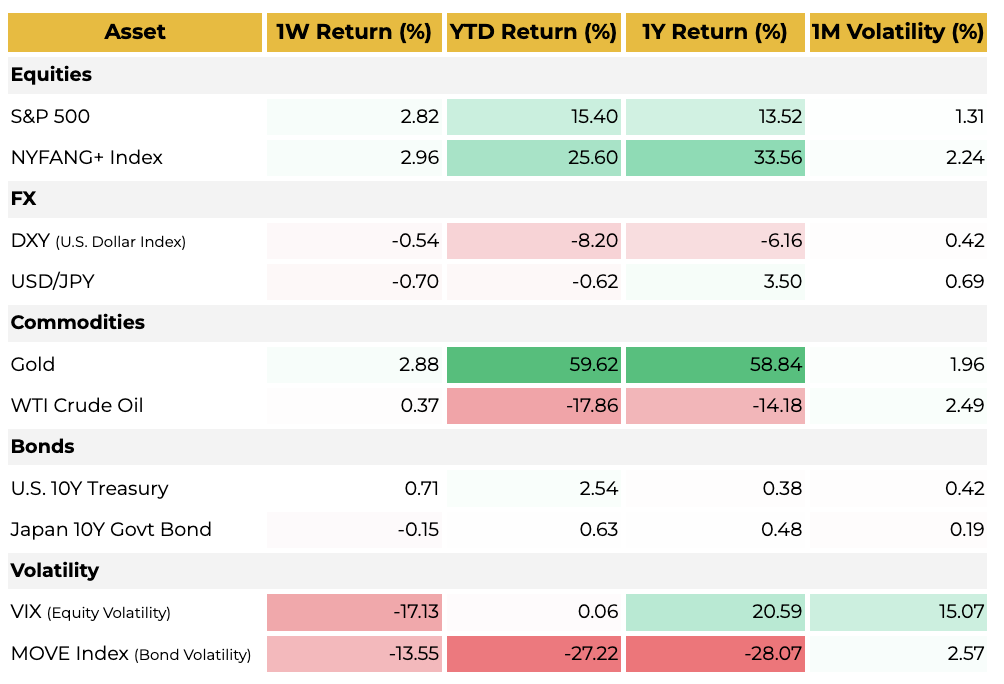

Figure 1: Weekly and YTD Performance – Crypto and Global Market Assets

As we enter the final month of 2025, markets are largely focused on the Fed policy direction. This includes any data influencing the 9 December decision and the next Fed chair nomination, which President Trump is anticipated to reveal before year-end. U.S. macroeconomic releases also resumed following the record 43-day government shutdown that ended in mid-November. While insight into current conditions remains limited, further indications of a softening labor market has pushed expectations firmly toward a rate cut.

1. Digital Assets

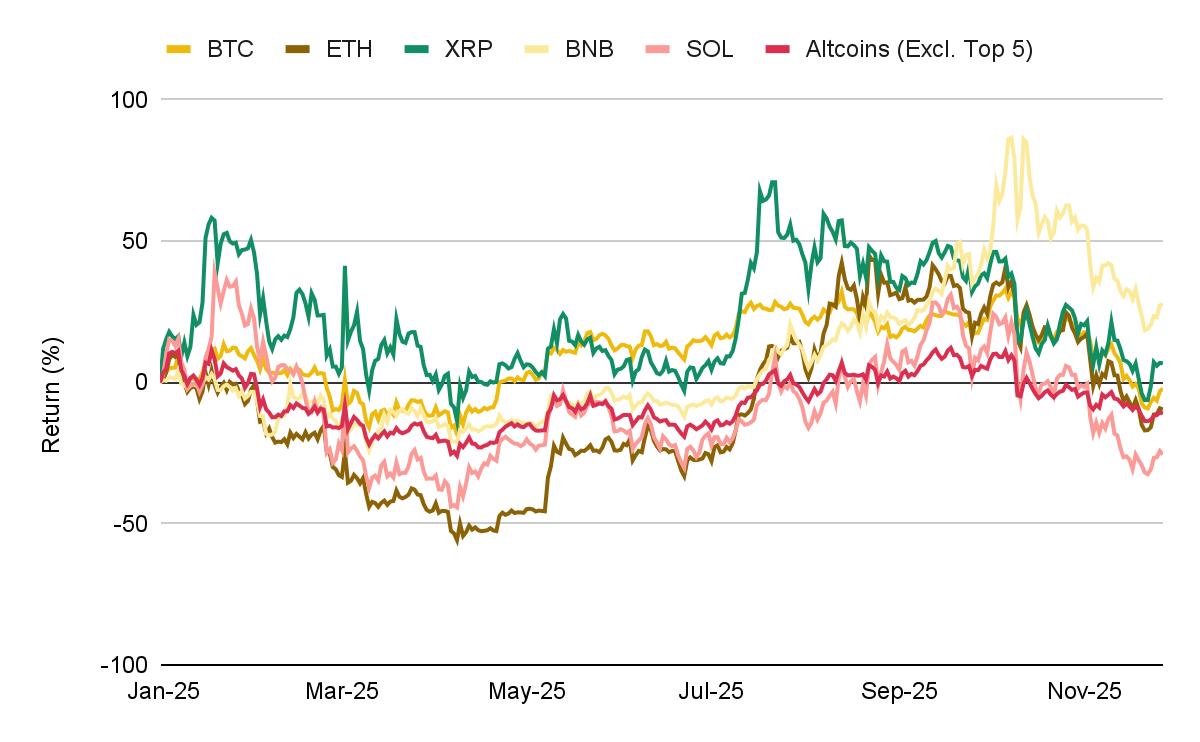

Digital assets recovered this week as selling pressures eased after several weeks of drawdowns, helped by markets shifting toward pricing in a December rate cut. Most assets gained at least 5%, although BTC and several majors (excluding BNB and XRP) remain negative on the year.

Figure 2: YTD Indexed Performance – Major Digital Assets

With markets posting a modest recovery this week, it is useful to contextualise where the broader crypto market stands this cycle. A look at the top 100 tokens shows that 79 are still more than 50% below their ATHs, which reflects how narrow this cycle’s rally has been. Despite several majors approaching or hitting new highs earlier in the year, most altcoins have not meaningfully participated.

Each correction in this cycle has also widened this dispersion: majors benefit from deeper liquidity and persistent inflows, while most altcoins lack a structural bid, causing every drawdown to push them further from prior highs. The segments that have recently held up comparatively better: Exchange/DEX tokens (benefiting from strong ecosystem support), DeFi (driven by growing token buybacks), and Privacy (supported by a rising on-chain narrative). This signals where capital is willing to remain allocated, even through volatility, into areas with clearer fundamentals and liquidity depth, rather than spreading broadly across older altcoins.

Figure 3: 79 out of the top 100 tokens are >50% below their ATHs

This pattern partly reflects how liquidity has behaved this cycle. Earlier in the year, when stablecoins, ETFs, and Digital Asset Treasury (DAT) issuance were expanding, those inflows were absorbed primarily by BTC and the majors. Rotation into the long tail never fully materialised before these channels began to slow, which left the rally concentrated at the top end. Many legacy tokens also still face past dilution or lack new catalysts, making it harder for them to capture momentum even when broader conditions are supportive.

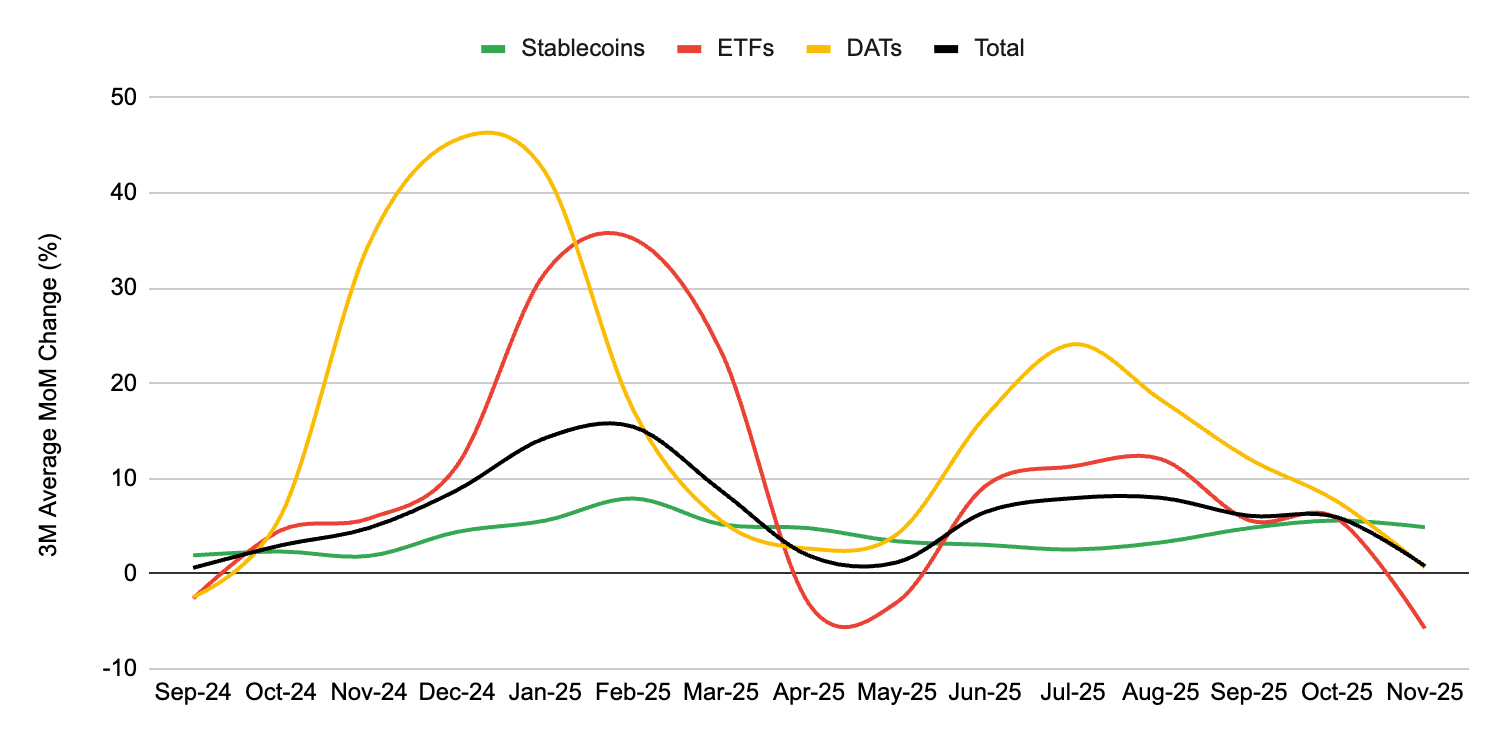

For the wider market to retrace more meaningfully, these liquidity channels would likely need both to re-accelerate and to rotate more broadly beyond majors. Stablecoin growth, ETF flows, and DAT issuance remain the clearest indicators of new capital entering the ecosystem, and all three have slowed in recent weeks. Each of these channels reflects a different source of liquidity: stablecoins capture crypto-native risk appetite, DATs reflect institutional yield demand, and ETFs signal broader TradFi allocation, underscoring why their combined momentum is important. Historically, when these indicators have picked up again, broader market strength has tended to follow. While the macro backdrop is becoming more supportive with expectations of a more dovish monetary policy path, liquidity is still favouring other expressions of risk, particularly equities, following recent volatility.

Figure 4: Market liquidity indicators across stablecoins, ETFs, and DATs have softened in recent months

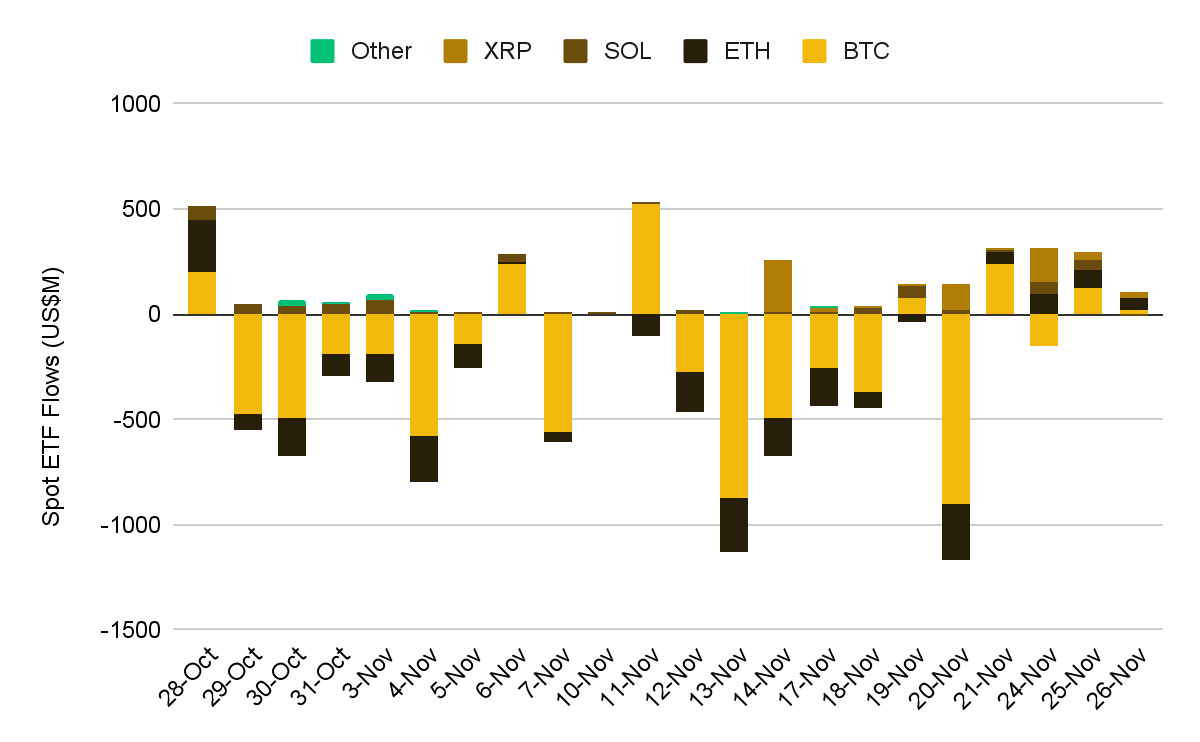

One theme that has remained active in recent weeks is altcoin ETF approvals (including SOL, XRP, LTC, DOGE, among others), many of which have seen consistent net positive flows since launch. It remains early, but with additional altcoin ETFs filed and awaiting approval, this trend is set to reshape altcoin trading by virtue of their extension to TradFi markets. As seen with ETH, the second spot ETF approved after BTC, markets may initially approach these products cautiously as access widens and early demand stabilises, before flows potentially strengthen over time.

Figure 5: Spot altcoin ETFs have posted steady net inflows since launch, surpassing US$1.3B to date, even through recent market drawdowns

2. Global Markets

Figure 6: Multi-Asset Performance – Equities, FX, Commodities, Bonds, Volatility

Equities:

Equities rebounded as sentiment improved and markets priced in higher odds of a Fed rate cut, with both the S&P 500 and the NYFANG+ Index rising near 3%.

FX:

The DXY fell modestly by 0.54%, reflecting softer labour data and growing market expectations of a December rate cut.

Commodities:

Gold extended its rally, rising by 2.88% on the week.

Bonds:

U.S. Treasuries gained on weaker macro data, including a soft ADP payrolls print and a decline in November consumer confidence.

Volatility:

Volatility declined sharply, supported by a calmer market tone and reduced activity during the U.S. Thanksgiving-shortened trading week.

3. Intermarket View

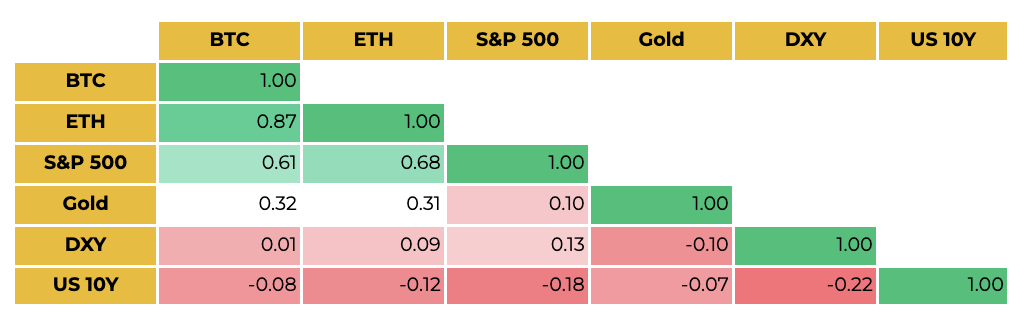

Although BTC and digital assets continue to trade broadly in line with risk assets, BTC’s 2-month correlation with equities has slipped slightly. At the same time, its correlation with gold has increased to 0.32, indicating a potential shift in market behaviour as the recent risk-off episode cools.

Figure 7: BTC 2M Correlation Matrix (vs ETH, S&P 500, Gold, DXY, US 10Y)

Macro Outlook: Rate-Cut Expectations Reprice Sharply

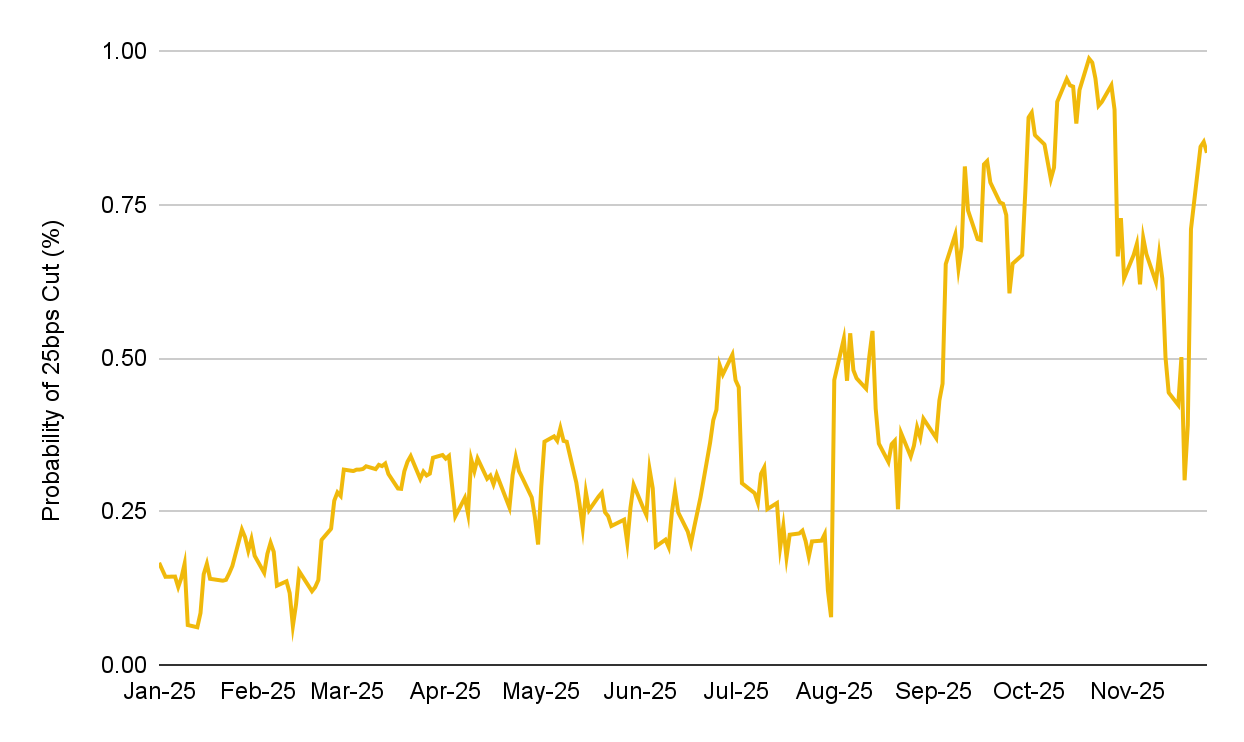

Markets significantly repriced Fed rate-cut expectations this week, with the probability of a December cut rising from lows of 30% to 84.7% following a series of inflation, labour-market, and consumer sentiment data releases.

September PPI data showed a moderation in both headline and core readings on a monthly and yearly basis. While headline PPI still came in higher than expectations on a YoY basis, the sharp shift in rate-cut odds suggests the market views the softening labour market as a more pressing concern than near-term inflation pressures.

Labour data reinforced this view: U.S. private employers cut 13,500 jobs per week in the four weeks to November 8, 2025, a notable increase from the earlier weekly decline of 2,500. Growth indicators also softened: U.S. retail sales rose just 0.2% in September, the smallest increase in four months. Meanwhile, consumer confidence weakened in November amid rising labour-market concerns. Expectations fell to their lowest since April, present-condition readings hit a more-than-one-year low, the share of consumers expecting income gains dropped to the lowest since February 2023, and sentiment around both current and future business conditions deteriorated.

According to CME FedWatch, markets now assign an ~85% probability of a 25 bps rate cut at the December FOMC meeting. This marks a new high, and a stark reversal from last week when odds briefly fell to around 30%.

Figure 8: Markets are now pricing in ~85% probability for a 25bps rate cut in December

Beyond the immediate rate decision, attention is increasingly shifting to the forthcoming Fed chair nomination. According to data from Polymarket, Kevin Hassett is reportedly the leading candidate to replace Jerome Powell when his term expires next May and is expected to broadly align with President Trump’s preference for lower interest rates. However, Trump’s personnel decisions can be unpredictable, so the nomination could still shift. Markets have historically responded positively after a nomination is announced and in the lead-up to appointment, though the reaction ultimately depends on how dovish the incoming chair is perceived to be and whether inflation remains persistent amid other policy uncertainties.

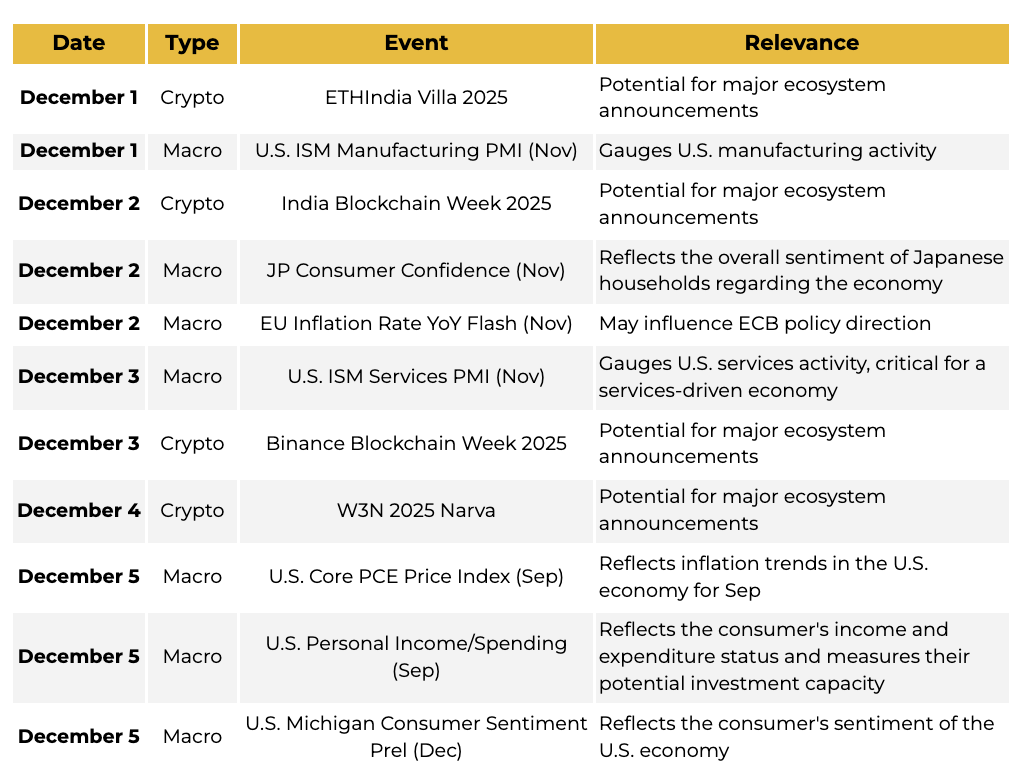

The Week Ahead

The key events this week centre on high-impact macro data that can shape policy expectations. U.S. ISM Manufacturing and Services PMIs, EU flash inflation, and Japan consumer confidence will provide an updated read on global activity and price trends. The most important release is Friday’s U.S. Core PCE, alongside personal income and spending, which will be closely watched for confirmation of cooling inflation and softening consumer strength.

Figure 9: Key Macro and Crypto Events for the Week of November 29 – December 5, 2025